The Canadian dollar strengthens against the US dollar, nearing 1.4100 ahead of Macklem’s speech.

The USD/CAD exchange rate dropped to about 1.4100 during the early European session on Thursday. This marks the end of a five-day upward trend, driven by rising crude oil prices that support the Canadian Dollar. Canada is set to release its October Ivey PMI data today, and the Bank of Canada Governor will also be speaking.

JPY remains resilient against a weaker USD amid uncertainty from the BoJ and fiscal concerns.

The Japanese Yen is gaining against a weaker US Dollar as the European trading session begins. Minutes from the Bank of Japan’s September meeting hint at a possible interest rate increase and talk of government action to support the Yen.

Barriers To Yen Gains

Japan’s new Prime Minister plans to boost spending without tightening policies, which poses a challenge for the Yen. The US Dollar has stayed strong since May due to the Federal Reserve’s actions, limiting how much the USD/JPY pair can drop. The BoJ minutes show a careful stance due to inflation worries, while Japan’s top currency official points out that Yen movements are straying from basics. Sanae Takaichi backs fiscal spending, which reduces aggressive bets on the Yen. ADP reported a rise of 42,000 jobs in the US private sector for October. Even with solid ISM Non-Manufacturing PMI data, the ongoing US government shutdown is affecting the USD, putting pressure on the USD/JPY pair. The USD/JPY pair faces resistance near 154.40-154.45, while support levels hover around 153.65 and 153.00-152.95. Further drops could push it toward the 152.55-152.50 zone or lower.Federal Reserve Impact

The Federal Reserve adjusts interest rates to manage inflation and employment, influencing the USD. They use Quantitative Easing and Tightening to ensure economic stability, affecting the currency’s strength. The ongoing tension between the Bank of Japan and the Federal Reserve is still a key factor for USD/JPY, similar to the past. The pair is currently trading around 158.20, raising speculation of direct intervention from Japanese officials. Concerns about Yen weakness have been present even when the pair was at lower levels. Discussions about a potential Bank of Japan rate hike eventually led to action, resulting in a current policy rate of 0.25%. However, the slow pace of these hikes—only three small increases since early 2024—has not significantly changed the wide interest rate gap with the US. This is why the Yen remains under pressure even after the BoJ left its negative interest rate policy over a year ago. On the US side, the previously aggressive Fed stance has softened as 2025 approaches. With the Fed funds rate at 4.75% and US unemployment rising to 4.2%, the market is now anticipating rate cuts rather than hikes. The risk of economic instability from political conflicts, like the government shutdown affecting the outlook before, remains a concern for Dollar bulls. For derivative traders, this situation suggests focusing on volatility and downside protection for the USD/JPY pair. Buying put options can safeguard against a significant drop, possibly caused by Bank of Japan intervention or unexpected dovish moves from the Fed. Selling out-of-the-money call options could generate income, but it carries risk if the Yen falls below the 160 level. The psychological level of 160 now serves as a significant barrier, more challenging than the 155-156 range monitored in previous years. A clear drop below 157 could signal a deeper pullback, prompting traders to target the 155 level as the next major support zone. This makes the current range especially sensitive to central bank announcements in the coming weeks. Create your live VT Markets account and start trading now.Australian dollar gains as US dollar weakens amid reduced Fed rate cut expectations

The Australian Dollar has strengthened against the US Dollar, posting gains of over 0.25% in a recent session. This rise came after data revealed that Australia’s trade surplus grew to 3,938 million MoM in September, exceeding expectations of 3,850 million and up from a previous figure of 1,111 million.

Meanwhile, the US Dollar is weakening as the chances of a Federal Reserve rate cut decrease. The US Dollar Index (DXY) has continued to decline, trading around 100.00, despite positive US economic reports. In October, the ADP Employment Change increased by 42,000, surpassing forecasts, and the ISM Services PMI rose to 52.4.

