Von der Leyen says AI is changing tech rivalry, prompting a need for more investment and competitiveness efforts

European Commission President Ursula von der Leyen spoke about how artificial intelligence is changing global tech competition. She mentioned signing initial pilot projects for AI gigafactories and emphasized the need for more public and private investment.

Von der Leyen highlighted issues like job losses to non-market economies and expressed her desire for competitiveness to be prioritized, similar to defense. The Commission aims to turn Mario Draghi’s competitiveness report into real policies and actions.

Italy’s final CPI and HICP for August were both 1.6%, with a slight increase in core inflation.

Italy’s consumer price index (CPI) for August remains at 1.6% compared to a year ago, consistent with early estimates. This is slightly down from last month’s reading of 1.7%.

The harmonized index of consumer prices (HICP) also confirmed an annual rate of 1.6%, down from 1.7% last month. Meanwhile, core inflation increased slightly from 2.0% in July to 2.1% in August.

European Central Bank Concerns

The European Central Bank (ECB) keeps a close eye on these inflation numbers. Currently, challenges are affecting Germany more significantly. Despite a small delay in reporting, the figures suggest a steady inflation outlook for Italy. Italy’s confirmed annual inflation rate of 1.6% for August 2025 continues to indicate a cooling trend, which is good news for the ECB. However, the rise in core inflation to 2.1% is a warning sign. This suggests that underlying price pressures remain even as the main inflation figure decreases. This situation contrasts sharply with Germany’s recent figure, where inflation stands high at 3.2%. This divergence poses a major challenge for the ECB since it must develop a single monetary policy that accommodates both a cooling Italy and an overheating Germany. As a result, we expect the ECB to keep interest rates higher for a longer time than previously thought.The Impact on Bond Markets

For traders, the obvious move now is focusing on the spread between Italian and German government bonds. This morning, the BTP-Bund spread widened to 155 basis points. With the ECB having to respond to German inflation, we anticipate this spread may increase further towards the 170-175 basis point range in the upcoming weeks. One effective trading strategy is to sell Italian BTP futures while buying German Bund futures. This approach profits as the perceived risk of holding Italian debt rises compared to safer German debt. This strategy has previously succeeded, especially during uncertain ECB policy times, like late 2022. Growing uncertainty around the ECB’s next actions suggests increased interest rate volatility. Options on Euribor futures are now gaining interest, as they offer opportunities to profit from significant rate changes without predicting a specific direction. Currently, the market only sees a 20% chance of a rate cut by year-end, a decrease from last month’s 50%. This tension within the Eurozone puts the euro in a tricky position against the dollar. While a strict ECB could support the euro, worries about economic struggles in countries like Italy may limit any major increases. This suggests a period of range-bound trading for EUR/USD, making options strategies that capitalize on this sideways movement worth exploring. Create your live VT Markets account and start trading now.The dollar weakens in early European trading as EUR/USD approaches the key 1.1800 level

The dollar is falling as trading begins in Europe, continuing its decline from last week. The EUR/USD pair is nearing the 1.1800 mark, up 0.3% to 1.1797, which suggests it could rise further.

However, large option expiries around this level may slow progress until the US retail sales data is released. Other currencies are also showing similar trends. The USD/JPY has dropped 0.4% to 146.72, while the GBP/USD has increased by 0.3% to 1.3638.

Attention on a Weaker Dollar

The spotlight on a weaker dollar is growing and could be a major concern if the Federal Reserve takes a softer approach in its upcoming announcements. The dollar’s decline is setting the stage for tomorrow’s important Fed meeting. Recent data supports this softer stance. The August 2025 inflation report showed the Consumer Price Index (CPI) cooling to 2.8%, falling short of expectations, marking the third consecutive monthly drop. This gives the Fed room to suggest that its tightening cycle, which began in 2023, is over. For traders watching EUR/USD, testing the 1.1800 level is crucial. Given the situation, buying out-of-the-money call options set to expire in the next few weeks might be a smart way to play a breakout above this level, especially if the Fed signals a gentler approach. This strategy aims for a significant upward move while managing risk, keeping in mind that large option expiries might limit movement in the short term. In USD/JPY, the drop toward 146.00 shows the market is expecting a reduction in interest rate differences. We might consider buying put options to take advantage of further declines in this pair if the Fed appears more dovish than anticipated. This trend is supported by the Bank of Japan’s slow policy normalization throughout 2025, which has bolstered the yen.Higher Volatility Around Fed Shift

