The GBP/USD pair is rising, meeting initial resistance at the nine-day EMA of 1.3501.

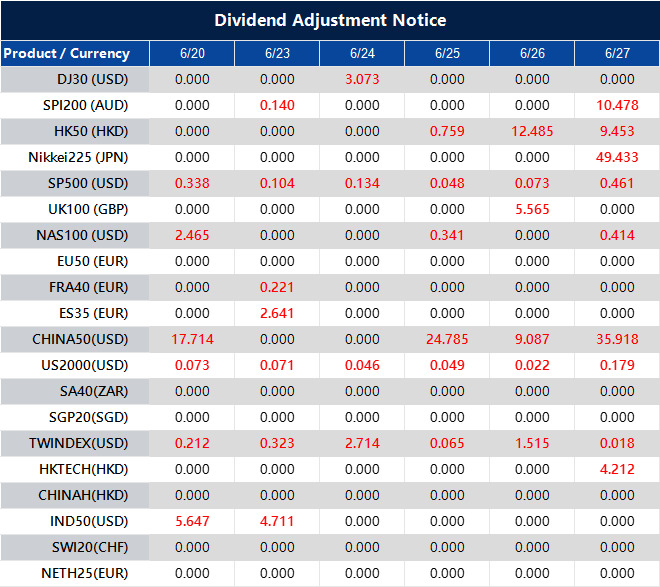

Dividend Adjustment Notice – Jun 20 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Improved short-selling access in South Korea boosts chances for future market classification upgrades

MSCI has announced that South Korea’s short-selling situation has improved, easing concerns ahead of the upcoming market classification review.

Right now, MSCI categorizes South Korea as an emerging market, even though it meets many criteria for developed markets. There is hope that South Korea may soon appear on MSCI’s watch list for a potential upgrade.

In March, South Korea ended a five-year ban on short selling. This decision responded to worries from foreign investors and MSCI. During its annual review, MSCI moved South Korea’s short-selling status from “–” (improvements needed) to “+” (no major issues, improvements possible).

The main takeaway from the report is that the removal of long-standing short-selling restrictions has caught MSCI’s positive attention. Until recently, short selling had been partially banned, which many institutional observers viewed as a barrier to a freer market. This change aims to bring South Korea’s regulations in line with developed market standards and to address pressure from global index providers.

While the upgrade in short-selling metrics doesn’t mean everything is perfect, it indicates that the basic infrastructure and regulations are no longer problematic for international evaluators. The timing of this change before a broader market review increases the chances that Korean stocks could be viewed more favorably in a future index reassessment.

For those analyzing regional indices and their weightings, this shift changes the assumptions we use. The enhanced short-selling conditions suggest that any issues caused by regulatory interference are now less concerning. It also clarifies how market dynamics may function during periods of volatility, which is crucial for leveraged or paired strategies.

When MSCI makes changes like these, they signal to global investors that previous obstacles have lessened. This means that a market that was hard to hedge may soon become more accessible, affecting borrowing costs and the availability of counterparty agreements. This will flow into option pricing models, volatility expectations, and overall risk assessments.

With this reclassification, we can now evaluate Korean derivatives without worrying about artificial limits on downside risks. This will enable more refined execution in strategies such as arbitrage or sector rotation as liquidity conditions improve in the coming weeks. Market players who had previously held back due to these restrictions may start to re-enter the market, leading to more pronounced price movements around corporate earnings or economic reports.

Lee from the Financial Services Commission previously suggested that Korea aims to reform more than just regulations; they want to enhance both appearance and function. Now that this regulatory piece better aligns with what we expect from developed markets, derivatives traders should assess how trading patterns may adjust, especially in the tech and large-cap industrial sectors.

We need to keep a close eye on borrowing rates. If they start to narrow, it will further indicate that price discovery is becoming clearer. This, in turn, will enable better pricing for structured products and volatility exposures, particularly in monthly roll strategies.

Now is the time to recalibrate our exposure metrics for Korean assets across all model portfolios that hold derivatives on regional indices. If the market progresses toward MSCI’s upgrade path, we may see spikes in tracking errors between futures and the spot market as flows adjust to potential index shifts. This could impact both hedged positions and strategies that depend on short-term liquidity.

This is a valuable moment for regulatory clarity, allowing for proactive adjustments rather than waiting for widespread confirmation of changes to the watch list.

