Samsung Electronics might invest $7 billion in an advanced packaging plant for AI chip production in the US.

Samsung Electronics is planning to invest $7 billion in a new packaging plant for high-bandwidth memory in the United States. This facility will be near Samsung’s existing chip factory in Taylor, Texas, boosting its role in the AI chip supply chain.

At the same time, SK Hynix is considering adding a new DRAM production line in the U.S. This expansion might go beyond their planned advanced packaging plant in Indiana, which is backed by the CHIPS Act.

These moves highlight South Korean chipmakers’ efforts to strengthen their U.S. presence due to the growing demand for AI semiconductors. The U.S. government is also encouraging this shift to localize semiconductor supply chains.

We view these developments from Samsung and SK Hynix as very positive for the semiconductor sector, particularly for memory manufacturers. In the short term, we should focus on call options for these companies to take advantage of potential gains from this news. Their investment in the U.S. shows a strong commitment to a piece of the expanding AI infrastructure market.

This news is especially important as we approach mid-2025 when the demand for high-bandwidth memory is expected to exceed supply. Recent industry analysis from Q2 2025 shows that demand for advanced memory could grow by another 40% in 2026, driven by new AI technologies. These U.S. facilities aim to capture that future growth and reduce supply chain risks for major American clients.

We should also look at semiconductor equipment manufacturers. Companies like Applied Materials and Lam Research, which provide fabrication and packaging tools, could receive significant orders from these big projects. Buying call options on these suppliers could be a smart way to invest in this wider cycle of investment.

Reflecting on past trends, we recall the significant stock price increases in late 2023 and throughout 2024 when the CHIPS Act funding was first announced. We can expect a similar pattern now, which may lead to higher volatility for stocks connected to these announcements. This suggests that buying straddles or strangles could be effective strategies to exploit expected price changes, regardless of market direction.

For a more diversified position, we can consider options on semiconductor ETFs like SOXX or SMH. The Philadelphia Semiconductor Index (SOX) has seen strong gains this year, and this new wave of investment news adds to the sector’s positive momentum. This strategy allows us to benefit from the overall market trend while minimizing risks related to individual companies.

China aims to improve coordination of investment funds to target key strategic development sectors.

China aims to improve the teamwork between national and local government investment funds to support its strategic development goals. The National Development and Reform Commission (NDRC) has released draft guidelines for public feedback, focusing on how funds are allocated and assessed.

The NDRC indicates that government-funded venture capital should concentrate on “new productive forces” to address technological challenges in key areas. National funds will support industries specified in official strategic catalogs, including those in the Catalogue of Industries for Encouraging Foreign Investment.

Boosting Modern Strategic Industries

The goal is to enhance modern strategic industries, making public investment align more closely with national economic objectives. These proposed changes are part of Beijing’s larger strategy to foster innovation, modernize industries, and achieve high-quality growth. The new draft guidelines provide a clear direction for government investment. We can expect more funding and policy backing for China’s high-tech and strategic manufacturing sectors. In the near future, derivative traders should focus on assets related to these areas, as they are likely to perform better. Traders should consider call options on ETFs that emphasize Chinese technology and innovation. For example, the Invesco China Technology ETF (CQQQ) and the KraneShares SSE STAR Market 50 Index ETF (KSTR) align well with the prioritized industries. The STAR 50 index faced a tough first half of 2025, dropping nearly 8%, but might see a rebound due to this targeted support. This initiative is reminiscent of the “Made in China 2025” plan from ten years ago, which led to a significant rally in sectors like robotics and electric vehicles. Historical trends suggest we can think about longer-term options, indicating that this is not just a short-term boost but the beginning of a prolonged policy effort. This hints at a trend that could extend into 2026.Market Volatility and Strategic Changes

Implied volatility for options in these targeted sectors will likely increase in the coming weeks as the market processes this news. The CBOE China ETF Volatility Index (VCHIX) has been around a stable 28 but might climb to the mid-30s. This presents a chance for traders wanting to sell volatility or to buy options before they get pricier. On the flip side, this focused strategy may lead to less funding for older, traditional industries. Traders should consider protective put options on ETFs that heavily overlap with sectors not listed in the strategic catalogs, such as real estate or basic materials. The Global X MSCI China Real Estate ETF (CHIR) has not performed well this year and could face more challenges. The government is essentially highlighting favored industries, such as semiconductors, artificial intelligence, and green technology. In the upcoming weeks, our trading strategies should focus on these “new productive forces.” We will be monitoring for updates from the NDRC to get confirmation on the final details and timing of these investment changes. Create your live VT Markets account and start trading now.Chinese investors are rapidly pulling out of gold ETFs to invest in local stocks.

Chinese investors are pulling money out of gold-backed ETFs at a record pace and putting it into local stocks. In July, four major gold ETFs—Huaan Yifu, Bosera, E Fund, and Guotai—had a total outflow of about 3.2 billion yuan (US$450 million).

