Japan’s tertiary industry index matches expected 0.3% increase for the month

Japan’s Tertiary Industry Index increased by 0.3% in September, which meets expectations. This index measures how well Japan’s service sector is performing.

In the UK, the GBP/JPY dropped from 204.00 due to concerns about finances and reduced expectations from the Bank of England. The Pound weakened further after reports that the UK government is reconsidering its plan to raise income tax rates.

US Dollar Index hovers around 99.15 amid doubts about a Federal Reserve rate cut

The US Dollar Index dropped to about 99.15 during the Asian trading session on Friday. Traders have lowered their expectations for a Federal Reserve rate cut in December. This change comes after Fed official Collins said the policy rate would likely stay steady for a while.

President Donald Trump’s decision to sign a funding package has ended a 43-day government shutdown. However, this is expected to bring weak economic data, which might weaken the USD. Currently, financial markets see a 51% chance of a Fed rate cut in December, down from 62.9% the day before.

Impact Of Fed Remarks

The Dollar’s decline is somewhat controlled by hawkish comments from Fed officials, who support keeping rates steady to manage inflation and employment risks. Ongoing discussions about the US economy and missing data are putting additional stress on the Dollar’s value. The US Dollar (USD) remains the most traded currency in the world, making up over 88% of all foreign exchange transactions. The Federal Reserve’s control over interest rates has a significant effect on the value of the USD. Generally, rate hikes strengthen the currency, while rate cuts tend to weaken it. Changes in quantitative easing also significantly impact the USD. Right now, there is a struggle for the US Dollar, creating a unique trading environment. On one side, Federal Reserve officials are suggesting rates will stay high to combat inflation. On the other side, there’s an expectation of weak economic data due to the recent government shutdown. This uncertainty before the release of delayed data indicates an opportunity for volatility plays. The latest weekly jobless claims were 245,000, suggesting a weakening labor market that the Fed may not fully recognize. Using options to prepare for a substantial move when the official employment and growth figures are finally released could be a wise strategy.Historical Context And Trading Strategies

We saw a similar situation after the 35-day shutdown in the winter of 2018-2019, which led to an estimated 0.2% drop in GDP the next quarter. Traders are now anticipating a similar or even greater impact, which could cause the dollar to fall if confirmed. This makes buying puts on the dollar index or call options on currencies like the Euro an appealing idea. However, the Fed’s caution is understandable, making it important to hedge any directional bets. The latest Core PCE inflation reading for September 2025 was 3.1%, still above the 2% target, giving supporters of steady rates like Collins justification to maintain their stance. The market appears divided, with the CME FedWatch Tool indicating it’s a toss-up for a rate cut in December. For derivative traders, strategies that benefit from significant price movements, regardless of direction, are especially enticing in the coming weeks. Positioning for a spike in volatility around the delayed data releases is crucial, rather than committing to a single direction. The current tension between a hawkish Fed and a potentially weakening economy is unlikely to resolve smoothly. Create your live VT Markets account and start trading now.Oil prices rise, strengthening CAD and keeping USD/CAD around 1.4020 during Asian trading

USD/CAD dropped to about 1.4020 during Friday’s Asian trading session, influenced by rising oil prices and concerns about the US economy. Canada’s status as the top crude exporter to the US helped strengthen the CAD.

WTI oil prices climbed to $59.50, up more than 1.5%, after a drone strike in Ukraine hit a Russian oil depot, causing damage to three apartments, an oil facility, and various coastal structures.

Concerns About the US Economy

The USD/CAD exchange rate also faced pressure due to US economic worries, even after the government shut down ended. Kevin Hassett raised caution about potential gaps in October’s data, as some agencies were unable to collect information. On the other hand, the US dollar might gain strength from cautious comments from Federal Reserve officials, which lowered the chances of a December rate cut. The CME FedWatch Tool shows nearly a 50% chance of a 25-basis-point cut this December, down from 69% earlier. St. Louis Fed President Alberto Musalem advised caution, noting that there is limited ability to ease. Minneapolis Fed President Neel Kashkari emphasized that inflation remains high at 3%. Early October reports suggest a cooling labor market and declining consumer confidence in the US. As we approach mid-November 2025, USD/CAD struggles to stay below the 1.4050 resistance level. The Canadian dollar benefits from high oil prices, especially considering Canada’s role as a major crude supplier to the US. This situation indicates that any strength in the US dollar may be limited against the loonie.Effect on USD/CAD Trading Strategies

