Japan’s PMI shows signs of recovery, but businesses stay cautious due to fragile demand and uncertainty

Japan’s private sector showed more signs of recovery in June. The flash composite PMI rose to 51.4 from 50.2 in May, thanks to stronger services and a small increase in manufacturing output.

However, demand conditions still appeared weak. New business growth remained modest, impacted by lower overseas demand due to U.S. tariffs and global trade uncertainties affecting exports.

Companies are cautious about the future, with sentiment close to post-pandemic lows. On the bright side, input cost inflation fell to its lowest in 15 months, and employment grew at its fastest rate in nearly a year.

The June figures reveal some resilience. Although the change in the composite PMI from 50.2 to 51.4 may seem small, it’s significant given the last 18 months. The improvement stems from stronger services and a rebound in manufacturing output—two sectors that had been opposing each other recently.

Still, while output levels increased, overall demand hasn’t surged. New business growth has been slow, indicating that customers—both domestic and international—remain uncertain. Exports are particularly struggling. International challenges like higher import taxes and unclear global trading rules are suppressing foreign orders. This hesitation has a ripple effect on broader industrial planning.

Expectations for the future haven’t returned to pre-2020 levels either. Business optimism is low, and there’s a sense of hesitation. Companies, whether small or large, are thinking carefully before making new investments or expansions.

However, some indicators show improvement. Input cost inflation has softened, which provides relief, especially for sectors that depend on imported energy or raw materials. This allows companies to stabilize their pricing without immediately passing higher costs onto customers. Job creation also increased, marking its fastest growth in almost a year, suggesting some confidence that orders will remain steady.

What’s important is that the data shows mixed signals. There’s neither a significant advance nor a dramatic decline. The uneven improvement is what matters most.

Given the increase in output but lingering demand concerns, we may be seeing a base forming under activity. However, it’s also fair to believe that there won’t be much room for growth, especially with global trade risks and sentiment stuck in narrow ranges. This provides a framework for considering potential short-term shifts.

The growth in employment reduces fears of sudden drops, but it also means that earnings and consumption expectations could improve slightly. A decrease in cost pressures might lead to lower inflation over time, influencing interest rate expectations. This could help stabilize the yen, particularly if Tokyo’s policies diverge from those of other major economies.

In terms of positioning, it makes sense to have moderate exposure to output-sensitive sectors, while hedging against potential downturns in demand. We should be cautious and not assume that early output growth confirms a broader trend. The inconsistencies across sectors, especially in exports, indicate that everything isn’t moving together just yet.

It’s also crucial to keep in mind last year’s weaker data, which raises the bar for interpreting month-to-month changes. A modest PMI increase like the recent one might seem more significant on paper than it feels to those managing supplies.

There’s potential for short-term trades if inflation expectations align with the slow trend in input costs. If the strength in employment leads to a slight increase in domestic consumption, that could tighten yield gaps even more. Strategic calendar spreads might capitalize on mismatched expectations of central bank reactions.

However, it’s not yet the time to dive into high-risk investments with strong confidence. The softness in new orders and ongoing uncertainty around foreign demand still loom large, suggesting that strategies should be focused on flexibility rather than long-term commitment.

Silver price exceeds $36.00 due to risk aversion and increased tensions in the Middle East

Silver prices have risen to about $36.10 early Monday during Asian trading. This increase follows the U.S. attacks on Iran’s nuclear sites, which have raised tensions in the Middle East.

Iran’s promise to respond has made the markets nervous. If things escalate, demand for safe-haven assets like silver could rise. U.S. President Trump has warned that any retaliation from Iran will lead to a stronger response.

