Japanese central bank Governor Kazuo Ueda suggests interest rate hikes may be on the table if forecasts remain accurate

The Bank of Japan may raise interest rates if the economy and price levels develop as expected, says Governor Kazuo Ueda. Even with some global economic issues, growth continues at a steady pace.

Private consumption is strong, but rising prices are affecting households, highlighting the need to monitor economic trends closely. US tariffs are impacting manufacturers’ profits, but they do not significantly affect overall capital spending.

PBOC sets the USD/CNY reference rate at 7.0759, lower than previous figures

The People’s Bank of China (PBoC) has set the USD/CNY central rate for Monday at 7.0759. This is a change from Friday’s rate of 7.0789 and slightly above the expected 7.0709 from Reuters. The PBoC’s main tasks are to keep prices stable, encourage economic growth, and make financial reforms to develop the financial market.

The PBoC is owned by the People’s Republic of China and operates under the influence of the Chinese Communist Party. The Committee Secretary of the CCP, chosen by the State Council Chairman, has significant control over the PBoC. Currently, Pan Gongsheng holds both the governor and secretary roles.

Monetary Policy Tools

The PBoC uses a variety of monetary policy tools, more than those found in Western countries. These include the seven-day Reverse Repo Rate, the Medium-term Lending Facility, and the Reserve Requirement Ratio. China’s benchmark interest rate, the Loan Prime Rate, influences loan rates, mortgage rates, and savings interest, helping the PBoC manage the Chinese Renminbi’s exchange rates. China has allowed the establishment of private banks, with 19 currently in operation. Among these are major digital lenders WeBank and MYbank. These private lenders were permitted to compete in the largely state-controlled financial sector starting in 2014. Today, the PBoC set the yuan’s reference rate stronger than before, but it was still lower than market expectations. This suggests that the authorities are cautious, allowing some appreciation while managing the pace to prevent rapid increases. It indicates a strategy to maintain stability. This decision highlights a tension between improving domestic data and external pressures. November 2025’s Caixin Manufacturing PMI rose slightly to 50.9, indicating a modest but gentle economic recovery, which could support a stronger currency. However, the PBoC appears wary of a quick yuan strengthening, likely to keep its exports competitive during this recovery.Interest Rate and Currency Strategy

This careful strategy becomes clearer when compared to the US Federal Reserve’s policy, which aims to keep interest rates “higher for longer” through late 2025. The large difference in interest rates between the US and China continues to benefit the US dollar. The PBoC’s recent rate adjustment reflects this external pressure. Currently, with the rate around 7.07, we see a clear improvement from the rates of 7.20 to 7.30 that occurred at times in 2024. This suggests that there has been a steady, managed appreciation over the past year. For traders, this indicates that the central bank is unlikely to allow extreme fluctuations, helping keep the currency within a predictable range of gradual strength. Given this policy of managed stability, traders might consider strategies that take advantage of low volatility in the coming weeks. Selling short-dated USD/CNY strangles or straddles could be a smart move to earn premiums, betting on the exchange rate staying within a certain range. Caution is advised when buying outright options, as the PBoC’s actions may limit the sharp movements needed for such positions to be profitable. Create your live VT Markets account and start trading now.In November, AIB Manufacturing PMI in Ireland rose from 50.9 to 52.8

The AIB Manufacturing Purchasing Managers’ Index (PMI) for Ireland rose from 50.9 to 52.8 in November. This increase shows that the manufacturing sector is growing, indicating better conditions for expanding output.

The AIB PMI gives valuable information on aspects like production levels, new orders, and changes in employment. When the PMI is above 50, it suggests growth; when below 50, it indicates a decline. The current PMI reading of 52.8 implies that demand and activity among Irish manufacturers have improved since last month.