This trend comes as the CSI 300 Index rose by 5.5% in July, marking its best performance since September. Investors are taking profits from gold, which has increased by around 25% this year, but has stabilized since April.

Investment Trends

Chinese stocks are gaining strength thanks to government actions aimed at reducing price wars and overproduction. Commodity stocks have rebounded after three years of poor performance, thanks to supply-side reforms and a $167 billion hydropower project in Tibet. However, equity ETF flows in Shanghai and Shenzhen have recently been negative. With Chinese investors selling gold ETFs and buying local stocks, there’s a clear shift happening. The notable outflow of 3.2 billion yuan from key gold funds in July indicates that investors are locking in gains. This money is now being used to chase returns in the domestic stock market. The CSI 300 Index is up 5.5% this month, showing renewed investor confidence. Given this momentum, traders might want to consider buying bullish positions on Chinese stocks through derivatives. This could mean buying call options on A-share ETFs like the Xtrackers Harvest CSI 300 (ASHR) to capture potential gains in the coming weeks.Economic Indicators

This optimism is backed by new economic data. China’s official manufacturing PMI for July is at 50.8, which is above expectations and signals growth for the fourth consecutive month. This suggests that government stimulus is positively impacting the economy, driving the stock market rise. Meanwhile, the price of gold has plateaued since its peak in April 2025, mostly trading sideways. After a 25% rise this year, the withdrawal by major investors could create challenges ahead. We should consider strategies that take advantage of this weakness, such as buying put options on the SPDR Gold Shares (GLD). Historically, similar patterns have occurred. After gold peaked in 2011, it entered a long bear market as investors turned back to other assets. The current outflows from Chinese ETFs might be an early sign of a similar, though smaller, shift in sentiment. A relative value trade is fitting for now. We could go long on CSI 300 futures while simultaneously shorting COMEX gold futures. This strategy would profit if Chinese stocks continue to outperform gold, shielding the trade from broader market fluctuations. However, we should be cautious since overall equity ETF flows in China remain negative. This indicates that the current rally might not be widespread and could focus on sectors supported by the government, like commodities. Targeting these specific areas may be a smarter move than betting on the whole market. Create your live VT Markets account and start trading now.Waller may side with Trump to position himself for a future Fed leadership role.

The upcoming Federal Open Market Committee (FOMC) meeting might see something unusual: several governors may vote against the Fed chair for the first time since 1993. This split reflects the current situation in monetary policy during a leadership change, with Chair Jerome Powell and most officials supporting a cautious approach.

Governors Christopher Waller and Michelle Bowman, both appointed by President Trump, might disagree because they back rate cuts, aligning their views with Trump’s calls for a looser policy. Waller sees dissent as a principled stance, stressing the importance of dissenting for the right reasons and avoiding “serial dissent.”

Fed Leadership Dynamics

Some colleagues think Waller’s dissent is his best chance to be considered for Powell’s job when Powell’s term ends. Waller has shown interest in this role, and his actions this week may be crucial for his future. The political dynamics within the Fed could pose risks to its stability. The potential for a politically motivated disagreement at today’s FOMC meeting introduces new risks for us. We now need to consider that Fed policy may become less predictable and more influenced by political events. This uncertainty often leads to increased volatility in the weeks to come. Given this, we should pay attention to options markets, where volatility might be undervalued. The MOVE Index, which tracks bond market volatility, has been stable this month after the last CPI report showed core inflation dropping to 2.8%. A dissenting voice, especially seen as politically motivated, could trigger a spike in interest rate volatility, making long positions in options appealing.Potential Market Implications

Currently, the chance of a rate cut by the September meeting is low, with the CME FedWatch Tool showing only a 15% likelihood. A strong dissent from Governor Waller could cause the market to rethink the rate path later this year, creating opportunities in SOFR and Fed Funds futures contracts for December 2025 and beyond. Looking back to late 2018, we saw a similar scenario when political pressure on the Fed’s independence coincided with a significant market downturn and a VIX that rose above 35. While history doesn’t repeat exactly, it highlights how markets react to this kind of uncertainty. Buying low-cost, out-of-the-money puts on major indices could serve as a smart hedge. This situation could also weaken the U.S. dollar. A Fed that seems more dovish usually has a negative impact on its currency. Shorting the dollar against currencies of central banks that are more hawkish might become a popular strategy. Create your live VT Markets account and start trading now.CPI data impacts the decline of the Australian dollar, confirming expectations for an RBA rate cut.

Australia’s inflation data for Q2 2025 shows the headline Consumer Price Index (CPI) at 2.1% year-on-year, slightly below the expected 2.2%. The trimmed mean CPI is on target at 2.7% year-on-year.

