EUR/JPY trades around 168.30 after losing over 0.50% as the Yen stays stable

EUR/JPY is holding steady near 168.50 after the Bank of Japan (BoJ) indicated it would keep interest rates the same. The potential for the pair to rise is linked to lower demand for safe-haven currencies due to the recent ceasefire between Israel and Iran. European Central Bank (ECB) member Villeroy de Galhau mentioned that interest rate cuts may be considered, even with oil market fluctuations.

After a decline of over 0.50% in the previous session, the pair is trading around 168.30 during Wednesday’s Asian hours. The Japanese Yen showed little change after the BoJ released its June meeting opinions.

The PBOC sets the yuan’s mid-point at 7.1668 and injects 209 billion yuan through repos.

The People’s Bank of China (PBOC) sets the daily midpoint for the yuan, also known as renminbi or RMB. The PBOC uses a managed floating exchange rate system, which allows the yuan’s value to change within a +/- 2% range around this midpoint.

Today, the USD/CNY midpoint is set at 7.1668, while the estimate was 7.1709. The previous close was 7.1712.

The PBOC injected 365.3 billion yuan into the market using 7-day reverse repos at a 1.40% interest rate. With 156.3 billion yuan maturing today, this means there is a net injection of 209 billion yuan.

This morning’s midpoint fix shows how the central bank is managing the currency. By setting the yuan at 7.1668 instead of the higher 7.1709, the PBOC subtly leans towards strengthening the currency. While this change is small, it’s intentional, aiming to influence sentiment without causing a major shift.

The recent close of 7.1712 indicates that the market is slightly weaker than the reference point. This means the fix suggests a strengthening perspective, but spot prices are showing some hesitance. The slight difference indicates that demand for dollars is still stronger than local interest in yuan.

With today’s operations, the PBOC injected 365.3 billion yuan through 7-day reverse repos, which is much higher than the 156.3 billion yuan maturing. This 209 billion yuan increase shows a clear commitment to keeping liquidity high. The stable 1.40% rate supports funding costs without signaling any major policy changes.

For those watching closely, this deliberate injection, along with a midpoint fix that is stronger than expected, indicates a careful balancing act by the authorities. They are providing ample liquidity but without excess. They are sending clear guidance on the exchange rate while managing internal liquidity and external currency pressures.

In the coming days, we can expect a heightened sensitivity in short-term interest rate products, especially those related to repo and short-term swaps. The focus on maintaining smooth liquidity through reverse repos means we must be quick to adjust rate positions in response to any shifts in the debt market or interbank stress.

A fix slightly below expectations often suggests a desire to limit declines in the yuan. Recently, we’ve seen this align with somewhat firmer onshore short-dated options, particularly those spanning one to two weeks. So, pricing for upside protection in USD/CNY may continue to find support, although a major repricing is not expected—at least for now.

As liquidity injections continue above the amounts rolling off into the early part of the quarter, we should watch for any changes in reverse repo volumes. A significant reduction in these injections would suggest a move away from the currently supportive stance. In contrast, increased volumes, especially if combined with stronger-than-expected midpoint fixes in the future, would point to a stronger short-term stabilization effort.

Regarding derivatives execution, there’s a chance to keep things steady, but we must not be complacent. If there are sudden moves outside the expected fix range, especially during larger liquidity drains or increases in short rate premiums, we may need to quickly reassess our risk appetite. The gap between expectations and actual fixings provides a clear measure of risk that needs careful attention.

Finally, today’s net liquidity boost changes the front-end funding curve, making it flatter near the 7-day mark. This slight shift makes very short-dated interest rate swaps more appealing from a carry-neutral perspective. However, any movement beyond two weeks may still carry some uncertainty, especially with broader macro data yet to be released.

The GBP rises to around 1.3620 as the USD weakens from lower safe-haven demand.