Impact on Irish Economy

As we move forward in the year, it will be important to monitor if this trend continues and how it may affect the overall Irish economy and monetary policy. The rise in Ireland’s manufacturing PMI to 52.8 signals stronger economic activity as we approach December 2025. This indicates solid growth and suggests that demand is increasing more quickly than expected. For traders, this news supports a positive outlook on Irish assets as we head into the end of the year. We might want to consider increasing our investment in the ISEQ 20 index, possibly through call options or futures contracts that expire in early 2026. This positive data stands out, especially when compared to the Eurozone Manufacturing PMI, which has struggled to stay above 50, last reported at 49.5. This difference suggests that Irish stocks could perform better than their European counterparts in the near future.Possible Implications for Traders

The strengthening Irish economy could help support the Euro. We are looking at opportunities in EUR/GBP call options, as this strong Irish data may reduce the European Central Bank’s inclination to signal future rate cuts. Recent UK growth figures have been weaker, creating a difference that FX traders can take advantage of. This rebound is significant given the economic slowdown experienced throughout much of 2024, when the PMI dropped into contraction territory. With the most recent Eurozone inflation estimate still slightly high at 2.3%, this strong Irish data could lead traders to believe there is less chance of an early rate cut by the ECB in 2026. As a result, we may see increased interest in interest rate swaps that bet on stable rates. Create your live VT Markets account and start trading now.During early Asian trading, gold rises to around $4,230 as expectations for a Fed rate cut increase.

Gold is currently priced at about $4,230, rising due to speculation around a potential interest rate cut by the US Federal Reserve in December. This speculation follows weaker US economic data and comments from Fed officials suggesting a more dovish stance. The CME FedWatch Tool shows nearly an 87% chance of a rate cut in December, up from 71% last week.

Interest rates influence the cost of holding gold, and lower rates can support this non-yielding asset. The US ISM Manufacturing PMI for November is expected to dip slightly from 48.7 to 48.6. If this number surprises and increases, it may strengthen the US Dollar and negatively affect gold prices since gold is dollar-denominated.

US and Ukraine Peace Talks Impact

In this context, ongoing peace talks between the US and Ukraine may lessen gold’s appeal as a safe haven. Gold is usually viewed as a protection against inflation and currency depreciation. It tends to move opposite to the US Dollar and risk assets, increasing when the Dollar weakens and when riskier markets decline. Central banks are adding more gold to their reserves, with a total of 1,136 tonnes added in 2022. Countries like China, India, and Turkey have notably increased their gold holdings. With gold trading above $4,230, we should keep an eye on the Fed’s anticipated rate cut announcement on December 10th. Recent US economic data supports this expectation, especially as November’s non-farm payroll numbers showed only 95,000 jobs added. The market reflects an 87% chance of a rate cut, driving our strategy. For derivative traders, this market suggests potential upside in gold. Purchasing call options on XAU/USD or gold ETFs could help us profit from the expected rally following the Fed’s decision. This strategy allows us to manage our risks if the Fed surprises the market by holding rates steady. We should also monitor today’s US ISM Manufacturing PMI release. A stronger PMI could briefly boost the US Dollar and lead to a temporary dip in gold prices. This pullback could create a good opportunity for us to increase our long positions ahead of the Fed meeting.Central Bank Demand and Historical Fed Changes

Looking ahead, central bank demand continues to support gold prices. According to the World Gold Council, central banks added another 250 tonnes to their reserves in the third quarter of this year. This ongoing institutional buying indicates resilience beyond short-term monetary policy shifts. Historically, a pivot by the Fed is very positive for gold. For instance, when the Fed shifted to an easing cycle in mid-2019, it led to a significant rally in gold prices. We believe a similar trend could happen in the coming weeks and into early 2026. The main risk to this positive outlook comes from reduced geopolitical tensions. Progress in peace talks between the US and Ukraine could decrease gold’s appeal as a safe haven. We should carefully watch for updates from the upcoming meeting in Moscow. Create your live VT Markets account and start trading now.AUD/USD stabilizes around mid-0.6500s after weak China PMI data

The AUD/USD pair is stabilizing around the mid-0.6500s after disappointing PMI numbers from China over the weekend. However, support comes from different expectations for Fed and RBA policies and a recent breakout above the 100-day SMA.

In November, China’s official Manufacturing PMI fell below 50.0 for the eighth consecutive month, signaling contraction. The Non-Manufacturing PMI dropped to 49.5, its lowest since December 2022, marking the first contraction in almost three years.