These figures indicate a possible 25 basis point interest rate cut by the Reserve Bank of Australia (RBA) at its meeting on August 11 and 12. Previously, there were expectations for a cut, but the RBA held the cash rate steady, leaving uncertainty in the air.

Inflation Numbers and Implications

The new inflation data for the second quarter was softer than expected. This increases the chances of the RBA cutting its cash rate in August, which is putting downward pressure on the Australian dollar. Interest rate futures show the likelihood of a 25 basis point cut has jumped to over 90%, up from around 75% before today’s data. The market is clearly expecting lower rates in the near future, which is influencing current trading activity. For traders, buying put options on the AUD/USD could be a strategic move. This would benefit from a decline in the Australian dollar if the RBA decides to cut rates. Implied volatility is also lower, making these options a potentially cheaper way to express a bearish outlook.Past Decisions and Future Expectations

It’s important to remember the RBA’s choice to keep rates unchanged during their last meeting in July 2025, even when a cut was widely anticipated. The RBA cited persistent services inflation as a reason for their decision, which could influence future choices. This recent surprise shows that nothing is certain. Australian 2-year government bond yields have already dropped following the inflation data, falling below the current RBA cash rate. This suggests that the bond market is expecting at least one rate cut soon. Traders may also consider positions in short-term interest rate swaps to take advantage of this trend. Create your live VT Markets account and start trading now.Consumer prices in Australia rise slower than expected, suggesting a potential cash rate cut by the RBA

Australia’s Consumer Price Index (CPI) for the second quarter of 2025 increased by 2.1% compared to last year. This is a bit lower than the expected 2.2%. However, the trimmed mean CPI rose by 2.7% as expected. These figures could lead to a 25 basis point cut in the cash rate by the Reserve Bank of Australia (RBA) in August.

Consumer prices have grown at the slowest rate in over four years, with core inflation hitting a three-year low. Following this inflation data, the Australian dollar has weakened. The Reserve Bank of Australia will meet on August 11 and 12.

Upcoming RBA Rate Decision

Given the soft inflation numbers for Q2 2025, a rate cut by the RBA next month seems almost certain. The market is pricing in over a 90% chance of a 25 basis point cut at the August 12th meeting, which opens up clear opportunities in the coming weeks. Traders should prepare for falling interest rates by opting for fixed rates in the swaps market. This outlook is backed by recent data, including weak retail sales figures from June 2025, indicating less consumer activity. It’s best to take these positions before the RBA meeting. We also expect Australian government bond futures to rise, especially the 3-year contracts which are most responsive to cash rate changes. Bond prices typically go up as yields drop in anticipation of central bank easing. Looking back to 2019, we saw the market respond ahead of the RBA’s actions, and we anticipate a similar trend now.Impact on Currency and Stocks

The Australian dollar is likely to weaken further against the US dollar, especially since the Federal Reserve is expected to keep rates steady. This difference in policies makes buying AUD/USD put options an attractive way to profit from or protect against a declining currency. A drop below this year’s lows appears more likely. For the stock market, these factors favor the ASX 200 index. Lower borrowing costs will help rate-sensitive sectors like real estate and banking. We expect increased buying in ASX 200 futures as investors prepare for a more supportive monetary policy. This perspective is further supported by the latest jobs report for June 2025, which showed the unemployment rate rising to 4.2%. This gives the RBA strong reasons to cut rates, addressing inadequate inflation and a weakening labor market. Governor Bullock has already indicated a cautious, data-driven approach in recent speeches. Create your live VT Markets account and start trading now.PBOC sets central USD/CNY rate at 7.1441, injecting 309 billion yuan

The People’s Bank of China (PBOC) set the USD/CNY central rate at 7.1441. This is lower than the estimated rate of 7.1742, showing how PBOC manages the currency in a floating exchange rate system.

The last closing rate was 7.1774. In this system, the yuan can change within a range of +/- 2% around the central rate.

Recent Financial Moves

The PBOC injected 309 billion yuan into the market through 7-day reverse repos at an interest rate of 1.40%. Out of this amount, 150.5 billion yuan will mature today, resulting in a net injection of 158.5 billion yuan. This yuan fixing sends a strong message from officials. The rate was set much stronger than expected, indicating a desire to prevent the currency from weakening further. This represents the largest difference between the official rate and market predictions in over a year. This action likely reflects that China’s Q2 2025 GDP growth surpassed expectations at 4.9%. This gives authorities confidence to strengthen the currency. The move aims to boost investor confidence and counter the ongoing capital outflows seen in the first half of 2025. It also strengthens Beijing’s position ahead of new trade talks with Washington next month. In the coming weeks, we should consider buying put options on the USD/CNY pair to bet on further yuan strength. With this surprising decision, implied volatility has likely risen, making it interesting to sell high-strike call options on USD/CNY for potential profit. The 7.20 level now looks like a strong ceiling for the dollar against the yuan.Strategic Financial Decisions

