The UK’s non-EU trade balance was £-3.46bn in January. This compares with £-10.994bn in the previous period.

The data shows the UK’s non-EU trade gap narrowed in January. The figures relate to trade in goods and services with countries outside the EU.

Implications For Sterling Strength

Given the sharp narrowing of the UK’s non-EU trade deficit in January, we should anticipate renewed strength in the Pound Sterling. This improvement, from a nearly £11 billion deficit in December 2025 to under £3.5 billion, is a significant positive signal for the currency. In the coming weeks, this suggests a bullish outlook for GBP against major pairs like the Dollar and the Euro.

We should therefore consider positioning through derivatives for a rise in Sterling’s value. Buying call options on GBP/USD with expiry dates in April or May 2026 would allow us to profit from an upward move while capping our potential losses. This strategy is supported by the fact that the pound has been sensitive to positive economic surprises over the last year.

This trade data is especially important when we consider the current economic environment. With UK inflation data from February 2026 showing consumer prices are still stubbornly high at 3.4%, this strong trade figure gives the Bank of England more reason to delay interest rate cuts. A higher-for-longer rate environment is typically supportive of a currency.

This may also be a good time to look at FTSE 100 index futures. Many of the index’s largest companies are multinational exporters, and a more favourable trade balance hints at stronger international earnings. We saw a similar pattern in the second half of 2025, where better-than-expected export data provided a temporary lift to UK equities.

Key Risk Drivers To Monitor

However, we must watch the upcoming retail sales figures for February to understand the full picture. If the trade deficit narrowed because of a collapse in imports, it could signal weak domestic consumer demand, which would undermine this positive view. But if it was driven by a surge in exports, our bullish stance on the pound and UK stocks will be confirmed.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

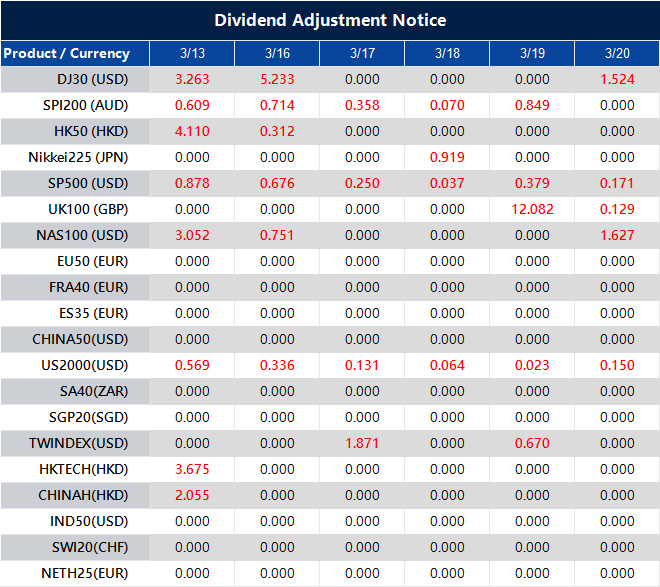

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The UK goods trade balance was £-14.45bn in January. This was above the expected figure of £-22.2bn.

The better-than-expected January trade balance figure of -£14.45 billion points to a more resilient UK economy than we initially priced in. This smaller deficit suggests exports are holding up or imports are moderating, both fundamentally positive for Sterling. We should therefore anticipate a firmer floor for the British Pound in the near term.

Trade Balance Implications For Sterling

This positive data point, when viewed alongside the recent February inflation report which showed core CPI remaining sticky at 2.4%, strengthens the case for the Bank of England to maintain its current hawkish stance. We should adjust interest rate derivative positions to reflect a lower probability of a rate cut before the third quarter. This is a marked change from the sentiment at the end of 2025 when the market was pricing in earlier cuts.

For those trading foreign exchange derivatives, this suggests a more bullish outlook on the Pound against the Euro (GBP/EUR). Recent manufacturing PMI data from the Eurozone has been soft, with Germany’s February figure coming in at 42.5, indicating continued contraction. This divergence supports strategies like buying GBP/EUR call options or selling out-of-the-money puts to position for further Sterling strength.