Fed’s Potential Influence

Officials from the U.S. Federal Reserve, including Governor Waller, have suggested possible interest rate cuts as early as July. This outlook has supported silver prices because lower rates can make the metal cheaper for foreign buyers. However, the renewed strength of the U.S. Dollar might limit how much silver prices can grow. Investors are looking forward to the preliminary U.S. S&P Global PMI for June. Strong data from the U.S. could strengthen the Dollar in the near future. Silver is used in many industries due to its excellent electrical conductivity. Changes in industrial demand can affect its price, as silver is widely used in electronics, solar energy, and is also tied to gold. Silver prices often follow gold’s movements, influenced by similar factors like economic stability and geopolitical issues. The recent surge in silver prices to around $36.10 reflects two key issues: geopolitical unrest and changes in monetary policy. With attacks on critical sites in Iran and warnings from Tehran, safe-haven assets are absorbing the market’s shock. Silver benefits from increased political risk, as it serves both as a store of value and an industrial metal. As seen early Monday, these trends continue, and market anxiety is growing. From Washington, the language has become more cautious. President Trump’s strong warnings about retaliation suggest that any further actions could quickly escalate the situation. As a result, market volatility has increased, with silver becoming a popular option for those seeking protection against potential losses. Traders should watch for possible price increases if tensions worsen, especially if reports become more direct or actions in the region resume.Monetary Positioning and Market Dynamics

At the same time, monetary positioning is providing additional support. Governor Waller and others at the Federal Reserve have left the possibility of rate cuts open for July. Lower interest rates increase the appeal of holding metals like silver, which do not earn interest. This environment is slightly favorable for metals due to easing inflation, encouraging more buying. Yet, it’s not all one-way movement. The Dollar has shown some strength, which can limit gains in USD-denominated commodities. If the upcoming S&P Global PMI data is better than expected, the Dollar could rally, putting further upward pressure on silver prices in the short term. This creates a mixed situation where the demand for safe-haven assets is rising, but a stronger Dollar could counteract that. From a strategic viewpoint, silver is sensitive not only to market sentiment but also to changes in manufacturing demand. It is heavily used in electronics, solar panels, and clean energy processes. Any decline in demand in these areas will have an impact on prices. We will also be monitoring gold, as their price movements are often linked and respond similarly to broader economic signals. We will keep an eye on guidance from the Fed at upcoming speaking events and monitor physical silver delivery trends. Stronger flows into ETFs or tighter spreads in dealer markets could suggest capital is shifting toward metals for the medium term. Currently, near-term options skews are low, indicating traders may not be fully prepared for sudden moves. Adjusting risk exposure while markets are sensitive to news could be wise. As events unfold in the Middle East and among central bankers, staying alert to cross-market signals is crucial. While the silver market typically reacts quickly, broader trends often take longer to adjust. Create your live VT Markets account and start trading now.Democratic Republic of Congo extends cobalt export ban, leading to sharp price increases

The Democratic Republic of Congo, the world’s top cobalt producer, has extended its temporary export ban on cobalt for another three months. This ban is now effective until September 2025, following an initial four-month pause that began in February. The extension comes after cobalt prices plummeted to a nine-year low of about $10 per pound.

As a result of this ban, cobalt prices have risen by 35%. The pause in exports is especially impacting companies like Glencore, and has led other regions, including Indonesia, to prepare for possible ongoing restrictions. These changes could alter market shares and affect global supply chains.

Market Supply Shift

The current scenario highlights a significant shift in market supply, driven mainly by policy changes in the Democratic Republic of Congo. With the cobalt export ban extended through the third quarter of next year, we are seeing changes in pricing. Initially, this was a reaction to long-term low prices, but it has evolved into a response that directly affects trading volumes and price volatility. Cobalt futures quickly reacted; the 35% price increase is not just recovery but also a re-evaluation of supply and future risks. Usually, slow physical market restrictions take time to reflect in derivatives, but that’s not happening here. Prolonged disruptions tend to alter assumptions about future pricing, and we are already seeing this recalibration, especially for the second half of 2025. These changes impact not just the current rates—there’s a growing sense of scarcity affecting shorter-term contracts. Market participants will have adjusted how they view the correlations between cobalt and related metals like nickel and lithium. Movements in those metals have been less drastic, suggesting that this reassessment is localized. However, there is potential for wider effects as substitution factors start to influence pricing models. The impact of reduced cobalt supply will also affect contract structures, particularly for instruments used for synthetic exposure by industrial hedgers.Glencore And Indonesia