The Pound rose against the US Dollar as a proposed ceasefire faced some violations, but risk appetite remained strong. The GBP/USD increased by over 0.65%, despite ongoing geopolitical uncertainties.

Impact of Federal Reserve Decisions

Fed Chair Jerome Powell suggested that rate cuts might be delayed while the central bank looks at the effects of tariffs. He pointed out that higher tariffs could raise prices and impact economic activity, with varying durations of these effects. GBP/USD stayed above the 1.3600 level, hitting heights not seen since early 2022. Traders reacted strongly to this change in sentiment. The easing of military tensions followed a ceasefire announcement by Trump, confirming that Iran and Israel agreed to stop hostilities. However, traders are not overly optimistic. They remain cautious due to past ceasefires in the region that have often failed to last. Despite this, the market still rallied. The news seemed like a welcome short-term relief from broader anxieties. The Pound continued to strengthen against the Dollar, even with reported ceasefire violations. This suggests that investors still prefer higher-yielding or risk-linked assets, a common behavior when geopolitical threats decrease, even if they don’t completely disappear. Powell’s recent comments shifted focus back to monetary policy, although with less clarity. He noted that incoming tariffs could increase prices, making it more difficult for the Federal Reserve to move forward with rate cuts. Normally, this would support the Dollar, but recent shifts in risk preferences have overshadowed that support.Short Term Opportunities and Risks

From our perspective, this creates a brief opportunity for the Pound to gain or at least remain stable amid global uncertainties. Trends in trading volume and options suggest traders are leaning towards an upward bias, possibly preferring reversal strategies at key resistance levels. Powell’s mention of a wide range of potential tariff impact “duration” indicates we may wait longer than expected for a decisive Fed rate move. It’s important to note that traders are not ignoring geopolitical developments; rather, they are adjusting and moving towards assets that are less affected by initial risks. This is clear from the strong rise of GBP/USD, while safe havens like Gold or the Yen have cooled down. Recent analysis of derivatives markets shows an increasing preference for call options on GBP/USD, indicating that many believe momentum can continue if no new disruptions occur. If the ceasefire holds and central banks remain uncertain about timing their policy moves, the Pound could continue to gain. The next important phase depends on how smoothly these geopolitical influences fade from the market and whether upcoming discussions about uranium enrichment lead to new volatility. In terms of trading strategies, short-dated gamma trades seem to be losing appeal. Instead, traders are shifting towards longer-term positions that allow for more recovery time if volatility returns. We are noticing a trend towards longer positions in risk-reward structures. While this comes with its own risks, it also suggests a belief that any pullbacks could be minor unless new shocks arise. Create your live VT Markets account and start trading now.Schmid believes the FOMC can assess the inflation impact of tariffs before making rate decisions.

Jeff Schmid is the president and CEO of the Federal Reserve Bank of Kansas City. He notes that jobs and inflation are nearly where the Federal Reserve wants them to be.

The central bank has time to explore how tariffs might impact inflation before making decisions about changing interest rates. The strength of the economy allows the Fed to take a cautious wait-and-see approach on possible rate cuts.

Concerns Over Tariffs

There are worries from various contacts that tariffs could raise prices and slow down economic activity. This situation needs close monitoring to assess its overall effect on the economy. Schmid’s comments indicate that the central bank is taking a careful approach. There is no strong pressure to change monetary policy right now. Inflation seems to be stabilizing near target levels, and employment numbers look healthy. Without urgent issues in these areas, there’s room to evaluate how extra costs from trade restrictions might affect households and businesses. Taking a wait-and-see position is important. It means that an immediate change in interest rates is not expected, which reduces volatility in interest-sensitive investments. For those watching the interplay between policy signals and pricing, this situation provides a bit more stability for making decisions—at least for the moment.Implications of Rising Costs