Looking at equity derivatives, the improved economic picture could benefit domestically-focused stocks. We may see increased demand for call options on the FTSE 250 index, which is a better barometer of the UK’s internal health than the more international FTSE 100. Back in 2024, we saw similar domestic resilience briefly boost the mid-cap index before global headwinds took over.

However, we must remember this is January data, and the key will be whether this strength continued into February and March. Looking back at the volatility in shipping costs we saw in 2025, any renewed supply chain pressure could quickly reverse this positive trend. It is wise to use options spreads to define risk rather than taking on unlimited exposure.

UK manufacturing production rose by 0.1% month on month in January. This was below the 0.2% forecast.

The release measures monthly changes in output from the UK manufacturing sector. The January figure follows the latest available reading from the prior month’s series.

January Data Signals Early Slowdown

That January manufacturing production miss, coming in at 0.1%, set a cautious tone for the first quarter of 2026. While it is older data, it was the first sign of a slowdown that subsequent figures have confirmed. More recent preliminary PMI data for February also dipped to 47.1, reinforcing this view of a struggling industrial sector.

This sustained weakness puts pressure on the Bank of England to consider a more dovish stance in its upcoming meetings. We are now pricing in a higher probability of a rate cut by the third quarter, a shift from the ‘higher for longer’ narrative we saw at the end of 2025. This situation is reminiscent of the policy pivot we observed in late 2024 when growth concerns began to outweigh inflation fears.

Consequently, we are looking at bearish strategies on the British pound, particularly against the US dollar. Implied volatility on GBP/USD options has ticked up as traders anticipate more downside potential. Recent data shows the pound has already weakened by 1.5% against the dollar since the start of February.

For the FTSE 100, the outlook is mixed, creating opportunities for relative value trades. The weaker pound is a tailwind for the index’s large international earners, which account for over 75% of its total revenue. However, domestically focused companies in the FTSE 250 are likely to underperform due to the sluggish UK consumer demand.

USD/CAD held near 1.3640 in Asian trading on Friday, after rising by more than 0.25% in the prior session. The Canadian Dollar was steady as oil prices eased.

WTI slipped slightly after jumping more than 9% in the previous session, trading near $95.00 a barrel. US crude prices are up more than 40% since the war began.

Strait Of Hormuz Risk Escalates

Oil prices may keep rising after the Strait of Hormuz was effectively closed during an escalating conflict involving the US, Israel and Iran. The International Energy Agency said the US-Israeli war on Iran is “creating the largest supply disruption in the history of the global oil market.”

Iran’s new supreme leader, Mojtaba Khamenei, said the Strait of Hormuz closure should continue as a “tool to pressure the enemy.” He also warned that US military bases in the region should close immediately or face possible attacks.

USD/CAD declines may be limited if the US Dollar stays supported by expectations the Federal Reserve will leave rates unchanged next week. The benchmark federal funds rate is currently 3.50%–3.75%.

Markets are also awaiting January’s Personal Consumption Expenditures Price Index later on Friday. Attention is also on the first revision of fourth-quarter US GDP growth and March consumer confidence.

Usd Cad Tug Of War

The market is seeing a major tug-of-war on the USD/CAD pair around the 1.3640 level. We have West Texas Intermediate crude holding near $95 a barrel, which should be driving the Canadian dollar much stronger. However, the flight to safety amid the Mideast conflict is keeping the US dollar in high demand.

The closure of the Strait of Hormuz is the dominant factor, choking off roughly a fifth of the world’s daily oil supply, a disruption unseen in decades. Historically, events like the 1973 oil crisis caused prices to quadruple, and Iran’s new leadership suggests this supply disruption is a long-term policy. This ongoing shock means we must prepare for oil prices to remain elevated or even climb higher.

