UK Energy Secretary Ed Miliband is set to travel to China on March 17. The purpose of the visit is to revitalise discussions on energy cooperation under the UK-China Energy Dialogue.

During his trip, he will also engage with Chinese investors. This visit aims to strengthen ties and facilitate collaborative efforts between the UK and China in the energy sector.

Ed’s upcoming visit is expected to bring fresh momentum into energy discussions between the UK and China. The talks will likely cover ongoing investment projects, supply chain concerns, and long-term policy goals. Given that both countries have made extensive commitments to decarbonisation, there is an opportunity to assess current agreements and determine whether any adjustments are needed to accommodate recent shifts in global energy markets.

We also anticipate that Ed will use this trip to gauge China’s willingness to expand its financial involvement in UK energy infrastructure. British officials have previously expressed both optimism and caution regarding foreign direct investment in sectors deemed essential to national security. Any new agreements reached during these discussions could influence investor sentiment in the coming months.

Meanwhile, concerns about energy security linger. With continued volatility in international gas prices and growing demand for renewable alternatives, maintaining steady investment flows into clean energy projects is more important than ever. Discussions may touch on supply chain resilience and whether the UK can benefit from China’s established manufacturing capacity in this area.

Back home, reactions to Ed’s trip will be mixed. Some policymakers will view stronger ties with Beijing as necessary, while others may raise concerns about dependency risks. Investors should pay close attention to any updates from these meetings, as they could hint at future regulatory changes or potential shifts in trade policies.

Timing will also play a role. With global markets already navigating numerous challenges, any fresh commitments announced during this visit could influence short-term sentiment. If discussions lead to agreements on joint energy ventures or supply chain solutions, market participants will need to assess the wider implications.

Written on February 28, 2025 at 10:03 am, by anakin

One of the biggest myths in the world of trading is that some might think “more trades mean more profits.” However, like the concept of supply and demand, you don’t simply increase profits by increasing the amount you sell.

Some market participants believe they need to be active every single day to stay sharp and profitable–as if taking a break would make their entire profit strategy fall apart.

What if the key to making more money wasn’t trading more–but less?

In this article, we’ll explore why taking a step back away from the charts and trading selectively can make you a smarter, more profitable and happier trader.

Why Trading Everyday Could Be Hurting your Profits

Many traders fall into the trap of thinking that the more they trade, the more they earn. However, overtrading often leads to unnecessary losses, increased fees, and a lack of discipline. Taking every opportunity that presents itself means exposing yourself to low-quality setups that don’t align with a strong strategy.

A well-placed trade on a high-probability setup beats any amount of rushed trades with no real edge. The best traders understand that waiting for the right moment is a strategy in itself.

Constant Trading and its Emotional Toll

Trading is a mental game, and market fatigue is real. Staring at charts all day and reacting to every price movement can lead to emotional exhaustion and decision paralysis. This often results in impulsive trades, revenge trading, or second-guessing strategies.

GIF: Don’t let this be you, it’s okay to take a TB* at times! (*Trade brake–patent pending).

Taking a step back from the charts and giving yourself time to process setups objectively can make you a sharper, more confident trader.

Not Every Day is a Good Day to Trade

Markets don’t move in clear patterns every single day. Some days, price action is choppy, unpredictable, and filled with false signals. Traders who force trades on these low-quality days often experience frustration and losses.

Understanding when not to trade is just as valuable as knowing when to enter the market. Being selective gives you an edge by ensuring that every trade is backed by solid reasoning.

Introducing the Power of Selective Trading

Successful traders operate with a high conviction, low-frequency approach. Instead of chasing every minor market fluctuation, they focus on setups that offer clear signals, strong confluence, and manageable risk. Every trade should have a purpose. If you can’t confidently justify why you’re entering a position, you probably shouldn’t be taking it.

Less Trading: Lower Costs and Smarter Risk Management

Frequent trading racks up spreads, commissions, and slippage, quietly eating into your profits. By reducing the number of trades, you preserve capital and increase profitability over time. Additionally, when traders take fewer but higher-quality trades, they can afford to be more patient with their entries and exits, rather than making emotional decisions under pressure.

Patience Pays Off

Inexperienced traders fear missing out on opportunities, but experienced traders wait for the market to come to them.

GIF: We know it’s tough but trust us–there’s power in waiting (be it for cookies or trades).

They know that the best setups don’t happen every hour or even every day, but when they do, they’re worth the wait. Patience isn’t just a virtue—it’s a strategy that separates successful traders from the rest.

