Dow Jones futures rise ahead of expected US CPI following Trump-Xi discussions

Dow Jones futures rose 0.16% to about 47,000 during European trading hours. S&P 500 futures climbed 0.26%, while Nasdaq 100 futures jumped 0.41%, breaking above 25,350.

This increase followed the announcement that US President Trump will meet with Chinese leader Xi Jinping in South Korea on October 30th at the Asia-Pacific Economic Cooperation Summit.

Germany’s HCOB Composite PMI surpasses forecasts, reaching 53.8 instead of 51.6

The HCOB Composite PMI for Germany hit 53.8 in October, exceeding the expected 51.6. This indicates increased economic activity and steady growth in Germany.

This positive result suggests that businesses are seeing higher demand and improved conditions. The services sector has significantly driven this growth, while manufacturing remains strong.

Future Considerations

Upcoming data releases will be closely analyzed to better understand the economic outlook for Germany and the Eurozone. The PMI figure could impact the European Central Bank’s policies and shape market perceptions of the Euro. Germany’s composite PMI of 53.8 shows that Europe’s economic engine is gaining strength. This figure is more than just a prediction; it reflects strong business activity. For traders, this means they must rethink any assumptions about slow Eurozone growth right away. This data is especially noteworthy when we consider the challenges faced in 2024, when recession fears and weak manufacturing plagued the region. Back then, PMI readings struggled to stay above 50, which indicates growth. The current strength, particularly in manufacturing, suggests a significant change that the market may not fully appreciate yet.European Central Bank Response

The European Central Bank cannot overlook this report, especially since inflation in the Eurozone remains stubbornly high. With the latest core inflation rate for September 2025 at 2.7%, above the ECB’s target, this strong growth data makes future rate cuts unlikely. We may see the market shift from expectations of rate cuts to a more cautious hold or even hawkish stance. Given these conditions, bullish strategies on the Euro may be beneficial. Buying call options on the EUR/USD with expiration dates in December 2025 or January 2026 could capitalize on a potential change in ECB rate expectations. The Euro has been steady around the 1.10 level, and this data could trigger a breakout higher. This economic strength also benefits German stocks, making long positions on the DAX index appealing. The DAX has already risen over 8% this year, and confirmation of a strong domestic economy could push it even higher. We can use DAX futures for direct exposure or buy call options to limit risk. However, we need to be cautious about potential increases in market volatility. One strong data point can lead to sudden price changes, so it’s advisable to use options strategies that manage risk, like bull call spreads, to avoid unlimited exposure. Keeping an eye on the VSTOXX index, Europe’s equivalent of the VIX, will be important in the coming days to assess market concerns. Create your live VT Markets account and start trading now.Beijing strengthens its commitment to tech independence by focusing on AI, semiconductors, aerospace, and clean energy

China is ramping up its efforts to be self-sufficient in technology, focusing on areas like AI, semiconductors, aerospace, and clean energy. The country’s fourth plenum has unveiled a five-year plan to transform the economy into a modern industrial powerhouse. The National Development and Reform Commission emphasizes that technological progress is vital.

Valuation Concerns

Although tech stocks initially saw a boost, valuations are raising alarms. The Hang Seng Tech Index has risen 35% this year, mainly driven by sentiment rather than actual earnings. Bloomberg forecasts a 25% decline in earnings per share (EPS) for the Hang Seng Tech in 2025, followed by a 44% recovery in 2026. Future growth will hinge on whether domestic chipmakers can turn policy support into profits. Chinese tech companies are aligning their strategies with national goals through the “AI Plus” initiative, which seeks to integrate AI into various sectors to enhance productivity. This focus could lead tech platforms to prioritize national interests over short-term profits. Investors should look for profitable tech leaders linked to government policies but remain aware of risks such as disappointing earnings and geopolitical tensions. The market needs actual profits, not just promises of policy support, for sustained growth. We’ve witnessed a strong rally in Chinese tech this year, with the Hang Seng Tech Index up 35% due to optimism surrounding policies. However, these gains have driven valuations to high levels, particularly with a 25% earnings drop predicted for 2025. The coming weeks will determine if this optimism is warranted or if it’s simply a bubble driven by sentiment. Valuations for key chipmakers like SMIC are now close to 80 times forward earnings, making downside protection essential. We suggest buying put options on wide tech ETFs, such as the Hang Seng Tech Index ETF (3067.HK), as a smart strategy before the Q3 earnings season. This approach allows traders to protect long positions or bet on a market correction if companies fall short of high expectations.Economic and Geopolitical Risks