On the other side, the Federal Reserve’s firm stance on holding interest rates at 3.50-3.75% provides a strong floor for the greenback. The ongoing war is creating immense risk-off sentiment, pushing capital into US assets for safety. This counteracts the positive pressure on the loonie from oil prices.

Given this uncertainty, we believe trading direction outright is extremely risky, and the focus must shift to volatility. Implied volatility on USD/CAD options has surged, with currency volatility indexes showing a more than 30% jump since the conflict escalated last month. Strategies that benefit from large price swings, such as long straddles, are becoming more attractive for hedging against sharp, unpredictable moves.

We are witnessing a breakdown in the typical inverse correlation between oil prices and the USD/CAD pair. Looking back at data from 2025, that relationship was consistently strong, but the current safe-haven demand for the US dollar is overriding it. This means historical models based purely on oil prices are likely to be unreliable in the coming weeks.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

NZD/USD edged up to about 0.5855 in early Asian trade on Friday, with gains limited by ongoing conflict in the Middle East. Markets are waiting for the US Personal Consumption Expenditures (PCE) Price Index for January later on Friday.

Donald Trump said stopping Iran from getting nuclear weapons and threatening the Middle East is more important than oil costs. Iran’s new supreme leader, Mojtaba Khamenei, said Tehran would seek to keep the Strait of Hormuz effectively closed, which could support demand for the US Dollar.

Us Pce Report In Focus

The January PCE report is the Federal Reserve’s preferred inflation measure and may affect rate expectations. Headline PCE is forecast at 2.9% year on year, with core PCE at 3.1%.

A softer inflation reading could weigh on the US Dollar and support NZD/USD. CME FedWatch data shows markets pricing a 99% chance the Fed will keep rates unchanged at its next meeting.

RBNZ Governor Anna Breman said policy is likely to stay accommodative for some time due to a fragile economy. Markets are pricing at least two Official Cash Rate hikes by end-2026, linked to an energy-price shock from Middle East conflict.

The New Zealand Dollar often moves with RBNZ policy, rate differences versus the US, Chinese economic conditions, and dairy prices. It also tends to rise in risk-on markets and fall during periods of market stress.

Central Bank Policy And Risk

The push and pull between central bank policies and global risk are keeping NZD/USD under pressure. We are seeing the US Dollar maintain its strength, driven by a robust US labor market that added 250,000 jobs in February and core PCE inflation that is stubbornly holding around 2.9%. This persistent data reduces the likelihood of near-term Federal Reserve rate cuts, making the dollar more attractive.

Last year, we saw markets begin to price in rate hikes from the Reserve Bank of New Zealand due to the energy price shock from Middle East conflicts. This has been validated by recent data, as New Zealand’s Q4 2025 CPI came in at 3.8%, well above the RBNZ’s target band. Supporting the Kiwi, however, the latest Global Dairy Trade auction saw prices jump 3.5%, providing a much-needed boost to export sentiment.

Given these conflicting signals, implied volatility on NZD/USD options has been rising, making strategies that benefit from price movement or defined ranges more appealing. Traders anticipating a break higher on RBNZ hawkishness could consider buying call spreads to cheaply position for a move towards the 0.6000 level. Alternatively, those expecting continued range-bound action could look at selling strangles to collect premium as long as the pair remains contained.

The Kiwi’s sensitivity to Chinese economic performance remains a key vulnerability. The most recent Caixin Manufacturing PMI from China printed at a disappointing 49.8, signaling a slight contraction and weighing on the New Zealand Dollar. This reliance on Chinese demand means traders should use any rallies in the pair to consider protective put options as a hedge against further negative data from New Zealand’s largest trading partner.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Silver (XAG/USD) rose in the Asian session on Friday and moved back above $85.00. It has ended a two-day fall and is set to finish the week little changed.

On the 4-hour chart, price remains below the descending 200-period Simple Moving Average (SMA). The Relative Strength Index (RSI) has lifted towards 48, while the MACD stays below its signal line and below zero, with a negative histogram.

Technical Picture And Key Levels

A clearer move below the rising support trend line is still needed before stronger selling positions are considered. If that break occurs, silver may fall towards $82.00 and then $80.00.