In June, consumer confidence in the Netherlands improved slightly, increasing from -37 to -36.

In June, consumer confidence in the Netherlands improved slightly, rising from -37 to -36. This uptick indicates a small boost in how consumers feel about the economy.

The GBP/USD pair is climbing and testing the 1.3500 level during the Asian trading session. This pair shows an upward trend as it continues to move in an ascending channel.

Euro Dollar Movement

The EUR/USD is rising, trading at around 1.1520, supported by a possible pullback in the weakening US Dollar. Unrest related to the Middle East may affect the Dollar’s performance. Gold prices have dropped to a one-week low due to the Federal Reserve’s tough stance, which is outweighing uncertainties in the Middle East. Although risk sentiment is weak, the XAU/USD pair may not see significant losses unless conditions change. In cryptocurrency, major players like Bitcoin, Ethereum, and Ripple are stabilizing. Bitcoin remains above a crucial support level, but if this level is broken, we may see price corrections. Monetary aggregates are still important in the Eurozone, with the European Central Bank (ECB) keeping a close watch. This shows that quantitative theory still matters in shaping monetary policy. With consumer confidence in the Netherlands rising slightly to -36, this indicates a minor improvement in sentiment. While still negative, this increase suggests that Dutch households may feel a bit less pessimistic. However, this alone might not change market strategies significantly. It could, however, lessen the likelihood of more fiscal support or emergency policies from Dutch leaders soon.GBP USD Trading

The GBP/USD pair is moving up and trading near 1.3500 during Asian hours, reflecting strong interest in the British pound. This trend suggests broader weakness in the dollar and a belief that UK interest rates will stay stable. Since the pair is within a defined ascending channel, trend-following traders will likely continue buying unless the price drops below channel support. Keeping an eye on this support level in the coming sessions is crucial, as breaking it could trigger sell-offs among leveraged positions. Meanwhile, the euro-dollar is attracting consistent bids, lingering around 1.1520. This movement corresponds to the dollar’s decline, driven by geopolitical worries about the US’s role in the Middle East. Increased tensions have weakened the dollar’s status as a safe haven recently. Any rise in tensions or aggressive actions could further weaken the dollar. This scenario offers euro holders chances to position themselves above recent resistance levels. Gold’s drop to a one-week low presents a different story. While geopolitical issues usually boost gold prices, the Fed’s firm stance has outweighed this boosting effect. Strong comments about economic strength and inflation have pushed gold prices down. Still, the current context suggests potential sideways movement unless the Fed changes its tone or international tensions escalate. We are watching inflation expectations closely; if they remain stable, gold’s potential for a price increase may be limited. In the cryptocurrency market, major cryptocurrencies are not showing strong trends. Bitcoin is stabilizing above key support levels, which have held firm during previous declines. If these support levels break with strong volume, prices could become volatile. Currently, the lack of trading activity indicates no significant speculative pressure, but investment in altcoins has decreased significantly. Without new drivers, the market may remain stagnant as we move into the next quarter. Finally, from a policymaker’s perspective, heightened attention on monetary aggregates highlights the ongoing relevance of traditional tools. The ECB’s focus on these aggregates suggests they aim to align liquidity trends with price movements. With M3 growth low and real interest rates positive, expectations for easing in future quarters are understandable. While market narratives may fluctuate, the ECB’s quantitative analysis of economic signals likely supports the dovish view more than many realize. Create your live VT Markets account and start trading now.People’s Bank of China projects the USD/CNY reference rate at 7.1801

The People’s Bank of China (PBOC) sets the daily value of the yuan using a managed floating exchange rate system. This allows the yuan to change within a range of 2% above or below a central reference rate.

Every morning, the PBOC decides the midpoint for the yuan based on a mix of currencies, mainly the US dollar. This midpoint takes into account things like market supply and demand, economic data, and global currency trends.

