Major currencies in Europe see sluggish trading due to cautious market sentiment and upcoming events

The dollar is stable in European trading, showing only slight changes. European markets are quiet as everyone waits for the upcoming Jackson Hole event. Recent strong PMI data from the euro area confirmed the ECB’s choice to hold off on rate cuts, but this hasn’t greatly affected market movements.

Notification of Server Upgrade – Aug 21 ,2025

Dear Client,

As part of our commitment to provide the most reliable service to our clients, there will be maintenance this weekend.

Maintenance Details:

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss, and Take Profit will be filled at the market price once the maintenance is completed. It is suggested that you manage the account properly.

3. During the maintenance period, VT Markets APP will not be available. It is recommended that you avoid using it during the maintenance.

4. During the maintenance hours, the Client portal will be unavailable, including managing trades, Deposit/Withdrawal and all the other functions will be limited.

The above data is for reference only. Please refer to the MT4/MT5 software for the specific maintenance completion and marketing opening time.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected].

Société Générale highlights Jackson Hole’s focus on labor market discussions amid Fed’s internal debates

Markets are keeping an eye on the chance of a 50 basis point rate cut in September. Société Générale highlights that the main focus of Jackson Hole will be the labour market.

Fed officials are discussing whether the current tight labour market results from low participation or a wider economic slowdown. When deciding in September, they will pay more attention to the labour market than to price trends. Rising prices could make rate cuts more likely if they threaten growth.

Jackson Hole will be the first moment for the Fed’s communication to face scrutiny. However, events like the Non-Farm Payrolls on September 5 and the Consumer Price Index on September 10 will likely have a bigger impact on market expectations.

If the upcoming employment data disappoints again, markets may consider the possibility of a 50 basis point rate cut next month.

With the Jackson Hole symposium approaching, our focus shifts to the labour market. Fed officials are debating if the tightness in jobs is a long-term issue or a sign of a slowing economy. This discussion will likely shape interest rates for the rest of the year.

We are seeing clear signs of a softening job market that supports the case for rate cuts. The last Non-Farm Payrolls report for July showed only 115,000 jobs added, far below the expected 190,000, and the unemployment rate has risen to 4.2%. This follows a pattern of declining labour data over the past quarter, putting more pressure on the Fed.

However, core inflation remains stubborn, with the latest CPI holding at 3.8%. This complicates the Fed’s situation, as they need to balance support for growth with the risk of increasing price pressures. A weak jobs report could force them to prioritize growth over inflation.

For traders, volatility will be key as we head into the first week of September. Implied volatility on index options, measured by the VIX, has risen above 19, and we expect it to go up further as key data releases approach. Preparing for a significant market move, rather than predicting a specific direction, could be a wise strategy.

This scenario reminds us of the Fed’s proactive shift in 2019 when they cut rates due to fears of global growth, even with a relatively strong domestic economy. This history suggests officials may overlook a single inflation reading if they see a real threat to the labour market. Thus, the Non-Farm Payrolls report on September 5 is now the most crucial event on our radar.

If that jobs data disappoints again, markets will likely aggressively test the chance of a 50 basis point rate cut in September. Traders should be ready for significant changes in interest rate futures and currency markets right after the release. The market is set for a big shift, and this report could be the trigger.

UK’s flash services PMI surpassed predictions at 53.6, while manufacturing PMI declined below expectations

The UK services PMI for August rose to 53.6, beating expectations of 51.8, up from the previous 51.8. The manufacturing PMI dropped to 47.3, lower than the expected 48.3, with last month at 48.0. The composite PMI was 53.0, also above the forecast of 51.6, compared to the previous reading of 51.5.

The UK has seen the biggest increase in private sector activity since August 2024. Economic growth accelerated over the summer, driven mainly by services, while manufacturing shows signs of stabilizing. However, demand is inconsistent, with concerns about government policy changes and geopolitical issues impacting exports.