It’s crucial to pay attention to the effects of rising costs at the border. Schmid’s contacts warn of price increases and slower production. These are significant concerns. If input costs go up and businesses pass these costs along, sectors like consumer goods and manufacturing could face pressure on their profit margins. If this starts to influence future earnings estimates, some market reactions could be different from what we’ve seen in recent weeks. We must remember that policymakers still have some flexibility. The effects of trade changes won’t be the same for everyone—it depends on whether businesses absorb the costs, pass them on to consumers, or adjust with currency changes. In the short term, we may not see a surge in options volume unless strong data changes the discussion. However, forward curves related to inflation expectations might already have built in additional costs, especially at the longer end. Those involved in rate-linked products should think about whether these added costs are justified by actual trends or simply a reaction to uncertainty. Keep an eye on price data over the next few weeks. Look at these figures in connection with consumption patterns and job market trends. If core measures, which usually exclude volatile food and energy costs, start to rise, it could change the momentum quickly. But as long as the numbers stay near target levels and hiring remains stable, the current approach is likely to continue. In the end, when leaders indicate they’re not in a hurry to act, they’re suggesting that risks of decline still outweigh concerns about excessive growth. This signals valuable insights—especially for planning for the latter part of the year. Expectations may have surged ahead of actual economic conditions. It’s wise to consider scenarios where no changes happen in the fall. Stay adaptable, but avoid getting distracted by noise. The opportunity to react is there—use it wisely instead of guessing what might happen next. Create your live VT Markets account and start trading now.NZD/USD pair climbs to 0.6035 as new buyers enter around 0.6000 level

The NZD/USD pair is currently trading near its weekly high at about 0.6035, thanks to a weaker US Dollar. This follows a three-day rebound from a recent one-month low, as investors expect the Federal Reserve to lower borrowing costs.

The USD Index is close to a one-week low, despite Fed Chair Powell’s aggressive remarks. Optimism around a ceasefire between Israel and Iran, along with a positive market atmosphere, is reducing the Greenback’s appeal as a safe haven, benefiting the Kiwi currency.

New Zealand Trade Data

New Zealand’s trade data exceeded expectations, supporting the NZD/USD pair. The monthly trade surplus was NZ$1.235 billion, while the annual deficit was NZ$3.79 billion in May. Expectations for further rate cuts by the Reserve Bank of New Zealand could limit significant gains for the NZD. The repeated difficulties near the 0.6065-0.6070 resistance levels make traders cautious, as they wait for a clear breakout above this barrier. The Kiwi’s value is influenced by the state of New Zealand’s economy, central bank policies, and China’s economic performance. Changes in dairy prices, New Zealand’s main export, also impact the currency’s value. The Reserve Bank aims for medium-term inflation between 1% and 3%, which affects the NZD/USD relationship. Looking at the recent price movement of the NZD/USD pair, the current rise around 0.6035 is mainly due to a softer US Dollar rather than strong Kiwi performance. This shift reflects changing expectations about the Federal Reserve’s future borrowing costs. Even though Powell kept a hawkish tone, markets are sensing some potential for rate relief in the medium term. This difference has led the USD Index to drop to a one-week low. Safe-haven demand is also waning as geopolitical concerns, especially in the Middle East, ease. A temporary ceasefire reduces the Greenback’s appeal, shifting interest toward risk-sensitive currencies like the NZD.Technical Dynamics and Market Sentiment