Resistance is near the 200-period SMA at about $85.70. A sustained move above $85.70 could lead towards $87.00 and then $88.50, while moves below $85.70 may face selling.

Looking back at the analysis from around this time in 2025, we recall the struggle silver had below the $85.70 moving average. Today, on March 13, 2026, with the metal trading closer to $78, those former price levels now represent significant overhead resistance. The market sentiment has shifted from cautious optimism to a more defined bearish pressure.

Recent statistics support this cautious stance, as the Global Solar Council’s Q1 2026 report indicated a slight contraction in industrial silver demand for the first time in three years. Furthermore, data shows major silver ETFs have seen net outflows of over 15 million ounces since the start of the year, suggesting investment demand is waning. This weak fundamental backdrop reinforces the technical selling pressure we are seeing.

For derivative traders, this suggests that the $80.00 and $82.00 levels, which were viewed as potential support last year, are now ceilings. Selling call options with strike prices at or above $82.00 could be a viable strategy to generate income over the coming weeks. This approach would profit from price stagnation or a further decline in the price of silver.

Options Positioning And Risk Scenarios

However, we are now testing a long-term rising support trendline that has held firm for several years. A break below the current $78 level could accelerate selling, similar to the sharp drop we experienced in late 2023 after a key technical failure. Therefore, buying put options with a $75 strike could serve as a cheap hedge against a significant downturn.

On the other hand, we must watch for any surprising strength, especially with the latest US inflation report due next week. A sustained break back above the old $85.70 resistance level from the 2025 analysis would invalidate the current bearish view. In that scenario, traders would quickly need to cover short positions and consider buying calls to ride a new wave of momentum toward last year’s highs.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

GBP/USD recovered some of the prior session’s falls and traded near 1.3370 in Asian hours on Friday. The move came as the US Dollar Index eased after rising by almost 0.5% on Thursday.

Traders are waiting for the US Personal Consumption Expenditures (PCE) Price Index for January, due later on Friday. Markets are also watching the first revision to fourth-quarter US GDP growth and March consumer confidence.

Middle East Tensions Support Dollar Demand

Middle East tensions have supported demand for the US dollar, alongside higher oil prices. Iran’s new supreme leader, Mojtaba Khamenei, said the closure of the Strait of Hormuz should remain a “tool to pressure the enemy”, and warned that all US military bases in the region should be closed or face potential attacks.

Futures markets and economists expect the Federal Reserve to keep rates unchanged at next week’s meeting, with the federal funds rate at 3.50%–3.75%. Markets are also pricing in a Bank of England rate cut next week, though higher oil prices have added uncertainty and may lead to delays.

We are seeing a familiar pattern emerge that reminds us of early 2025. The US Dollar is gaining strength from geopolitical risks, much like it did during the tensions over the Strait of Hormuz last year. This safe-haven demand is being reinforced by renewed instability in the Middle East, which has pushed Brent crude oil prices back above $95 a barrel.

The case for a stronger dollar is supported by recent inflation data. February’s Personal Consumption Expenditures (PCE) index in the US came in at a stubborn 2.9%, making it unlikely the Federal Reserve will signal any rate cuts soon. This echoes the period in 2025 when the Fed held its benchmark rate firm at 3.50%–3.75%, supporting the greenback.

BoE Pressure Builds Policy Divergence

Conversely, the Bank of England is facing a different economic picture. With UK inflation having fallen to 2.2% and recent GDP figures showing near-stagnant growth, the BoE is under pressure to cut rates at its upcoming meeting. This policy divergence is creating a clear path for potential GBP/USD weakness, a scenario we watched develop closely last year.

Given this divergence, we believe traders should consider buying put options on GBP/USD to position for a potential decline towards the 1.3200 level. Last year, we saw how quickly the pair could move when central bank expectations shifted against the pound. The current setup, with a hawkish Fed and a dovish BoE, presents a similar opportunity.

