Start trading now – Click here to create your real VT Markets account

Back

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Key Points

Gold prices weakened as the U.S. dollar continued to strengthen, pushing bullion toward a weekly loss. Futures in New York slipped 0.6% to $5,095.30 a troy ounce, while spot gold hovered around 5075.35, down -4.43 (-0.09%).

A stronger dollar often creates headwinds for gold. When the U.S. dollar index rises to 100.06, up 0.3%, dollar-denominated commodities become more expensive for international buyers. This tends to reduce demand from outside the United States and can weigh on bullion prices.

The dollar’s strength also reflects broader risk dynamics. Traders have moved into the currency as geopolitical tensions and volatile energy markets increase uncertainty.

If the dollar holds near 100.06 or continues climbing, gold may struggle to regain upward momentum in the near term.

Rising oil prices have introduced another challenge for bullion. Higher energy costs can increase inflation expectations, which complicates the outlook for Federal Reserve policy.

Analysts at ANZ note that the dollar has strengthened partly because the United States is a net energy exporter, meaning rising oil prices can support the U.S. economy relative to energy-importing regions.

This dynamic shifts capital toward the dollar while creating pressure on gold. When energy prices rise, traders may anticipate higher interest rates or a delay in rate cuts as central banks try to contain inflation.

If oil prices remain elevated, markets may continue adjusting expectations for U.S. monetary policy, which could keep pressure on gold.

Uncertainty surrounding Federal Reserve policy remains a central theme for bullion traders. Higher oil prices increase the possibility that inflation pressures return, which could complicate the timing of interest rate cuts.

Gold tends to perform best when interest rates fall or when traders expect easier monetary policy. When rate cuts appear less certain, yields can rise and reduce the appeal of non-yielding assets such as gold.

Markets are therefore balancing two competing forces: geopolitical risks that support safe-haven demand, and monetary policy uncertainty that limits upside momentum.

If incoming data suggests inflation remains sticky, expectations for rate cuts may fade further and gold could remain under pressure despite ongoing geopolitical tensions.

Gold (XAUUSD) is trading near 5,075, slightly lower on the session, as the metal continues to ease after the earlier rally that pushed prices to a peak around 5,598.60.

The recent price action suggests the market is undergoing a consolidation phase, with momentum cooling as traders digest the strong gains seen earlier in the year.

From a technical perspective, gold is currently hovering around its short-term moving averages. The 5-day moving average (5,132) and 10-day (5,147) sit just above the current price, indicating mild downward pressure in the near term. Meanwhile, the 20-day moving average (5,121) is close to the market and beginning to flatten, while the 30-day moving average (5,062) remains below current levels and continues trending upward, suggesting that the broader bullish structure is still intact.

Immediate support is located near 5,050–5,070, where the market is currently attempting to stabilise. A break below this zone could expose further downside toward 4,950–5,000, which represents a stronger structural support area.

On the upside, initial resistance appears near 5,130–5,150, followed by a more significant resistance zone around 5,250–5,300, where recent rallies have stalled.

Overall, gold appears to be consolidating within a broader uptrend, with the current pullback likely reflecting short-term profit-taking rather than a full reversal.

Holding above the 5,000 psychological level would keep the longer-term bullish outlook intact, while a sustained move back above 5,150 could signal renewed upward momentum.

Learn more about trading Precious Metals on VT Markets here.

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

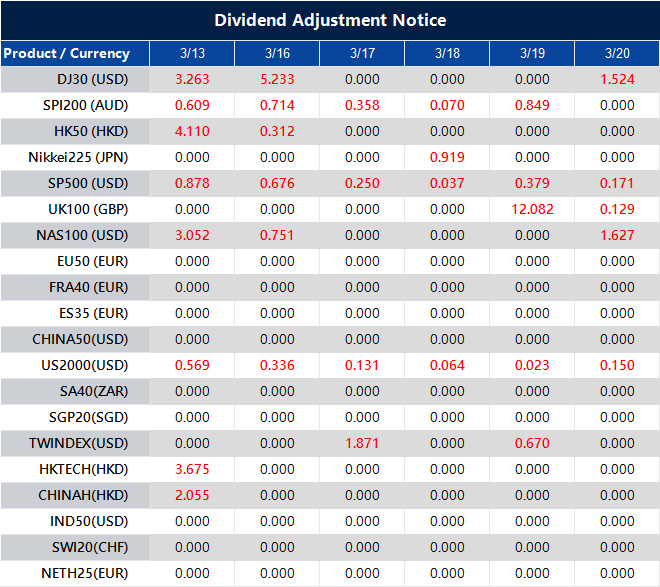

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Hello there 👋

Hello there 👋

Scan the QR code with your smartphone to start a chat with us, or click here.

Don’t have the Telegram App or Desktop installed? Use Web Telegram instead.