West Texas Intermediate crude is a key factor in pricing, currently around $82 a barrel. This strength comes from ongoing geopolitical tensions, including recent drone strikes in Ukraine that targeted Russian oil facilities. For derivatives traders, the persistent rise in oil prices supports strategies favoring a stronger Canadian dollar. Conversely, the US dollar faces challenges amid mixed economic signals. The latest jobs report for October showed a cooling labor market, while recent CPI data revealed that core inflation remains stubbornly above 3%. This confusion complicates the Federal Reserve’s plans, making significant gains in USD/CAD difficult. The Fed stated it requires evidence of a stable return to 2% inflation before making any policy changes. At the last FOMC meeting, the narrative of “higher for longer” was reinforced. The CME FedWatch Tool now indicates that the market is hardly expecting a 25-basis-point rate cut before the second quarter of 2026, leading to a cautious outlook for the US dollar. Given this climate, selling call options on USD/CAD with a strike price above 1.4050 may be a sound strategy in the weeks ahead. The strong resistance at this level, along with supportive oil prices for the CAD, suggests a ceiling that could hold. Traders will be watching closely for any changes in Fed commentary or significant shifts in the energy market. Historically, the 1.4000 level has been an important psychological level for this pair, particularly during uncertain times, such as the 2020 global shutdown. With the current mixed forces, establishing option strangles could also be wise for those anticipating a breakout from this tight range. This strategy would allow traders to profit from volatility spikes, whether the pair moves sharply up or down. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Nov 14 ,2025

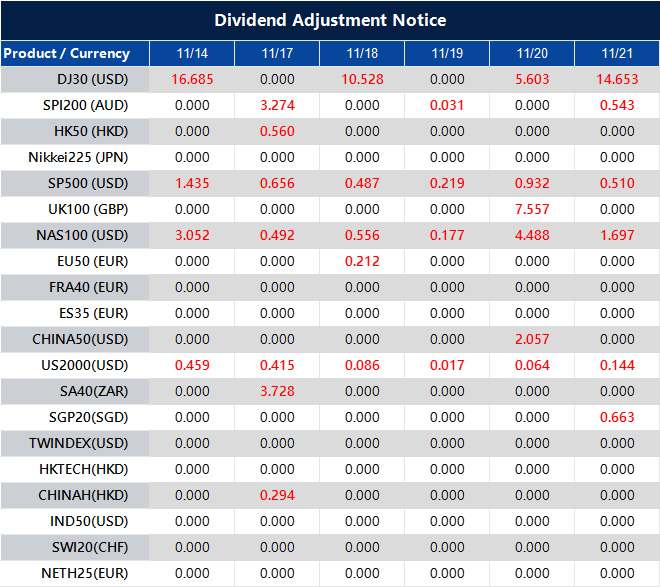

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

WTI nears $60 following Ukrainian drone attack on Russian oil depot

West Texas Intermediate (WTI) Oil has nearly reached $60.00 after a Ukrainian drone strike hit an oil depot at Russia’s Black Sea port in Novorossiysk. During Asian trading hours, WTI prices climbed over 2%, hitting around $59.90. Lukoil PJSC is reducing staff just days before new US sanctions, set to take effect on November 21. These events may leave about a third of Russia’s seaborne oil exports stranded due to delays in rerouting.

Despite the increase in oil prices, there are concerns about potential oversupply. The International Energy Agency (IEA) warns that production could exceed demand by 2.4 million barrels this year and 4 million next year. OPEC and OPEC+ members, including Russia, have boosted production since April. Supply from the US and Brazil adds to oversupply worries. According to OPEC’s report, there could be a small surplus of around 20,000 barrels per day next year.