We’ve seen this strategy before, especially in 2019 and 2023, when the central bank acted to defend the currency against rapid declines. Historical patterns suggest these strong fixes are just the beginning of a policy effort that could last for several weeks. Therefore, we should not expect significant yuan weakness in the near future. A stronger yuan usually increases China’s buying power for commodities, which could support industrial metal prices. Copper, which was around $8,400 per tonne in July 2025, may find solid support here. We should also expect stronger currencies from key trading partners, like the Australian dollar. The large cash injection into the banking system is key to this strategy. It shows that while officials want a stronger currency, they aim to maintain domestic credit and not slow the economy. This dual approach tells us to focus on currency intervention rather than anticipating a broad tightening of financial policy. Create your live VT Markets account and start trading now.The US dollar continues to decline against major currencies as we await Australian inflation figures

The US dollar is continuing to drop against major currencies during the Asian morning trading session. There hasn’t been any new information added to what’s already known.

All eyes are on upcoming Australian inflation data, which could impact the currency markets. We are closely watching the dollar’s movements as data releases could also have an effect.

US Dollar Loses Ground

The US dollar is losing ground, indicating a shift in market sentiment. Last week, the preliminary estimate for Q2 2025 GDP showed only a 1.4% growth, which was lower than expected. This has led to the belief that the economy may be slowing down. Traders seem to be adjusting their positions in anticipation of more significant data releases. This decline follows the Federal Reserve’s decision to keep interest rates unchanged during its July 2025 meeting, where the tone suggested a more cautious and data-focused approach. Currently, futures markets are reflecting a 65% likelihood of a rate cut by the end of 2025, a significant rise from the 40% chance just a month ago. This has been putting steady, albeit modest, pressure on the dollar. For those trading derivatives, implied volatility in key currency pairs is at a notably low level. The Currency Volatility Index (CVIX) is around 6.8, a figure we haven’t seen consistently since the calm periods of early 2024. In this environment, buying options is relatively cheap, helping traders position themselves for larger market moves with limited risk.Looking Ahead to Australian Inflation Data

We are closely watching the upcoming Australian inflation data for Q2 2025, which will be released soon. The market expectations are for a 0.8% quarterly increase, but if the data comes in higher than this, it could sharply boost the Australian dollar against the US dollar. Consider short-term AUD/USD call options as a way to take advantage of this event risk. Looking back to late 2023, we saw the market start anticipating the end of the Fed’s aggressive interest rate hikes. During that time, the dollar began a slow, steady decline as economic data softened. This pattern suggests that the current market conditions could lead to a longer-term trend rather than just a temporary dip. Create your live VT Markets account and start trading now.Confidence in New Zealand businesses increased to 47.8%, while activity decreased to 40.6%

New Zealand’s business confidence rose to 47.8% in July, up from 46.3% in June. However, business activity dipped slightly to 40.6%, down from 40.9%.

Agriculture saw growth, but construction and retail deteriorated further. Indicators for future activity showed little change during the month.

Business Confidence vs. Activity

The increase in business confidence to 47.8% might be misleading. The more important figure, business activity, actually decreased, indicating that how businesses feel doesn’t reflect their actual performance. This suggests the economy is stagnant without clear progress. This mixed data means the Reserve Bank of New Zealand is likely to keep the cash rate at 5.50% for now. They face weak demand locally and persistent inflation, which suggests the New Zealand dollar will stay in a narrow range. We see limited chances for significant currency movement in the coming weeks.Sector Differences and Trading Opportunities

The key takeaway is the stark divide within the economy. Notably, agriculture is “storming ahead,” while construction and retail are facing a “renewed slump.” This difference between sectors offers clearer trading opportunities than betting on the economy as a whole. To take advantage of this, we are considering call options on agriculture-related companies. The recent 3.1% rise in the Global Dairy Trade auction supports the strength of this sector, providing a direct way to trade the positive trend mentioned in the survey. On the flip side, we are looking at put options for major retail and construction firms. Official data shows retail sales volumes fell by 1.2% last quarter and building consents are also declining. This confirms the reported slump, offering a clear opportunity to bet against these sectors. Create your live VT Markets account and start trading now.Modifications on ECN Account – Jul 30 ,2025

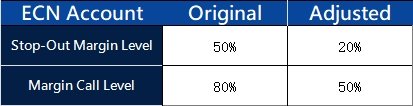

Dear Client,

To provide our valued clients with an enhanced trading environment, VT Markets will adjust certain trading conditions for ECN account on August 2, 2025:

Friendly reminder:

1.All account settings stay the same except for the above adjustments.

2.All account types now have the same Stop-Out and Margin Call Level.

If you’d like more information, please don’t hesitate to contact [email protected].