Payroll Numbers Decline

Payroll numbers are down due to weak order books and worries about rising staff costs tied to the autumn Budget. These issues contribute to ongoing inflation pressures, which reached 3.8% in July. The prospects for further interest rate cuts this year are unclear, as we need more data to assess the sustainability of growth and inflation. The economic data from August shows unexpected growth at its fastest pace since last year, mainly thanks to the services sector. This makes us reconsider the likelihood of the Bank of England lowering interest rates again this year. The key takeaway is that policy may remain tighter for longer than we initially thought. The Bank of England has cut its main interest rate twice since spring 2025, bringing it down to 4.0% to stimulate the economy. However, this recent report, following July’s inflation figure of a stubborn 3.8%, challenges expectations for another rate cut before winter. This suggests that speculations about immediate price cuts in short-term interest rates may need to be revised.Currency Traders and the Pound

For currency traders, this unexpected strength might support the pound. As the chance of another rate cut decreases, sterling may perform better against currencies from central banks still expected to ease policy. Options strategies to protect against a sharp drop in GBP or position for modest gains may now be more suitable. The outlook for UK stocks has become more complex, indicating higher volatility. While stronger economic growth is beneficial for company earnings, the ongoing weakness in manufacturing and reports of significant job cuts are concerning. With the UK unemployment rate already at 4.5% in Q2 2025, this tension between a robust service sector and a fragile industrial base could lead to unpredictable market movements, making volatility-focused options on the FTSE index more appealing. We must heed the report’s warnings about weak demand and sharply falling goods exports. Since early 2025, UK goods exports to the EU have declined by over 5%, significantly affecting manufacturers. As such, any investment strategies should be tactical, as the upcoming official inflation and labor market reports will be crucial in determining if this economic strength can be maintained. Create your live VT Markets account and start trading now.In August, manufacturing thrived, enhancing the eurozone economy, while services showed consistent growth trends.

The Eurozone’s August Flash Services PMI was slightly below expectations at 50.7, while the forecast was 50.8. However, the Manufacturing PMI surprised with a score of 50.5, well above the expected 49.5, marking the highest level in 38 months.

The Composite PMI also exceeded predictions, reaching 51.1 compared to the expected 50.7, mainly driven by strong performance in Germany. Employment continues to grow for the sixth month in a row, but price pressures are rising. Inflation remains below the average, which eases some worries.

Manufacturing Output Improvement

The manufacturing output index improved, hitting a 41-month high, even as cost pressures in the services sector increased. Despite challenges like U.S. tariffs and uncertainty, economic activity is gaining momentum, with both manufacturing and services experiencing growth. Germany is at the forefront of this manufacturing increase, while France seems to be stabilizing after facing difficulties. Trade policies are impacting foreign orders in the manufacturing sector, which declined for the second month in a row. Both Germany and France are grappling with foreign demand challenges, despite some signs of recovery. The unexpected strength in manufacturing is making the overall economy look better than expected. This may pose risks for those betting against European stock indices like the DAX. The robust manufacturing performance, the best in over three years, could be a good reason to consider buying call options or selling put spreads.Implications for the European Central Bank

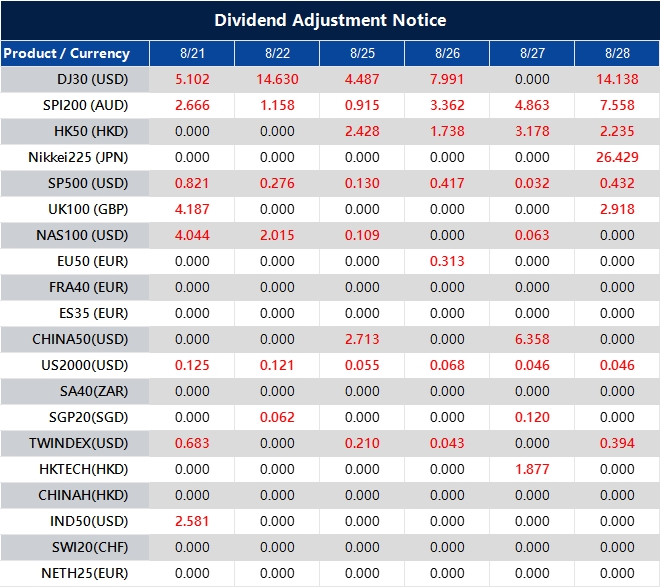

The rise in price pressures, especially in services, complicates the European Central Bank’s (ECB) outlook. Expectations for near-term interest rate cuts may need to be reconsidered, as the ECB remains focused on wage growth. Eurozone core inflation dipped to 2.8% last month in July 2025, but this report suggests it could become sticky, making interest rate swap markets interesting. The outlook for the euro is mixed, which is ideal for traders seeking volatility. Strong domestic data boosts the currency, but the decline in foreign orders linked to U.S. trade policy and the aftermath of the 2024 election cycle pulls it down. This situation hints that buying straddles or strangles on EUR/USD could be a smart strategy for potential big moves in either direction. It’s important to watch the gap between Germany and the rest of the Eurozone. With German manufacturing reaching a 38-month high, derivative plays favoring German industrial stocks over the broader Euro Stoxx 50 index may perform well. This aligns with Germany’s surprisingly strong factory orders data from June 2025, indicating relative strength that can be leveraged. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Aug 21 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