The upcoming central bank meetings introduce significant event risk, suggesting higher volatility ahead. We remember how implied volatility on currency pairs jumped during the geopolitical flare-ups of 2025. Therefore, using options strategies like straddles, which profit from a large price move in either direction, could be a prudent way to trade the uncertainty.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Australia will release up to 762 million litres of fuel from its reserves after easing stockholding rules. The move is intended to manage fuel supply disruptions linked to the Iran conflict.

The government also plans to cut minimum fuel stockholding obligations by up to 20%. The change is designed to increase flexibility during the disruption.

Market Reaction And Current Pricing

West Texas Intermediate (WTI) was down 1.05% on the day at $93.85 at the time of writing.

We saw how Australia’s decision back in late 2025 to release fuel reserves initially pushed West Texas Intermediate prices down. This was a classic short-term reaction to a supply-side announcement, as the market priced in the immediate availability of more fuel. That dip to around $93 proved to be temporary as the underlying supply chain risks from the Iran conflict remained.

Looking at the market today, March 13, 2026, WTI is trading closer to $88 per barrel after a volatile start to the year. Recent data from the U.S. Energy Information Administration now points to a potential global supply surplus of nearly 500,000 barrels per day for the second quarter. This forecast is creating downward pressure and suggests the initial supply panic from last year has been absorbed.

The key for us in the coming weeks is the elevated implied volatility in the options market. The CBOE Crude Oil Volatility Index (OVX) is hovering around 37, which is significantly higher than the levels below 30 we saw before the conflict escalated in 2025. This environment suggests selling options premium through strategies like iron condors or strangles could be profitable, assuming no major escalation.

We should also remember the lessons from the massive strategic reserve releases that occurred back in 2022. Historically, these government actions provide a temporary ceiling on prices but do not fix the fundamental geopolitical problems driving the risk. Therefore, any sharp price drops in the coming weeks on further supply news could be viewed as buying opportunities for longer-dated futures contracts.

Geopolitical Risks And Shipping Constraints

Our primary focus must now shift back to the geopolitical situation and tanker traffic through the Strait of Hormuz. Shipping data from early March 2026 shows insurance premiums for vessels in the region are still 15% higher than they were a year ago. Any actual disruption to passage there would immediately override inventory data and send prices sharply higher.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