Trading Band Overview

The PBOC permits the yuan to move within a 2% trading band from the midpoint each trading day. This band can change based on the economy and policy needs. If the yuan nears this band limit or shows too much volatility, the PBOC may intervene. The central bank can buy or sell yuan in the foreign exchange market to stabilize its value. This ensures adjustments happen gradually and under control. This approach gives the PBOC steady oversight instead of letting the currency float freely, as other central banks might. The midpoint, established daily, guides trading and serves as a reference against speculation and short-term trends. It’s about more than just the number; it also signals sentiment, policy stance, and their view on outside risks. Prices reflect traders’ expectations and their reactions to what the central bank communicates. A subtle shift in the midpoint can signal a change—sometimes small but usually intentional. Recently, we’ve noticed the morning fix bias in one direction while the spot market moved the other way. These discrepancies suggest caution in policy.Impact on Market Dynamics

For those tracking synthetic positions or option structures, we are paying close attention to the difference between market prices and the fixing level. A widening gap can influence carry trades or show stress in short-term risk. We also observe that around key economic announcements, the fixing often tightens to promote stability. When adjusting our expectations for market movements, it’s crucial to understand how carefully set these daily numbers are. Policymakers can subtly influence market activity through the midpoint boundary. This creates execution risk if political or economic events occur sharply in the evening, especially in the US or emerging markets. Overnight changes can affect the implied volatility the following morning. We watch where spot trades open in relation to the fixing. This matters because it influences volatility expectations and daily hedging decisions, especially for those with leveraged products or weekly expirations. The opening signal often leads to volume spikes and activity in dark pools around the midpoint. Moreover, we are seeing changes in how forwards are priced. Short-term tenors have shifted slightly, indicating that policy remains active. This influences rate expectations and derivative pricing. We see opportunities, but the approach has become more direct. Timing entries around the fix and assessing slippage from the midpoint are now vital, more so than simply having a directional bias. Market players should also focus on options skew. The differences in call and put premiums provide insights into pressure areas. When intervention risk rises, we often see a decrease in put demand, especially if the market feels supported from above. If spot pressures clear quickly and the midpoint adjusts, expectations for future trends can shift dramatically. We continue to view the daily setting not only as a reference point but as a decision being made. It’s not simply a calculation; there’s a level of discretion involved. For those managing delta or gamma exposures, monitoring continues past the morning print—we need to react to trades occurring around that print. As we approach the upcoming weeks, with global forces uncertain and rates active, it’s wise to consider how quickly midpoint adjustments are being made. This helps set limits on how aggressive short-term price movements can be, guiding how we approach directional positions. Create your live VT Markets account and start trading now.Gold prices in Malaysia dropped today due to a decline in value, according to compiled data.

Gold prices in Malaysia dropped on Friday. The price per gram decreased to 459.22 Malaysian Ringgits from 461.51 the day before. The price for a tola also fell to MYR 5,356.28, while a troy ounce was priced at 14,282.97 MYR.

In Malaysia, gold prices are determined by adjusting international rates and converting them into the local currency and units. Prices change daily based on market trends, although local rates may vary slightly.

Central Bank Gold Reserves

Central banks hold most of the world’s gold. In 2022, they bought 1,136 tonnes, worth about $70 billion, making it the largest annual purchase on record. Countries like China, India, and Turkey are rapidly increasing their gold reserves. Gold usually moves in the opposite direction of the US Dollar; when the Dollar weakens, gold prices tend to rise. Prices can change due to geopolitical issues or economic concerns. Generally, lower interest rates boost gold prices, while a strong Dollar can keep them in check. Recently, we saw a slight dip in Malaysian gold prices. The value per gram fell to 459.22 MYR, down over 2 Ringgits from the last session. Prices for tola and troy ounce formats also showed similar declines. This isn’t an isolated drop; it’s a local adjustment reflecting changes in global prices, currency conversions, and rounding in domestic rates. This suggests that local gold prices are closely following global trends rather than setting their own path. These trends become particularly important during times of macroeconomic uncertainty. The key issue is global reserves. Central banks from countries like China, India, and Turkey aren’t just making small adjustments—they’re significantly increasing their gold holdings. Last year, they acquired over 1,100 tonnes. This represents billions in USD at current prices. When central banks adjust their reserves, it’s usually a long-term strategy that aims to protect against currency fluctuations or support economic confidence during tight financial conditions.Gold And The US Dollar