Domestically, New Zealand’s trade balance data exceeded forecasts with a monthly surplus of NZ$1.235 billion. While the annual trade gap is more cautious, this immediate boost in exports is significant for those monitoring the Kiwi. A positive trade performance helps strengthen the NZD, particularly when China—an important trading partner—maintains stable demand. However, challenges remain. The Reserve Bank of New Zealand is navigating ongoing price pressures and declining domestic demand. Market discussions are trending toward more dovish policies in the upcoming months, which could limit substantial upward momentum for the NZD. Technically, the 0.6065 to 0.6070 zone has proven to be a strong resistance level. The price has struggled here multiple times, indicating uncertainty that keeps short-term excitement in check. Until we see a clear break above downward trends or former resistance levels, optimism will be cautious at best. The currency is influenced by several factors. Commodity prices, especially dairy (New Zealand’s main export), are critical drivers. Changes in global milk powder auctions affect exchange rates, so monitoring upcoming GDT releases is essential. Additionally, domestic inflation targeting within the 1% to 3% range guides RBNZ policy, and any fluctuations will impact interest rate futures and the NZD. Traders need to stay flexible. Support for the pair is near the 0.6000 mark, and falling below this level could lead to a broader drop towards early-June levels. Volatility will likely stem from various sources: US economic data, market sentiment shifts, and changes in expectations regarding China’s growth. Ultimately, patience is key, and traders should balance short-term price signals with broader, slower-moving macro factors. Create your live VT Markets account and start trading now.US and Israeli strikes reportedly delay Iran’s nuclear program by two years amid concerns of rebuilding

The early US intelligence assessment indicates that recent strikes on Iran didn’t cause major damage to the country’s nuclear sites. However, Israeli officials believe that the combined military actions of the US and Israel have delayed Iran’s nuclear program by two years.

Israel argues that Iran’s program was already delayed by two years before the US operation. However, Israeli officials are determined to stop Iran from easily rebuilding its nuclear capabilities.

The situation remains tense and could lead to conflicts unless there is a change in the Iranian leadership, which is often left out of discussions. It seems Israel will keep watch and may try to disrupt Iran’s nuclear activities.

This scenario blends intelligence with military strategy amid ongoing tension between long-time rivals. Initial American intelligence suggests little physical damage to Iran’s nuclear infrastructure, which may seem to lessen the impact of the strikes. Nonetheless, this does not capture the broader goals of their joint mission.

From Tel Aviv’s viewpoint, Iran’s timeline for nuclear development has already been extended by two years, a conclusion reached even before the latest strikes. This implies that Israeli officials see the recent attacks not as a start but as a continuation of efforts to maintain that delay and prevent any swift rebuilding. Their strategy is an ongoing campaign rather than a single action.

Netanyahu and his defense team show readiness to act consistently instead of just reacting in urgency. Their aim goes beyond halting progress; they want to create regular disruptions. It’s no longer about one-off attacks. They’ve established a pattern to keep up pressure, even if growth seems to be stalled. This strategy depends heavily on surveillance and timely action as much as it does on airstrikes and sabotage.

The underlying theme requires constant vigilance. Acceleration in Iran’s nuclear activities could happen quietly, without any headlines, and Israel cannot afford to give them any space. Their goal is to restrict not just figuratively but literally the ability to enrich uranium or develop missile sites. Air bases, logistics, and enrichment facilities are all targets under this strategy.

Raisi’s silence on the issue has been noteworthy, and what he doesn’t say is significant. In military and political circles, this silence suggests a lack of confidence or perhaps indicates that Iran is still assessing the damage, which could signify hesitation in their response. When public statements are absent, covert adjustments are likely taking place.

For those interested in future developments, the risk premiums related to geopolitical tension aren’t merely speculative; they’re based on actual state actions and efforts to limit the growth of adversarial capabilities. This creates temporary imbalances in anticipated market volatility, leading to sudden shifts not grounded in material change. High volatility related to Gulf assets may not be limited to oil prices alone.

In summary, we need to consider factors beyond just visible weaponry or public statements. Timelines, hesitations, and strategic targeting create a pattern that demands responsive actions rather than mere predictions. Short-term options are more appealing not just because of macro changes, but due to the nature of immediate retaliation and sudden changes in tactics.

We should also examine trailing indicators—like logistics delays, power fluctuations near known development sites, and shifts in air defense systems. These are all part of a broader strategy. Calculated patience doesn’t equate to inaction.