Looking at Glencore, the pause in Congolese exports has significantly reduced market flow. This creates an opportunity for smaller producers to fill the gap, although they may do so slowly. Since processing is concentrated in just a few areas, especially China, any drop in raw materials leads to delays that impact settled prices. We can no longer just depend on stated production capacity—timing is now more critical than volume. In Indonesia, we’ve noticed mining companies gearing up to increase output, likely in anticipation of future supply needs. If this trend continues, and if exports are made under competitive contracts, the differences in pricing between regions could tighten paper market spreads. Currently, these movements show less correlation, but they suggest a buffer capacity that we didn’t focus on earlier in the year. The tight supply situation should raise awareness about margin requirements, especially for short positions. Strategies that relied on earlier low prices now face risks from both price changes and access costs—financing availability and delivery obligations are now more sensitive to changes in contract pricing. We are increasing our near-term volatility estimates, especially around important inventory data releases and policy updates. Seasonal factors are less impactful now; policy and logistics play a much larger role. Create your live VT Markets account and start trading now.USD/CHF trades near 0.8170 as safe-haven demand increases after earlier gains

USD/CHF has dropped, trading around 0.8170 during Asian hours on Monday. The Swiss Franc gained support as safe-haven demand rose, driven by recent U.S. actions regarding Iran’s nuclear sites.

U.S. President Trump confirmed attacks on Iran’s nuclear facilities in cooperation with Israel. As a result, tensions are likely to increase, with Iran vowing to defend itself.

Switzerland’s trade surplus fell to CHF 2.0 billion in May, down from CHF 5.4 billion in April. This is the smallest surplus since December 2023, and key economic data will be released this week.

In the U.S., Federal Reserve Governor Christopher Waller hinted at possible easing of monetary policy soon. However, Fed Chair Jerome Powell cautioned that this depends on improvements in labor and inflation data.

The Swiss Franc (CHF) is one of the most traded currencies globally. Its value is influenced by market sentiment, economic conditions, and the Swiss National Bank’s actions.

Switzerland’s stable economy and political neutrality make the CHF a favorite safe-haven asset. Its value is also impacted by the economic health of the Eurozone, closely related to the Euro.

The Swiss National Bank reviews its monetary policy quarterly, aiming for inflation of less than 2%. Changes in economic growth or inflation can affect the CHF’s value.

Given recent events, currency traders dealing with the USD/CHF pair should focus less on speculative sentiment and more on real changes in macroeconomic and geopolitical landscapes. The Franc’s early-week gain shows a direct market response to increased military tensions and defensive posturing from Iran. Rising geopolitical stress typically boosts demand for safe-haven currencies, including the CHF, especially during potential military conflicts. Switzerland’s political neutrality reinforces investor interest, leading to a swift influx into the Franc.

The recent reduction in Switzerland’s trade surplus – from CHF 5.4 billion to CHF 2 billion – suggests a quicker-than-expected decline in export contributions. For traders, this is significant beyond just a statistic; it could indicate weakened external demand or higher import costs, slightly weakening the case for long CHF positions. Before this week’s data releases, any disappointing figures may have additional negative effects. Currently, market sentiment is more influenced by external events than by domestic data.

Meanwhile, in the U.S., uncertainty remains. Waller’s suggestion of potential rate cuts has raised expectations of possible monetary easing, but there’s no clear timeline. Traders should be cautious about misinterpreting signals since Powell’s remarks tie any actions to upcoming labor and inflation data. Thus, monetary policy will depend on the outcomes, not a set schedule.

Until there are notable improvements in U.S. employment and clear signs of decreasing inflation, the dollar is unlikely to weaken significantly. Temporary dips will likely result from external shocks, like these recent military strikes, rather than from dovish central bank policies. A full pivot from the Fed is not apparent yet, and traders should avoid jumping to conclusions too soon.