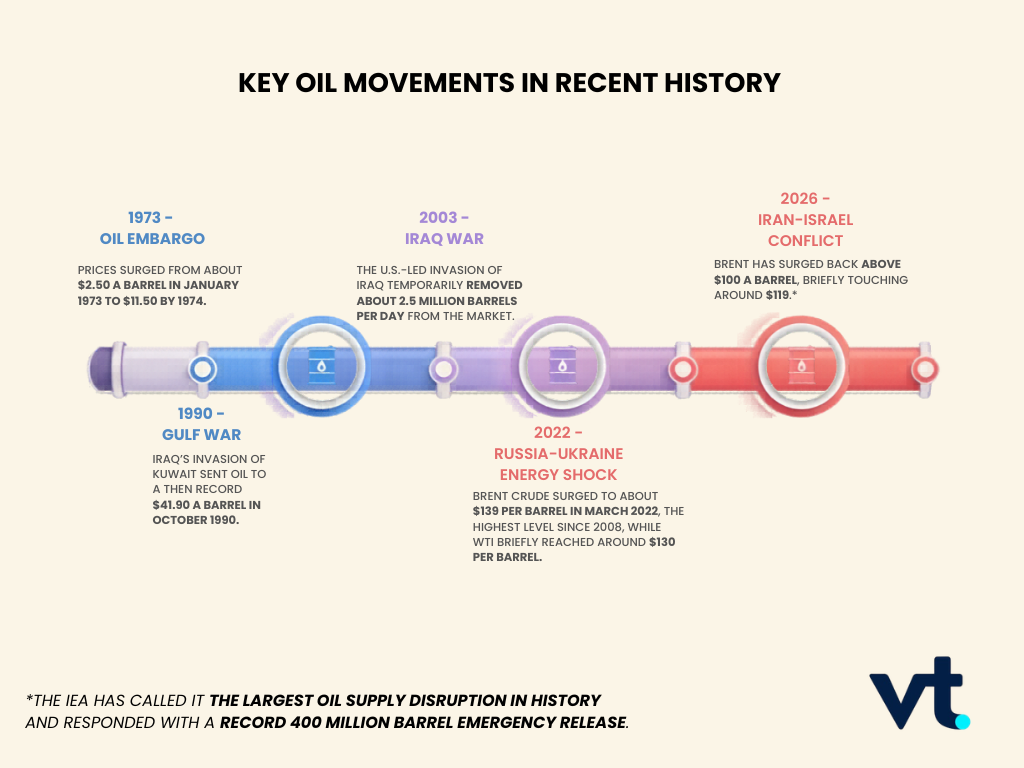

Conflicts involving major oil-producing regions often trigger spikes in global oil and gas prices.

Historical events such as the 1973 oil embargo and the Gulf War show how quickly geopolitical shocks can move energy markets.

The Iran–Israel conflict has raised similar concerns because the Middle East remains central to global oil supply.

Fuel prices are closely tied to global geopolitics. When conflicts occur in energy-producing regions, oil markets often react quickly, pushing crude prices higher and eventually raising gas prices for consumers.

This dynamic has played out repeatedly throughout modern history. From the 1973 oil crisis to more recent geopolitical conflicts, wars that threaten oil production or transport routes have often triggered energy price shocks.

Today, concerns about the Iran–Israel conflict and gas prices reflect a familiar pattern. Markets are once again watching developments in the Middle East closely because the region remains a major source of global oil supply.

An energy price shock caused by the Iran war has led to jitters in global bond markets and a rethink on the outlook for interest rates

Understanding how wars affect energy markets can help explain why fuel prices often rise during periods of geopolitical tension.

