On 28 February 2026, the United States and Israel launched a coordinated military strike on Iran. Codenamed Operation Epic Fury,the world hasn’t been the same since.

The goals of the US forces are clear: 1. Put an end to Iran’s uranium-enrichment programme. 2. Destroy Iran’s missile production and air-defence systems. 3. Minimise the reach of Iran-backed militias that had been harassing US forces, allies, and commercial shipping across the region.

Iran, on the other hand, didn’t stand down. It retaliated with waves of ballistic missiles and drones targeting US military bases, Gulf infrastructure, and oil depots. Iran also capitalised its leverage by closing the Strait of Hormuz, the narrow waterway through which roughly 20% of the world’s oil supply flows every single day.

Brent crude jumped more than 8.5% on the first trading session after the strikes, surging to $75 a barrel. That was just the opening act. Prices peaked at nearly $120 a barrel before settling closer to $90 as markets tried to price in the chaos.

By mid-March, Brent was sitting at $106 a barrel, more than 40% above where it was just days before the first strike.

For investors and traders, this wasn’t just a geopolitical headline. It was a live stress test of how fast energy markets can reprice risk when a single conflict threatens a chokepoint that keeps the global economy breathing.

And here’s the uncomfortable truth. This has happened before. Different countries, different decades, but the same brutal playbook. Understanding those past crises isn’t just a history lesson. It’s a blueprint for what tends to happen next.

Energy Crisis Déjà Vu: The Oil Shocks That Shaped Modern Markets

1. The 1973 Oil Embargo: When Politics Turned Off The Tap

The spark was the Yom Kippur War. In October 1973, Egypt and Syria launched a surprise attack on Israel. The US backed Israel with military aid, and Arab members of OPEC hit back the only way they could by cutting off oil.

The embargo targeted the US, Western Europe, and Japan, choking the supply lines that powered the world’s biggest economies almost overnight.

The price impact was staggering. Oil quadrupled in a matter of months, from around $3 a barrel to nearly $12.

What followed was a painful stretch of stagflation that central banks hate most, plus fuel rationing, long queues at petrol stations and a global recession that reshaped how governments thought about energy security forever.

Impact Of The Crisis On Inflation And Central Bank Policy

The inflation aftermath of the crisis hit heavy and hard. US inflation went beyond 12% in 1974, up from 3.4% in 1972. The Americans obviously had an easy target to blame: skyrocketing gas prices, and they weren’t wrong.

Oil doesn’t just power cars. It flows through almost every part of an economy. When the price of energy spikes, the cost of making things, moving things and growing food spikes with CPI.

The Fed’s reaction in the middle of this oil crisis is an interesting chapter in its history. Rate hikes were the Fed’s preferred inflation-mitigation strategy in the heating economy between 1972 and 1973.

However, the FOMC reversed course in October 1973 and began to cut rates despite persistent inflationary pressures. In the Fed’s view, the oil shock was a demand-side headache rather than supply-side complications. By March 1974, the Fed made a U-turn and resumed rate hikes, but the damage was done.

The initial easing was premature before inflation had been fully contained, leading to the infamous stagflation era. It wasn’t until Paul Volcker took the helm in 1979 and pushed rates to 19% that the inflationary cycle was finally broken, triggering a deep recession.

2. The 1979 Oil Crisis: The Fall Of Shah

Long before the current conflict, Iran was already at the centre of an energy crisis. The 1979 Islamic Revolution toppled the Shah. Iran’s oil production effectively collapsed in the chaos that followed.

Then came the Iran–Iraq War in 1980, which tightened global supply even further, sending an already rattled market into a second wave of panic.

Prices surged to levels that, adjusted for inflation, rivalled anything seen before. The damage compounded inflation already burning through Western economies from the first shock.

Impact Of The Crisis On Inflation And Central Bank Policy

Unlike the 1973 crisis, US inflation had been boiling for years, even before the revolutionary cry echoed throughout Tehran. The Iranian Revolution played a role in turning up the heat to a level nobody was prepared for.

The inflation rate skyrocketed from 1% in 1965 to a staggering 13% by 1980. Adding heat to the economic crisis was unemployment, which climbed steadily to 9.7% by 1982. The potent mix of surging prices and spiralling joblessness became the defining economic scar of an entire generation.

It’s impossible to recount the economic upheaval of the late 70s and early 80s without mentioning Paul Volcker. Volcker took the reins of the Fed chairman in August 1979 and immediately got to work battling unanchored inflation.