The broader economic conditions add to this caution. China’s Q3 GDP growth of 4.8% was just below expectations, showing that the domestic recovery is still weak. This overall economic challenge makes it tougher for tech companies that rely on growth to achieve the revenue increases that their stock prices suggest. Uncertainty is rising, presenting an opportunity for traders focusing on volatility. Implied volatility on Hang Seng Tech options has increased above 40%, highlighting market worries about earnings and policy execution. This scenario indicates that strategies like long straddles could be useful, as they benefit from significant price movements in either direction. The geopolitical situation introduces more risk, especially with recent talks in Washington hinting at possible new restrictions on semiconductor equipment exports. We saw how similar news led to sharp declines in the sector in 2022 and 2023. Maintaining unhedged long positions during this tense period could be excessively risky. Despite a generally cautious outlook, there may be targeted opportunities in companies with strong balance sheets and confirmed government contracts from last year’s “AI Plus” initiative. For these specific companies, selling out-of-the-money put spreads could generate income. This strategy takes advantage of high implied volatility while managing risk, but it requires selecting the few firms capable of turning policy into real profits. Create your live VT Markets account and start trading now.Traders remain cautious as NZD/USD holds around 0.5750 following previous session gains.

NZD/USD is hovering around 0.5750 as traders exercise caution while awaiting US Consumer Price Index (CPI) data. The ongoing US government shutdown, now 24 days long, is causing risk aversion and may impact the US Dollar’s performance.

In early European trading, NZD/USD showed slight movement after previously gaining. The delay in US economic data due to the government shutdown adds to uncertainty in the financial markets.

Potential Impact of US-China Trade Agreement

The New Zealand Dollar is holding steady due to hopes for a possible US-China trade agreement. Changes in China’s economy could affect the Kiwi Dollar because of their trade ties. US President Donald Trump expects to make agreements with Chinese President Xi Jinping at a meeting in South Korea on October 30th during the Asia-Pacific Economic Cooperation Summit. The New Zealand Dollar’s value is influenced by its economic health, central bank policies, and dairy prices. The Reserve Bank of New Zealand’s interest rate decisions are key in determining the currency’s worth. Additionally, overall market sentiment can strengthen the NZD during periods of economic positivity. Looking back at early 2019, when NZD/USD struggled around 0.5750, we see a useful comparison for today’s market. Now that the pair is trading higher at around 0.6100, the focus has shifted from data delays to persistent US inflation, which currently stands at 3.1% annually. This shift suggests that the Federal Reserve’s decisions are now central to market uncertainty.Market Sentiment and Future Strategies

We recall the 35-day US government shutdown at the end of 2018 and early 2019, which also postponed important economic reports and caused market chaos. Although we face another wave of budget negotiations in Washington, traders seem less anxious now, as they’ve seen similar situations resolved in the past. Consequently, traders should avoid over-committing to downside protection and should instead consider trading the short-term volatility around negotiation deadlines. Unlike the earlier optimism about a US-China trade deal that supported the Kiwi, the current situation is more complicated and less promising. Additionally, New Zealand’s domestic outlook shows some weaknesses, such as a 2.8% decline in prices from the latest Global Dairy Trade auction and a modest quarterly GDP growth at 0.4%. These signs suggest any strength in the New Zealand dollar might be temporary. Given this scenario, we anticipate that implied volatility will remain high ahead of upcoming central bank meetings and US inflation data. A possible strategy for the next few weeks is to buy straddles on NZD/USD, which allows for a profit from significant price movement in either direction without wagering on a specific outcome. Selling far out-of-the-money puts seems risky until we see a clear recovery in dairy prices or a significant improvement in global risk sentiment. Create your live VT Markets account and start trading now.Investor sentiment boosts the Australian Dollar, maintaining AUD/JPY above 99.50 amid positive trade talks.

