Key Points

- Mortgage rates are primarily driven by US Treasury yields, with the 10-year acting as the key benchmark rather than the Fed’s policy rate.

- The Fed’s cautious stance on rate cuts in 2026, amid persistent inflation and energy-driven risks, is keeping long-term yields—and mortgage rates—elevated.

- Mortgage rates serve as a leading indicator for financial conditions, influencing housing demand, consumer spending, and broader market sentiment.

The Fed does not set Mortgage Rates

Mortgage rates are often misunderstood as being directly controlled by the Federal Reserve. In practice, the relationship is indirect and mediated through financial markets.

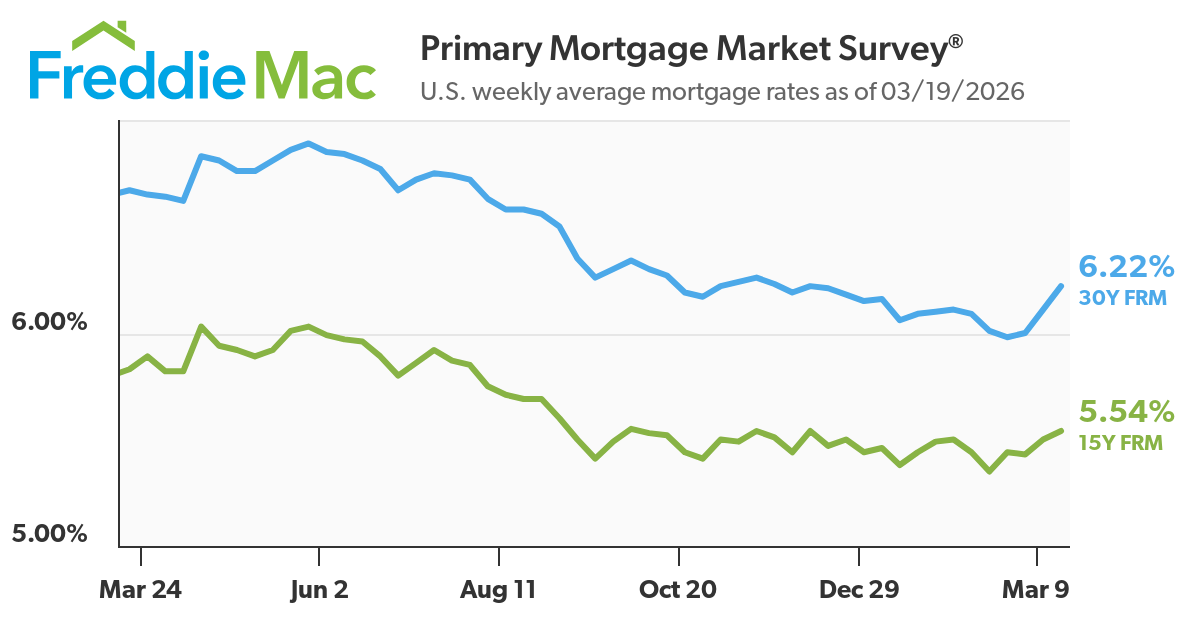

As of early 2026, the average US 30-year fixed mortgage rate has been hovering just above the 6% mark—rising to around 6.1% in mid-March after briefly dipping below 6% in February. This movement did not come from a change in the Fed’s policy rate, which remained on hold, but from shifts in bond yields and market expectations.

For traders, this distinction matters. Mortgage rates are not a policy tool, they are a market-derived price of long-term capital, reflecting inflation expectations, growth outlook, and risk premia.

Not sure about bonds? Learn about them here.

