Australia’s Westpac Leading Index fell 0.1% month on month, down from 0.08% in January

Australia’s Westpac Leading Index (month-on-month) fell to -0.1% in January. It was 0.08% in the previous period.

The Westpac leading index has moved into negative territory, falling to -0.1% in January. This points to Australian economic growth running below its long-term trend in the months ahead. The shift from small growth to contraction is an important forward-looking signal. For us, it suggests we should prepare for a possible slowdown.

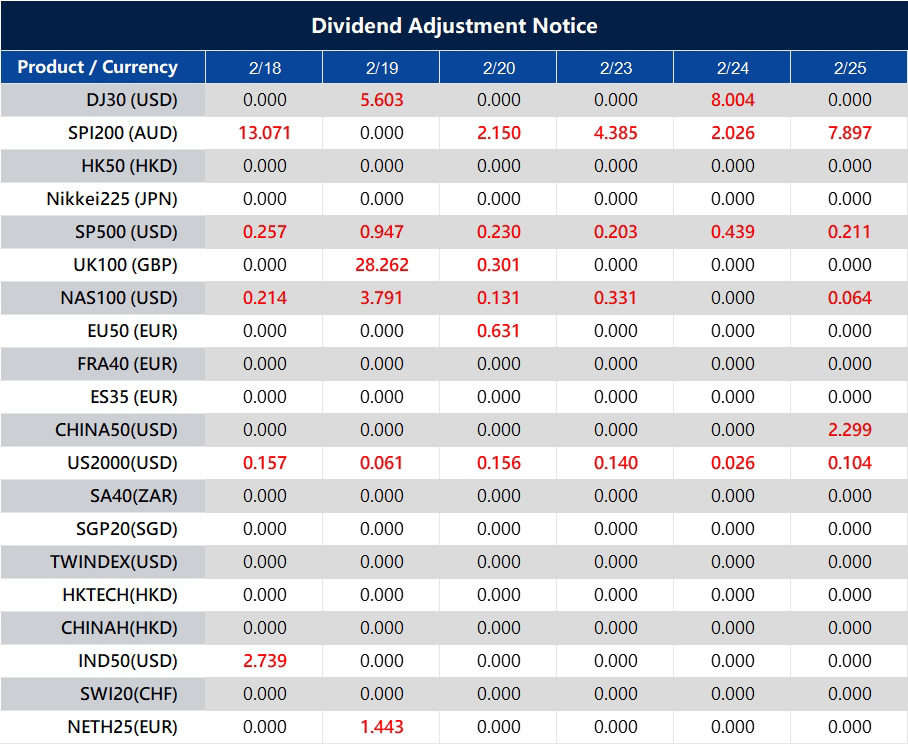

Dividend Adjustment Notice – Feb 18 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

NAB’s Australian business confidence fell to -0.1 quarter-on-quarter, down from 2 in Q4

National Australia Bank said its business confidence measure fell from the prior quarter. It dropped to -0.1 in the fourth quarter, down from 2 in the previous quarter.

Business confidence turned negative in late 2025, falling to -0.1. This is a clear bearish sign. It suggests many businesses expect weaker conditions ahead. That often leads to less investment and slower hiring. For us, this raises the odds of a weaker Australian dollar in the near term.

Implications For The Australian Dollar

We should look at trades that benefit if AUD/USD falls, such as buying put options. This view is supported by recent data showing January inflation slowing to 2.9% year over year. Lower inflation gives the Reserve Bank of Australia more room to cut rates. In the past, when business confidence dipped below zero—such as during the 2011 and 2019 slowdowns—the AUD often lagged in the months that followed. This negative mood could also weigh on the stock market by lowering expectations for corporate earnings. The ASX 200 has started 2026 slowly and has struggled to hold gains as global sentiment changes. Index derivatives can be used to hedge or to position for a downturn, such as buying put options on the XJO. Weak confidence and easing inflation also strengthen the case for a more dovish RBA. The RBA held rates steady at the early February meeting, but markets are now pricing a higher chance of a cut by mid-year. Traders should watch interest rate futures, which may react strongly to upcoming employment and retail sales releases. With more uncertainty, market volatility may rise from the calm levels seen late last year. Higher implied volatility can make options strategies more attractive. Buying protective puts on major Australian banks and miners could help protect portfolios if growth slows.Managing Risk With Options

Create your live VT Markets account and start trading now.During Asian trading, USD/CAD hovered near 1.3645 as softer CPI and lower oil prices weakened the Canadian dollar

USD/CAD rose to around 1.3645 during Asian trading on Wednesday. The Canadian dollar weakened after softer inflation data and falling crude oil prices.