As traders, it’s crucial to understand how responsive measures can turn into proactive disruptions. Those with advanced intelligence can act before news breaks. Movements in regional currencies, defense stocks, and shipping indexes might serve as an early warning system. Given the events of the past month, we should be preparing for ongoing pressure in various forms rather than waiting for a climactic moment.

GBP/USD remains on an upward trend above 1.3600, recently hitting 1.3648, its highest level since February 2022.

The GBP/USD is rising as the US Dollar weakens because of reduced demand for safe-haven assets following a ceasefire between Israel and Iran. Comments from Fed Chair Powell indicate that rate cuts may be delayed until the fourth quarter. Meanwhile, the British Pound (GBP) could face challenges due to the Bank of England’s (BoE) dovish policies.

The GBP/USD pair has increased for three sessions in a row, trading near 1.3620 during the Asian trading hours on Wednesday. It is close to a peak of 1.3648, the highest level since February 2022. Improved risk sentiment after tensions in the Middle East eased is boosting the GBP/USD.

Ceasefire’s Impact on Forex Markets

US President Trump announced a ceasefire between Iran and Israel, creating hope for an end to their 12-day conflict. However, uncertainties about the ceasefire’s durability remain, especially regarding potential nuclear talks and the status of Iran’s enriched uranium. In his testimony, Fed Chair Powell suggested that rate cuts should be delayed until later this year. Kansas City Fed President Schmid advocates for waiting to see the economic effects of tariffs. The dovish comments from BoE officials could affect the GBP, as BoE Governor Bailey has expressed concerns over the reliability of labor data. The Pound Sterling is the UK’s official currency and plays a vital role in global foreign exchange trading. The BoE’s monetary policy, especially through interest rate changes, significantly influences its value, particularly in managing inflation. Economic indicators like GDP, PMI, and trade balances also affect the strength of Sterling. The GBP/USD pair has sustained its upward movement and is nearing levels not seen since early 2022. This rally coincides with improved global risk appetite, shifting flows away from safe-haven currencies like the US dollar. The fragile ceasefire in the Middle East serves as temporary relief for global markets, giving the Sterling more space to rise.Monetary Policies and Market Reactions

While US officials claim that military tensions have eased, there is still low confidence in the ceasefire’s stability. As we watch for the potential restart of nuclear negotiations and their implications, any setback could reverse the current favorable mood and bring demand back to the dollar. Until then, lighter trading volumes are likely to favor risk-oriented currency pairs. On the monetary policy front, Powell’s comments emphasized patience. He noted that inflation remains stubborn and the US job market has been stronger for longer than expected. His remarks suggest that interest rate cuts are unlikely in the near term, pushing expectations for the first cut potentially toward late 2024. Schmid supported this view by noting that new tariffs could change growth and inflation dynamics in ways that will take time to reflect in the data. This indicates a reluctance to make premature cuts to monetary policy. In contrast, the Bank of England has a different outlook. Bailey’s concerns about the inconsistencies in labor market data raise worries about ongoing wage pressures. Without clear employment trends, policymakers may feel limited. If revisions show weaker job growth, it could point toward earlier rate cuts in the UK. Recent communications from BoE officials have leaned toward caution, reflecting discomfort with maintaining tight policies amid uncertainties about economic slack. In the coming weeks, we will closely monitor the UK’s GDP figures and upcoming PMI surveys. Any signs of weakness may reinforce dovish expectations and limit the Pound’s gains, even if the dollar remains weak. In the US, inflation data and employment reports will be scrutinized for signs of slowing, which could lead markets to adjust their timelines for Fed easing. Markets are currently testing assumptions around central bank reactions daily. We expect increased sensitivity to speeches and unexpected data. The widening gap between Fed and BoE rate trajectories could lead to more volatility, especially if geopolitical risks resurface. For instance, Victoria at the BoE earlier stressed the importance of looking past one-off price shocks, showing their tendency to under-react. This stance contrasts with US officials, who are currently less flexible. From a trading perspective, market positioning appears skewed toward expectations of slower US rate cuts, but this could change rapidly. For now, the Pound remains strong, but this depends on ongoing optimism that attracts capital to risk trades. With market pricing potentially shifting quickly due to unexpected data, we should be prepared for changes. Create your live VT Markets account and start trading now.Members voice concerns about tariffs, wages, inflation, and economic stagnation at recent meeting