The key takeaway for the coming weeks is that volatility is likely to increase due to the Fed pivot. Traders might think about volatility plays, like purchasing straddles on major pairs like EUR/USD, which could benefit from a significant price move in either direction after tomorrow’s announcement. This approach is wise since market reactions to policy changes are often sharper than the initial signals. We have seen similar patterns during past Federal Reserve shifts, such as the late 2023 shift when signals of halting rate hikes led to a multi-month decline in the dollar index. The recent economic data, especially the lower-than-expected August non-farm payrolls, which showed only 150,000 new jobs, suggests we are entering a similar period. This historical context strengthens the belief that we may be at the beginning of a longer-term trend of dollar depreciation. Create your live VT Markets account and start trading now.Initial claims surge in Texas raises concerns about fraud and misrepresents US labor market strength indicators

A recent rise in new jobless claims in Texas has been linked to fraudulent applications, affecting last week’s employment statistics. The U.S. jobless report showed claims reaching their highest level since 2021, raising concerns about the labor market and influencing expectations of lower interest rates.

Anna Wong from Bloomberg shared a statement from Sarah Fisher at the Texas Workforce Commission. Fisher indicated that the jump in claims for the week ending September 6th was due to an increase in fraudulent activity.

Positive Jobless Report Indicators

Without the effect of these fraudulent claims, last week’s jobless report would have looked better. Also, the improvement in continuing claims may suggest a stronger labor market. The next jobless claims report is expected on Thursday. It’s unclear if the data will worsen or show continued improvement. The market’s response to last week’s jobless claims now seems like an overreaction. Treasury yields fell sharply as traders anticipated a weaker labor market and a more cautious Federal Reserve. This misjudgment means positions may quickly adjust in the coming days.Market Implications And Trading Opportunities

We anticipate interest rate futures will reverse their recent gains. For instance, Secured Overnight Financing Rate (SOFR) futures for December 2025 had priced in about a 40% chance of a rate cut, but that probability is likely to drop back to around 10% this week. This presents a good chance to sell rate futures or buy put options, betting on higher yields. For equity index traders, this situation creates a classic “good news is bad news” environment. While a strong labor market is generally positive, it allows the Fed to stick to its restrictive policies. We expect increased volatility, so buying call options on the VIX, which has recently been near a low of 13.5, could be a smart hedge against a market dip as hopes for rate cuts diminish. The U.S. dollar should also gain strength from this news. After falling to around 104.40 on the DXY index due to last week’s flawed data, we expect it to rally back towards the 105.50 level. This makes going long on the dollar against currencies like the Euro or Yen an appealing move. Ultimately, all eyes are now on this Thursday’s jobless claims data. We are preparing for a return to a strong labor market, similar to data revisions seen in the post-pandemic era of 2022, when isolated data points often misled analysts. If Thursday’s numbers confirm that last week’s spike was just an anomaly due to fraud, these trades are likely to perform well. Create your live VT Markets account and start trading now.European stocks opened quietly, with major indices experiencing declines ahead of the Fed decision.

European Market Prepares

European markets are starting off slowly, causing traders to pause before significant economic events. This kind of price fluctuation often signals opportunities for strategies that can benefit from increased volatility. Today, derivative traders should focus on positioning for the US retail sales data and the Federal Reserve’s interest rate decision tomorrow. The retail sales figures from the US are critical and could influence the Fed’s meeting. A strong report may raise concerns about a more assertive central bank, putting pressure on the markets. We’ve seen this happen before in 2023, where solid economic data led to quick sell-offs in stocks as expectations for interest rate hikes grew. As uncertainty mounts ahead of the Fed’s announcement, demand for options is rising. The VIX index, which measures anticipated volatility, has jumped to 18.2 this week, up from a low of 15.6 last month. This indicates that traders are purchasing protection with puts or are preparing for a significant price movement using straddles.Market Reactions and Strategies

The decline in European indices like the DAX and FTSE MIB is linked to the anticipation of the Fed’s next steps. In previous instances, European markets reacted more strongly than US markets to the Fed’s tightening policies. Therefore, using options on the Euro Stoxx 50 can be a smart way to hedge or speculate on the potential impact of tomorrow’s US monetary policy decision across Europe. Once the Fed makes its announcement, much of the anticipated volatility is expected to diminish. This “volatility crush” offers a chance for those selling options premiums. We might then consider strategies like iron condors on major indices to benefit from the market settling into a more defined range in the following weeks. Create your live VT Markets account and start trading now.Gold’s rally continues as it reaches new highs amid dovish sentiment ahead of the FOMC decision.

