For most of 2026, investors were working with a straightforward script. Inflation was expected to cool, growth was expected to slow, and the Federal Reserve was expected to eventually cut interest rates.

That script has now been torn up.

The April inflation data did not look like a minor blip. Headline CPI rose 3.8% year over year. It was the highest reading since May 2023, while core CPI climbed 0.4% month over month and 2.8% year over year. Energy was the main shock, with energy prices up 17.9% from a year earlier and petrol prices surging 28.4%.

This matters well beyond the cost of living. Inflation directly dictates how the Fed manages interest rates, and when it re-accelerates, the Fed has to defend its credibility. The April CPI report immediately forced investors to reassess the entire rate path.

Inflation Changed The Bond Market First

The first major reaction did not come from the Fed itself. It came from the bond market.

Following the CPI shock, the Producer Price Index added further pressure by recording its largest monthly gain since early 2022. That told investors inflation was not only appearing at the consumer level. It was building earlier in the supply chain as well.

Once both CPI and PPI pointed in the same direction, Treasury yields moved sharply higher. The 10-year Treasury yield climbed to around 4.54%, its highest level since May 2025, while the 30-year yield broke above 5% and the 2-year yield pushed past 4%.

Higher Treasury yields signal that markets are demanding greater compensation for inflation risk, and they carry a direct message for the Fed. Investors no longer believe the central bank can comfortably pivot toward rate cuts. The bond market was effectively pricing in a Fed that stays restrictive for longer.

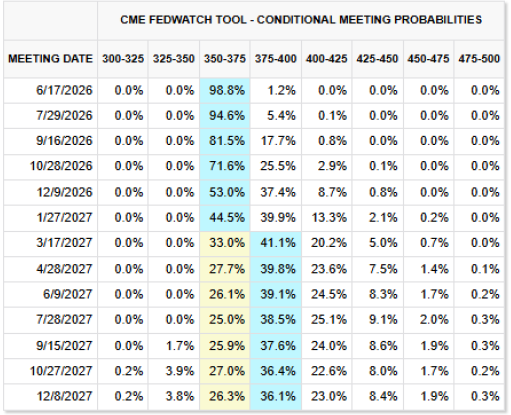

What the FedWatch Data Is Telling Us

That shift is also clearly visible in the CME FedWatch data, which tracks market expectations for Fed rate decisions at upcoming meetings.

For the 17 June 2026 meeting, the market is still largely expecting the Fed to hold rates steady. The probability of the Fed keeping the target range at 3.50% to 3.75% stands at 98.8%, with only a 1.2% chance of a hike to 3.75% to 4.00%. So a June hike is not the story, but what comes after is.

The CME conditional probability table tells a more revealing tale further down the calendar.

The probability of rates moving to 3.75% to 4.00% rises from 1.2% in June, to 5.4% in July, 16.9% in September, 24.2% in October, and 36.9% by December 2026.

Just one month ago, markets were debating when rate cuts would arrive. Now, they are beginning to price in the possibility that the next move is a hike instead. That is a significant macro shift.

When Fed Expectations Shift, Every Asset Has To Reprice

The breadth of the market reaction reflects just how central Fed expectations are to asset valuations.

If investors believe the Fed may hike again, the discount rate used to value financial assets rises. That hits long-duration assets hardest. Growth stocks, technology companies, AI names, and speculative equities all become more vulnerable because their valuations depend heavily on future earnings or future liquidity conditions.

That is why the Nasdaq 100 opened lower and the S&P 500 fell in tandem. The market was not reacting to a single inflation print. It was reacting to the possibility that the Fed’s entire policy direction had changed.

The same logic drove the sell-off in metals. Gold fell 2.7%, silver dropped nearly 8%, and copper declined 4.2% as the rate hike narrative took hold. Gold can benefit from geopolitical uncertainty, but when bond yields rise sharply, holding a non-yielding asset like gold becomes comparatively less attractive.

Crypto was hit by the same mechanism. Bitcoin fell towards $76,100, whilst crypto-linked equities, including Coinbase, Circle, and Strategy, dropped between 5% and 7%.

This is a reminder that crypto remains highly sensitive to liquidity conditions. When markets expect easier policy, crypto can rally strongly. When tighter policy gets priced in, it becomes one of the first assets to sell off.

Warsh Inherits The Problem At The Worst Possible Time

This inflation shock also carries political weight because Kevin Warsh is preparing to take over the Federal Reserve as Powell’s term comes to an end.

That timing is genuinely difficult. A new Fed chair typically wants to shape market expectations quickly and clearly, but the data has made that harder. With CPI re-accelerating, PPI rising, energy prices surging, Treasury yields climbing, and real wages slipping, it is difficult to argue for lower rates without putting the Fed’s credibility at risk.

The Fed now finds itself trapped between two uncomfortable outcomes.

Sound too dovish, and markets may conclude the Fed is tolerating inflation, pushing bond yields even higher. Sound too hawkish, and equities, commodities, and crypto face another round of selling pressure. Warsh steps into a role where there is no easy move on the board.

There Is Still One Reason Not To Panic

Before drawing firm conclusions, there is one mitigating factor worth considering.

Part of the April inflation spike may not be permanent. The shelter category appears to have been affected by a data collection issue linked to the October 2025 government shutdown, which distorted rental inflation figures. Some of the April increase may therefore reflect a delayed statistical correction rather than a genuine re-acceleration in underlying inflation.

If shelter inflation cools again over the coming months, the April core CPI reading may look considerably less alarming in hindsight.

However, the Fed cannot act on that possibility alone. It needs the evidence. Until inflation data begins to cool again, the central bank has very little room to sound dovish without risking a further loss of market confidence.

The Real Question Now

The entire market is now orbiting one central question:

Was April’s inflation reading a one-month shock driven by energy prices and data distortions, or is it the opening chapter of a second inflation wave?

If it proves temporary, the Fed can hold rates steady and gradually return to a more balanced policy stance. That outcome would ease pressure on bond yields and offer support to equities, gold, and crypto.

If inflation remains sticky, the Fed may need to keep rates higher for longer, or seriously consider another hike later in 2026. That scenario would strengthen the dollar, weigh on risk assets, and keep investors firmly in defensive mode.

This is why Fed rate management has become the defining macro story of the moment. The Fed is no longer simply managing expectations around rate cuts. It is now managing the risk that inflation has returned before the economy is ready to withstand another tightening cycle.

And every trader should be watching that story closely.