Federal Reserve Rate Cut Expectations

The probability of a Fed rate cut in December has dropped to 62% from 68% just a day before. This shift is influenced by Fed Chair Jerome Powell’s careful stance and the ongoing US government shutdown. Additionally, the White House has announced that China will pause some tariffs in return for US concessions, which affects trade dynamics. Technical analysis shows the AUD/USD pair stabilizing around 0.6500. Depending on market trends, it may test either lower or higher levels. Gains in the Australian Dollar also reflect global economic conditions and trade relations, especially with China, which play a role in currency movements. The Reserve Bank of Australia is maintaining its interest rates. Recent Q3 2025 inflation data revealed core prices remain high at 3.8% year-over-year. This strong position, along with the unexpectedly large September trade surplus, supports the Australian dollar. These domestic factors suggest the currency will remain strong in the near future. However, we need to keep an eye on China, as it poses the greatest risk for long AUD positions. While China has shown positive signals regarding agricultural tariffs, its manufacturing PMI for October fell to 50.6, and state-owned companies are advised to avoid foreign chips. These ongoing tensions and economic slowdowns could limit any significant gains in the AUD, especially with iron ore prices fluctuating around $125 per tonne.US Dollar Vulnerability and Trading Strategies

Conversely, the US dollar appears vulnerable as the government shutdown moves into its eighth week, creating economic uncertainty. The market has raised expectations for a December rate cut, with fed funds futures now indicating a 75% probability, up from 62% last week. This anticipation of looser policy adds pressure on the greenback. Given these contrasting factors, the AUD/USD pair is tightly consolidating near the 0.6500 level, setting up a classic situation for range-bound trading strategies in the short term. For derivative traders, this means selling options through iron condors or credit spreads could be a smart move, allowing them to collect premiums while the market decides its direction. Yet, with pressure mounting from both central banks, a breakout seems likely. We are also considering strategies that could benefit from a rise in volatility, such as long straddles or strangles, which would profit from sharp moves in either direction. A decisive drop below the 0.6460 support level could lead to a move towards the August 2025 lows, while a rise above the 0.6630 resistance could bring the pair back to its September 2025 highs. The key will be positioning for the upcoming—and likely sharp—resolution of this current indecision. Create your live VT Markets account and start trading now.USD/CHF pair fights to keep upward momentum, currently around 0.8095

The USD/CHF pair is struggling to keep its rally above the 11-week high of 0.8125 and has dipped slightly to about 0.8095 during late Asian trading. This pause follows a retracement in the US Dollar after the release of US ADP Employment Change and ISM Services PMI data for October.

The US Dollar Index, which measures the dollar against six major currencies, has fallen a bit to around 100.05 after hitting a five-month peak of 100.35. The latest ADP Employment report showed 42,000 new jobs in October, exceeding the expected 25,000. Additionally, the Services PMI improved to 52.4, above the estimate of 50.8.

Fed Rate Cut Probabilities

The outlook for the Federal Reserve’s December meeting now shows a reduced chance of a 25 basis point interest rate cut, estimated at 62.5%, down from 94.4%. For the Swiss Franc, SNB Chairman Martin Schlegel expects inflation to rise slightly, which means interest rates will likely stay steady. This is good news for the Swiss currency. The ADP Employment Change measures changes in private-sector jobs and influences consumer spending and economic growth. Traders pay close attention to ADP data as it can indicate trends before the Nonfarm Payrolls report from the Bureau of Labor Statistics. Higher employment numbers often suggest increased inflationary pressures and can impact interest rate decisions. We are seeing the USD/CHF pair pull back from its 11-week high near 0.8125. This seems to be a temporary pause rather than a reversal. The dip appears to be driven by profit-taking in the US Dollar after its recent gains. For traders, this might offer a better opportunity to position for a bullish move.US Economic Data and Market Strategy

Recent upbeat US economic data, especially the ADP job figures that exceeded estimates by nearly 70%, strengthen expectations for a solid Nonfarm Payrolls report this Friday. In early 2024, we observed a similar trend where strong labor reports pushed the dollar higher against other currencies. With the market now factoring in only a 62.5% chance of a Fed rate cut in December, down from over 90% just last week, the fundamental support for the USD looks strong. Given this positive outlook, we should consider buying call options on USD/CHF to benefit from the anticipated upward movement. December 2025 expiry contracts with a strike price around 0.8200 could yield profits if the pair breaks through recent highs following the NFP data. This strategy minimizes downside risk while offering substantial upside potential if the US Dollar rally continues as expected. While the Swiss National Bank’s comments about maintaining rates are relevant, they are unlikely to outweigh the influence of the Federal Reserve. The interest rate differential, with the US benchmark rate currently at 3.75-4.00% compared to Switzerland’s 1.75%, strongly favors the US Dollar. Any strength in the Swiss Franc is likely to be short-lived and may provide even better levels to enter long USD/CHF positions. Create your live VT Markets account and start trading now.EUR/GBP at 0.8810 targets May highs as Eurozone data is released and BoE makes a decision