Gold Price Projections

Gold prices have reached new all-time highs. This rise is driven by a cautious approach ahead of the Federal Open Market Committee (FOMC) decision. The price increase followed a US Consumer Price Index (CPI) report and a higher-than-expected number of initial jobless claims, although many claims were found to be fraudulent. Despite this, labor market data shows strength. Fewer continuing claims indicate potential improvements. Unless there are negative signals, the positive sentiment may last until the FOMC decision or another market event. Lower real yields and the expected dovish response from the Fed support a long-term uptrend. On the other hand, rising interest rate expectations could lead to short-term corrections. On a daily chart, gold’s upward trend is strong, with buyers targeting a major trendline at the 3,400 level. Sellers may wait for a break below that level to aim for a drop to 3,120. Looking at a 4-hour chart, small upward trends enhance bullish momentum, while sellers are ready to challenge at 3,400. In the 1-hour chart, prices are stabilizing above recent highs, providing minor support. Buyers are likely to keep prices up around the 3,675 level, while sellers aim for a decline to the 3,620 support. Upcoming reports, including US Retail Sales, the FOMC announcement, and jobless claims, could impact market movements.Market Expectations

Gold is hitting new highs ahead of tomorrow’s FOMC meeting. The market expects a dovish stance, especially after the August 2025 CPI report showed core inflation cooling to 2.8%. This is reflected in fed funds futures, which show over a 90% chance the Fed will keep rates steady. However, we should consider signs of economic strength that might surprise investors. Fraudulent jobless claims from Texas masked a tight labor market, and today’s retail sales report for August 2025 was better than expected at +0.5%. This raises the risk that the Fed’s statement could be more hawkish than anticipated. The difference between dovish expectations and strong data suggests that gold derivatives may be undervalued. Traders should think about using options strategies like straddles or strangles ahead of the announcement to benefit from significant price movements in either direction. Implied volatility on near-term options has risen to 18%, which could seem low if the Fed surprises the market. For those feeling bullish, long call positions or call spreads targeting prices above current highs seem sensible. If the Fed confirms a dovish stance, gold could quickly reach the $3,750-$3,800 range. Major trendline support around $3,400 offers a clear risk management point for long-term bullish strategies. On the flip side, the risk of a hawkish pullback is notable, reminding us of the market’s eagerness for a shift back in late 2023. A drop below the $3,675 level could trigger put options, with an initial target near the $3,620 support. A surprisingly strong stance from the Fed could easily reverse recent gains and push gold back towards the $3,400 trendline. The key will be to focus not just on the headline rate decision but also on the Fed’s language and economic outlook tomorrow. The fraudulent claims data reminds us that early reports can be misleading. We should be ready for the Fed to emphasize that their fight against inflation isn’t over, despite recent progress. Create your live VT Markets account and start trading now.Week Ahead: A Glimmer On The Horizon

Not everything that shines is gold. Silver is stepping back into the spotlight, too.

Traditionally viewed as a crisis hedge, both metals have shifted into the mainstream. Since 2023, gold has surged by 103% compared with a 72% rise in the S&P 500.

In 2025 alone, gold has climbed 40% and silver 44%. Gold has smashed through $3,600 per ounce to all-time highs, while silver trades around $41, its strongest level since 2011.

The takeaway is clear: investors are reassessing what constitutes stability in a world of deficits, sticky inflation, and heightened political risk.

The Three Drivers Of The Rally

Three forces underpin this bull run. First, relentless deficit spending has pushed the US fiscal shortfall close to $2 trillion annually, flooding markets with Treasuries and sending yields to their highest in 11 years.

With real returns eroded, bonds no longer look compelling, prompting a shift into tangible assets.

Second, gold’s relationship with equities has evolved. In 2024, its correlation with the S&P 500 hit 0.91, showing that gold is no longer just a backstop against weakness but also a parallel hedge against inflation and debt-fuelled expansion.