During the June meeting, participants shared different views on Japan’s economic situation, especially regarding the impact of U.S. tariffs. Concerns were raised about how these tariffs could affect business confidence and the overall economy. Despite these worries, many companies are likely to continue tackling labor shortages and making investments.

The Japanese economy is at a critical point, balancing between growth fueled by wages and investments or falling into stagflation. Alongside tariff worries, there are also concerns about domestic wage growth and a slightly higher-than-expected consumer price index (CPI). Rice prices have emerged as a significant factor influencing inflation expectations.

Global Economic Policies

Global economic policies and their effects on Japan were discussed, highlighting potential inflationary pressures. Several members emphasized the need to keep current interest rates and financial conditions stable due to ongoing uncertainties from global geopolitical issues. They noted the risk of unintended market effects from international events and rising bond market volatility. Even with inflation higher than expected, some members supported maintaining current policies due to these uncertainties. Meanwhile, the USD/JPY exchange rate remains stable. Recent discussions have clearly shown opposing forces at play domestically. On one side, businesses display a moderate resilience, particularly those focused on investment and keeping labor amid structural shortages, despite external shocks. This ongoing commitment indicates a long-term confidence in internal growth. However, these positive actions must also deal with external risks that are not temporary or minor. The stability of the dollar-to-yen exchange rate may seem reassuring, but it should not lead to complacency. It reflects investor expectations that policy changes are unlikely to happen abruptly without significant data shifts. If bond markets become more sensitive—experiencing increased volatility from abroad—the assumption of stable rates could be challenged. Any sharp reactions in rates could impact leveraged positions, especially those linked to long-term instruments, as yield predictions influence margin behaviors. Interestingly, rice prices, less discussed in Western markets, are rising enough to shape public inflation expectations, affecting future pricing behaviors. If not addressed through policy discussions or economic developments, these effects could build up, prompting yield changes in instruments that track household consumption. The latest Consumer Price Index figures support this notion, slightly ahead of consensus predictions, suggesting even well-prepared portfolios may need adjustments.Corporate Sentiment and Tariff Policies