The EUR/GBP currency pair is holding steady above 0.8800, currently around 0.8810, as we await new data from the Eurozone. In September, Germany’s Industrial Production is expected to rebound by 3% after a previous drop of 4.3%. Additionally, Eurozone Retail Sales are projected to rise by 0.2%, maintaining an annual growth rate of 1%.

The European Central Bank (ECB) is likely to proceed cautiously in its next policy meeting, keeping the deposit rate steady at 2.0%. Meanwhile, the Bank of England (BoE) is expected to hold its policy rate at 4% this November, while considering possible rate cuts due to easing inflation and wage data.

UK Fiscal Measures and Monetary Policies

Chancellor Rachel Reeves intends to propose fiscal measures in the upcoming budget to tackle borrowing, which may include tax increases. The BoE’s monetary policies, encompassing interest rate decisions and Quantitative Easing, significantly impact the value of the Pound Sterling. When inflation rises, the BoE uses Quantitative Tightening, which can strengthen the Pound. In the past, the market was closely monitoring the EUR/GBP pair as it remained above 0.8800, focusing on the differing policies of the central banks. Understanding how the ECB and BoE have changed since then is crucial. Back then, the ECB had kept its deposit rate at 2.0% for three consecutive meetings, but it has since taken a different approach. The ECB has raised rates to fight inflation and has started a cautious easing cycle, with the deposit facility rate now at 3.50%. Recent Eurostat data shows that inflation in the Euro Area has decreased to 2.4%, allowing the ECB to think about more cuts. On the other hand, the BoE has faced persistent domestic inflation, leading to a hike in the bank rate from the expected 4.0% to 5.0% in the latest meeting. According to the Office for National Statistics, UK inflation remains high at 3.1%, reinforcing the BoE’s tougher stance compared to the ECB.Fiscal Pressures and Economic Growth

The fiscal pressures associated with the November 26 budget are still a significant concern for the UK economy. The debt-to-GDP ratio is notably high at 98.5%, which restricts the government’s ability to maneuver financially. This limitation impacts the BoE’s policies and caps long-term growth prospects, which should be considered in our sterling strategies. With the BoE taking a more aggressive approach compared to the dovish ECB, the EUR/GBP pair appears likely to trend lower. To prepare for potential volatility around the upcoming central bank meetings in December, consider using options. Buying put options on EUR/GBP could be an effective strategy to capitalize on further declines resulting from the widening interest rate gap. Create your live VT Markets account and start trading now.HSBC Composite PMI for India rises to 60.4, up from 59.9

In October, India’s HSBC Composite Purchasing Managers’ Index (PMI) rose from 59.9 in September to 60.4. This growth signals increased activity in India’s private sector, showing that the economy is expanding.

Gold prices surpassed $4,000, driven by a weaker US Dollar and greater demand for safe assets. The USD/INR stabilized after initial losses, while the EUR/CAD maintained its position above the nine-day EMA at 1.6200 during a consolidation phase.

Central Banks and Market Sentiments

The Bank of England’s upcoming policy announcements are likely to impact the Pound Sterling. Crude oil prices remained strong as the European market opened, with WTI leading the upward trend. Markets face challenges from various factors, including a possible US government shutdown and comments from the Federal Reserve. The release of Eurozone Retail Sales data was expected to influence the direction of EUR/USD, which was slightly over 1.1500. Solana remained stable above $160, indicating strong interest from both institutional and retail investors. This points to potential further growth as part of the broader recovery in the crypto market. The latest HSBC Composite PMI for India shows the economy is thriving at 60.4, continuing the trend of growth since the post-pandemic recovery. For derivative traders, this strengthens the case for long positions on Nifty 50 futures, aiming for new highs. It may be wise to sell out-of-the-money puts to collect premium, as the robust domestic data supports this strategy.Market Volatility and Strategy