Third, safe-haven flows have gained new importance as bonds lose their anchor role in global portfolios.

Central Banks In The Lead

The official sector is a key engine of demand. For the first time since 1996, gold now outweighs US Treasuries in global reserves.

Gold accounts for around 20% of FX reserves, overtaking the euro’s 16%. The rationale is straightforward: Treasuries and SWIFT access can be frozen, whereas gold stored domestically cannot.

Purchases have been unrelenting, surpassing 1,000 tonnes annually for three consecutive years, more than double the pace of the previous decade.

China leads the charge with continuous monthly purchases, while Russia, Turkey, and India have also been steadily increasing their holdings.

A World Gold Council survey shows 95% of central banks expect global gold reserves to continue rising, with nearly half planning to increase their own.

This persistent demand suggests gold’s rally is not just cyclical but signals a deeper structural rebalancing of global reserves.

Silver’s Twin Appeal

Silver is benefitting both from investment flows and industrial use. ETFs alone added almost 1,000 tonnes in June 2025, bringing total holdings to around 24,000 tonnes.

Retail demand for coins and bars remains strong, while lease rates have surged above 5% from near zero, pointing to scarcity. A $1.20 premium has also opened up between COMEX futures and London spot prices.

Beyond financial flows, silver is central to the green transition, used in solar panels, EVs, and electronics, providing a solid demand floor.

Where Prices Could Head

The outlook for the months ahead hinges on inflation trends and central bank policy. If inflation remains elevated and the Fed pivots towards easing, gold could advance towards $4,000 by year-end.

If inflation cools and real yields strengthen, consolidation is more likely. Silver should broadly follow gold but with more volatility. A firm break above $40 could open the door to $50 – last seen in 2011 – although weaker industrial demand would expose it to sharper setbacks.

At present, the bias remains constructive. Gold enjoys strong support from deficits, inflation risks, and central bank demand.

Silver, with its mix of monetary and industrial appeal, carries higher volatility but also the potential for outsized returns if momentum continues.

Market Movements Of The Week

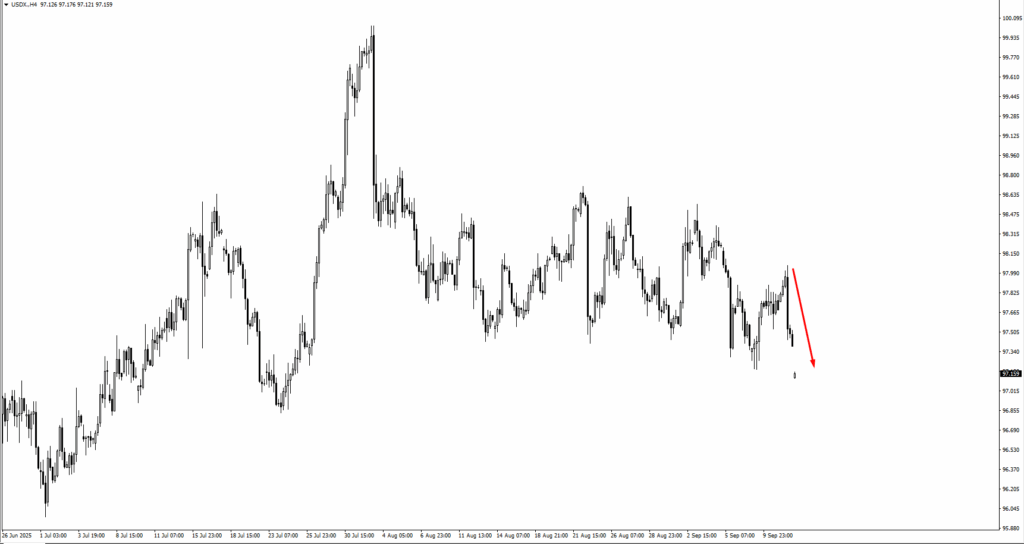

The US Dollar Index has retreated from 97.90 and risks slipping through 96.834 if weakness deepens. EURUSD is edging up from 1.1675 with scope to test 1.17795, while GBPUSD is climbing from 1.3510 and eyeing 1.35901.

USDJPY has dropped from 148.10, with a close below 147.058 opening the way towards 146.298. USDCHF is also under pressure, threatening 0.79148 if 0.7957 gives way.