PMI data from France and Germany indicate that the ECB’s decision to pause in summer is reasonable and careful.

Recent PMI data from France and Germany shows that Europe’s largest economies are holding strong. This supports the European Central Bank’s (ECB) choice to pause interest rate changes throughout the summer. The stability is reassuring amid concerns about stagflation, as the euro area’s economy has improved compared to the fourth quarter of last year. While economic slowdown persists, it is not as prominent in discussions as one might expect.

In August, France faced increased inflation pressure, with input costs rising at the fastest rate since May. This trend affected various sectors, mainly due to wage increases and higher raw material costs. As a result, French companies raised their prices for the third month in a row. Similarly, in Germany, August saw a rise in both input and output cost inflation, following a slowdown in July. The service sector drove this increase, marking the highest input prices since March, while output price inflation reached a three-month peak.

Implications of Rising Price Pressures

These trends suggest a rise in price pressures, making the ECB cautious after summer. The ECB’s decision to pause on rate changes appears justified and may extend into the fourth quarter, with markets expecting only slight rate cuts by the end of the year. The latest August PMI data from France and Germany confirms economic resilience, supporting the ECB’s decision to hold interest rates steady through the summer. Germany’s composite PMI stands at 51.2, while France’s is at 50.8, placing both in the expansion zone. This strength reinforces the case for the ECB to stay cautious. More importantly, the reports show concerning inflationary pressures returning, with input costs and selling prices rising sharply. This corresponds with the Eurozone Harmonised Index of Consumer Prices for July 2025, which is at 2.5%, still above the ECB’s 2% target. These price increases will make the central bank wary of lowering rates too quickly.Market Reactions to Inflationary Pressures

The market is reacting, with expectations for interest rate cuts by the end of 2025 fading. Overnight Index Swaps now suggest only about 10 basis points of easing by year-end, a sharp shift from earlier predictions in the second quarter. This indicates that traders are moving away from bets on a 2025 rate cut. For derivative traders, this means that positions betting on lower rates, like long positions in Euribor futures, are increasingly at risk. The smarter strategy in the coming weeks is to prepare for a prolonged pause from the ECB, which may last the rest of the year. This could involve selling short-term interest rate futures to hedge against any sudden rate cuts. Given the uncertainty surrounding the ECB’s next move, we can expect increased volatility for options linked to the October and December policy meetings. This opens up opportunities for strategies that can benefit from a stable rate environment while protecting against unexpected changes. Betting on stable rates seems to be the main focus right now. We should remember the economic resilience shown during the winter of 2024-2025, which helped the Eurozone avoid the feared recession. This underlying strength, together with ongoing inflation, suggests that the ECB’s “higher for longer” approach is well-founded. Any derivative strategies should now align with this reality. Create your live VT Markets account and start trading now.Germany’s August manufacturing PMI exceeds expectations, signaling economic growth despite business challenges

Germany’s manufacturing PMI for August is 49.9, beating the expected 48.8 and improving from 49.1 last month. The services PMI came in slightly lower than expected at 50.1, down from 50.6 in July. Meanwhile, the composite PMI is 50.9, which is above the forecast of 50.2 and a slight increase from 50.6.

The manufacturing sector has shown growth for six months and has seen an increase in new orders. However, companies in this sector are cutting jobs, which may help improve productivity and competitiveness. Input prices have dropped due to lower oil prices and a strong euro, and some of these savings have been passed to customers.

