Key Takeaways

- The AI boom is real in both spending and earnings impact, but profits are currently concentrated in a small group of infrastructure companies, not the broader economy.

- Early winners are the “bottleneck owners” like cloud providers (Microsoft, Amazon, Alphabet), chipmakers (Nvidia, AMD), and key suppliers, who monetise AI first while others pay to adopt it.

- Massive AI capital spending (projected $700B+ by 2026) confirms this is a real infrastructure buildout, but most end-user companies are still in the cost and experimentation phase, with delayed payoffs.

- The market rally is increasingly driven by the Magnificent Seven, creating high index concentration risk where a few stocks heavily influence overall market performance.

The AI boom is real. The spending is real. The earnings impact is real. The problem is that the reward is not evenly distributed across the market yet. That distinction matters because investors are treating artificial intelligence as both a technological revolution and a stock market justification. On the technology side, the case is strong. AI is already reshaping artificial intelligence, cloud computing, chips, data centres, advertising, and enterprise workflows. On the market side, however, the benefits remain concentrated in a relatively small group of companies. It is also increasingly influencing AI trading systems used across financial markets.

The First Wave of AI Profits Goes to the Bottleneck Owners

In the early stage of any major technology cycle, the biggest profits flow to the companies that control the bottlenecks. Right now, those are clear. You can see this reflected in top AI stocks that dominate infrastructure and compute demand. Cloud infrastructure is controlled by Microsoft, Amazon, and Alphabet. AI chips are dominated by Nvidia, with AMD and Broadcom playing significant roles.

Microsoft, Meta, Alphabet, and Palantir lead AI platforms and enterprise software. Memory and networking are benefiting Micron, SK Hynix, Marvell, and Arista. The companies that merely use AI may benefit later, but they first have to pay the infrastructure providers. That explains the current market structure. The AI economy is broad in theory. The AI profit pool is still narrow in practice.

The Spending Is Real and Enormous

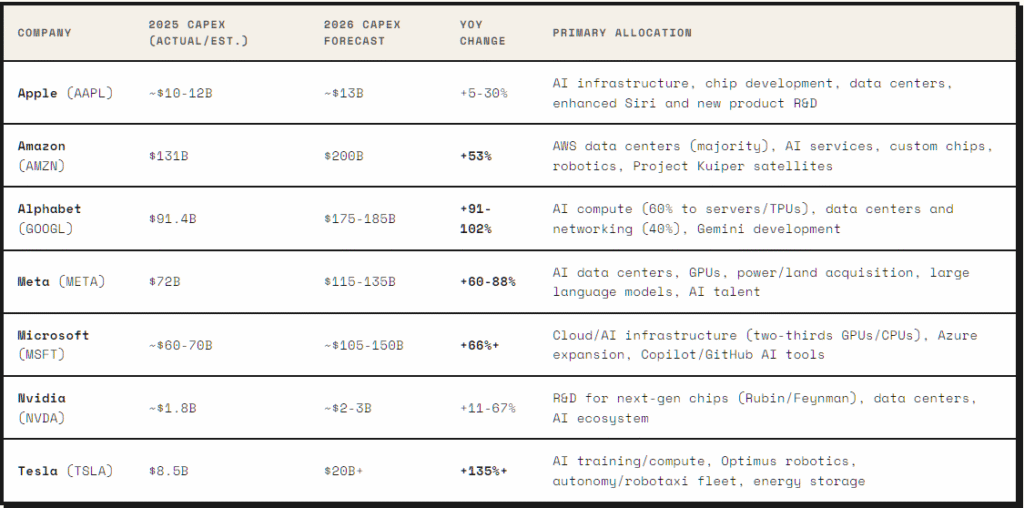

The strongest argument against calling this cycle hype is that the spending is tangible. Concerns about an AI bubble are rising as capital expenditure accelerates. AI capital expenditure is showing up in corporate budgets, data centre construction, chip demand, and cloud growth. Estimates suggest AI infrastructure spending by major tech firms could exceed $700 billion in 2026, up sharply from around $410 billion in 2025. The biggest companies in the world are not treating AI as a side project. They are treating it as the next core layer of infrastructure in the digital economy. However, the scale of spending raises the central market question. Who earns the return on it? Right now, the answer is still mostly the infrastructure owners.

Source: r40.io

Why AI Has Not Benefited Everyone Yet

For most companies, AI is still more of a cost and productivity experiment than a clear earnings driver. A bank may detect fraud faster. A retailer may improve inventory planning. A manufacturer may sharpen predictive maintenance. These are real benefits, but they do not immediately appear as explosive revenue growth.