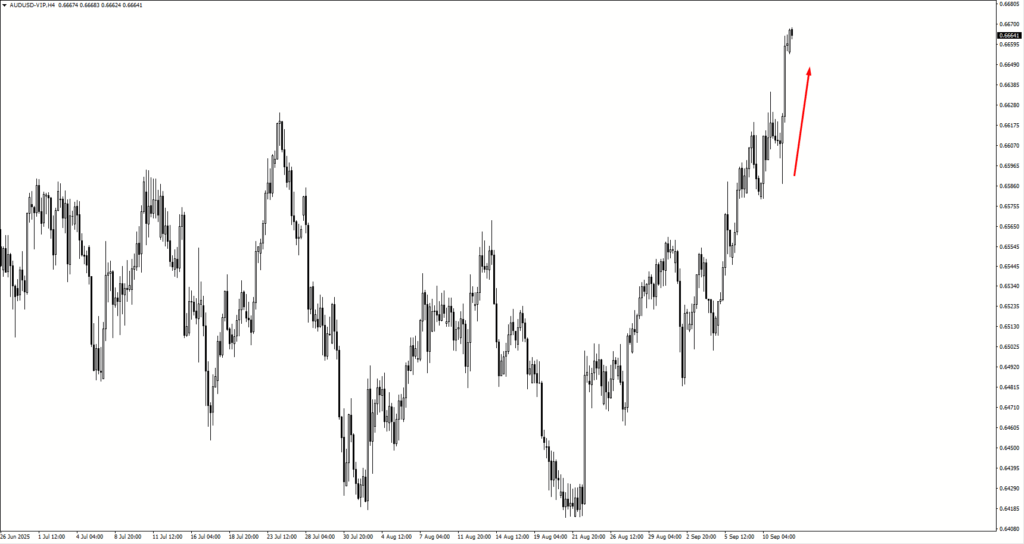

Commodity currencies are gaining ground. AUDUSD is aiming for 0.6690, NZDUSD is pushing toward 0.6000, and USDCAD has slipped under 1.38574 with 1.3820 now in focus.

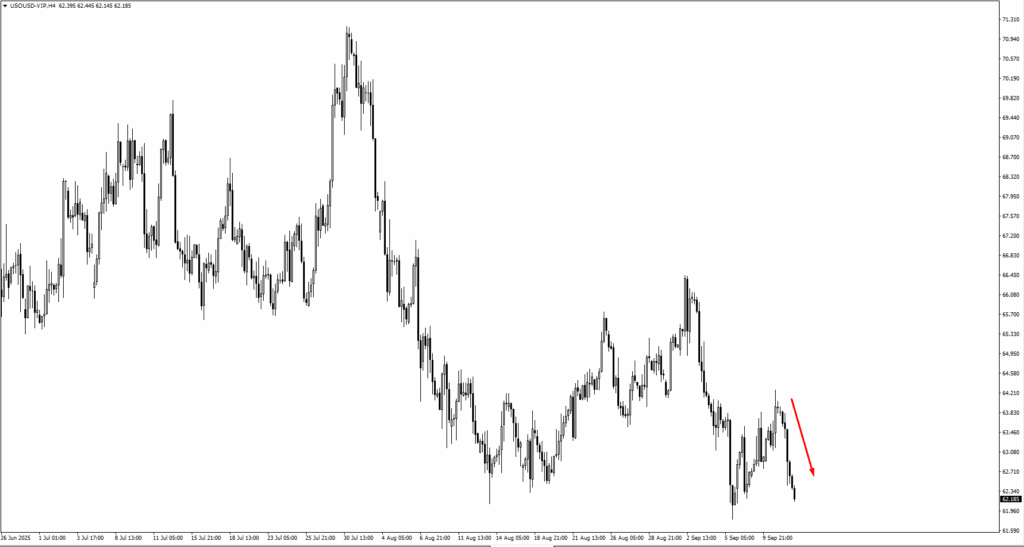

Oil remains volatile, rebounding from $62.70 before stalling at $64.35. A break under $61.804 could bring $58.40 into play.