The AUD/JPY is currently around 99.35 in early Friday trading in Europe. Positive news regarding US-China trade talks is helping the Australian Dollar gain strength against the Yen.

The reduction in trade tensions between the US and China is favorable for the Aussie. High-level discussions are set to take place in Malaysia, where US and Chinese officials will cover various topics, including trade and nuclear weapons limits.

Potential Impact Of Presidential Meeting

A possible meeting between the US and Chinese presidents at the Asia-Pacific Economic Cooperation summit could further affect the Aussie. China’s important trade relationship with Australia plays a significant role in this situation. Despite an increase in Japanese core inflation in September, the Japanese Yen is losing ground against the AUD. Analysts expect the Bank of Japan to keep interest rates steady in their upcoming meeting. Expectations for a rate hike have shifted to December, with most anticipating it will happen later. This outlook could limit the Yen’s ability to strengthen, although its appeal as a safe-haven currency may increase during uncertain times. Several factors influence the Japanese Yen, including the Bank of Japan’s policies and the difference in bond yields between Japan and the US. The Yen, known as a safe-haven currency, attracts investment during market turmoil due to its stability.Strategies For A Rising AUD/JPY

Optimism about the US-China trade talks is supporting the Australian Dollar, keeping the AUD/JPY above 99.50. We expect this trend to continue with negotiations starting today in Malaysia, ahead of the presidential meeting next Thursday. This positive environment favors the Aussie, given its link to the Chinese economy. Recent information from the Australian Bureau of Statistics shows that exports to China increased by 3.2% in the third quarter of 2025, mainly due to strong iron ore demand. This connection underscores the Aussie’s sensitivity to positive news from the trade negotiations. A successful outcome could lead to a significant rise in the currency pair. Conversely, the Japanese Yen is likely to stay weak. Japan’s Core CPI for September, released last week, was 1.9%, still under the Bank of Japan’s 2% target. Therefore, it is likely that the BoJ will keep interest rates unchanged in their meeting next week, limiting the Yen’s potential for strength. Given this situation, we suggest strategies that benefit from a rising AUD/JPY. Buying near-term call options with a strike price of about 99.75, due after next week’s summit, could capture potential gains from a trade deal. This method allows us to take advantage of a positive outcome while minimizing our initial risk. However, there is a real risk that the talks could fall through, which would likely lead to a flight to safety and strengthen the Yen. Therefore, we should consider a small investment in out-of-the-money put options as a hedge against a sudden downturn. This protective measure safeguards our portfolio if the summit disappoints investors. Create your live VT Markets account and start trading now.Consumer confidence in France rises to 90, exceeding expectations of 87

The latest data on the US Consumer Price Index (CPI) shows inflation is expected to rise by 3.1% year-over-year in September. This increase puts more pressure on the economy and could influence the Federal Reserve’s interest rate choices soon. Economists are closely monitoring these figures, especially in light of US-China trade discussions and their effect on prices.

In the foreign exchange market, the EUR/USD currency pair remains stable above 1.1600, supported by solid Eurozone PMI data. Similarly, GBP/USD stays above 1.3300 due to positive UK retail sales and PMI reports. Analysts are keen to see how the US CPI data impacts these currency pairs.

Gold Prices and Market Reactions

Gold prices have been fluctuating, with a recent pullback ahead of the US CPI announcement and ongoing trade negotiations. Currently, gold is around $4,100 after a recent spike. Traders are particularly interested in how gold interacts with the US Dollar and geopolitical events. Upcoming events, like Federal Reserve meetings and key economic data releases, could greatly influence market sentiment and trading strategies. Participants are trying to gauge the future direction of monetary policy and the economy. With the September US Consumer Price Index at 3.1%, inflation remains a pressing issue. This number is notably above the Federal Reserve’s target, especially when considering the inflation peaks we faced in 2022. The recent jobs report from early October 2025 highlighted 260,000 new jobs, supporting the idea that the Fed will continue its strict monetary policy.Market Strategies in Response to Fed Policy