Gold and the US Dollar have a long-standing inverse relationship. When the Dollar weakens, gold prices often rise. However, it’s important not to oversimplify this relationship. If the Dollar remains strong, it can limit gold’s upward movement. Additionally, in times of increased risk appetite, investors may shift funds from safe havens like gold to stocks or other higher-yield investments. Geopolitical or economic fears can also impact gold prices, sometimes in ways not directly related to inflation or interest rates. Price spikes can occur due to market sentiment rather than hard data, especially during times of conflict or when major economic policies change. Currently, we should pay attention to interest rate expectations from the Fed. Lower interest rates can support gold prices since it reduces the opportunity cost of holding non-earning assets. However, if inflation remains stable or increases in the US or Western Europe, the Dollar can still strengthen, which would put pressure on gold prices even if rates are lower. For those trading metals like gold, it’s essential to monitor central bank announcements, inflation data, and changes in emerging market policies. These factors can significantly influence market direction. Often, markets misprice future probabilities, leading to unexpected changes in futures contracts when guidance shifts or data surprises. As we look ahead, flexibility in hedging strategies is crucial. Relying solely on interest rate predictions for gold trading is no longer effective. It’s important to consider the relative strength of the Dollar, the pace of reserve buying, and current political statements. We must acknowledge that gold is highly sensitive—not just to central bank actions but also to traders’ perceptions about timing. Create your live VT Markets account and start trading now.Upcoming events: BOJ’s May meeting minutes and Governor Ueda’s speech

The Bank of Japan’s minutes from their May meeting will be available at 2350 GMT (1950 US Eastern time). A preview is already available based on the Summary of Opinions from the Monetary Policy Meeting held on April 30 and May 1, 2025.

Bank of Japan Governor Kazuo Ueda will address the Annual Trust Association Meeting, though the exact time of his speech is not yet confirmed.

In May 2025, Japan’s Consumer Price Index (CPI) stayed above the Bank of Japan’s target rate, continuing the central bank’s ongoing evaluations.

The summary from the late-April and early-May meetings gives some hints about the tone of the full minutes. These excerpts indicate a persistent inflation above the desired target. Although the central bank has made only gradual changes so far, there’s a growing belief that monetary support might need to decrease sooner than expected.

Governor Ueda’s upcoming speech may echo these concerns, especially given the steady CPI readings. Since inflation isn’t decreasing, it suggests that policies could become stricter, either soon or in the coming quarters. There’s also worry about waiting too long to make changes. Traders should pay close attention to Ueda’s words, as they often reveal more than official statements.

For short-term traders focusing on interest rate products and volatility linked to JPY-denominated assets, the focus should shift to the yield curve’s predictions for potential changes, not just the policy rate. There’s clear evidence of internal disagreements within the central bank. Some members are more vocal about ongoing inflation and currency weakness pushing prices up. This could lead to increased volatility following each new CPI report or economic forecast.

We should monitor the implied volatility in options for Japanese government bonds, especially as it might increase around key announcements from the monetary authorities. Even if no rate change happens at the next meeting, clearer forward guidance could lead swap markets to widen expectations, affecting cash bond yields and forward contracts. Traders should consider two key questions: what happens if the yen weakens further? What actions would lead to a sharper domestic tightening?

These signals are increasingly relevant now. The output gap has narrowed, labor markets are tight, and higher import costs are being passed on to consumers. Conditions that would not have prompted policy changes a year ago are now different. Members like Nakagawa are voicing concerns that inflation may not just be temporary, especially as energy costs continue to rise.

As a result, carry trades involving Japanese government bonds (JGBs) may now be priced too optimistically. Our models indicate a slight increase in market-based inflation expectations. While not alarming, this suggests a need to rethink any short-term holdings relying on long-term dovish policies. Upcoming option expirations should be evaluated accordingly, especially where gamma exposure is sensitive to sudden changes.

Overall, there’s a trend: comments from the monetary board are becoming less patient. While not overtly hawkish, they are not neutral either. Japan’s usually flat interest rate structure may soon begin to rise again if policy changes accelerate. Repricing will be inconsistent, but for those in swaps, futures, or leveraged bond ETFs, timing the sentiment shift could be more crucial than just predicting direction.

We believe that hedging strategies will need quick adjustments in the next few weeks. Keep an eye on changes not only in headline CPI but also in core readings that exclude fresh food and energy. These core figures will increasingly influence policy decisions from the board’s key members. A careful analysis of the next minutes will be crucial to understanding when—and not if—the next policy change will occur.

Silver’s decline continues as it falls below $36.00 for three consecutive days

Silver has seen strong selling pressure for three days in a row, bringing prices down to around $35.65, a level not seen in over a week during the Asian trading session. This decline follows a drop from a high not reached since February 2012.