How to Start Integrating Selective Trading

First, start by creating a strict trade entry checklist–setting non-negotiable conditions that must be met before you place your trades.

For example;

A strong trend confirmation

Key support or alignment of resistance

Clear risk-to-reward ratio

Market conditions that match your personal trading strategy

Don’t hard force any trades that don’t meet all your criteria–another will come your way.

GIF: When one trading door closes–another opens!

You can also use an economic calendar to pick the right days to trade. High-impact news events like NFP, interest rate decisions, and CPI reports create volatility that can present both opportunities and risks. Having a plan for when to trade around these events helps you avoid unnecessary noise in the market.

Finally, another good tactic would be to set ‘no-trade’ days for yourself. Traders often feel pressured to be in the market every day. But what if you intentionally took days off from trading to review setups, refine your strategy, or just step away from the screens?

Final Thoughts

Selective trading allows you to:

Focus on quality setups over random entries

Avoid mental burnout and trades ruled primarily by emotion

Rude unnecessary trading costs

Increase long-term profitability

By shifting the mindset from “trade more” to “trade better,” you’ll not only improve your performance but also experience a more disciplined and stress-free trading journey.

The next time you’re about to place a trade, ask yourself—does it truly meet your criteria? If not, maybe the best trade is no trade at all.

Emini S&P March dropped from resistance at 6010/6015, reaching a range of 5873 to 6014. A break below 5975 suggested a decline towards support levels at 5925/5915, allowing for potential profits of up to 1000 points on shorts.

Emini Nasdaq March fell below 21000 for a sell signal, with last session levels between 20583 and 21386. A short-term buying opportunity appears at 20450/350, with stops advised below 20250.

Emini Dow Jones March saw a successful trade at resistance 43750/850, collapsing to near the target at 43100/43000. Longs need to set stops below 42850 while resistance remains at 43750/850.

Key Support And Resistance Levels

The S&P’s retracement from the upper level of 6010/6015 was in line with expectations, as sellers capitalised on weakness, driving prices down towards a well-established lower boundary. The dip under 5975 provided confirmation of a bearish bias in the short term, offering those positioned correctly the chance to secure sizeable gains. The area between 5925 and 5915 continues to attract attention as a potential floor, though further declines cannot be ruled out if momentum remains.

In the Nasdaq, the breakdown below 21000 gave sellers control, leading to price action contained between 20583 and 21386. The suggestion that 20450/350 presents a buying setup means that some traders will be preparing for a potential reversal, though there’s little room for complacency with protective stops recommended under 20250. Those looking to engage here will need to balance the opportunity with the potential for selling pressure to extend lower.

The Dow adhered to the outlined resistance levels near 43750/850, with sellers taking full advantage to drag the price down to the anticipated 43100/43000 zone. For those considering buy positions, stops must be kept tight beneath 42850 to manage risk properly. The resistance at 43750/850 remains decisive, and unless buyers can push through, more downside moves remain a possibility.

Trading Strategies And Considerations

For traders focused on derivatives, the recent price movements reinforce the importance of recognising when levels hold and when they break. The market continues to react to predefined technical areas, and adjusting position sizes and stop levels accordingly will be key heading into the next sessions. Each index has shown responsiveness to key levels, and the ability to adapt as momentum shifts will dictate short-term success.

China’s National Bureau of Statistics (NBS) will release the February PMIs over the weekend, with expectations for improvements in both manufacturing and services. Manufacturing PMI is anticipated to enter expansion territory after a contraction in January, influenced by the Lunar New Year holiday.

Recent data shows fluctuations in manufacturing activity, with the PMI rising to 50.3 in November 2024 before dropping to 49.1 in January 2025. The non-manufacturing PMI experienced similar trends, dipping to 50.2 in January 2025 after a recovery in December.

The NBS and Caixin/S&P Global PMIs differ in scope and methodology. The NBS PMI focuses on large state-owned enterprises, reflecting government priorities, whereas the Caixin PMI covers small to medium enterprises, offering insights into private sector performance.

Both indices provide valuable perspectives on China’s economy. The NBS PMI represents the broader economic landscape influenced by state policies, while the Caixin PMI highlights the more responsive and volatile private sector.

We expect the upcoming PMI data to shed light on the strength of China’s economic momentum following the New Year holiday. A reading above 50 for manufacturing would indicate a return to expansion, reinforcing recent sentiment that economic conditions are stabilising. The services sector, which has been hovering just above contraction territory, is also being watched closely for signs of continued growth.