Statistics Canada said Canada’s CPI inflation cooled to 2.3% year over year in January, down from 2.4% in December. The figure also came in below the 2.4% market forecast. This increased expectations of another Bank of Canada rate cut.

Oil Prices And Geopolitical Tensions

Oil prices slipped as tensions between the US and Iran eased. Iran’s Foreign Minister Abbas Araqchi said both sides agreed on the main “guiding principles” in the nuclear talks, but also stressed that a deal is not close. Canada is a major oil exporter, and lower oil prices often put pressure on the Canadian dollar. Markets are now watching the FOMC Minutes due later on Wednesday. The Minutes may offer clues about the Federal Reserve’s next moves on interest rates. If the tone is dovish, the US dollar could weaken in the near term. In February 2025, markets correctly priced in a Bank of Canada rate cut as inflation fell. The BoC followed with cuts in April and June 2025, which helped lift USD/CAD toward 1.39 by mid-year. Today, the situation looks different.How The Backdrop Has Changed

Canada’s story has shifted from cooling inflation to more persistent price pressure. Statistics Canada’s latest report for January 2026 showed CPI rising to 2.9%. That is well above last year’s levels and makes near-term BoC rate cuts less likely. This firmer inflation gives the Canadian dollar support that it did not have in early 2025. Last year, WTI crude prices weakened as geopolitical risks cooled, which weighed on the loonie. Now, crude is holding above $82 a barrel on tighter global supply forecasts for 2026. That strength is a clear tailwind for the commodity-linked CAD, reversing the pattern seen a year ago. The Federal Reserve was also central last year. By keeping rates steady through 2025, the Fed created a wide policy gap versus the Bank of Canada. Now, with Canadian inflation staying sticky, that gap is expected to narrow. This shift in rate expectations is making the US dollar less attractive compared with the Canadian dollar. Against this backdrop, USD/CAD appears more likely to drift lower. Traders may consider strategies that benefit from a falling or range-bound pair, such as buying CAD call options or selling out-of-the-money USD call options. These strategies target a possible move toward the 1.3500 support area in the weeks ahead. A key risk to this view is a stronger-than-expected US economic report that brings back hawkish expectations for the Fed. To manage that risk, a bearish put spread on USD/CAD can help define downside exposure. This approach seeks to profit from a moderate decline while limiting losses if the US dollar rallies unexpectedly. Create your live VT Markets account and start trading now.After the RBNZ holds rates steady, NZD/USD attracts sellers and retreats toward 0.6000 again

NZD/USD fell after the Reserve Bank of New Zealand (RBNZ) left policy unchanged on Wednesday. The pair drifted back toward 0.6000 after hitting a more than one-week low the previous day. Markets are now focused on whether it will break below 0.6000.

The RBNZ kept the Official Cash Rate at 2.25% at its February meeting, after three rate cuts in 2025. With no clear move toward tighter policy, the decision gave little support to the New Zealand Dollar.

Rbnz Signals And Market Reaction

In its statement, the RBNZ said inflation is moving back toward its target and it nudged its projected rate path slightly higher. It also said policy is still accommodative and that a gradual return to more normal settings is expected. Markets are watching the post-meeting press conference for clues from Governor Anna Breman about the next policy move. Meanwhile, the US Dollar stayed soft as traders expect the Federal Reserve to cut rates in June and deliver at least two cuts in 2026. Holding rates at 2.25% has pushed NZD/USD back toward the key 0.6000 level. This area has long been a major psychological support and resistance zone, and it was tested many times in 2024 and 2025. If the pair breaks below 0.6000 and stays there, it would point to stronger bearish momentum. This pause makes sense after the three cuts in 2025. New Zealand’s latest quarterly inflation data showed inflation cooled to 2.9% in Q4 2025, supporting the RBNZ view that price pressures are returning to the target band. Traders will now focus on Governor Breman’s press conference for any hint that the “gradual normalisation” path could happen faster, or be more hawkish than expected.Usd Side Volatility And Positioning