Volcker guided the Fed in raising the federal funds rate from 11% when he took office to a peak of 19% in 1981, successfully lowering twelve-month inflation from a peak of nearly 15% to 4% by the end of 1982.

The restrictive anti-inflation policies of Volcker’s Fed laid off workforce in numbers that rivalled the Great Depression-era unemployment. A brief recession gripped the US from 1980 to 1983 as the full impact of monetary contraction unfolded.

3. The 1990 Gulf War Shock: Kuwait In Iraq’s Crosshair

On 2 August 1990, Iraq invaded Kuwait and wiped a significant chunk of global oil supply off the map almost instantly. International sanctions followed, and the combined loss of Iraqi and Kuwaiti exports sent oil prices from roughly $17 a barrel to over $40 in just a few months, a spike of more than 130% at its peak.

The crunch didn’t last.

Once the US-led coalition expelled Iraqi forces in early 1991, supply fears eased, and prices retreated relatively quickly. The episode reinforced a lesson markets keep relearning. The Middle East doesn’t have to be the source of a supply cut for a long time. The threat alone is enough to move prices violently.

Impact Of The Crisis On Inflation And Central Bank Policy

Interestingly, the US enjoyed a period of economic growth during the Reagan Era before the Gulf War unravelled the prosperity. Although the Gulf War recession lasted eight months, it significantly impacted the economy.

The surging oil prices pushed the overall inflation rate in the US to a high of 6.3% between October 1989 and October 1990. The uncertainty surrounding the war negatively impacted business investments and financial markets.

The Fed, under the leadership of Alan Greenspan, raised the borrowing costs a couple of times between 1988 and 1989, with a peak of 10% in 1989. Greenspan reacted to the Gulf War recession by lowering interest rates from 8% in 1990 to 3% in 1992.

4. The 2000s Price Surge: A Slow Burn To $147

This one didn’t start with a war or an embargo. It built slowly, fuelled by demand from emerging markets, years of under-investment in new production, and reduced OPEC spare capacity. Disrupted Iraqi production from the Iraq war and Venezuelan unrest catalysed the crisis.

It peaked at a nominal record of nearly $147 a barrel in July 2008 from the low of $28 in early 2003. At the time, it felt like it might never come down. Then the global financial crisis hit, demand collapsed, and oil crashed below $40 within months.

It was a brutal reminder that supply shocks and demand destruction are two sides of the same coin. Extreme price spikes rarely sustain themselves without taking the broader economy down with them.

Impact Of The Crisis On Inflation And Central Bank Policy

A dilemma from the 2000s oil surge that deserves recounting is the gap between headline and core inflation. As oil climbed steadily through the decade, it dragged the headline CPI with it. Oil prices contributed to US inflation averaging 3.3% in 2005 – 2006, which was above the 2.5% average of the preceding decade.

The 12-month change in the overall CPI rose from around 2% in October 2007 to just over 4% by February 2008, while core inflation stayed tame. That split between an elevated headline CPI due to energy prices and a stable core reading is a defining pattern across major oil shocks.

The Fed’s policy path through this period was essentially a tale of two phases. The Fed steadily raised interest rates to curb inflation as oil prices climbed through 2005 and 2006. Then, as the financial crisis erupted beneath the surface of an oil-stressed economy, the Fed pivoted hard and fast.

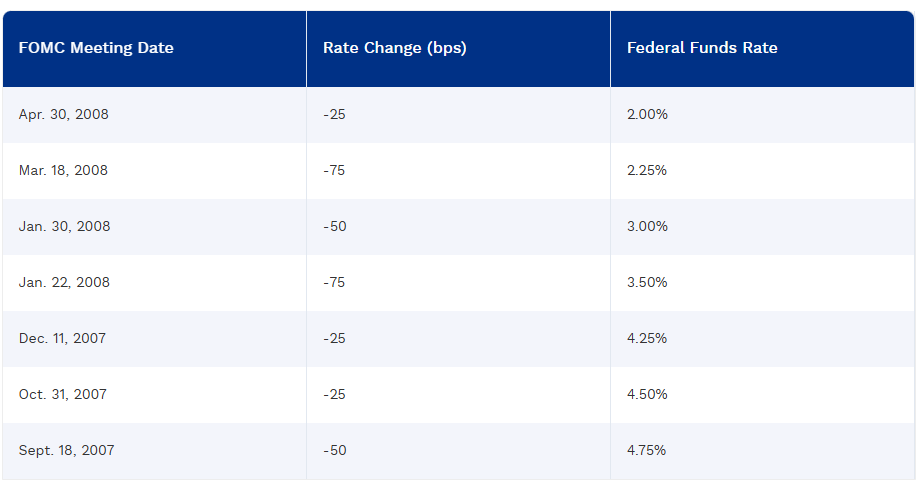

The Fed began cutting the federal funds rate aggressively from September 2007 until spring 2008 by 325 basis points, making it one of the most rapid and proactive policy responses in historical comparison.