The Swiss National Bank focuses on price stability with a ceiling of 2%. While they review their policies every quarter, they usually react decisively when their goals are threatened. Currently, with inflation within their target and no pressing concerns in GDP growth, there’s little need for a major change in approach. More likely, they will maintain a wait-and-see stance unless rising import costs or Eurozone instability demand intervention.

It’s also important to recognize that the CHF often moves with the EUR due to the close relationship between the two regions. Should Eurozone data decline—whether in manufacturing PMIs or consumer confidence—it could negatively impact Swiss exports and the Franc’s value. We’re monitoring that situation closely for any warning signs.

In terms of market positioning, significant military escalations should not be overlooked. The recent shift in USD/CHF shows how quickly market sentiment can change. However, if U.S. macro data remains strong, fluctuations in dollar strength could mitigate any reaction from geopolitical tensions. These two forces—regional stability and monetary clarity—will create pressures in both directions, requiring traders to be adaptable and strategic in the coming days.

Rising mortgage arrears in Australia linked to high costs and interest rates affecting households

Fitch Ratings has noticed a significant rise in mortgage arrears in Australia during the first quarter of 2025. This spike is mainly due to ongoing cost-of-living pressures and high interest rates affecting household finances.

Conforming mortgage arrears (loans overdue by 30 days or more) increased by 0.23% to 1.36%. Non-conforming arrears rose by 0.39% to 5.32%. This increase is nearly three times the usual seasonal rise of about 0.08% in the first quarter.

The combination of high interest rates and continuing inflation has driven this increase. Although the RBA cut rates in February and May, the benefits of these cuts weren’t visible in the first quarter data.

Housing prices also bounced back with a 0.9% increase after dropping in late 2024. Fitch expects prices to continue rising in 2025 due to limited housing supply, lower interest rates, and strong migration.

To manage potential losses from mortgage defaults, Fitch Ratings has changed Australia’s outlook from stable to negative while keeping its current rating.

This data clearly shows that mortgage arrears in Australia have risen substantially more than expected. Typically, we see a slight rise at the beginning of the year due to post-holiday spending pressures. However, this data indicates that these temporary issues have evolved into deeper financial challenges.

Standard loan arrears have surged, which is unusual. Riskier loans are seeing even greater difficulties since their borrowers have less flexibility with high rates. When interest rates stay elevated, we can anticipate some problems. Coupled with persistent inflation, the strain is evident in this data.

It’s important to note that these arrears increased even before recent rate cuts could impact them. While the rate reductions in February and May could provide some relief, the effects will take time to materialize. We likely won’t see significant changes until later this year, and financial stress continues to grow in the meantime.

Housing prices are picking up again after a brief drop. Rising prices can help borrowers struggling to make repayments. A borrower with equity in their home is less likely to default if they can sell or refinance. However, timing is a challenge. The support from equity may not be quick enough for households falling behind. Also, since the price increase is partially due to limited supply rather than strong demand, it’s not a complete solution.

The credit ratings landscape is responding. Moving from a stable to a negative outlook signals a warning. While the current rating remains the same, the underlying support is weakening. High arrears and sensitivity to interest rates cannot be overlooked. If conditions worsen, the calls for a reassessment will become louder.

From our perspective, this has clear implications. Risk pricing must change to reflect delinquencies that are not just seasonal hiccups. Credit performance is shifting. If we continue to rely on last year’s models, we risk underestimating true exposure. We need to recognize that borrower stress is lasting longer than initially expected, especially in more vulnerable asset pools.

Volatility linked to interest rate predictions will stay high as markets try to gauge when and how much monetary easing will happen. Even small cuts in policy rates may not immediately ease arrears. Borrowers adapt slowly, not instantaneously. Additionally, ongoing high costs for rent, utilities, and food are tightening the discretionary budgets that households rely on to stay current on payments.

For mortgage-linked instruments, past performance is no longer a reliable guide. We need to prioritize forward-looking metrics, such as wage growth and unemployment expectations, particularly when making adjustments to manage risk. The same applies to interest rate curves that are flattening based on optimism that remains, for now, unproven.