In light of this information, derivative traders should expect a hawkish tone in future Fed communications. They might consider preparing for longer-lasting higher interest rates by using options on Treasury futures, particularly puts on SOFR futures contracts for early 2026. The market now places the likelihood of at least one more rate hike before the end of 2025 at over 70%, a big increase from just a month ago. In the foreign exchange market, while the EUR/USD holds above 1.1600, its stability may be at risk as the dollar strengthens. The European Central Bank has indicated it will pause, which creates a policy gap favoring the US dollar. Traders could see this as a chance to buy at-the-money puts on the EUR/USD pair for protection against a drop. The British pound has also been buoyed by solid UK PMI data, keeping it above 1.3300, but it too faces challenges. The Bank of England seems more focused on sluggish growth than the Fed, which limits GBP/USD’s potential for gains. In this situation, strategies that benefit from a stronger dollar, such as call options on the U.S. Dollar Index (DXY), look increasingly appealing. Gold’s volatility, currently near $4,100, mirrors market uncertainty regarding geopolitical tensions and rising real yields. A hawkish Fed usually boosts the dollar and pressures gold prices, but any escalation in trade conflicts might prompt investors to seek safety. For the upcoming weeks, a long volatility strategy using option straddles on gold futures could capitalize on significant price movements in either direction. Create your live VT Markets account and start trading now.Sweden’s Producer Price Index increases to 0.5% year-on-year after a previous decline of -0.7%

US Consumer Price Index (CPI) data is expected to show a rise in headline inflation to 3.1% year-on-year for September. The report will come out on Friday at 12:30 GMT, and there’s a lot of focus on how tariffs from the Biden administration might be affecting prices. Market reactions are likely to be significant, as this data could shape the Federal Reserve’s interest rate decisions for the rest of the year.

**Financial Markets React**

Financial markets are cautious ahead of the CPI report. Key currency pairs and other assets have reacted to recent economic indicators, like UK retail sales and PMI data, which have boosted the British Pound. Strong PMI figures from the Eurozone have helped the Euro gain against the US Dollar, aiding the EUR/USD recovery.

Gold is facing pressure from rising US Treasury yields and geopolitical tensions impacting oil prices. During this instability, traders are looking to the CPI data for guidance.

In Sweden, the Producer Price Index unexpectedly rose to 0.5% year-on-year in September, a jump from -0.7%. This information may sway market sentiment as investors consider inflation pressures locally and globally. Analysts believe upcoming CPI data could spark market volatility, affecting the US Dollar and related currency pairs.

**Anticipating Market Moves**

With the September Consumer Price Index report just a few hours away, we’re preparing for a significant market shift. The consensus forecast is a 3.1% year-on-year increase, which keeps inflation above the Federal Reserve’s target and recalls the inflation battles of 2023 and 2024. Implied volatility on S&P 500 options expiring next week has increased, indicating traders are willing to pay more to protect against a sharp price swing.

If the headline number exceeds 3.1%, we can expect the market to factor in a higher chance of a Fed rate hike before the year ends. Currently, Fed funds futures suggest a 25% likelihood of a hike in December, but a higher CPI reading could push that over 50%, strengthening the US Dollar. In this case, buying put options on major stock indices or bond futures could be an effective strategy to profit from the anticipated risk-off reaction.

On the other hand, if the CPI comes in below 3.0%, it would indicate that inflationary pressures are easing. This would likely lead to a rally in equities and a sell-off in the US Dollar, giving the Fed a clear reason to maintain their current stance. For this scenario, we’re considering call options on technology-heavy indices or selling put spreads to take advantage of renewed investor optimism.

The currency market is particularly tense, with the Euro and Pound showing strength from recent positive economic data. A strong US inflation report could reverse the recent rebound of the EUR/USD from its lows earlier this quarter. We can use currency options to position for this, as a stronger Dollar would create immediate pressure on the pair.

Gold remains vulnerable due to high US Treasury yields, with the 10-year note around 4.3%, making it costly to hold the non-yielding metal. A high CPI reading would cause yields to rise even further, likely lowering gold prices and making put options on gold futures an attractive play. We are also monitoring the VIX, currently at about 17, since any surprises in the data will likely trigger a spike in market-wide volatility.