The divergence between the official and private-sector PMIs will be particularly relevant. The former, reflecting trends in larger state-owned businesses, will show whether government-driven measures aimed at revitalising industrial activity are yielding results. The latter, with its emphasis on small- and mid-sized firms, should give a sense of how private businesses are coping with domestic demand and external pressures. If both point in the same direction, confidence in that trajectory strengthens. If not, it adds an extra layer of uncertainty.

Markets have been reacting sensitively to any signs of weakness in China, and these numbers will influence sentiment in broader risk assets. A return to expansion in manufacturing could lift spirits and reduce concerns about sluggish industrial output. On the other hand, if the numbers fail to break past contractionary territory, it could revive discussions about the need for additional policy support.

Looking beyond just the headline figures, we will also be paying attention to sub-indices such as new orders and employment. These provide context beyond the overall reading and help determine whether any improvement is sustainable. A rebound driven purely by short-term factors lacks the durability needed to shift expectations longer-term.

In the coming weeks, markets will also be digesting how policymakers interpret the data. Stronger PMIs may lead to a more measured approach from authorities when it comes to further support, while weaker prints would make additional intervention appear more likely. As attention remains on policy direction, any surprises in this data set will set the tone for expectations.

Written on February 28, 2025 at 9:32 am, by anakin

The Consumer Price Index (CPI) in France for February 2025 registered a year-on-year increase of 0.9%, falling short of the anticipated 1.2%. This marks a continuation of cautious economic signals as the market watches for future developments.

Global market movements are influenced by various factors. The EUR/USD pair remains below 1.0400 amid increased demand for the US Dollar due to tariff concerns, while cryptocurrencies like Bitcoin have seen a decline exceeding 15% within the week.

In the forex market, GBP/USD has dropped below 1.2600, facing pressure from tariff uncertainties. Moreover, gold prices are hovering near a two-week low as traders anticipate the upcoming US PCE Price Index data, which could impact market sentiment.

What we’re seeing with the lower-than-expected CPI in France is a cooling of inflation pressure, at least for now. Analysts had been looking for a 1.2% rise, yet the actual figure came in at 0.9%. This isn’t a number to ignore, especially with growing concerns over growth and inflation trends across Europe. Those who rely on economic indicators to plan trades should keep a close watch on whether this is part of a broader slowdown or just a temporary shift.

Meanwhile, moves in the currency market aren’t happening in isolation. The euro has been struggling against the US dollar, with the EUR/USD pair staying below 1.0400. The strength of the dollar comes from concerns over tariffs, which are leading investors towards safer assets. When trade policies look unstable, markets tend to favour the dollar over other currencies. This isn’t just affecting the euro – sterling has lost ground as well, with GBP/USD slipping below 1.2600 under similar pressures. That’s a clear indication that traders remain sensitive to economic uncertainty.

At the same time, the world of digital assets is not being spared. Bitcoin, down more than 15% this week, is showing just how fragile sentiment is in the cryptocurrency sector. Those who had pushed prices higher in previous weeks might now be reconsidering their positions or taking profits while they can. Volatility remains a constant in this space, and when broader economic worries take over, risk exposure tends to shrink.

Gold, often seen as a haven in uncertain times, is also under pressure. Prices are near a two-week low, with traders holding back ahead of the latest US PCE Price Index data. This data point carries weight because it will shape expectations around inflation and, in turn, influence Federal Reserve policy. If inflation remains elevated, we could see stronger anticipation of tighter financial conditions in the US, reinforcing dollar strength and keeping gold under pressure.

Short-term strategy will depend on how these factors progress in the coming days. Inflation figures, currency movement, and commodity prices are all feeding into broader financial trends. With unpredictable shifts in economic policy and market sentiment, reaction speed will be key. Those watching for opportunities should pay attention to both structural trends and near-term fluctuations, since markets are unlikely to settle into a steady rhythm just yet.

Written on February 28, 2025 at 9:07 am, by anakin

Donald Trump is scheduled to speak with the media on Friday at 9 am US Eastern time, which is 2 pm GMT. He is expected to address tariffs that have been subject to fluctuations.

Later, a press conference will take place at 1 pm US Eastern time, or 6 pm GMT, featuring the President of Ukraine. After these engagements, Trump will travel to Florida for a golf weekend.

Trump will likely make comments that could affect expectations around trade policies. That alone means traders will have to monitor his statements carefully. If he delivers a message that reinforces prior commitments, there may only be modest adjustments to market sentiment. However, should he introduce new details or shift his tone, this could prompt movements in futures markets. As always, volatility can arise if his words differ from what was anticipated.