Market Reactions to China’s Economic Measures

The initial market reaction was brief, helped by easing trade tensions and government efforts to boost consumption in China. A weaker US Dollar and lowered expectations for RBA policy easing are strengthening the Australian Dollar. The USD Index is close to a two-week low, influenced by expectations of a Federal Reserve interest rate cut. Positive market sentiment is weakening the USD, benefiting riskier assets like the AUD/USD. Technically, the breakout above the 100-day SMA supports further gains for the AUD/USD. Traders are cautious and are looking forward to upcoming US economic data, such as the ISM Manufacturing PMI, for guidance. The NBS Non-Manufacturing PMI, which assesses China’s service sector, indicates trends based on figures above 50 for expansion and below 50 for contraction. The recent reading of 49.5 shows a downturn, affecting the Renminbi.Impact of Central Bank Policies

The AUD/USD is holding steadily just under the 0.6550 mark, demonstrating strength despite the disappointing Chinese economic data. The market is focused more on the contrasting approaches of the Reserve Bank of Australia and a Federal Reserve expected to cut interest rates. This difference in policies creates support for the currency pair. The main story is the weakness of the US Dollar, driven by increasing certainty of a Fed rate cut this month. Looking back at October’s inflation report, which showed US CPI cooling to 2.9%, futures markets now see over a 90% chance of a rate cut at the December 17th meeting. This expectation is putting pressure on the dollar and lifting risk-sensitive currencies like the Aussie Dollar. In contrast, the RBA is maintaining its position, as Australia’s inflation remains persistent, with the latest indicator showing a steady 3.8%. This divergence in policies—one central bank easing while the other holds—signals a bullish trend for the AUD/USD. It suggests that interest rate differences will increasingly favor the Aussie Dollar in the coming weeks. However, the Chinese data is still significant, as the Non-Manufacturing PMI’s drop to 49.5 indicates its first contraction since the recovery began in December 2022. Traders could consider buying call options to prepare for potential AUD/USD gains while protecting against a downturn linked to China’s economy. This strategy allows participation in a rally while limiting potential losses if the situation in China worsens. From a technical perspective, last Friday’s breakout above the 100-day simple moving average is a key bullish development. This level, around 0.6520, should now be seen as critical support. As long as the pair stays above this mark, the path of least resistance seems to lead toward the next major resistance level near 0.6650. Before making significant moves, traders should pay attention to the upcoming US ISM Manufacturing PMI data. A weaker-than-expected number would reinforce the slow growth narrative in the US, likely pushing the AUD/USD higher. Conversely, a surprisingly strong reading could result in a temporary pullback, presenting a better entry point for those betting on long-term trends. Create your live VT Markets account and start trading now.In November, Australia’s ANZ job advertisements increased to -0.8%, up from -2.2% previously.

ANZ job advertisements in Australia fell by 0.8% in November, an improvement from the previous decline of 2.2%. This suggests a slower drop in job ads and offers some hope for the job market.

In other news, silver prices reached record highs above $57.50. However, the Relative Strength Index (RSI) indicates it might be overbought, which could limit further gains for XAG/USD.

NZD/USD and GBP/USD Currency Movements

The NZD/USD stayed steady near a one-month high just below the mid-0.5700s, despite weak data from China. The GBP/USD remained around 1.3250, buoyed by a positive UK budget. China’s manufacturing PMI fell to 49.9 in November, below the anticipated 50.5, signaling contraction. The EUR/USD faced resistance near the 200-day Simple Moving Average (SMA) but stayed above 1.1600. In commodities, gold rose to $4,250 as expectations of a Federal Reserve interest rate cut weakened the US Dollar. However, notable crypto losers at the beginning of December included Zcash, Starknet, and Ethena, all showing further declines. Ripple’s price remained stable, trading between $2.15 and $2.30 for four consecutive days. This tight range suggests ongoing market uncertainty.The Impact of the Weak US Dollar

The market is currently focused on one main issue: the weak US Dollar. There are strong expectations for a Federal Reserve interest rate cut this month, which is benefiting other currencies and assets. This makes long positions in pairs like EUR/USD, which is climbing above 1.1600, a key focus for the next few weeks. This sentiment is backed by a steady decrease in US inflation since its peaks in 2024, with the latest Core PCE reading at 2.8%. Although the labor market continues to add jobs, the pace has slowed to an average of 150,000 per month in the latter half of this year, allowing the Fed to ease its policies. This data strengthens the notion that we should not oppose the Fed’s dovish stance. In Australia, the job market shows slight improvement, with job ads down only 0.8% in November compared to a 2.2% drop earlier. However, we need to be cautious about the Australian dollar’s strength. Weak manufacturing data from China, a major trading partner, may limit any significant rallies. The slow GDP growth of 0.2% observed in the third quarter of 2025 reinforces this cautious perspective for Australia. This slow growth environment makes it difficult to support aggressive long positions on the Aussie dollar, even with a weak US Dollar. Strategies like call spreads on the AUD/USD might help manage risk. For traders looking to capitalize on the weak dollar theme, commodities are a promising area. Silver has hit a record high over $57.50, and gold is pushing past $4,250. Using call options on gold and silver ETFs could provide upside exposure while managing the risk of a potential short-term pullback. A clear divergence trade is forming against the Japanese Yen. While we anticipate rate cuts from the Fed, the Bank of Japan is openly discussing rate hikes. This policy difference suggests that shorting the USD/JPY pair, possibly using futures or put options, could be a compelling strategy in the coming weeks. Create your live VT Markets account and start trading now.Australia’s company gross operating profits for the third quarter were 0%, falling short of expectations.