In many cases, AI first arrives as higher technology spending. Companies pay for cloud services, software subscriptions, model integration, and employee training. The productivity benefit comes later. Microsoft, Nvidia, Amazon, Alphabet, and Meta do not face that delay. They collect revenue as other companies build, test, and scale AI systems. That is why AI benefits exist but remain highly unequal.

The Magnificent Seven Problem

The Magnificent Seven still carry a disproportionate share of market earnings growth and market value, accounting for roughly 34% of the S&P500 as of December 2025, up from just 12% a decade ago. In 2025 alone, roughly 42% of the S&P 500’s total return came from these seven stocks. That concentration is not automatically irrational.

These companies have stronger balance sheets, stronger margins, and clearer AI monetisation paths than most of the market. HSBC has raised its year-end S&P 500 target, citing continued earnings strength and AI investment driven by major technology firms. However, the risk is that investors may think they own a diversified market when they are actually holding a highly concentrated AI trade. If one or two mega-cap leaders disappoint on earnings or cloud growth, the whole index can suddenly look weaker. Concentration cuts both ways. On the way up, it creates powerful index performance. On the way down, it creates fragility.

What Is Not Hype and What Still Might Be

Several parts of the AI story are clearly not hype. Capital expenditure is real. Cloud, chip, memory, and networking demand are real. Revenue growth at the infrastructure leaders is real. Dismissing the entire AI boom as a bubble is too simplistic. The potentially hyped part is the assumption that AI will quickly lift earnings across the entire economy. That has not been proven yet. Many companies are still in the experimentation phase, testing tools and restructuring workflows. Some will generate meaningful returns. Some will waste money. Some use AI mainly as a marketing label.

The next phase of the AI cycle will require investors to separate three groups. As markets evolve, this also ties into broader shifts in algorithmic trading and execution speed across institutions. First, companies selling critical AI infrastructure. Second, companies using AI to create measurable productivity gains. Third, companies using AI as branding. The first group has already been rewarded. The second may drive the next leg of broadening. The third is where the real hype risk sits.

The Bottom Line

The AI boom is real, but it is not yet democratic. The biggest profits are flowing to infrastructure owners, not the wider economy. The market may be pricing in a future where AI benefits everyone before that future has fully arrived. For traders and investors, understanding how to start trading forex and choosing the right forex broker becomes part of positioning in this broader macro shift.

The bull case is that AI eventually spreads across the entire economy and creates a new productivity cycle. The bear case is that the market has already rewarded infrastructure winners too aggressively while assuming the rest of corporate America will catch up quickly.

AI is no longer a future story. It is already reshaping how businesses operate and where capital flows. The challenge for investors is not deciding whether AI matters — it clearly does.

The challenge is identifying who captures economic value.

So far, the biggest rewards have gone to companies building the infrastructure that powers AI. Whether those benefits eventually spread across the broader economy may determine whether today’s AI rally becomes a long-term productivity revolution or remains a narrow market phenomenon.

The Big Questions

1) Why are AI profits concentrated in so few companies if technology is revolutionary?

The AI economy is broad in theory, but the profit pool is narrow in practice. In the early stages of a technology cycle, profits flow to “bottleneck owners” — the companies controlling the essential infrastructure. Cloud platforms (Microsoft, Amazon, Alphabet) and hardware/networking layers (Nvidia, AMD, Broadcom, Micron, SK Hynix, Marvell, Arista) collect high-margin revenue upfront because everyone must pay them just to build, test, and run AI systems.

2) Why hasn’t AI translated into explosive revenue growth for regular businesses yet?

For most non-tech companies, AI currently arrives at an upfront operational expense rather than a revenue driver. Businesses face massive immediate bills for cloud computing blocks, software tokens, system integration, and employee training. While tools like predictive maintenance or automated fraud detection provide real productivity help, it takes time for internal efficiency gains to scale into explosive top-line revenue.

3) What concrete proof shows that the AI boom is driven by fundamental value, not hype?

The spending is entirely tangible and massive. Global AI capital expenditure (CapEx) from major technology firms is projected to scale past $700 billion, marking a steep surge from roughly $410 billion. This capital isn’t funding speculative software ideas; it is being poured directly into physical infrastructure like microchips, fibre-optic networking, data centres, and power grids.

4) Why is market concentration in the Magnificent Seven a double-edged sword?

The Magnificent Seven account for roughly 34% of the S&P 500’s total value, meaning standard index investors are essentially holding a highly concentrated AI trade. While their dominant margins and massive balance sheets justify a premium, concentration cuts both ways. It creates powerful, upward stock index performance during growth periods, but injects immense fragility if just one or two leaders miss their cloud growth or earnings targets.

Start trading now – Click here to create your real VT Markets account