After months of ‘higher for longer’ messaging, the latest labour figures point to a cooling yet still resilient jobs market. The delayed September non-farm payrolls report showed 119,000 jobs created, although the unemployment rate climbed to 4.4%, its highest level in four years. Revisions to the July and August readings suggested the broader trend is slowing.

The mixed outcome leaves the Federal Reserve treading a fine line: robust hiring in sectors such as healthcare and education sits alongside rising continuing claims.

This divergence is reinforcing the view that inflation is easing more quickly than employment conditions.

Traders Position For A December Cut

The FedWatch probabilities shifted dramatically last week. Markets now price in a 71% chance of a 25-basis-point cut at the 10 December FOMC meeting, up from just 39% the previous day. Looking ahead to January 2026, traders assign a 58% probability to an additional 25-bp cut, signalling growing confidence that the easing cycle will soon begin.

Lower bond yields have lifted equities and pressured the US dollar. The two-year Treasury yield fell towards 3.5%, while AI and technology stocks spearheaded the rally. Selling pressure in Bitcoin and Ethereum has also eased, mirroring the broader, mild “risk-on” shift fuelled by softer yields and rising expectations of a December rate cut.

Risk Appetite Returns

The S&P 500 bounced back after two consecutive weeks of declines, supported by dovish rate expectations and strong corporate earnings. More than 80% of the index’s constituents surpassed profit estimates, with technology and healthcare leading the outperformance.

Elsewhere, crude oil steadied after rebounding from the $57.60 support level, while gold remained firm near $4,000, buoyed by a softer US dollar.

Market Movements Of The Week

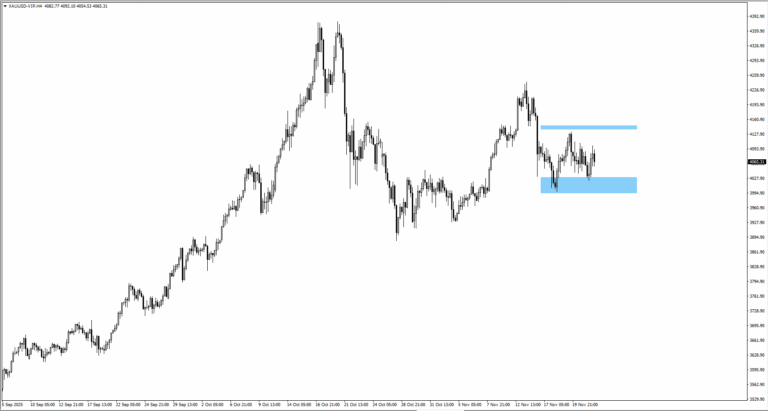

Gold (XAUUSD)

– Gold bounced from $4,020, continuing its range between $3,940 and $4,075.

– Softer yields and rising cut odds underpin support near $4,000.

– A break below $3,940 could expose $3,900, while resistance remains at $4,075.

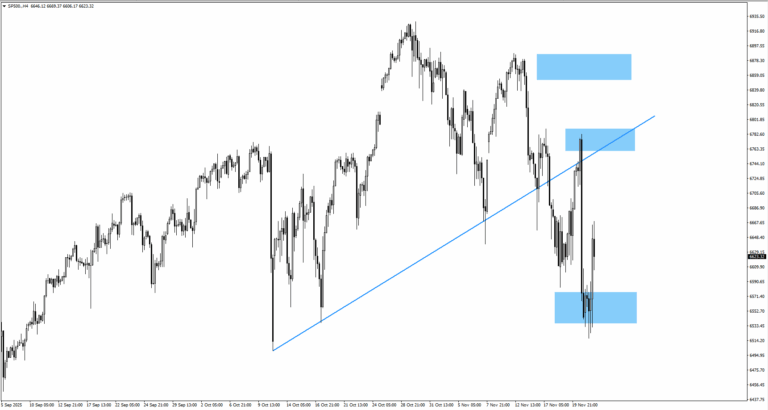

S&P 500 (SP500)

– Index rebounded as rate-cut optimism drove tech stocks higher.

– Traders watch 6,760 resistance for directional bias amid easing yields.

– Sustained buying above 6,700 could open the door to a year-end rally.

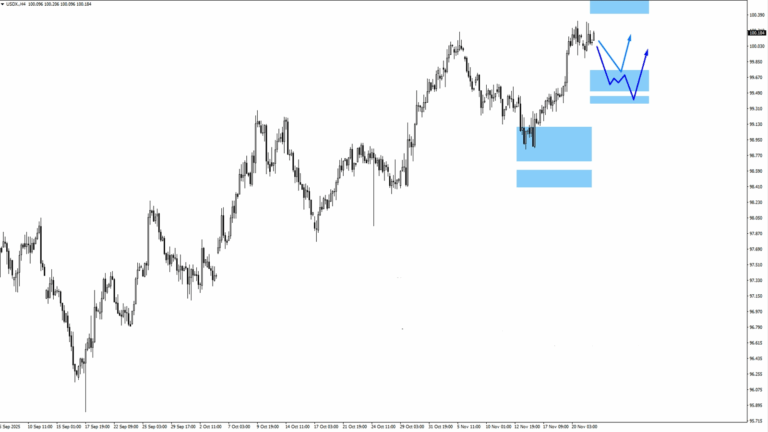

USD Index (USDX)

– USDX eased from its peak, testing the 99.65 zone for support.