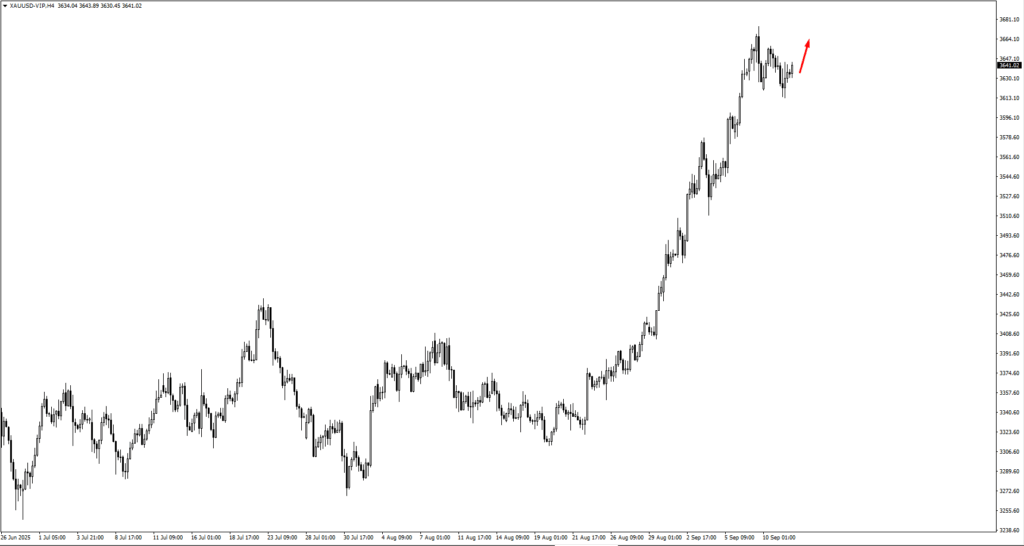

Gold is consolidating with support at $3,585 and $3,550, while a breakout could aim for $3,835. Silver is holding above $40.511, with bulls targeting $42.55.

US equities remain buoyant: the S&P 500 is testing 6,870, while the Nasdaq is pushing towards 25,450.

Crypto is firm, with Bitcoin bouncing from 110,250 toward 116,200 and Ethereum breaking higher with 4,585 in sight. Natural gas remains under pressure near 2.97.

On the equity front, UnitedHealth is holding above 326.22 with an intrinsic value closer to 410, while Novo Nordisk has rallied from 52.80 toward a fair value of 90. Earnings momentum is keeping both names supported.

Key Events Of The Week

On Tuesday, September 16, attention turns to Canada’s median CPI y/y and US retail sales m/m. For the CAD, a hot inflation print could reinforce expectations that the Bank of Canada stays cautious, giving the loonie a lift.

For the USD, retail sales will be closely watched as a barometer of consumer strength, where any slowdown could weigh on the dollar.

Wednesday, September 17 brings the Bank of Canada’s overnight rate decision. Markets are split on whether policymakers can hold steady or hint at easing, given growth headwinds.

The CAD is likely to stay sensitive to both the policy tone and inflation context.

Thursday, September 18 is stacked with event risk. The US Federal Reserve announces its federal funds rate, where traders will parse not only the decision but the language around growth and inflation. New Zealand releases its GDP q/q, a key test for the NZD after recent soft spots in data.

The Bank of England also sets its official bank rate, where the balance between inflation control and growth concerns will be critical for GBP traders.

Friday, September 19 closes the week with the Bank of Japan’s policy rate. Even small shifts in tone can rattle JPY markets, given the yen’s sensitivity to global yield differentials. Any signal that the BOJ may adjust its stance would reverberate across FX markets.

Create your live VT Markets account and start trading now.

Kazaks from the ECB says there is no current need for rate cuts, while others are considering increases.

ECB’s Kazaks has said there’s currently no reason to cut interest rates. This view is shared by many on the Governing Council.

This indicates that the ECB is halting rate cuts for now. Some members, like ECB’s Schnabel, are even thinking about possible rate increases.