That wasn’t the end of it.

When the crisis deepened, the Fed, in coordination with the European Central Bank, the Bank of England, and other major central banks, slashed rates by 50 basis points, with the Fed eventually lowering its target rate to 1.5%. The Fed then launched quantitative easing to keep the financial system from seizing up entirely.

5. The 2020 Oil Price Crash: When Demand Simply Disappeared

This one was unlike anything markets had seen before. When COVID-19 lockdowns swept across the globe in early 2020, entire economies essentially stopped moving. No commutes, no flights, no freight. Demand for oil fell off a cliff almost overnight.

At the same time, Saudi Arabia and Russia picked that precise moment to fall out over production cuts, flooding an already drowning market with even more supply. It was a perfect storm of the worst kind.

The result was historic. In April 2020, the US crude benchmark WTI didn’t just fall. It briefly went negative, dropping to around -$37 a barrel.

Traders were essentially paying people to take oil off their hands because storage was full and there was nowhere left to put it. For context, oil had been trading above $60 just weeks earlier.

Impact Of The Crisis On Inflation And Central Bank Policy

The 2020 oil crash flipped the inflation script. Unlike other crises in this article, this episode raised the alarm about prices plunging like a stone. This round, the risk isn’t inflation. It’s deflation.

In May 2020, the official CPI recorded a negative reading as collapsing energy and transportation costs dragged the broader price lower.

For investors and traders, 2020 was a masterclass in subverted expectations. It’s a demand-driven energy crash that threatens to pull prices dangerously close to zero.

As businesses closed and the US economy was on the brink of a recession, the Fed took drastic measures to rescue Americans’ households and businesses.

On 15 March 2020, the Fed slashed its benchmark interest rate to a range of 0% to 0.25%. In retrospect, it was a rare moment when then-President Trump showered praise on Powell, the Fed chair at the time.

On top of the major slash, the Fed announced a new round of quantitative easing, committing to purchase at least $500 billion in Treasuries and $200 billion in mortgage-backed securities over the coming months.

The Fed also eliminated reserve requirements for banks, slashed the discount window rate, and encouraged banks to use liquidity facilities.

6. The 2021–2023 Global Energy Crisis: The Rebound Nobody Was Ready For

When the world reopened after the pandemic, it needed energy fast. The problem was that years of underinvestment in fossil fuel production, combined with a rushed energy transition in parts of Europe, meant that supply simply couldn’t keep up with the pace of the recovery.

Natural gas inventories across Europe entered winter 2021 dangerously low. Electricity prices surged to record highs, and energy bills for households and businesses became a serious political issue across multiple continents.

Then came Russia’s invasion of Ukraine in February 2022, which poured fuel on an already burning fire. Europe, which had spent decades making itself heavily dependent on Russian gas, suddenly had to scramble for alternatives.

The episode forced governments to make uncomfortable decisions fast. Rationing, emergency imports of LNG, rushed renewables rollouts, and in some cases, restarting coal plants they had only recently closed. The IEA described it as the first truly global energy crisis.