Create your live VT Markets account and start trading now.

In September, Sweden’s Producer Price Index fell from 0.5% to -0.7% compared to previous levels.

US CPI

Headline inflation in the US is expected to rise by 3.1% year-over-year in September. On the other hand, Sweden’s Producer Price Index (PPI) fell from 0.5% to -0.7% during the same period.

Economic Data Releases

Economic data releases have a big impact on how markets react. The US Bureau of Labor Statistics will soon share the Consumer Price Index (CPI) for September. Investors are particularly interested in inflation trends due to ongoing geopolitical tensions and trade discussions. The pound sterling is gaining strength, thanks to strong UK retail sales and positive flash PMI data. The EUR/USD has bounced back from recent lows due to encouraging Eurozone PMI figures. At the same time, gold prices have dropped as the market anticipates important economic reports. September’s CPI data is expected to show a rise in inflation, which could influence the US dollar and the Federal Reserve’s strategy on interest rates. Several factors, including trade relations and monetary policies in the US and globally, are affecting the economic landscape. Last week, September’s US CPI data was confirmed at a 3.1% year-over-year increase, maintaining inflation concerns. This suggests that the Federal Reserve will stick to its restrictive policies and likely delay any rate cuts until 2026. Traders may want to adopt strategies that benefit from a strong US dollar and ongoing pressure on interest rate-sensitive assets.US Inflation and Market Strategy

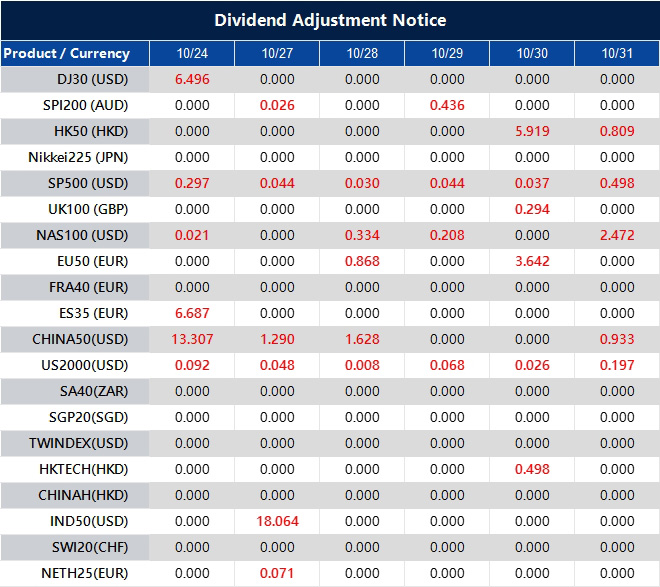

We see uncertainty reflected in the options market, where the CBOE Volatility Index (VIX) rose to 17.5 this past week, up from its lows earlier this month. The CME FedWatch Tool now shows that there is more than an 80% chance the Fed will keep rates unchanged at its December meeting. In this environment, using protective put options on equity indices is a wise strategy for hedging against potential losses in the coming weeks. In Europe, the situation is more mixed. Sweden’s PPI drop of -0.7% indicates emerging disinflationary pressures that the US has not yet experienced. This highlights the differences in policy we observed in 2023, where central banks acted at different paces. There may be opportunities to trade currency pairs like EUR/USD using options, as it has shown strength following positive PMI figures. Gold’s recent decline to the $2,240 level is due to the market adjusting to higher real yields, with the 10-year Treasury yield now staying above 4.5%. This makes gold, which doesn’t yield any interest, less attractive for the short term. Traders might consider using futures to express a bearish view or selling call options against existing holdings to generate income, especially if gold’s upside is constrained by a hawkish Fed. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Oct 24 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

UK retail sales exceed forecasts with a 1.5% year-on-year increase.

Retail sales in the United Kingdom for September increased by 1.5% compared to last year, exceeding expectations of just 0.6%. This growth occurred amid various global economic activities and market events.

In Europe, the Eurozone’s HCOB Composite Purchasing Managers’ Index rose to 52.2 in October. In the United States, the Consumer Price Index (CPI) for September is expected to show the highest inflation in sixteen months.