In the third quarter, companies in Australia reported no change in gross operating profits, which was below the expected growth of 1.7%. This indicates a stagnant period for businesses, despite hopes for profit increases.

Gold prices have jumped to $4,250, fueled by speculation about a Federal Reserve rate cut, which has weakened the US Dollar. At the same time, the GBP/USD pair remains stable as UK traders consider the recent Autumn Budget and potential future decisions from the Fed regarding interest rates.

November Market Movements

In November, the markets experienced unpredictable movements, keeping traders on their toes. Ripple has remained in a narrow trading range of $2.15 to $2.30 for several days, showing a struggle between opposing market forces. Upcoming economic data, including ISM PMIs, ADP employment figures, and core PCE inflation, will likely influence market expectations. Key indicators to monitor include Eurozone CPI, Australian GDP, and Canadian employment data. For those planning future market strategies, choosing the right brokers is crucial, especially those offering high leverage and swap-free accounts in regional markets. This highlights the need for thorough research and awareness of market risks.US Dollar and Federal Reserve Expectations

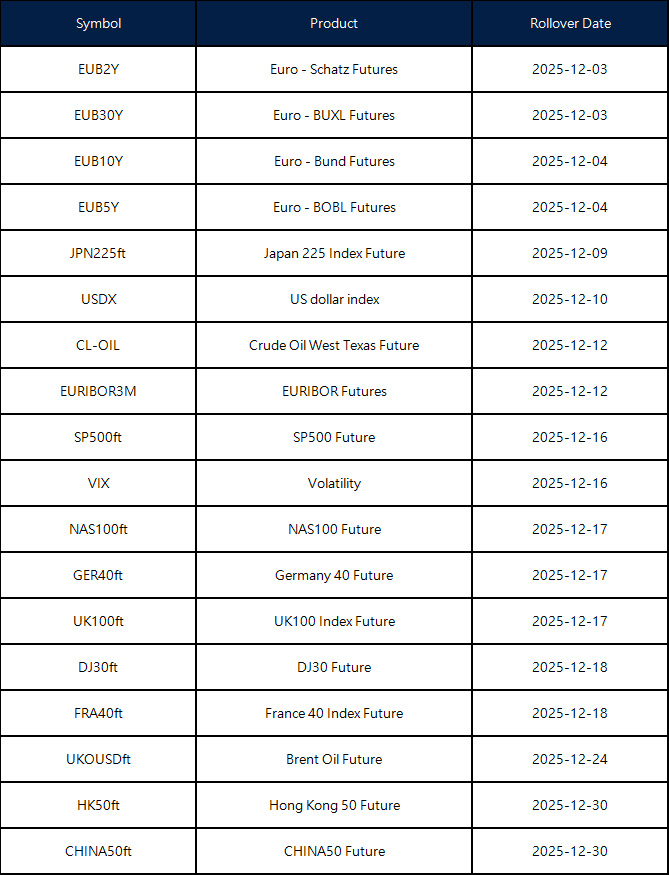

With the US Dollar showing general weakness, there are strong expectations for a Federal Reserve rate cut in December. The market is pricing in an 85% chance of a 25-basis point cut, the first since major policy changes in the early 2020s. This dovish outlook is driving current liquidity and risk appetite. Traders should closely watch the EUR/USD pair as it tests the 200-day Simple Moving Average just above the 1.1600 mark. A consistent break above this level could lead to increased buying interest, making call options appealing. This trend is a direct result of a weak US Dollar sentiment in the currency markets. The environment for precious metals remains very bullish, with Gold testing the $4,250 level, a significant increase compared to late 2024. This rise is driven by expectations of lower interest rates, which makes holding non-yielding bullion more attractive. While Gold’s ascent is strong, Silver’s recent rise to a record high above $57.50 raises concerns. The Relative Strength Index (RSI) is now heavily overbought, suggesting the rally may be overextended and at risk of a sharp correction. Traders may want to take profits or hedge long positions with put options, as a correction could be near. Looking at the Asia-Pacific region, the outlook appears less optimistic, presenting potential bearish opportunities. Australian company profits stagnated with 0% growth in Q3 2025, falling short of the expected 1.7%. This follows a reported 0.2% GDP growth by the Australian Bureau of Statistics for the second quarter, indicating a slowing economy. This weakness is compounded by disappointing data from China, Australia’s largest trading partner. China’s manufacturing PMI for November dropped to 49.9, marking three consecutive months of contraction. For derivatives traders, the combination of poor domestic profits and negative external demand strengthens the case for shorting the Australian Dollar, perhaps through futures or put options on AUD/USD. In contrast, the Bank of Japan is hinting at a possible rate hike if its economic forecasts hold. This divergence between a dovish Fed and a potentially hawkish BOJ creates an interesting opportunity. Traders should consider strategies that favor a stronger Japanese Yen against a weaker US Dollar, such as shorting the USD/JPY currency pair. Create your live VT Markets account and start trading now.December Futures Rollover Announcement – Dec 01 ,2025