Despite this positive outlook, Foreign Institutional Investors reduced their holdings, pulling out $2.5 billion from Indian equities last month, despite the strong PMI. This suggests that global risk aversion, likely linked to the US situation, is currently outpacing local strengths. This divergence may lead to volatility in the USD/INR pair, making option straddles an attractive strategy to profit from potential sharp movements. The ongoing US government shutdown, now in its fifth week, continues to hurt the dollar, with the DXY index dropping below the 96.00 support level. This signals a favorable environment for short-dollar positions across the board. Call options on EUR/USD and GBP/USD look appealing, as both pairs show technical strength and benefit from the dollar’s political weakness. Gold crossing the $4,000 mark is a significant milestone, supported by a falling US Dollar and strong demand for safe-haven assets. While the inverse relationship with the dollar boosts gold, the demand for safety indicates underlying market fears. We recommend buying long-dated call options on gold futures or gold ETFs for exposure to potential gains while capping risk if the US political situation changes unexpectedly. Although the Euro is gaining against the dollar, the European economy shows weaknesses, as evident in Germany’s recent industrial production figures missing expectations. This lackluster data may keep the European Central Bank cautious, limiting the Euro’s strength. We see an opportunity in trading the EUR/GBP cross, looking to short the Euro against a Pound that could be strengthened by a hawkish Bank of England announcement. Create your live VT Markets account and start trading now.HSBC Services PMI for India recorded 58.9, exceeding the expected 58.8

India’s HSBC Services PMI for October performed better than expected, reaching 58.9, slightly above the forecast of 58.8. This growth in the services sector shows that economic activity remains strong.

Gold is trading above $4,000, gaining from a weaker US Dollar. The metal continues to recover as the market becomes more cautious, focusing on comments from Federal Reserve officials.

Currency Movements and Investor Actions

The USD/INR has bounced back as foreign institutional investors (FIIs) have reduced their investments in the Indian stock market. Meanwhile, the GBP/USD has stayed steady above 1.3050, thanks to a general decline in the US Dollar amid fears of a government shutdown. Solana has risen by 4% and is stabilizing above $160, supported by strong institutional demand. Retail interest is also returning, which could point to further gains for this cryptocurrency. In Europe, German industrial output for September increased by 1.3% compared to the previous month, which was below the expected 3%. This suggests that there may be challenges ahead for the industrial sector. India’s services sector remains strong, with the PMI data for October showing continued growth. However, there are challenges as FIIs withdrew over ₹20,000 crore from Indian equities last month. This creates mixed signals, suggesting that we should consider using options to prepare for volatility in the Nifty 50 index rather than making definitive bets.Market Fear and Strategies