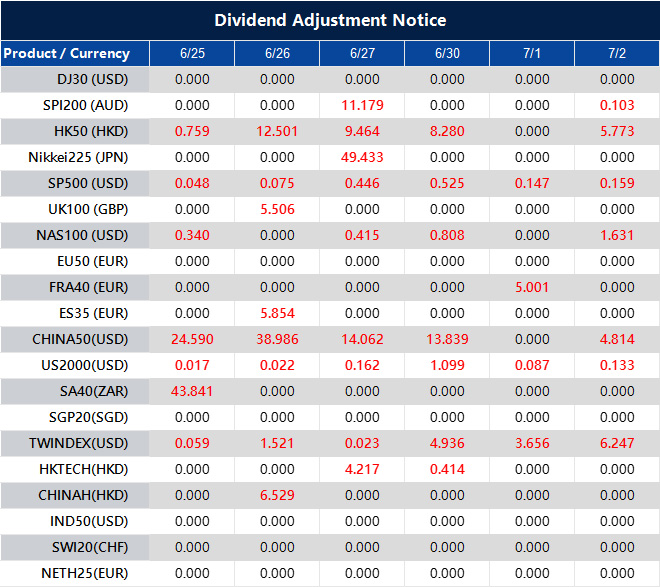

Pressure from foreign tariff policies, particularly those from Washington, is affecting corporate sentiment. While the direct impact might take time, senior management teams are adopting a cautious approach, which could influence hiring and domestic capital expenditures. Any decline in forward business confidence indicators—especially in export-sensitive sectors—should be taken into account regarding implied volatility. Wage growth remains a glimmer of hope. Sustained upward pressure could indicate wage-driven inflation instead of cost-driven inflation, changing how official releases are interpreted in the next three quarters. This could also influence implied rate volatility, especially if policymakers do not take counteractive tightening measures. Some policymakers might prefer to pause rather than act preemptively, waiting for more data before making changes. This caution is understandable given the current uncertainties, but it means there will be a heightened focus on upcoming domestic inflation and global trade data, which may broaden implied curve trades. From our perspective, a near-term shift seems unlikely unless prompted by significant external events. In the meantime, paying attention to subtle changes in yield curvature and slope steepening may prove beneficial as the market adjusts its expectations for forward guidance. Monitoring open interest in bond-related futures and options shows no sudden shifts yet, but increased activity in contracts further out may indicate greater confidence in hedging against rate surprises down the line. Therefore, closely watching how sentiment shifts regarding commodity-linked inflation, currency alignment with rate policies, and relative differences between Japan and its main trading partners could provide clearer entry and exit points. With market pricing very finely balanced, minor disturbances—whether from geopolitical changes or short-term data fluctuations—could lead to temporary but significant disruptions. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 25 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Japan’s services producer price index rises 3.3% annually, exceeding expectations of 3.1%

The Bank of Japan released its Services Producer Price Index (PPI) for May 2025, showing a 3.3% increase compared to last year.

This rise exceeded the expected 3.1% and was higher than last month’s figure of 3.1%. This data offers a glimpse into price changes in Japan’s service sector.

The new Services PPI is higher than both forecasts and the previous month, indicating continued cost pressures in the service industry. This steady 3.3% rise suggests a real trend rather than a mere fluctuation. It shows that businesses are regularly passing increased costs to consumers.

As a result, those watching monetary policy may reconsider how the Bank of Japan operates. The central bank has been cautious, but stronger inflation data—especially from non-traded sectors—might affect how soon rate adjustments happen. Ueda, the head of the BoJ, may face fewer obstacles in signaling restraint or even tightening measures. A change in tone may be on the way as the yen remains weak, leading to higher imported costs.

From a volatility perspective, the services inflation data suggests increased movement in yen interest rates, especially at the short end. Interest may rise for upcoming policy meetings. Those holding short-duration positions may need to reevaluate if current pricing does not reflect a more hawkish stance.

What matters now is the trend, not just the current level. The rise from April confirms that this is a widespread movement, not limited to a few categories. Areas like transport, professional services, and real estate are contributing to the overall index increase. This type of inflation tends to persist and will warrant closer attention.

This trend will likely impact future GDP deflators, supporting expectations for rate hikes. We’ve seen similar patterns in other advanced economies, where services inflation gradually builds before contributing to overall price increases. Short gamma positions on Japanese rates may feel pressure because of this context.

There will also be effects on forward guidance assumptions. Traders dealing in long-dated options will factor in higher implied policy variations—not just this month, but into the third quarter and beyond. If the sector continues to perform well and domestic demand remains strong, this case will only strengthen.

The recent data delivers a clear message: price increases are not limited or temporary. This opens the door for clearer communication from policymakers. Delta hedgers and those using calendar spreads on the JPY curve may find more benefit in using flatter structures, particularly as volatility becomes less directional and more based on mean reversion.

We have adjusted our short-term exposures accordingly. Outside Japan, investors might reassess carry trades involving the yen, as rate differences adjust to stronger domestic factors. This is especially true for leveraged positions in Asia-Pacific cross-currency pairs.

Monitoring the upcoming Tankan and BoJ summaries will now be routine. However, the key question is whether the momentum in services inflation continues into summer. If it does, delta positioning may not be enough—vega exposure could be a more critical factor in profitability in less actively traded markets.