WTI as a Market Benchmark

WTI Oil is a key market benchmark, known for its light and sweet qualities. The price of oil depends on various factors, such as supply and demand, global economic growth, political events, and OPEC’s production decisions. Reports from organizations like the API and EIA also influence WTI prices. Changes in OPEC’s production quotas can lead to fluctuations in WTI prices. The drone strike on Russia’s Novorossiysk port has pushed WTI crude close to $60, presenting a short-term buying opportunity. This situation reflects similar supply disruptions from early 2024, which caused price spikes of 5-7% in the following weeks. This incident serves as a catalyst for price increases before fundamental factors take over. With new US sanctions on Russian oil effective November 21, supply pressure will likely rise significantly. Major buyers such as India and China are already halting their purchases, which could leave a substantial amount of crude stranded. This creates a genuine supply crunch, making call options with expirations in late November and early December particularly appealing to traders who anticipate rising risks.Immediate Tension vs. Long-Term Pressure

Nevertheless, we must acknowledge the strong bearish factors looming ahead. The IEA projects a large supply glut of 4 million barrels per day by 2026. Recent data shows that US crude production recently hit a record 13.5 million barrels per day, which reinforces this trend. This clash between immediate geopolitical tension and long-term oversupply suggests we may face a period of high volatility. OPEC+ has been increasing production since April 2025, which weakens the cartel’s historical role in stabilizing prices. The interplay of short-term supply shocks and long-term surpluses has caused a 15% increase in implied volatility for oil options this week, making strategies like straddles appealing for trading expected price swings without committing to a specific direction. Create your live VT Markets account and start trading now.NZD/USD remains strong above 0.5650 during Asian trading hours, despite mixed data from China

The NZD/USD pair remains strong, trading above 0.5650 during Asian hours. This stability comes after mixed economic data from China for October. Retail Sales rose by 2.9% year-on-year, which was better than expected, but growth has slowed for the fifth consecutive month. Industrial Production increased by 4.9% year-on-year, but this didn’t meet market expectations. Despite these numbers, the Kiwi’s value has not been greatly affected because it often reflects the state of the Chinese economy.

Recently, the Reserve Bank of New Zealand (RBNZ) lowered its Official Cash Rate by 50 basis points to 2.5%. This decision stems from concerns about a weakening economy, highlighted by a nearly nine-year high unemployment rate of 5.3%. Such conditions might lead to further rate cuts, putting additional pressure on the NZD against the USD. On the other hand, the US government shutdown has ended after President Trump signed a funding bill, leading to the release of previously delayed economic data. Analysts believe these reports might reveal weaknesses in the US labor market, which could impact the USD.

Factors Influencing The NZD

The value of the New Zealand Dollar (NZD) is influenced by various factors. These include the health of New Zealand’s economy, the central bank’s policies, and China’s economic performance. Prices of dairy, a major export for New Zealand, also affect the NZD. Market sentiment is crucial too; a positive risk environment tends to support the Kiwi. Currently, the NZD/USD is around 0.5675, although its position seems fragile following China’s October data. While Industrial Production exceeded forecasts, Retail Sales fell short, indicating a hesitant consumer recovery. Since China is New Zealand’s largest trading partner, this mixed data does not give a clear lift to the Kiwi. On the domestic front, we believe the RBNZ may consider cutting interest rates further due to a struggling economy. New Zealand’s unemployment rate has recently climbed to 4.2%, and the GDP growth for Q3 2025 was weak, supporting the case for lowering the Official Cash Rate from 5.0%. A similar, though more aggressive, rate-cutting cycle occurred in 2019 when economic challenges emerged.US Dollar Support

In contrast, the US Dollar is gaining strength from a solid American economy. The October 2025 non-farm payroll report showed over 200,000 new jobs that far exceeded expectations, while core inflation remains stubbornly above 3%. This situation suggests that the Federal Reserve might maintain higher interest rates for a longer period, leading to a growing policy gap between it and the RBNZ. For derivative traders, this increasing divergence signals potential weakening of the NZD/USD pair in the upcoming weeks. There could be value in purchasing put options with strikes below 0.5600, targeting expirations for late December 2025 or January 2026. This strategy allows for the opportunity to profit from a possible decline while managing risk in case the pair unexpectedly rises. This scenario is reminiscent of 2014-2015, when a slowing China and a stronger US policy outlook resulted in a notable drop in the Kiwi. We also need to keep an eye on dairy prices, which have decreased in recent Global Dairy Trade auctions, putting further pressure on the NZD. Positive surprises from Chinese data or a sudden dovish shift from the Fed are the main risks to this outlook. Create your live VT Markets account and start trading now.Retail sales in China rose by 2.9% year-on-year, and industrial production increased by 4.9%.