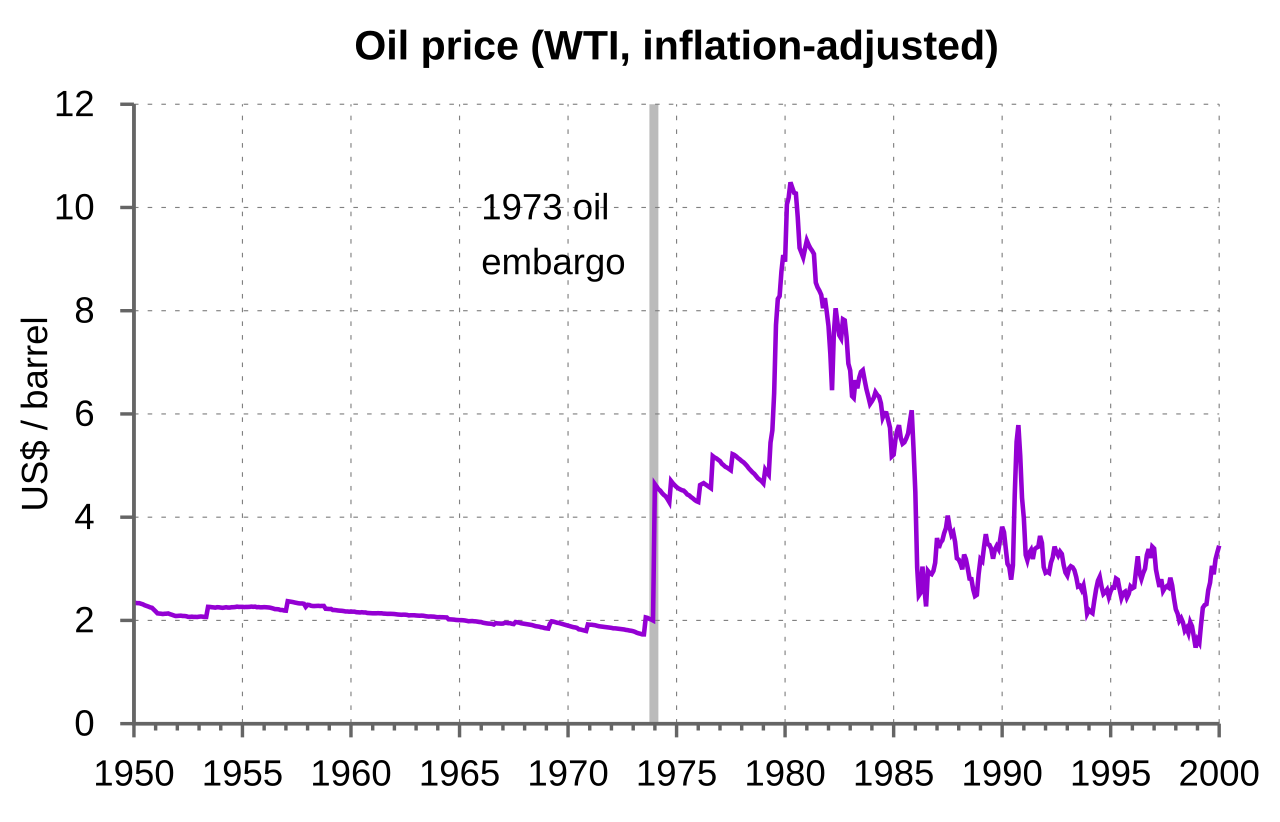

The 1973 Oil Crisis: The First Global Energy Shock

One of the most significant examples of war driving fuel prices higher occurred during the 1973 oil crisis.

Source: Wikipedia

Following the Yom Kippur War between Israel and several Arab states, members of the Organization of Petroleum Exporting Countries (OPEC) introduced an oil embargo against nations that supported Israel.

The consequences were immediate.

The 1973 oil embargo triggered inflation, political turmoil and global upheaval. As the Iran war now threatens energy markets again, history shows how quickly an oil crisis can ripple into everyday life. https://t.co/p1x7ZsDDJg

Oil prices quadrupled within months, fuel shortages spread across Western economies, and long lines formed at petrol stations. The surge in energy costs contributed to inflation, economic slowdown, and lasting changes in global energy policy.

The crisis demonstrated how geopolitical tensions in the Middle East could rapidly destabilise energy markets and push gas prices higher worldwide.

The Gulf War and Oil Market Volatility

Another major example occurred during the 1990 Gulf War, when Iraq invaded Kuwait.

At the time, both countries were major oil producers. The invasion raised fears that oil production across the region could be disrupted.

As uncertainty spread through energy markets, oil prices surged sharply within weeks. Traders anticipated potential supply shortages and began pricing in geopolitical risk.

Although production eventually stabilised after international intervention, the episode reinforced an important lesson for energy markets. Even the threat of conflict in major oil-producing regions can drive significant price volatility.

The Russia–Ukraine War and the Modern Energy Shock

More recently, the Russia–Ukraine war triggered another major energy price surge.

Russia is one of the world’s largest producers of oil and natural gas. When the conflict began in 2022, global energy markets reacted quickly to fears of supply disruptions and sanctions targeting Russian exports.

The highest weekly crude shipments since its 2022 invasion of Ukraine aren't helping Russia. Ballooning volumes of undelivered oil on tankers are boosting a supply glut that's undermining prices and hitting the Kremlin's war chest, writes @JLeeEnergyhttps://t.co/lchsBU6X6M

Oil prices climbed sharply and natural gas prices surged across Europe. Fuel costs rose worldwide, contributing to inflation and forcing governments and central banks to respond to rising energy bills.

The crisis demonstrated once again how closely global fuel prices are linked to geopolitical stability.

Why the Iran–Israel Conflict Matters for Oil Markets

The current Iran–Israel conflict has renewed concerns about gas prices because of the Middle East’s critical role in global energy supply.

Several factors make the region particularly important for oil markets.

Strategic shipping routes

One of the most important is the Strait of Hormuz, a narrow passage between Iran and Oman. Roughly one-fifth of the world’s oil shipments pass through this route each day.