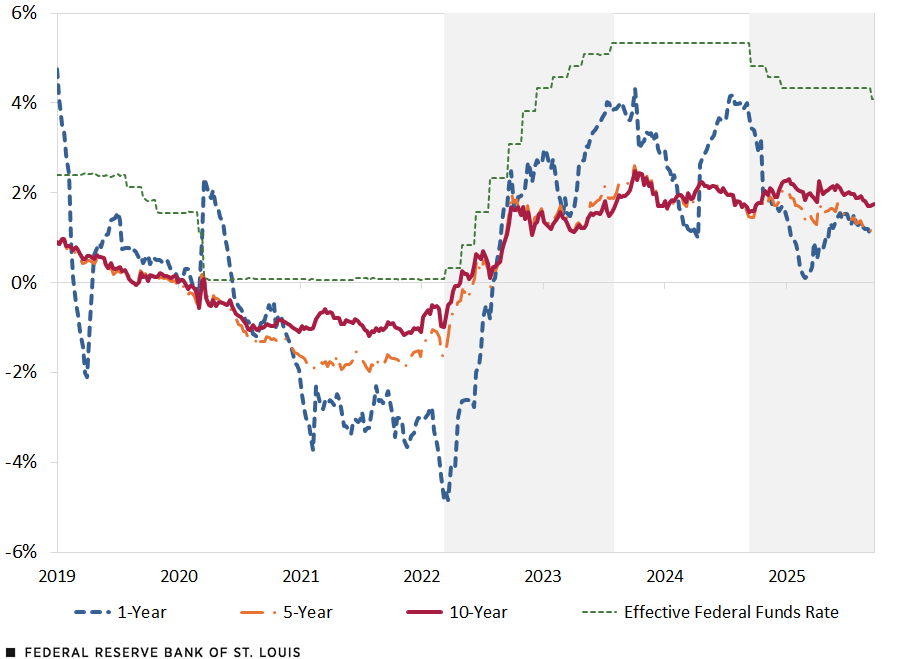

The Key Link: Treasury Yields and Mortgage Rates

Mortgage rates track the US 10-year Treasury yield because both represent long-term borrowing costs.

Historically, the spread between the 30-year mortgage rate and the 10-year yield sits around 150 to 300 basis points, depending on market conditions.

For example:

- If the 10-year yield is around 4.2%, mortgage rates may price closer to 6.0%–6.5%

- During periods of stress (e.g. 2022–2023 tightening cycle), the spread widened due to volatility and risk repricing

SOURCES: Bloomberg and FRED (Federal Reserve Economic Data).

NOTES: Weekly data based on Treasury inflation-protected securities. Data retrieved on Sept. 24, 2025.

Key drivers of this relationship include:

- Inflation expectations Higher expected inflation pushes yields higher, lifting mortgage rates.

- Term premium Investors demand compensation for holding long-duration bonds in uncertain environments.

- Market volatility In unstable conditions, lenders widen spreads, increasing mortgage rates beyond what yields alone would suggest.

For traders, this makes the bond market the primary signal to watch. Read about how liquidity affects the movement of bond markets and geopolitical structure here.

Why the Fed Still Matters

The Federal Reserve might not set mortgage rates, but they definitely shape them.

The Fed anchors expectations around inflation, growth, and future policy. Those expectations feed directly into bond markets, particularly the US 10-year Treasury yield, which is the primary benchmark for mortgage pricing.

In 2026, the Fed’s stance has shifted markets away from aggressive easing and toward a more cautious outlook. That shift alone has been enough to keep borrowing costs elevated.

What the Fed is Signalling in 2026

- Data-dependent rate cuts The Fed has made it clear that easing will depend on sustained progress in inflation, not forecasts alone.

- Persistent inflation concerns Core inflation—especially in services—remains sticky, limiting the scope for rapid rate cuts.

- Sensitivity to energy prices Rising oil prices and geopolitical risks are feeding into inflation expectations, keeping pressure on yields.

How This Feeds Into Mortgage Rates

- Delayed rate-cut expectations Markets have repriced from multiple cuts to a slower path. This has kept the 10-year yield elevated around ~4.1%–4.3%.

- Higher-for-longer narrative Even without hikes, the absence of cuts keeps financial conditions tight and borrowing costs elevated.

- Quantitative tightening (QT) The Fed continues to shrink its balance sheet, reducing demand for Treasuries and mortgage-backed securities—pushing yields higher.