On the other side of the pair, US Dollar weakness is helping to limit losses for now. Markets are pricing in a more than 70% chance of a Federal Reserve cut by June. That view strengthened after last week’s US inflation report showed inflation easing to 3.0%. With the RBNZ on hold and the Fed potentially turning more dovish, the setup is mixed and harder to trade. For derivatives traders, this push-and-pull is lifting expected price swings. One-month implied volatility for NZD/USD options has risen to 9.5%. That suggests strategies such as buying straddles may work for traders looking to capture a breakout in either direction after the Governor’s comments or upcoming US data. There is also growing interest in put options with strikes just below 0.6000, which suggests many traders are preparing for a move lower. Create your live VT Markets account and start trading now.New Zealand’s RBNZ keeps interest rates at 2.25% as expected, with markets largely unsurprised by today’s decision

New Zealand’s central bank, the Reserve Bank of New Zealand (RBNZ), kept its official interest rate at 2.25%. This decision was in line with market expectations.

By leaving the rate unchanged, the RBNZ is keeping its current monetary policy settings. The update did not signal any further moves.

Short Term Volatility Outlook

Because the decision matched expectations, short-term currency volatility may fall. With this key event now behind the market, selling New Zealand dollar options could look more appealing over the next few days. Traders may try to collect option premiums by betting the currency moves into a calmer period. Holding rates at 2.25% reflects ongoing inflation pressure. Inflation has dropped from its 2025 highs, but the Q4 reading of 3.8% is still well above the target band. At the same time, GDP growth was weak at just 0.2% last quarter. This leaves the RBNZ trying to balance stubborn inflation against a slowing economy. Attention now shifts from today’s decision to when the first rate cut might happen. Given the bank’s cautious tone, traders may look for opportunities tied to a “higher for longer” outlook, with rate-cut expectations pushed out to late 2026. We saw something similar in late 2024, when markets priced in early easing too soon and had to adjust later. From here, the Kiwi dollar is likely to be driven more by what other central banks do, especially the US Federal Reserve.Cross Central Bank Rate Dynamics

With the Fed also signaling a pause at its January 2026 meeting, the relative rate advantage for the NZD remains steady. That could help support the currency, especially versus currencies where central banks may need to cut rates sooner. Create your live VT Markets account and start trading now.Australia’s fourth-quarter Wage Price Index rose 0.8% quarter on quarter, matching economists’ forecasts and market expectations

Australia’s Wage Price Index rose 0.8% quarter-on-quarter in the fourth quarter. This matched market expectations.

The data suggests wage growth stayed steady over the quarter. The update did not include any additional details.

RBA Policy Outlook

The fourth-quarter Wage Price Index came in at 0.8%, exactly as expected. Because of this, there is no clear reason for the Reserve Bank of Australia to change its current view. It also removes a major short-term uncertainty for markets. As a result, we expect a limited reaction in interest rate futures and the Australian dollar. With no surprise in the data, implied volatility has dropped, especially in options linked to the AUD/USD pair. This “volatility crush” can make selling option premium—using strategies such as short strangles—more appealing in the days ahead. We saw this often in 2025 when major releases landed right on consensus, which tended to reward positions built for calm markets. Annual wage growth is now running near 3.3%, still above the RBA’s preferred 2–3% range. This ongoing wage pressure supports the RBA’s decision to keep the cash rate at 4.10% and reinforces the “higher for longer” view. In cash rate futures, the market is now slightly reducing expectations for a rate cut before mid-year. For ASX 200 traders, a steady domestic rate outlook means attention is likely to shift to other drivers, such as global growth and company earnings. With no local shock, the index may continue to follow moves in U.S. markets. Option strategies that benefit from sideways or slow, gradual price action may make sense in this setting.What To Watch Next

Focus now turns to the next major releases: the monthly CPI report and employment data. This wage result supports the idea that the RBA can afford to wait. It also puts more importance on the next inflation print to justify any future policy change. Until then, we expect markets to stay within their usual ranges. Create your live VT Markets account and start trading now.Australia’s year-on-year Wage Price Index held steady at 3.4% in the fourth quarter, unchanged from the previous quarter

Australia’s Wage Price Index rose 3.4% year-on-year in the fourth quarter. This was unchanged from the previous reading.

The data shows that annual wage growth stayed the same in 4Q. The year-on-year rate held at 3.4%.