From a technical standpoint, silver’s drop below $37.00 and the 23.6% Fibonacci retracement level suggests a bearish trend. The oscillators on the 4-hour chart show negative momentum, indicating the possibility of further declines. If the price breaks decisively below the mid-$35.00 range or the 100-period simple moving average (SMA) on the 4-hour chart, we could see deeper losses.

If the downward trend continues, silver might reach the 38.2% Fibonacci level around $35.15, potentially moving down to the psychological level of $35.00. Additional support is found at $34.75, with a further drop to the 50% retracement level at $34.45 signaling more downturn.

If silver attempts to recover above $36.00, it may face resistance in the $36.40 to $36.50 range. A sustained breakthrough could shift momentum towards bullish traders, targeting $37.00 and higher.

Silver’s price is affected by geopolitical tensions and the behavior of the US Dollar, with changes in industrial demand also influencing costs. The market’s reaction to technical levels and external factors will shape silver’s future direction.

Currently, silver’s prices are hovering at the lower end of their recent range, with ongoing pressure felt over several sessions. The drop from multi-year highs has gained attention and has broken through both technical and psychological support levels, such as the 23.6% Fibonacci retracement. This pattern suggests that a reversal is not likely yet; instead, the trend seems to continue downward.

On the charts, momentum oscillators on shorter timeframes like the 4-hour show a clear bearish trend. Since falling below $37.00, bears have regained control, evidenced by a downward bias in price action and a lack of support from demand. The recent movement below the 100-period simple moving average suggests trouble ahead; this average often serves as a key reference for mid-range traders. Remaining below this level opens the possibility of testing the $35.15 mark, and potentially lower levels at $34.75 or $34.45 if selling pressure persists.

These levels are not picked randomly; they align with key retracement zones from previous rallies where price has often paused or reversed. If we revisit these levels, it would indicate more than just daily fluctuations; it would suggest a change in market sentiment that has been riding high since early May.

We’re also closely watching the $36.00 level. This price point has repeatedly indicated whether stabilization attempts gain traction or fail quickly. A bounce above may only be short-covering unless the price convincingly holds above $36.50. Short-term traders may see a recovery opportunity, but without consistent buying support, we should approach any rebounds cautiously. A significant shift toward the upside cannot be expected until $37.00 is breached with volume and follow-through.

It’s important to remember that silver doesn’t trade in isolation. As an industrial material and a quasi-monetary asset, it reacts in complex ways. Currently, external factors, especially geopolitical stress and changes in dollar flows, are affecting how charts behave. A stronger US Dollar puts pressure on silver, while cooling tensions can reduce safe-haven demand. Traders need to consider these external macro cues alongside technical indicators that may signal changes.

As market positions adjust, we are monitoring how support and resistance levels hold up. The inability of silver to maintain February 2012 levels is significant; it shows potential overextension rather than underlying strength. Unless the broader context changes, we anticipate further tests of support, especially as sellers remain active for now.

Growing concerns about the Israel-Iran conflict weaken USD/CHF, leading to a shift towards the Swiss Franc

The USD/CHF pair fell to about 1.3690 during Friday’s Asian trading session. Concerns about the US getting involved in the Middle East conflict have strengthened the Swiss Franc, leading to this drop after a three-day increase. The conflict has now lasted for seven days, and uncertainty rises with potential US involvement in the Israel-Iran war.

Recently, the Swiss National Bank (SNB) lowered its interest rate by 25 basis points to zero, hinting that negative rates could return in the future. Consequently, the Swiss Franc has gained strength against the US dollar. In contrast, the US Federal Reserve kept its key borrowing rate steady but indicated possible rate easing due to trade tensions.

Importance Of The Swiss Franc

The Swiss Franc is valued as a safe haven currency, thanks to Switzerland’s stable economy and neutral politics. The SNB’s decisions greatly influence the Franc’s value, with interest rates playing a vital role. Economic data from Switzerland, its relationship with the Eurozone, and global market sentiment are crucial in determining the currency’s strength. The Swiss Franc often moves similarly to the Euro due to close economic ties with the Eurozone. This situation represents a significant shift in foreign exchange sentiment, largely influenced by external factors rather than domestic ones. The drop in the USD/CHF pair to around 1.3690 is a response to rising geopolitical risks. The prospect of increased US involvement in conflicts involving Iran and Israel has unsettled markets, prompting investors to seek stability in safer assets like the Franc. This sudden shift explains the upward move in the Franc. The SNB, led by Jordan’s team, surprised the market with a 25 basis point cut to zero. While some easing was expected, the sharpness of this decision and its communication indicated the SNB’s readiness to accept or even encourage further strength in the Franc, if it supports overall monetary conditions. This is significant as inflation remains manageable, allowing the bank to act without risking rapid price growth. However, it raises concerns about potentially returning to negative rates, signaling that demand for safe havens is the main driver currently, rather than interest rate differences. On the other hand, Powell and his colleagues have maintained a more static stance. Although they kept rates steady, they hinted at possible easing in the future to balance trade pressures from tariffs and retaliation. This cautious approach suggests that the Fed sees global risks rising and prefers to keep options open.Risk Sentiment And The USD/CHF Pair