What the Data Shows

- The US 10-year Treasury yield has remained above 4% in recent weeks

- The 30-year fixed mortgage rate has rebounded to around ~6.1% in March, after dipping below 6% in February

- The spread between yields and mortgage rates remains elevated, reflecting risk and market volatility

Why This Matters for Markets

- Fed tone moves yields—even without action

A hawkish shift in communication can push yields higher immediately. - Mortgage rates follow expectations, not decisions

Markets price future policy, not current rates. - Housing becomes a transmission channel

Higher mortgage rates tighten financial conditions, impacting consumption and growth.

Mortgage Rates as a Macro Signal

Mortgage rates act as a real-time indicator of financial conditions.

When rates rise:

- Housing affordability deteriorates

Monthly repayments increase significantly. A 1% rise in mortgage rates can increase monthly payments by hundreds of dollars on a standard loan. - Transaction volumes slow

Existing home sales and mortgage applications tend to decline. - The “rate lock-in effect” intensifies

Homeowners with sub-3% mortgages from prior years are reluctant to sell, tightening supply further.

When rates fall:

- Refinancing activity picks up

- Homebuyer demand improves

- Housing-related sectors stabilise

For instance, earlier in 2026, when rates briefly dipped below 6%, pending home sales saw a modest rebound, highlighting how sensitive housing demand is to even small rate moves.

For traders, this links mortgage rates directly to:

- consumer confidence

- retail spending

- cyclical equity sectors

What is Driving Mortgage Rates in 2026

Several macro forces are currently shaping mortgage rate dynamics:

- Sticky core inflation Services inflation remains persistent, limiting the Fed’s ability to ease policy aggressively.

- Energy market volatility Geopolitical tensions, particularly in the Middle East, have supported oil prices, feeding into inflation expectations and bond yields.

- Repricing of Fed expectations Markets have shifted from expecting multiple cuts to a more gradual easing cycle, supporting higher yields.

- Structural housing demand Despite higher borrowing costs, demographic demand and limited housing supply are preventing a sharp collapse in the market.

- Elevated term premium Investors are demanding higher compensation for holding long-term debt amid fiscal uncertainty and large government issuance.

Together, these forces explain why mortgage rates have remained relatively elevated despite no new rate hikes.

What Traders Should Watch

To anticipate mortgage rate movements, traders should monitor a combination of macro and market indicators:

- US 10-year Treasury yield (primary driver) Sustained moves above key levels (e.g., 4.2%–4.5%) typically lead to higher mortgage rates.

- Inflation data (CPI, PCE) Upside surprises tend to push yields higher and delay rate cuts.

- Federal Reserve communication Shifts in tone, particularly around inflation or labour markets, can quickly reprice expectations.

- Housing data releases Mortgage applications, building permits, and home sales provide real-time demand signals.

- Oil and energy prices Rising energy costs can feed into inflation expectations, indirectly lifting yields.

Bottom Line

Mortgage rates are best understood as a reflection of the bond market rather than a direct outcome of Federal Reserve policy.

In 2026, the combination of persistent inflation, cautious central bank messaging, and elevated term premiums keeps borrowing costs relatively high. For traders, mortgage rates offer a valuable lens into financial conditions: bridging policy expectations, consumer behaviour, and market sentiment.

Understanding this relationship is key to navigating both housing trends and broader macro-driven market moves.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Trader’s Takeaway

Do mortgage rates follow the Federal Reserve rate?

Not directly. Mortgage rates are more closely tied to long-term Treasury yields, though Fed policy influences those yields through expectations.

Why did mortgage rates rise even when the Fed paused?

Because bond yields increased due to inflation concerns and shifting expectations around future rate cuts.

What spread exists between Treasury yields and mortgage rates?

Typically between 150 and 300 basis points, depending on market conditions and risk factors.

Will mortgage rates fall if the Fed cuts rates?

Not necessarily. Mortgage rates will only decline meaningfully if long-term yields fall, which depends on inflation and growth expectations.

Start trading now – Click here to create your real VT Markets account