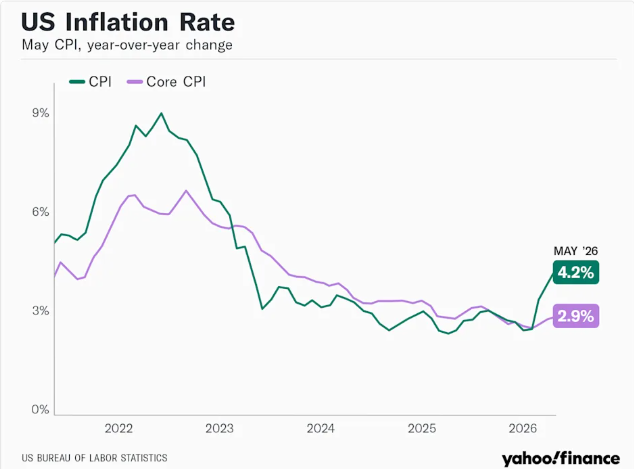

The latest US inflation report landed with a thud. Headline CPI rose to 4.2% year on year in May, up from 3.8% in April. It’s the hottest inflation reading in roughly three years and a clear sign that price pressures are moving further away from the Federal Reserve’s 2% target.

What makes this report particularly concerning is not just the number itself, but the trajectory behind it. In February, inflation stood at 2.4%. By March it had climbed to 3.3%, then 3.8% in April, and now 4.2% in May.

That is not a blip. It is an acceleration, and markets are being forced to reckon with what it means for interest rates, risk assets, and the broader economic outlook.

Headline CPI Came In Hot

For much of this year, investors were holding onto the hope that inflation was on a gradual downward path. That narrative has now taken a serious hit.

A headline CPI reading of 4.2% year on year is not simply above target. It represents inflation moving in the wrong direction at an uncomfortable pace. With each successive monthly report pushing the number higher, it becomes increasingly difficult to argue that the Fed has the conditions it needs to loosen policy.

When inflation is accelerating away from target, rate cuts become a harder case to make, regardless of how much investors might want them.

For traders, this is the critical context. The May CPI report does not just raise questions about June’s Fed meeting. It reshapes the entire outlook for the rest of 2026.

Core CPI Cooled, So The Report Was Not Uniformly Bad

Before drawing sweeping conclusions, it is worth understanding what the report actually showed beneath the headline number.

There is an important distinction between headline CPI and core CPI. Headline inflation captures the full basket of consumer prices, including food and energy. Core CPI strips those out to give a cleaner read on underlying price pressures across the broader economy. In May, that distinction made a meaningful difference.

Core inflation rose 2.9% year on year and just 0.2% month on month, a relatively contained reading that suggests the latest inflation shock is not yet spreading broadly across the economy. The Fed will take note of that.

If core inflation is stable or cooling, the central bank may not feel compelled to react as forcefully as it would if every component of the price basket were accelerating simultaneously. However, the Fed cannot simply look past a headline reading of 4.2%.

Energy costs feed through into transport, logistics, production, and business input costs. If they remain elevated long enough, they will eventually bleed into the wider economy. The report gives the Fed some nuance to work with, but not nearly enough comfort to justify cutting rates in the near term.

Energy Is The Main Inflation Problem

The primary driver of May’s headline inflation jump is unambiguous. Energy prices are surging, and geopolitics is at the heart of it.

The resumption of the Iran conflict has introduced fresh uncertainty around global oil supply. Markets do not need a full-scale escalation to keep energy prices elevated. They only need enough uncertainty to keep supply flows restricted and traders on edge.

As long as that uncertainty persists, oil prices are likely to remain high, and headline inflation will reflect that.

The knock-on effects extend well beyond petrol prices at the pump.

Higher oil costs raise shipping and transport expenses, push up production costs for manufacturers, and increase input costs across virtually every sector of the economy. Over time, businesses absorb only so much before they begin passing those costs on to consumers.