For traders focused on interest rate differences, conditions have become less favorable. With the SNB taking more decisive action and the Fed being more cautious, we may need to accept that interest rate divergence may not be the primary driver for this pair in the short term. Instead, we should closely monitor global developments, especially those outside economic factors. The Swiss Franc has shown that it can gain strength without policy support. Investors look for reliability when narratives become unstable, which has been a hallmark of the Franc for decades. Its connection to the Euro adds complexity due to its ties with Germany and France, although the Franc tends to act independently under fear. Even with a relatively dovish SNB stance, the Franc can appreciate when demand for safe havens rises. Currently, the currency pair’s movement may depend more on the strength or weakness of the USD than on domestic factors. Economic indicators like real rates and CPI may become less significant if geopolitical risks continue. From our standpoint, short-term strategies should focus on response rather than prediction. Risk sentiment is more important than policy biases. The technical level around 1.3700 has already been tested. If it holds, counter-trend movements may be limited. However, if geopolitical tensions escalate, further CHF appreciation is possible, regardless of the SNB’s intentions. Keep an eye on event risks, especially those beyond economic calendars. Structured derivative positions should reduce reliance on interest rate predictions alone. Create your live VT Markets account and start trading now.TD Securities says the Bank of England’s decision offers little hope for the pound

The Bank of England decided to keep interest rates steady with a 6-3 vote. This was surprising because many expected a wider 7-2 vote. Three members wanted to lower rates by 25 basis points, showing a difference in opinions within the committee.

Analysts believe the Bank’s decision probably won’t greatly affect the pound. Instead, larger global issues, like geopolitical tensions, are playing a more significant role in currency values.

One major concern is the potential for the U.S. to take military action against Iran. This could cause the dollar to move more than the Bank of England’s decision affects the pound.

The Bank is trying to balance its internal situation with external pressures. With a closer-than-expected vote to hold rates steady and some members pushing for a cut, it’s clear that opinions on easing differ within the committee. The fact that more members support a cut introduces uncertainty about future meetings.

Market expectations were leaning towards a smoother consensus to maintain rates without such disagreements. Now, with this surprising vote, attention shifts to the implications for the future—market participants will be looking for signals before the next meeting.

Currently, the situation seems to be changing. The recent calls for rate cuts can’t be ignored as just symbolic. These calls often start as outliers and build momentum over time. The upcoming inflation and growth data in the next few weeks will be crucial. If the data is weaker than expected, the majority might lean towards easing.

However, the currency markets showed little reaction to the decision. This was not surprising, as the decision to hold rates did not distract from larger global pressures. Ongoing unrest in the Middle East and concerns about U.S. military involvement have drawn market attention to safe-haven assets and energy prices instead.

We are in a situation where larger events are overshadowing short-term monetary decisions. Even a bold move by policymakers might not shift broader expectations. The pound’s stability after the decision suggests this. The limited effect of the vote on implied volatility for sterling shows that investors are being cautious and not reacting strongly to domestic news.

Given this context, the upcoming days will require careful planning. When domestic data comes in, especially labor market figures and services PMIs, we should analyze not just the main figures but also if they support those advocating for easing. If the numbers disappoint or if past data is revised downward, more members may join the call for cuts.

As we prepare for this data, monitoring implied rate paths and short-duration swaps will be increasingly helpful. These indicators will reflect any repositioning before it affects overall yields. We are already seeing a slight reduction in expectations for interest rate hikes this summer, which may change quickly.

In this environment, the focus shifts from each piece of news to how quickly the data aligns with those calling for earlier action. Whatever opportunities arise each day, being adaptable between data releases will help respond to the evolving messages from decision-makers.