– A bullish reversal could follow if the Fed tempers dovish expectations.

– Further downside to 99.45 remains possible if PCE cools sharply.

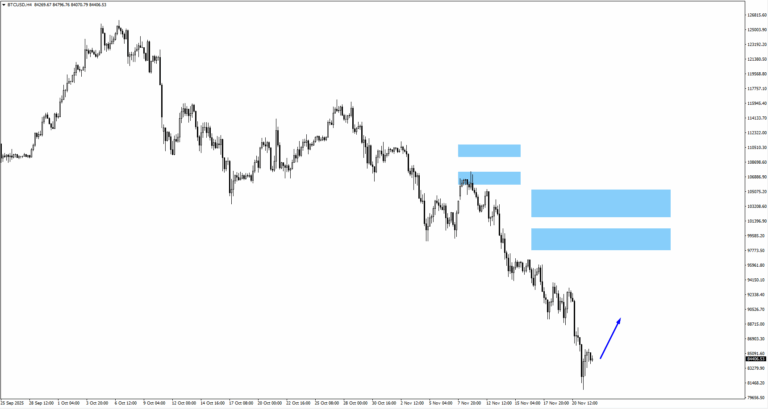

Bitcoin (BTCUSD)

– BTC tested $81,700, slipping amid risk rotation.

– Consolidation patterns suggest potential continuation of short-term weakness.

– Traders eye support near $80,000, with resistance around $84,000.

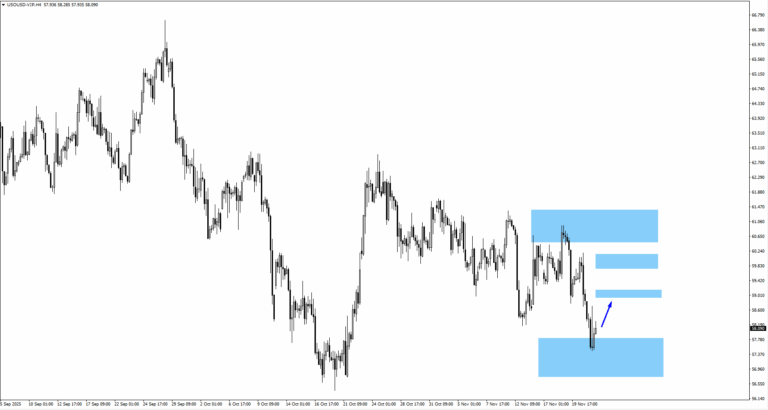

US Oil (USOIL)

– Crude rebounded from $57.60 toward $59.80, aided by improving sentiment.

– Resistance sits at $61.05, with potential pullback zones near $59.05.

– Market focus shifts to OPEC+ signals and global demand data.

Key Events This Week

25 November

1. US PPI m/m, Forecast: -0.10%, Previous: -0.10%

Soft data could weigh on USD sentiment.

26 November

1. NZ Official Cash Rate, Forecast: 2.25%, Previous: 2.50%

RBNZ expected to maintain cautious tone.

2. US Core PCE Price Index m/m, Forecast: 0.20%, Previous: 0.20%

Inflation gauge to steer FOMC expectations.

3. US Prelim GDP q/q, Forecast: 2.50%, Previous: 2.90%

Focus on growth momentum before FOMC.

28 November

1. CA GDP m/m, Forecast: 0.20%, Previous: -0.30%

Growth rebound may strengthen CAD ahead of December data.

Market Snapshot

The latest upswing across global markets is being driven less by new economic data and more by a shift in the Federal Reserve’s tone. Comments from John Williams suggesting that policy is only “modestly restrictive” have reopened the door to near-term easing, reigniting risk appetite across equities, gold, and cryptocurrencies.

With the odds of a December rate cut now at 71%, traders have begun repricing the policy trajectory into early 2026.

For the moment, the economic picture remains mixed. The US jobs market continues to create employment, yet the jobless rate has risen to 4.4% and unemployment claims have reached their highest since 2021. Inflation risks appear to be retreating faster than economic activity, giving the Fed room to edge towards a more neutral policy stance.

A December rate cut would simply confirm what markets have already priced in, though a pause accompanied by dovish language could still help sustain the improved risk sentiment.