Impact Of The Crisis On Inflation And Central Bank Policy

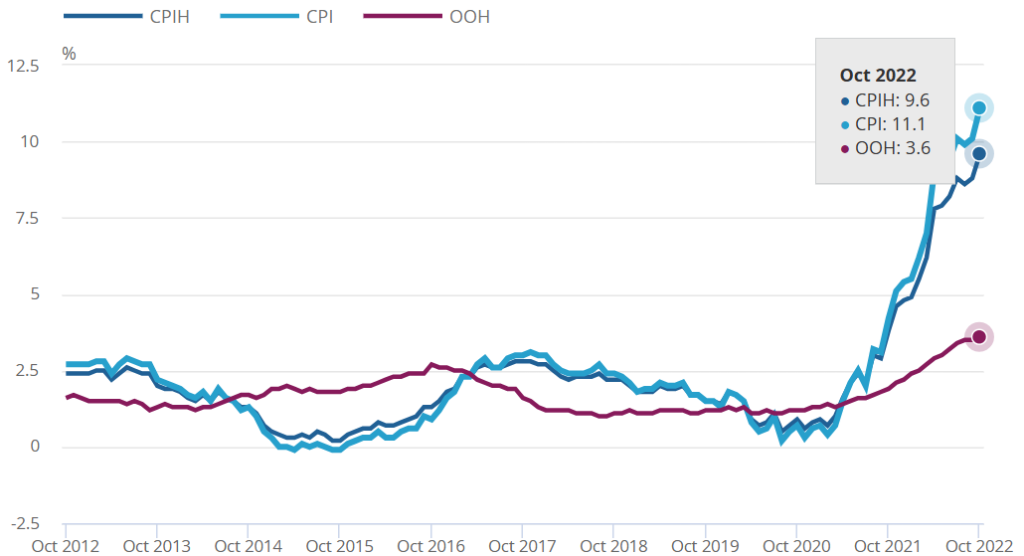

The EU faced the brunt of the 2021-2023 energy crisis in the form of severe inflation. The EU’s annual inflation rate hit 11.5% in October 2022, up from 10.9% the month before. Meanwhile, the UK’s CPI rose by 11.1% in the 12 months to October 2022, a 41-year high.

Across the Atlantic, the US wasn’t faring better either. February 2022’s CPI came in at 7.9% year-over-year. It was the hottest reading since January 1982, with energy the single biggest contributor to price gains, accounting for roughly a third of the entire headline increase.

Central banks’ response to the crisis is etched in history books as more reactive than proactive. The Fed, the ECB and others paid a heavy price for misjudging the post-pandemic inflation as a temporary storm.

The central banks’ waiting game to react to inflation, as they did in 2021 and 2022, amplified the jump in inflation. In fact, the Fed stayed idle for roughly a full year before reacting to inflation that had surged above 2%.

The ECB, which had been even slower to pivot, faced the same reckoning. The risk of falling behind the curve in 2022 left the ECB scrambling to turn hawkish long after inflation had already become entrenched.

Four Next Possible US-Iran War Scenarios, And What They Mean For Oil

Let’s circle back to the current turmoil of the US-Iran war.

The Islamabad talks were supposed to be the moment the world exhaled…but they weren’t.

The first round of talks on April 11 didn’t bear the outcome that the world hoped for. Trump originally extended the ceasefire until 22 April, but the fate of the war remains delicately balanced.

For investors and traders, the question isn’t whether this conflict ends. It’s how it ends, and what each outcome means for energy markets. Here are the four scenarios worth watching:

Scenario One: A Deal Gets Done. Oil Drops

If both sides reconcile at the table and reach a win-win agreement, including the reopening of the Strait of Hormuz and the US withdrawing its naval blockade, oil can reprice sharply downward. Since 28 February, markets have been running a substantial war premium on oil.

The moment that premium starts unwinding, the sell-off could be rapid. Energy stocks would likely follow crude lower, while airlines, manufacturers, and consumer-facing sectors would catch a meaningful tailwind.

Scenario Two: The Talks Collapse. Strikes Resume

Trump warned that “lots of bomb will start going off” if there’s no agreement before the ceasefire deadline. If talks collapse entirely and military offensives resume, oil would almost certainly retest its wartime highs, and potentially push beyond them if the Strait of Hormuz closes again or new infrastructure is targeted.

Therefore, a return to $120 and beyond Brent is not impossible.

Scenario Three: Talks Drag On. Volatility Stays Longer

Classic Trump’s TACO will come into the picture (and as of 22 April, Trump has indeed extended the ceasefire). Any mention of a ceasefire will remove pressure from Iran and allow Iran room to drag out talks.

A ceasefire that moves like a bouncing ball – proposed, extended, broken, and re-extended traps oil in a sideways movement. While intraday and scalping traders rejoice at the wealth of opportunities, the same can’t be said for long-term investors.

It’s a risk-management headache, with inflation staying elevated and central banks left in an uncomfortable position.

Scenario Four: A Partial Deal. The Straits Open, But The Tension Remains

This scenario is akin to a taut rope in a tug-of-war.

Iran agrees to reopen the Strait of Hormuz in exchange for sanctions relief, but the broader military situation remains unresolved. Iran reopening the Strait is a key demand from the US, with a regional framework for guaranteed maritime security forming part of the proposed terms.

While this scenario carries underlying tension, it would still be bearish for oil. A partial deal would ease the immediate supply crunch but leave a persistent geopolitical risk premium for the oil prices.

Think of it less as a resolution and more as a pause, with the clock already ticking on the next flashpoint.