Service Sector Challenges

On the flip side, the services sector is facing rising costs, mainly from higher wages. Companies are managing to pass on some of these costs to their clients. Manufacturing input inventories are falling, indicating reduced buying as companies remain cautious. This caution persists despite signs of recovery and challenges such as U.S. tariffs and global uncertainties. The unexpected strength in German manufacturing could benefit equities, especially the DAX index. The composite PMI’s growth gives reason for considering positive positions. This aligns with recent Destatis data showing that industrial production has stabilized in the second quarter of 2025. This strong data supports the euro against the U.S. dollar. A strong German economy may lead the European Central Bank to delay any expected interest rate cuts. We’re already noticing shifts in money markets, with the likelihood of a rate cut before the end of 2025 decreasing from 50% to below 30%.Implications for Bonds

We need to be careful with German government bonds, as strong growth and ongoing inflation in the service sector could push yields higher. The gap between falling factory prices and rising service costs, which official data revealed reached a 3.2% annual rate in July 2025, presents a complex situation. For now, unexpected economic strength may keep downward pressure on Bund prices. The contrast between a recovering manufacturing sector and a slowing services industry suggests chances for sector-specific trades. Industrial exporters might do better than domestically focused service companies, which are facing rising wage costs highlighted by recent union deals. This internal strife, along with continued corporate caution—like job cuts for productivity—might also lead to greater market volatility. The rise in new manufacturing orders to its highest level since March 2022 is particularly noteworthy. That period marked the start of significant geopolitical and economic uncertainty from events in Ukraine, which dampened sentiment for years. This latest data could indicate that we are finally breaking out of long-term industrial stagnation. Create your live VT Markets account and start trading now.August’s French PMIs show slight improvements, but economic challenges and weak demand remain amid cautious optimism

The latest data from HCOB, released on 21 August 2025, shows France’s flash services PMI at 49.7, slightly better than the expected 48.5. The manufacturing PMI is at 49.9, surpassing the predicted 48.0, and the composite PMI stands at 49.8 against an anticipated 48.5. These numbers mark 12-month highs for services and composite readings, and a 3-month high for manufacturing.

Despite these improvements, demand is still weak. New orders have dropped for the fifteenth month in a row, though this decline has slowed to the smallest rate in a year. Employment levels increased for the first time since last November. Even though the Composite PMI is still below the growth threshold, both the manufacturing and services sectors have seen less severe downturns, which offers a glimmer of hope.

Challenges in the Services Sector

The services sector is struggling, with few chances for quick recovery due to falling foreign demand. Although prices are stable, rising input costs could squeeze profit margins. The manufacturing sector faces issues from decreased competitiveness and protective policies. Changes in global supply chains may be causing longer delivery times, and while there wasn’t a repeat of a sharp drop in orders in August, producer sentiment remains low, as shown by a declining Future Output Index. The recent French PMI data exceeds expectations, indicating that the economy may be stabilizing after a long stretch of weakness. This brings some relief, especially following a small GDP contraction of 0.1% in the second quarter of 2025. However, with the European Central Bank keeping rates steady since their last meeting in July, any potential rally from this news may be limited, as overall growth is still fragile. For traders focused on the CAC 40 index, which is around the 8,200 mark, this report doesn’t hint at a big breakout soon. It’s worth considering selling out-of-the-money call options or using bear call spreads, as significant increases seem unlikely due to the ongoing weakness in new orders. This strategy lets us earn premiums while recognizing that the economy is stabilizing, not yet speeding up.Market Strategies and Uncertainty

The mixed signals in the report—improving employment alongside a falling Future Output Index—indicate that uncertainty remains high. Reflecting on the volatility spikes from late 2024, it’s smart to keep some downside protection. Buying affordable, out-of-the-money puts on the broader Euro Stoxx 50 index could be a sensible hedge against unexpected negative developments. In currency markets, this French data might temporarily support the Euro, but the overall sluggishness of the European economy remains unchanged. With Eurozone inflation at a persistent 2.8% in July 2025, the ECB has limited ability to stimulate growth, likely keeping the EUR/USD pair within a tight range. Strategies that profit from low volatility, like short strangles, could be useful in this setting. Create your live VT Markets account and start trading now.Gold stays within a range as it awaits Fed Chair Powell’s speech amid changing interest rate expectations and data

Gold is currently trading in a narrow range as traders await speeches and economic reports. There is uncertainty about interest rates, and the upcoming Non-Farm Payroll (NFP) report is likely to influence market predictions.

Recent economic data from the US showed mixed results. The Consumer Price Index (CPI) met expectations, but the Producer Price Index (PPI) was higher than forecasted, and jobless claims improved. Inflation expectations have also risen according to a University of Michigan survey.