At midday in New York, Ukraine’s President will take questions from journalists. Given the context of ongoing negotiations and external pressures, this event also carries weight. If new information emerges about financial support or geopolitical risks, certain assets may respond accordingly. Depending on how markets interpret the message, shifts in direction could follow.

Following these appearances, Trump will head to Florida, ostensibly for a weekend away from Washington. That means there’s limited potential for direct political developments from him through to Monday. However, any remarks before his departure could linger in the market. When a figure of his influence makes off-the-cuff comments, they sometimes take a few sessions to be fully absorbed.

What this tells us is that traders will need to plan carefully. Price swings could be triggered by statements during the first half of the day, particularly if they deviate from expectations. Keeping an eye on these events as they unfold will be essential, especially for those tracking short-term movements.

Written on February 28, 2025 at 9:03 am, by anakin

The core Personal Consumption Expenditures (PCE) Price Index is anticipated to increase by 0.3% month-on-month and 2.6% year-on-year for January. The Federal Reserve is expected to maintain its current monetary policy during upcoming meetings, with annual PCE inflation projected to decline slightly to 2.5%.

The US Bureau of Economic Analysis will release the PCE data at 13:30 GMT on Friday. This index serves as the Federal Reserve’s preferred inflation measure, focusing primarily on changes excluding volatile food and energy prices.

Analysts suggest that January may see a weaker core PCE advance compared to previous data, with forecasts indicating a decrease in annual inflation from 2.8% to 2.5%. Personal spending is also expected to drop, marking the first decline since March.

After a rate cut of 25 basis points in December, the central bank held interest rates steady in January, citing concerns over persistent price increases. Market participants anticipate a low chance of rate cuts after the upcoming PCE readings, with a 98% probability of unchanged policy in March.

Unexpected movements in the PCE index could lead to quick fluctuations in the US Dollar’s value. A reading of 0.4% or higher might bolster the Dollar, while below 0.2% could weaken it substantially.

While inflation impacts currency valuation and market dynamics, current expectations lean towards steady economic measures from the Fed. Further soft readings may prompt a reconsideration of policy adjustments later in the year.

Expectations for Friday’s PCE release suggest inflation pressures may ease slightly, with core PCE forecasted to rise by 0.3% on a monthly basis and slow to 2.6% over the year. Given that this measure excludes volatile food and energy prices, it provides a clearer view of inflation trends and remains the Federal Reserve’s preferred gauge. We are also anticipating personal spending to decline for the first time since March, reinforcing concerns that consumer demand could be cooling.

Core inflation has been stubborn in previous months, but January’s reading is expected to retreat further from December’s 2.8%, inching towards the Fed’s target. This aligns with the central bank’s stance of keeping policy steady after its last rate cut in December, when it opted to hold rates unchanged in January. With PCE data due at 13:30 GMT, market expectations for rate adjustments remain minimal in the short term—futures pricing suggests a 98% chance the Fed remains on hold in March.

If the data were to deviate sharply from forecasts, however, volatility could be swift. A stronger-than-expected 0.4% monthly increase might fuel US Dollar strength, signalling that inflation remains sticky. On the other hand, a lower-than-anticipated 0.2% or less could weaken the Dollar, reinforcing the notion that pricing pressures are softening and increasing discussions around potential policy shifts later in the year.

Monetary authorities will closely assess whether inflation trends justify a continued pause in policy adjustments. The persistence of price increases has been a consistent talking point, and fresh data will be critical in shaping how markets approach rate expectations across the next few months. A softer trajectory could begin shifting sentiment more firmly towards eventual easing measures, though abrupt policy shifts remain unlikely in the near term.

Written on February 28, 2025 at 8:37 am, by anakin

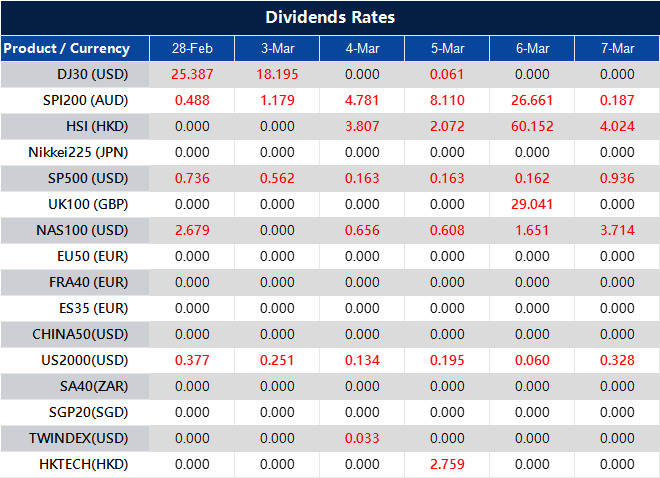

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on February 28, 2025 at 8:36 am, by anakin

Bitcoin is experiencing a decline, with its value hitting levels not observed since 11 November of the previous year. This downturn occurs as the US dollar strengthens against other currencies.