That is the deeper risk the May report is signalling. The immediate problem is the energy-driven spike in headline inflation. The bigger concern is that today’s energy shock quietly becomes tomorrow’s broad-based inflation problem.

By which point, it becomes significantly harder for the Fed to respond without risking a sharp tightening of financial conditions.

Trump Says Inflation Could Fall If The War Ends

The inflation outlook is now directly entangled with geopolitical developments, and that has introduced a new layer of uncertainty into the Fed’s calculus.

President Trump has argued that inflation could fall sharply once the Iran conflict is resolved. His logic is straightforward. If the war ends, energy flows normalise, oil prices come down, and the headline inflation shock fades. It is a plausible scenario, and markets are not dismissing it outright.

However, there is a significant gap between a plausible scenario and a reliable forecast, and investors are understandably reluctant to price in a resolution that has not yet materialised.

For now, the war continues, oil flows remain restricted, and the inflation data reflects that reality. If a credible peace deal emerges and energy prices fall quickly in response, the outlook could shift considerably.

Until then, the Fed is dealing with a headline inflation rate that is accelerating, and it has to set policy based on the data it has, not the data it hopes to see. That leaves very little room to ease, even if the energy shock eventually proves temporary.

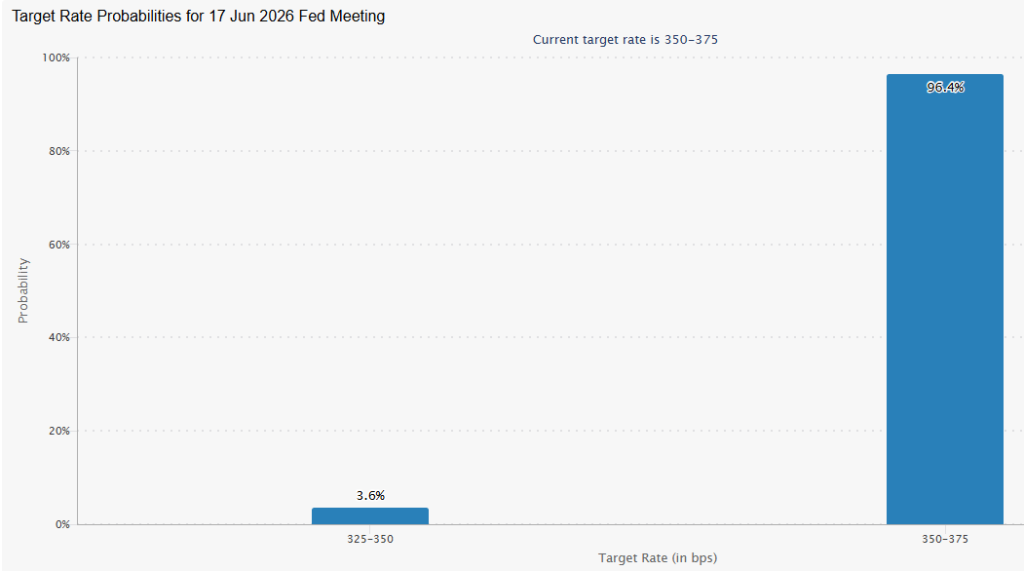

The CME FedWatch Picture: No Cut In June

The market has moved swiftly to reprice the Fed outlook in the wake of the May CPI report, and the CME FedWatch probabilities tell the story clearly.

For the 17 June meeting, there is a 96.4% probability that the Fed leaves rates unchanged. With headline inflation running at 4.2% and the labour market still described as resilient, there is simply no credible basis for a cut at this stage. That outcome is essentially fully priced. There is no suspense around June.

July Expectations Show A Small But Notable Hike Risk

The July meeting, scheduled for 29 July, is where the data-watching becomes more interesting. Markets are still leaning heavily toward no change, with an 84.3% probability that the Fed holds rates steady. However, the probability of a rate cut has fallen to just 3.3%, while the probability of a rate hike has climbed to 12.3%.

