Start trading now – Click here to create your real VT Markets account

Back

Start trading now – Click here to create your real VT Markets account

Key Takeaways

Fuel prices are among the most visible indicators of economic conditions. When petrol prices rise or fall, the effects ripple through transportation costs, consumer spending, and inflation.

Although drivers experience fuel prices locally at the pump, the forces behind them are global. Oil supply and demand, geopolitical tensions, refining capacity, government policy, and currency movements all combine to determine what consumers pay.

Understanding these dynamics helps explain why fuel prices can change rapidly and why they remain one of the most closely watched indicators in the global economy.

At the centre of fuel pricing is crude oil, the raw commodity refined into petrol, diesel, and aviation fuel.

Global oil prices are typically measured against benchmark contracts such as Brent crude and West Texas Intermediate (WTI). These benchmarks act as reference points for oil traded across international markets.

When crude oil prices rise, fuel prices usually follow.

Oil prices move based on several core factors.

Strategic shipping routes also play a critical role. For example, the Strait of Hormuz handles roughly one fifth of the world’s oil shipments, making it one of the most important energy corridors in global trade.

Interested in trading Energies? Download the VT Markets app and monitor real-time CFD price action on Crude Oil (CL-OIL) and other energy-related charts.

Fuel prices are not determined by crude oil alone. Several cost layers are added before petrol reaches the pump.

A simplified version of the fuel price structure looks like this:

Fuel price = crude oil cost + refining cost + distribution + taxes + retail margin

Each component contributes to the final price drivers see.

Because these components vary by country, petrol prices can differ significantly between regions even when crude oil prices are similar.

Energy markets are highly sensitive to geopolitical events.

Conflicts involving oil-producing nations, sanctions on exporters, or instability along shipping routes can restrict supply and push oil prices higher. Even the threat of disruption can trigger market volatility as traders anticipate shortages.

Recent years have demonstrated how quickly geopolitical tensions can affect fuel prices, particularly when major energy producers or transportation routes are involved.

For example, supply disruptions in the Middle East or production cuts by major exporters have historically led to sharp price movements in global oil markets.

Once crude oil is extracted, it must be refined into usable fuels.

Refineries convert crude into products such as petrol, diesel, and jet fuel. When refining capacity becomes constrained, whether due to maintenance shutdowns, regulatory limits, or operational issues, the supply of refined fuels may tighten even if crude oil production remains stable.

Transport logistics also influence fuel prices. Shipping, pipelines, and trucking networks are required to move refined fuel from refineries to storage terminals and retail stations.

Any disruption within these supply chains can push prices higher.

For more market commentary, explore the latest Analysts’ report on oil markets on VT Markets.

Oil is traded globally in US dollars, meaning exchange rates can significantly influence fuel prices.

When the US dollar strengthens, countries importing oil must pay more in local currency terms. This can push fuel prices higher domestically even if global oil prices remain stable.

Conversely, when the dollar weakens, imported oil becomes cheaper for many countries, easing pressure on fuel prices.

Currency movements, therefore, play an important role in how global energy costs translate into local pump prices.

Fuel prices influence far more than transportation costs.

Energy is a fundamental input for industries such as logistics, manufacturing, agriculture, and aviation. Rising fuel prices can increase operating costs for businesses, which may ultimately pass those costs on to consumers.

As a result, energy prices often feed directly into inflation data. This is why central banks and policymakers closely monitor oil and fuel markets.

For investors and traders, movements in oil and fuel prices can signal broader shifts in economic growth, supply chains, and geopolitical risk.

In recent years, oil markets have experienced significant volatility due to shifting geopolitical conditions, production adjustments, and changes in global demand.

Brent crude, the international benchmark, has frequently traded between the range of $70 and $90 per barrel, while WTI crude has typically followed a similar trend at slightly lower levels.

Events such as production cuts by major exporters, supply disruptions, or geopolitical tensions can quickly push prices toward the higher end of this range.

Because crude oil remains the largest component of fuel costs, these market movements often translate directly into fluctuations at the pump.

Fuel prices reflect the intersection of global oil markets, geopolitical developments, refining capacity, taxation, and currency movements. While consumers experience these costs locally, the forces shaping them are overwhelmingly international.

As global energy demand evolves and geopolitical risks continue to influence supply chains, fuel prices will remain one of the most important indicators of economic conditions worldwide.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Start trading now – Click here to create your real VT Markets account

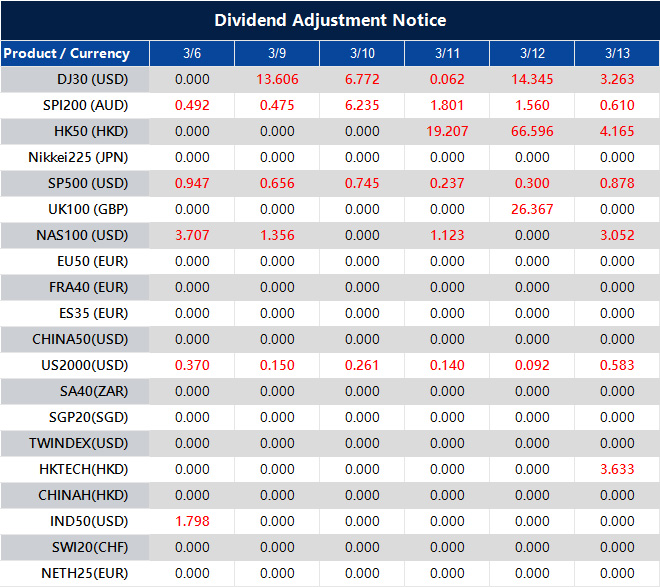

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Hello there 👋

Hello there 👋

Scan the QR code with your smartphone to start a chat with us, or click here.

Don’t have the Telegram App or Desktop installed? Use Web Telegram instead.