Wage Growth Holds Steady

In early 2025, the fourth-quarter 2024 Wage Price Index came in steady at 3.4%. Along with other signs of cooling at the time, this suggested the Reserve Bank of Australia’s rate hikes were starting to work. It was a key moment when markets began to shift away from expecting more tightening. Now, on February 18, 2026, events have moved much as expected. The latest official data for the fourth quarter of 2025 showed annual inflation fell to 2.8%. That put inflation back inside the RBA’s target band for the first time in years. As a result, markets are no longer focused on hikes. Instead, they are pricing in at least a 75% chance of a rate cut by the August 2026 meeting. For traders watching the Australian dollar, this points to ongoing weakness versus currencies backed by more hawkish central banks. We are seeing more interest in buying AUD/USD put options with third-quarter expiries to benefit from this expected policy gap. Implied volatility in the pair may rise ahead of the RBA’s mid-year meetings, which can make long-volatility strategies more appealing. On the other hand, the outlook for lower borrowing costs supports domestic equities and bonds. Traders may look at long positions in ASX 200 index futures, as rate-sensitive sectors such as technology and real estate investment trusts could lead any gains. Australian 3-year government bond futures have already rallied strongly, and we expect that trend to continue as the first cut gets closer. The main risk is an upside surprise in the next monthly CPI indicator or a stronger-than-expected jobs report. Either could delay the RBA’s timeline. Because of that, it may be sensible to use options to control risk—for example, buying call spreads on the ASX 200 instead of taking outright futures exposure. We also need to watch the next labour force release for any sign that underlying economic strength is improving.Key Risks And Trade Management

Create your live VT Markets account and start trading now.Gold slips near $4,860 in early Asian trade as Lunar New Year closures thin liquidity and ease demand

Gold slipped to about $4,860 in early Asian trading on Wednesday. Trading was quiet because many Asian markets are closed for the Lunar New Year. Traders are now waiting for the Federal Open Market Committee (FOMC) Minutes due later today.

Liquidity remained low because of regional holidays. Markets are also watching whether a stronger US dollar could reduce demand for gold.

Us Iran Tensions Ease

Gold also faced pressure as tensions between the US and Iran eased. Gold is often bought when uncertainty is high. Iran’s Foreign Minister Abbas Araqchi said on Tuesday that both sides agreed on key “guiding principles” in nuclear talks, but added that a deal is not close. The FOMC Minutes may give clues about where US interest rates are heading. If the Minutes sound more dovish, the US dollar could weaken, which may support commodities priced in dollars, including gold. Gold is widely used in jewellery and is often viewed as a store of value. Many investors also use it as a safe-haven asset and as a hedge against inflation and weaker currencies. Central banks hold large amounts of gold. In 2022, they bought 1,136 tonnes worth about $70 billion, the highest annual total on record. Gold often moves in the opposite direction to the US dollar and US Treasuries. It can also move differently from risk assets such as equities.Market Focus Today

With gold trading near $4,860, the key focus is the FOMC Minutes later today. Trading is thin because of the Lunar New Year holiday, which can make price moves look bigger if news surprises the market. The main question this week is what the Fed signals about the future path of interest rates. Markets are leaning toward a more dovish Fed, especially after January CPI came in a bit cooler than expected at 2.8%. If the Minutes suggest policymakers are moving toward rate cuts later in 2026, the US dollar could weaken. That would likely support gold. Some traders may look at call options if they expect a break above recent highs. Even so, gold appears to have a strong level of support, which reduces the appeal of outright short positions. Central bank buying stayed strong into late 2025. The World Gold Council also reported another quarter of solid purchases, led by emerging market central banks. This steady demand suggests that large dips may be bought quickly. Geopolitical risks still provide support, even with improving US-Iran relations. Markets are also watching rising political uncertainty ahead of key European elections and renewed tensions in the South China Sea. These issues help keep gold’s safe-haven appeal strong, making it a useful hedge in a diversified portfolio. Derivatives markets also reflect the current mood. The CBOE Gold Volatility Index (GVZ) has risen to 17.5, showing more caution ahead of the Fed release. Traders who expect a big move but are unsure of the direction may consider options strategies such as straddles or strangles to target higher volatility. In 2023 and 2024, aggressive rate hikes helped the dollar and limited gold’s upside. In early 2026, the conversation has shifted to when and how fast the Fed will ease. This change in policy expectations supports a bullish outlook for gold in the months ahead. Create your live VT Markets account and start trading now.Japan’s total merchandise trade balance was ¥-1B in January, beating forecasts of ¥-2,142.1B.

Japan’s merchandise trade balance came in at ¥-1B in January. That was much better than the forecast of ¥-2142.1B.

This means Japan’s trade deficit was far smaller than expected. No other details were included in the update.