AUD Strength Against Yen

China’s October retail sales grew by 2.9% compared to last year. This was slightly higher than the 2.7% forecast but lower than September’s 3.0%. Industrial production rose by 4.9%, missing the 5.5% prediction and down from 6.5% earlier. Fixed asset investment fell by 1.7% year-to-date, worse than the expected decline of 0.8%, compared to September’s 0.5%. Despite this mixed data, the Australian Dollar remained stable. The AUD/USD pair rose by 0.18% to 0.6541. The Australian Dollar also gained strength against the Japanese Yen this week. In currency movements, the AUD rose against the CAD, NZD, and JPY but fell against the USD, EUR, GBP, and CHF.Chinese Economic Impact on AUD

China’s retail sales and industrial production are essential indicators of consumer spending and industrial output. These figures can influence the Australian Dollar because of the close trade relations, especially since China is Australia’s largest trading partner. China’s economic performance affects Australia’s export volumes, which, in turn, impacts demand for the currency. As of November 14, 2025, the latest data from China shows a mixed but troubling situation. The shortfall in industrial production is particularly concerning, hinting at a slowdown in the manufacturing sector, which is crucial for regional growth. Although retail sales remain steady, weaker industrial output and fixed asset investment indicate a slowing economic recovery. This situation leads to a cautious outlook for the Australian Dollar. With China being Australia’s top export market, a slowdown there directly reduces demand for key commodities. Recent data from major commodity exchanges shows iron ore prices have dropped to around $110 per tonne, down from the $130-$140 range seen in early 2024. The market’s initial muted response to this data may create opportunities for derivative traders in the coming weeks. We see the fundamental outlook for the AUD weakening, making strategies that benefit from a decline in the currency more appealing. This could include purchasing put options on the AUD/USD or taking short positions in AUD futures contracts. The external pressures from China add complexity to the Reserve Bank of Australia’s (RBA) outlook. The RBA has maintained its cash rate at 4.35% for two full years, since November 2023. A decline in demand from its largest trading partner makes future rate hikes unlikely, raising the possibility of rate cuts for 2026. Now, we are focusing on the upcoming high-frequency data for further confirmation of this slowing trend. We will closely monitor the upcoming Caixin Manufacturing PMI from China. Another weak reading could strengthen bearish sentiment and may lead to a more significant drop in the AUD/USD, potentially heading towards the 0.6400 level. Create your live VT Markets account and start trading now.China’s industrial production growth missed expectations, registering 4.9% instead of the predicted 5.5%

In October, China’s industrial production grew by 4.9% compared to last year, which is below the expected 5.5%. This decline raises concerns in the global financial markets, affecting currencies and commodities.

The Japanese yen is close to a nine-month low against the US dollar, as doubts linger about the Bank of Japan’s potential interest rate increases. At the same time, gold prices have been fluctuating, gaining attention as economic worries impact the US dollar and reduce expectations for a Federal Reserve rate cut in December.

Commodities And Cryptocurrencies

Commodities like orange juice are attracting market interest due to differing investment views. Solana (SOL) has dropped to a five-month low, falling over 13% amid weakening sentiment and ETF inflow data. Bitcoin, Ethereum, and Ripple have also seen declines, with weekly losses over 5%, 10%, and 2%, respectively. As selling pressure increases, these cryptocurrencies are at risk of further losses, with Bitcoin even slipping below $100,000. In light of these developments, there’s growing interest in broker choices, with many guides discussing the best brokers for 2025. These guides include top-regulated brokers and those offering the MT4 platform. China’s lower-than-expected industrial production points to trouble for global growth. With growth at 4.9% compared to the 5.5% forecast, we expect decreased demand for commodities. China is the largest consumer of industrial metals, accounting for over 50% of global copper use, indicating bearish pressure on industrial activity-related assets.Opportunities In Currency Markets