Any disruption to shipping traffic in the Strait of Hormuz could affect global oil supply and push crude prices higher.

Regional oil production

The Middle East remains one of the largest oil-producing regions in the world. Countries across the Gulf export millions of barrels of oil each day to global markets.

Escalating conflict in the region raises the risk that production or transport infrastructure could be disrupted.

Market psychology

Energy traders often react to geopolitical risks before supply disruptions actually occur. Even the possibility of escalation can cause oil prices to move higher as markets attempt to price in uncertainty.

This is why news about the Iran–Israel war and gas prices often appear together in financial headlines.

Why Oil Prices Affect Gas Prices

Crude oil typically represents the largest component of the price consumers pay at the pump.

When oil prices rise because of geopolitical tensions, refiners pay more for raw crude. Those costs move through the supply chain, eventually raising petrol and diesel prices for drivers.

As a result, global conflicts that push oil prices higher often lead to higher gas prices as well.

Oil movements have more than just an influence on gas prices. Read more about how oil prices play a role in the AI revolution here.

What History Suggests About Future Gas Prices

History shows that geopolitical conflicts often trigger temporary spikes in oil prices and fuel costs.

However, the long-term impact can vary depending on several factors:

Whether oil supply is actually disrupted

How long the conflict lasts

How quickly producers adjust output to stabilise markets

In many cases, prices stabilise once markets gain confidence that supply will remain stable. In other situations, prolonged tensions can keep energy markets volatile for extended periods.

Because the global economy depends heavily on oil, geopolitical developments will likely continue to influence fuel prices for years to come.

The Bottom Line

From the 1973 oil embargo to the Russia–Ukraine war, history shows that geopolitical conflicts often lead to spikes in oil and gas prices.

The Iran–Israel conflict has raised similar concerns because of the Middle East’s central role in global energy supply and the importance of shipping routes such as the Strait of Hormuz.

While the long-term impact on gas prices will depend on how events unfold, one lesson from history remains clear. When conflict threatens global energy supply, oil markets react quickly, and fuel prices often follow.

Why does the Iran–Israel war affect gas prices? The Iran–Israel war affects gas prices because conflicts in the Middle East can disrupt global oil supply and shipping routes. When traders fear supply shortages, crude oil prices often rise, which can then push petrol and diesel prices higher.

Does war always make gas prices go up? War does not always lead to higher gas prices, but it often does when the conflict involves major oil-producing regions or key transport routes. Markets tend to react quickly to supply risks, even before actual disruptions happen.

Why do Middle East conflicts affect fuel prices worldwide? Middle East conflicts affect fuel prices worldwide because the region plays a major role in global oil production and export flows. Important routes such as the Strait of Hormuz handle a large share of global oil shipments, so any threat to supply can raise prices internationally.

How quickly do oil price spikes affect petrol prices? Oil price spikes can affect petrol prices within days or weeks, depending on the country and the fuel supply chain. The final impact depends on refining costs, transport costs, taxes, and how quickly retailers adjust pump prices.

Have wars caused major fuel price spikes before? Yes. Historical examples include the 1973 oil crisis, the 1990 Gulf War, and the 2022 Russia–Ukraine war. In each case, geopolitical conflict created supply fears that pushed oil and fuel prices higher.

What is the connection between oil prices and gas prices? Oil prices are a major component of gas prices because crude oil is refined into petrol and diesel. When crude oil becomes more expensive, the cost of producing fuel usually rises as well, which can lead to higher prices at the pump.

Could gas prices fall even if the conflict continues? Yes. Gas prices can fall if markets believe supply will remain stable, if oil producers increase output, or if demand weakens. Fuel prices depend on market expectations as much as on the conflict itself.

Why do traders watch the Strait of Hormuz so closely? Traders watch the Strait of Hormuz because it is one of the world’s most important oil shipping routes. Any disruption there can slow global energy flows and quickly push oil prices higher.

Start trading now – Click here to create your real VT Markets account