End Of Interest Rate Cuts

We believe the long period of interest rate cuts has come to an end. European policymakers are currently not interested in further easing. The focus is now shifting toward discussing potential rate hikes. This change is supported by recent data showing Eurozone inflation remains high. In August, inflation rose back to 2.4%, well above the central bank’s 2% goal. This reinforces the conclusion that the easing cycle, which included three cuts earlier in 2025, has ended. The market is now adjusting to this new reality. The bond market is responding, as seen by the German 2-year yield, which rose 15 basis points just last week. This suggests that expectations for another rate cut this quarter are fading fast. Traders who anticipated lower rates are likely feeling the heat to change their positions.Market Reactions And Strategies

For those dealing with interest rate derivatives, paying fixed rates on interest rate swaps is becoming a better option. Now is also a good time to rethink any short positions on short-term interest rate futures, like those linked to Euribor. It seems that rates have stabilized for the near future. In the currency market, this shift towards a more hawkish stance is boosting the Euro, which has strengthened against the US dollar, surpassing the 1.10 mark. We should think about buying call options on the EUR/USD to take advantage of further potential gains. This strategy lets us benefit as the interest rate difference moves in favor of the Euro. We can also expect increased volatility as the market processes this policy shift. This environment makes buying options, such as straddles or strangles on major European stock indices, a smart move. These strategies can profit from significant market moves in either direction without needing to predict which way it will go. This situation reminds us of the policy pause in late 2023, when the market underestimated the central bank’s resolve to combat inflation. Those who anticipated a quick return to rate cuts were mistaken. We should learn from that time and pay attention to the clear message from policymakers today. Create your live VT Markets account and start trading now.The German ZEW report focuses on European activity, while US inflation and retail sales take center stage in American discussions.

The German ZEW report is the highlight of the European session. Expectations are for a decline to 27.3 from 34.7. However, this report is not expected to change the European Central Bank’s current approach.

Focus On Canadian And US Data

In North America, the spotlight shifts to Canadian and US data. The Canadian Trimmed Mean CPI Year-over-Year is expected to stay steady at 3.0%, which is at the top of the Bank of Canada’s target range. Even with stable inflation, attention is turning to the weakening job market, as unemployment rises to 7.1% from 6.9%. Rate cuts are predicted, with one 25 basis point cut anticipated soon and another by the end of the year. Today’s data may not heavily influence these forecasts, but a negative surprise could sway expectations for future cuts. In the US, Retail Sales Month-over-Month growth is predicted to slow to 0.2%, down from 0.5%. Meanwhile, ex-Autos is expected to rise to 0.4% from 0.3%, and the Retail Sales control group is projected at 0.4%, down from 0.5%. While this data can impact markets, its reliability is often questioned because of volatility. Overall, traders will focus on upcoming FOMC decisions and US Jobless Claims. For Europe, we do not anticipate the German ZEW economic sentiment report to create much impact. The European Central Bank has already indicated its focus on controlling core inflation, which remains high. Therefore, any short-term trades based on this sentiment data are likely to face challenges.Implications For The Canadian Dollar

Today, the Canadian inflation data is more intriguing, as the market waits to see if it stays at 3.0%. Inflation has been rising since it hit bottom at 2.5% in December 2024, but the Bank of Canada is mainly worried about the job market. With unemployment rising from 6.2% in January 2025 to 7.1% last month, the central bank has a strong reason to cut rates. For traders, this sets a clear scene for the Canadian dollar. Since the market anticipates two rate cuts by the year’s end, if inflation is lower today, traders might bet on a third cut, making put options on CAD appealing. Conversely, a surprise increase in inflation could temporarily raise the currency’s value, but it likely won’t change the Bank of Canada’s overall dovish stance. In the US, Retail Sales data is likely to show a slight slowdown in consumer spending. This report is known for its volatility and is overshadowed by the Federal Reserve’s interest rate decision tomorrow. Consumer spending has eased in 2025, so a weaker report won’t be shocking. Any immediate reaction in S&P 500 futures or the US dollar from the retail sales figures will probably be short-lived. The real market mover will be tomorrow’s FOMC statement, which will set the market direction for the weeks ahead. Traders will overlook today’s data noise and prepare for potential volatility with the Fed’s announcement. Create your live VT Markets account and start trading now.Early European trading sees modest gains in Eurostoxx and major indices, indicating stability

Eurostoxx futures have risen by 0.1% in early European trading, indicating small gains when the market opens. The German DAX, French CAC 40, and UK FTSE futures also show a 0.1% increase.

US futures share this trend with a 0.1% gain as the session approaches. Stocks are stable as investors await the Federal Reserve meeting, which is set to influence market sentiment this week.