Dear Client,

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

In November, Japan’s Jibun Bank Manufacturing PMI reported 48.7, missing expectations

Japan’s Jibun Bank Manufacturing PMI fell to 48.7 in November, which was below the expected 48.8. This indicates a shrinkage in the manufacturing sector, as any score under 50 shows reduced activity.

China’s Ratingdog Manufacturing PMI also dropped to 49.9, short of the anticipated 50.5. Meanwhile, GBP/USD stayed steady around 1.3250 after some relief measures in the UK budget.

Silver Price Surge

The price of silver soared past $57.50, though gains may be limited due to a high RSI. Also, the EUR/USD is testing the 200-day SMA resistance, trading above 1.1600 during a period of overall USD weakness. In other news, the Federal Reserve’s expectations for interest rate changes pushed gold prices above $4,250. Despite some market turbulence, Ripple saw low on-chain activity and whale selling, keeping its trading pattern stable. The market is now expecting Federal Reserve rate cuts, which weakens the US dollar. Recent US inflation data has cooled to 2.5%, and the last jobs report showed a disappointing increase of only 110,000 jobs, giving the Fed a clear path to ease its policy. This situation makes strategies betting against the dollar a straightforward choice as we approach the year’s end.Manufacturing Data and Global Slowdown

Today’s manufacturing data from Asia suggests a global slowdown. With Japan’s PMI at 48.7 and China’s at 49.9, the industrial sectors in these countries are struggling. This follows a trend we have observed for months, echoing fears of a slowdown that affected markets in late 2023. The most compelling opportunity comes from the differing policies of the US and Japan. While the Fed is set to cut rates, Bank of Japan Governor Ueda is hinting at rate hikes, continuing the normalization that started when negative rates ended in 2024. This fundamental difference makes selling USD/JPY futures or buying Japanese Yen call options an appealing strategy. Gold and silver benefit from a weak dollar and growing economic uncertainty. Silver’s rise above $57.50 is remarkable, and gold has surpassed $4,250, well above the previous high of around $2,450 seen in 2024. Given the current overbought conditions, using call spreads could enable further gains while limiting risk in case of a sharp price drop. Overall market volatility is increasing as these issues unfold. The VIX index has risen steadily from the low teens to over 18 in the past month, showing growing anxiety about the Fed’s next moves and the severity of the slowdown in Asia. This heightened volatility makes options-based strategies, such as buying straddles on major currency pairs like EUR/USD, a smart way to trade the anticipated price swings. Create your live VT Markets account and start trading now.In November, South Korea’s S&P Global Manufacturing PMI remains steady at 49.4

The South Korean S&P Global Manufacturing Purchasing Managers’ Index (PMI) stayed the same at 49.4 in November. This indicates that the manufacturing sector continues to shrink since it remains below the neutral mark of 50.

The stable PMI shows ongoing challenges in the manufacturing industry, with continued pressure from low demand and production.