Given this slowdown, there’s a strong opportunity to short the Australian dollar. Australia’s economy heavily relies on China, which has purchased over 30% of its exports in recent years, mainly iron ore and coal. This close link suggests that using AUD/USD put options or shorting AUD futures could be smart strategies in the coming weeks. Additionally, the widespread risk-off sentiment, driven by crypto weakness and UK political concerns, signals that market volatility may increase. Historical data shows that during high uncertainty, like in 2020, the VIX index can soar above 50. We recommend buying VIX call options as a way to hedge against and possibly profit from this expected volatility. The weakness of the Japanese yen offers another trading opportunity, as the Bank of Japan seems reluctant to raise rates from 0.5%. This difference in policy compared to other major central banks is favorable for carry trades. Holding long positions in pairs like USD/JPY could leverage the attractive interest rate differential. We are also cautious about the British pound due to rising fiscal concerns. The UK’s debt-to-GDP ratio is close to 100%, and any signs of unfunded government spending could remind investors of market chaos in late 2022. Therefore, we anticipate further weakness in the pound, making shorting it against the euro a reasonable strategy. While gold benefits from a flight to safety, its upward movement may be limited by cautious expectations for a December Fed rate cut. Gold usually performs well when real yields drop, but a strong stance from the Fed may keep gold prices below recent highs. We advise approaching long gold positions carefully, possibly using call spreads to manage risk. Create your live VT Markets account and start trading now.Retail sales in China surpass expectations, growing 2.9% instead of the anticipated 2.7%

China’s retail sales increased by 2.9% in October compared to last year, beating the expected 2.7% rise. This indicates a positive trend in consumer spending.

At the same time, the USD/INR exchange rate fell as the US dollar weakened ahead of upcoming economic reports. The EUR/GBP climbed above 0.8850 due to worries about the UK’s financial health and poor GDP data.

Euro and Commodity Developments

The EUR/CAD pair approached 1.6250 as the European Central Bank signaled a careful stance on interest rates. Meanwhile, the Australian dollar strengthened while the US dollar declined due to concerns over upcoming data releases. Silver prices also rose, with XAG/USD moving above 52.50 amid uncertainty around US economic data. The Japanese yen gained against the weakening USD, though its potential for further gains is limited. Bitcoin, Ethereum, and Ripple saw significant drops, losing over 5%, 10%, and 2%, respectively, throughout the week. Bitcoin fell below $100,000, reflecting the current bearish market trends.Market Risk and Strategic Outlook

The markets are showing a risk-off attitude, influencing our strategy for the upcoming weeks. Gold has climbed back above $4,200 an ounce, while speculative assets like Bitcoin have fallen below the critical $100,000 support. This trend suggests that traders are looking to lower their risk as the year comes to a close. The US dollar is weakening due to recent economic concerns, impacted by October’s disappointing jobs report and a slight cooling in inflation data (CPI). The market is now less likely to expect a Federal Reserve rate cut in December, with futures indicating only a 35% chance, down from over 60% last month. This situation creates uncertainty, suggesting we might use options to leverage volatility in pairs like EUR/USD, which is currently trading below its 50-day moving average. China’s better-than-expected retail sales growth of 2.9% offers a glimmer of hope for global growth. This small improvement from the sluggish third quarter of 2025 might support commodity-linked currencies. We see potential in pairing the Australian dollar against currencies facing domestic challenges, such as the British Pound. With the UK government recently deciding to halt tax increases, fiscal uncertainty is heavily impacting the Pound Sterling. We should expect further weakness in pairs like GBP/USD as markets question the country’s financial discipline. This makes buying GBP puts or taking short positions an appealing strategy through the end of November. Create your live VT Markets account and start trading now.China’s fixed asset investment for the year was recorded at -1.7%, below expectations.

China’s fixed asset investment fell by 1.7% year-on-year (YoY) in October, which is worse than the expected decrease of 0.8%. This shows a decline since the start of the year, contradicting earlier predictions.