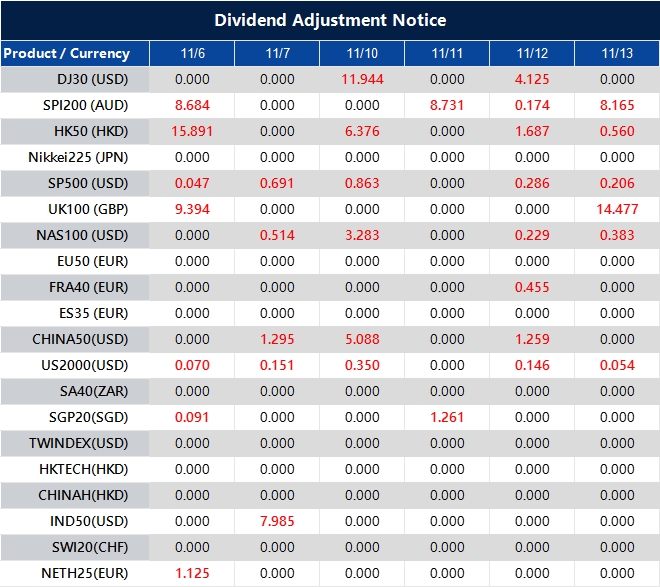

Currently, the market is driven by fear rather than fundamentals, highlighted by the ongoing US government shutdown and gold’s jump past $4,000 an ounce. The weak US dollar is a direct consequence of this situation, contributing to FII outflows from emerging markets like India. In this environment, it’s wise to adopt hedging strategies and be cautious about taking on too much risk. Gold’s sharp rise from around $2,450 in mid-2024 to over $4,000 is noteworthy. While central banks are still buying, such rapid increases often lead to a period of consolidation or a pullback. We now see an opportunity to sell out-of-the-money call options to earn premium, anticipating that the intense upward momentum may slow in the coming weeks. The tension between a strong local economy and weak global sentiment affects the USD/INR rate. The Reserve Bank of India has been actively managing the rupee, keeping it within a narrow range for months, but external pressures are increasing. We should anticipate that this stability could be challenged, making long volatility plays on the currency pair, such as buying straddles, a smart strategy. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Nov 06 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The GBP/JPY pair stays steady around 201.00, unable to break past Wednesday’s one-month low.

The GBP/JPY pair remains steady around the 201.00 level as traders look forward to the Bank of England (BoE) policy update. Concerns about the UK’s financial stability are weighing on the British Pound, while the Yen is gaining strength from expectations of a Bank of Japan (BoJ) rate hike and possible intervention.

The pair is trying to hold onto gains after bouncing back from a one-month low near 199.00. Current trading reflects the anticipation surrounding the BoE’s decision, which could significantly impact the British Pound and the GBP/JPY cross.

Economic Indicators and Predictions

Economic data shows lower inflation, financial challenges, and rising unemployment in the UK. The market expects a 33% chance of a 25bps rate cut by the BoE, and there’s a 70% probability of a rate cut by the end of the year. Concerns about the UK’s financial outlook are growing ahead of the Autumn budget, while the Yen shows signs of improvement. The latest BoJ meeting minutes indicate a possible rate hike soon, which supports the Yen. However, expectations that Japan’s new Prime Minister will increase fiscal spending to tackle inflation may limit the Yen’s gains. The BoE’s interest rate decision is crucial, with potential changes affecting the Pound Sterling significantly. The consensus for the next interest rate release remains at 4%. With the market hesitating around the 201.00 level for GBP/JPY, we expect volatility today, November 6, 2025. The immediate focus is on the Bank of England’s interest rate decision, expected to remain at 4%. Any hints at a future cut could easily push the pair below the important 199.00 support level, which was tested just yesterday.Current GBP/JPY Strategy

The outlook for a weaker Pound is growing, guiding our strategy. Recent data from the Office for National Statistics shows UK inflation slowed to 2.8% in October, marking the fourth month in a row of declines. With wage growth also easing to 4.5% and unemployment rising to 4.5%, the BoE has room to ease policies without worrying about inflation spiking. This follows the BoE’s first rate cut of the current cycle in August 2025, moving from 4.25% to the current 4%. We are also monitoring fiscal pressures ahead of the Autumn Budget on November 26, which could further impact the Pound. Thus, any rallies in GBP/JPY may present selling opportunities in the coming weeks. On the Yen’s side, it is seeing some support. The Bank of Japan exited its negative interest rate policy in March 2024, setting the policy rate at 0.25%. Markets expect another rate hike by early 2026. This situation contrasts sharply with the BoE’s easing approach, creating a fundamental divergence that favors a lower GBP/JPY. Given that the pair is trading near levels not seen consistently since before the 2008 financial crisis, it appears overextended. The combination of a dovish BoE and a cautiously hawkish BoJ suggests a downward correction is likely. A sustained drop below the 199.00 one-month low would indicate that this downward trend has started, and we should adjust our positions accordingly. Create your live VT Markets account and start trading now.EUR/JPY pair shows slight gains above 177.00 as the Yen weakens

The EUR/JPY exchange rate saw small gains, trading around 177.15 during early European hours on Thursday. The Yen lost ground against the Euro due to better risk sentiment and uncertainty about the Bank of Japan’s actions, which could impact the Yen.

The technical outlook for EUR/JPY looks strong, as it remains above the 100-day EMA and the RSI is at 55.60, above the midline. Immediate resistance is at 178.23, with potential movement toward 178.45. On the downside, initial support is at 175.70, and declines could reach 175.00.