This downturn suggests that broader economic forces are influencing prices, with traders adjusting their positions in response to external pressures. A stronger US dollar often leads to downward movements in assets like Bitcoin, as it becomes more expensive for those using other currencies to invest. This pattern has played out before, and it is happening again now.

Market sentiment is also shifting. Investors who were optimistic just a month ago are reassessing their strategies, especially as global liquidity tightens. When borrowing costs rise and liquidity declines, riskier assets tend to see less demand. Bitcoin, which has long been viewed as both a hedge and a speculative instrument, is reacting much as it has in previous cycles.

Technical indicators now show momentum slowing. The latest charts suggest pressure building near key support levels, and if those do not hold, further declines could follow. At the same time, historical data reminds us that corrections of this scale are part of Bitcoin’s behaviour. Some see this as an opportunity, while others step to the sidelines and wait for a more favourable entry.

Macroeconomic conditions cannot be ignored. Inflation data, central bank policies, and employment statistics all play a role, directly or indirectly, in shaping expectations. Jerome, as head of the Federal Reserve, remains firm in his stance, and his recent remarks indicate that tightening policies will not change course too soon. That has consequences not only for traditional markets, but also for digital assets. In previous instances, similar tightening cycles led to reduced activity in speculative markets.

Meanwhile, institutional involvement shows contrasting signals. Some firms continue to accumulate, while others pause. This divide reflects differing views on what comes next. Long-term holders often take downturns in stride, while short-term participants may feel pressure to exit. These opposing forces create the kind of volatility that has defined Bitcoin for years.

As we look ahead, the coming weeks will likely be shaped by external economic factors as much as by technical trends. Responses from policymakers, adjustments in global liquidity, and shifts in sentiment will all influence what happens next. The question now is whether the current support levels will hold, or if further adjustments need to be made.

Written on February 28, 2025 at 8:32 am, by anakin

EUR/GBP is trading around 0.8260 as concerns regarding potential US tariffs on the UK grow. President Trump indicated tariffs might be imposed after discussions with PM Keir Starmer, creating risk aversion amidst US-EU trade tensions.

The Pound Sterling weakened following this announcement and Bank of England Member Swati Dhingra’s support for several rate cuts. Dhingra noted that maintaining a pace of rate cuts would still leave monetary policy overly restrictive by the end of 2025.

Tariffs, customs duties aimed at protecting local producers, are considered by some economists necessary while others view them as harmful. Trump has indicated plans to impose tariffs to bolster the US economy, particularly on imports from Mexico, China, and Canada.

With the euro currently hovering near 0.8260 against sterling, we are watching the market wrestle with political uncertainty and monetary expectations. Concerns over potential US tariffs on the UK have unsettled investors. After discussions between Donald Trump and Keir, the possibility of increased trade barriers has come into sharper focus, pulling the pound lower.

In response to these developments, traders have shifted towards safer assets, a pattern that often emerges when global trade relations look fragile. As a result, sterling lost ground, amplifying the euro’s strength. Beyond trade disputes, policy signals from the Bank of England remain in focus. Swati’s support for multiple rate cuts has reinforced an expectation that UK interest rates may fall faster than previously thought. She argued that even with planned reductions, borrowing costs would likely stay high by the end of next year. Markets have responded by factoring in a looser monetary stance, pushing investors to reassess their positions.

A key question moving forward is how trade policy concerns and monetary shifts will affect sentiment in the derivatives market. Tariffs, which are intended to protect domestic industries from foreign competition, have long been a source of debate. Some argue they support jobs and manufacturing, while others warn they raise costs for businesses and consumers alike. Trump has left little doubt about his intentions on this front, reaffirming plans to impose tariffs across multiple trade partners, not just the UK. This stance has led to increased speculation regarding the potential economic fallout.

As a result, the coming weeks could see further volatility. Political shifts, interest rate bets, and shifting trade policies are creating a fluctuating environment where sentiment can pivot quickly. Given how markets have responded to similar situations in the past, movements in EUR/GBP will likely depend on both upcoming central bank signals and any fresh developments on the tariff front.

Written on February 28, 2025 at 8:07 am, by anakin