That asymmetry deserves attention. The hike probability is not the base case, and markets are not forecasting an imminent tightening move. But the fact that the probability of a hike now exceeds the probability of a cut is itself a significant shift in sentiment.

It reflects a market that is no longer just debating the timing of rate cuts. It is now seriously entertaining the possibility that the next move could be upward if inflation continues on its current trajectory. For traders positioned around a rate-cutting cycle, that is a meaningful change in the macro backdrop.

Year-End Pricing Points To Higher For Longer

Zoom out to the end of 2026, and the FedWatch data becomes even more instructive. By December, markets are pricing a 68% probability that interest rates will be higher than they are today, a 30.8% chance that rates stay the same, and just a 1.2% probability that rates end the year lower.

That is a striking reversal from where market expectations stood just a few months ago, when rate cuts were the dominant narrative and investors were debating whether the Fed would cut two or three times before year-end.

The base case has now flipped. The market is no longer asking when cuts will arrive. It is asking whether the Fed may need to tighten further before this inflation episode is truly resolved.

For equity markets, this matters enormously.

Higher-for-longer rates reduce the liquidity support that has underpinned valuations, raise borrowing costs for businesses and consumers alike, and compress the multiples investors are willing to pay for future earnings. Tech-heavy indices and growth-oriented sectors are particularly exposed, given how sensitive their valuations are to the interest rate environment.

Why Strong Jobs Data Can Be Bad For Markets

One of the more counterintuitive dynamics of the current environment is the way markets have been responding to strong economic data.

Under normal circumstances, strong jobs data would be welcomed as a sign of economic health. However, in the current environment, a robust labour market actually reduces the Fed’s incentive to cut rates.

As a result, a strong payrolls number can push stocks lower, because investors read it as confirmation that the Fed has no reason to loosen policy any time soon.

The inverse is also true.

A weak jobs report can sometimes lift markets, not because bad economic news is inherently positive, but because it signals that the Fed may finally have the justification it needs to begin easing. It may seem paradoxical, but it reflects the dual mandate the Fed operates under: stable prices and maximum employment.

Right now, inflation is well above target, and employment remains broadly healthy. That combination gives the Fed very little reason to move. Until one of those conditions changes materially, markets are likely to remain in a holding pattern where higher-for-longer rates continue to weigh on sentiment.

Warsh’s Real Test May Come After The War

For incoming Fed Chair Kevin Warsh, the May CPI report provides a defensible reason to keep rates on hold. Headline inflation is running well above target, energy prices remain volatile, and the labour market has not softened enough to justify an immediate pivot toward easing.

Holding rates steady in this environment is the straightforward call, and even politically, Trump may be willing to tolerate a pause while the war continues to distort energy prices and inflation expectations.

The real pressure on Warsh, however, is likely to build once the conflict ends. Trump has been explicit about his expectation that inflation should fall quickly once energy flows normalise. If and when that happens, the political case for rate cuts will intensify sharply. That is where Warsh’s credibility as Fed chair will genuinely be tested.

If inflation cools quickly and decisively after the war ends, the path forward is relatively clean. But if core inflation proves sticky, or if the energy shock has already fed through into broader price pressures, the Fed may still be reluctant to cut rates even after the geopolitical situation resolves.

That puts Warsh in a genuinely difficult position. He will be caught between mounting political pressure for lower rates and the institutional obligation to maintain the Fed’s inflation-fighting credibility.

The stakes extend beyond domestic monetary policy. If markets come to believe the Fed is cutting rates in response to political pressure rather than because inflation is genuinely under control, confidence in the dollar could weaken materially.

The credibility of the Federal Reserve and the strength of the US dollar are closely linked, and any perception that the former is being compromised will be felt quickly in the latter.