Moreover, short-term growth in housing prices might lead some models to underestimate the chance of defaults. A small increase in prices does not equate to strong consumer confidence, especially when driven by supply shortages and migration. These price hikes offer little comfort to borrowers still struggling to keep up with repayments.

We should not assume that historical trends will repeat themselves perfectly. Risk buffers and stress tests need continual adjustment. We should expect volatility in arrears to persist through midyear until we see clearer signs of recovery in disposable income – which we have not seen yet.

When making decisions based on assumptions about borrower behavior, it’s essential to be cautious. Models that fail to account for the transition from liquidity issues to actual loan deterioration risk missing crucial outcomes.

NZD/USD pair falls from yearly highs as it reacts to news about Iran

NZD/USD starts the week with a slight downward trend after last week’s peak near 0.6100. During the Asian session, the pair hits a new monthly low around 0.5930, showing signs of downward pressure in a risk-averse market.

Current events include the US and Israel’s military actions against Iran, specifically targeting its nuclear facilities. This rise in geopolitical tensions in the Middle East is increasing interest in safe-haven assets, benefiting the US Dollar (USD) while putting stress on the New Zealand Dollar, also known as the Kiwi.

US Fed Influence

The USD is also gaining strength from the Federal Reserve’s hawkish signals. They forecast fewer rate cuts in 2026 and 2027, while still expecting two cuts in 2025. Meanwhile, the Reserve Bank of New Zealand is likely to lower interest rates due to falling inflation and economic issues caused by US tariffs. From a technical perspective, if NZD/USD drops below the short-term trading range and the 0.6000 psychological level, it suggests a downward trend. This view is supported as the market waits for upcoming US PMIs to provide new direction. The recent downward pressure on NZD/USD indicates not only a change in overall sentiment but also a significant shift in risk due to the latest geopolitical events. With tensions in the Middle East rising after US actions targeting Iran, traders are moving their money into safer assets. The US Dollar, typically the go-to asset in uncertain times, has benefited from this trend. When risk appetite decreases, currencies linked to commodities or global growth expectations, like the New Zealand Dollar, generally decline. Additionally, expectations around US monetary policy are helping the Dollar. The Federal Reserve’s guidance suggests a waning chance of prolonged easing, leading to continued strength for the Dollar. Although there may still be a couple of rate cuts next year, longer-term signs indicate the Fed is not in a rush to ease their tightening stance. This perspective keeps rates relatively high, providing ongoing support for the Dollar.RBNZ Perspective

On the other hand, the Reserve Bank of New Zealand (RBNZ) is on a different path. With inflation rates falling and new challenges from US trade policies, New Zealand may soon have to lower borrowing costs. The softening inflation could push policymakers to relax conditions, although this won’t happen immediately. This difference in direction is not favorable for the Kiwi. When we look at the charts, the importance of the 0.6000 level is clear. The recent breach below this threshold suggests a more sustained move downward. Hitting fresh monthly lows shows how shifted market sentiment has become. Support is not expected until closer to the 0.5900 area, where there’s historical buying interest. As for upcoming economic releases, Wednesday’s US PMI figures may create some volatility and lead to corrections if expectations aren’t met. Conversely, if the data remains strong and reaffirms a robust US economy, the Dollar could strengthen even more. Traders should keep an eye on supply chains and business orders, both of which indicate persistent inflation that the Fed will pay attention to. We anticipate continued high volatility. A tactical approach may be more effective in the near term, given the reliance on data for US monetary policy. It’s wise to set tighter stop-loss orders, especially below recent support levels, while monitoring short-term resistance near 0.5980 during any corrective rallies. In summary, without a significant easing of geopolitical risks or a major decline in upcoming US economic data, any rebound in the NZD/USD pair may be limited. Current positioning favors Dollar strength over Kiwi resilience in the immediate future. Create your live VT Markets account and start trading now.GBP/USD falls to around 1.3405 as safe-haven flows rise amid geopolitical tensions

Rising Tensions and Market Dynamics

The US has launched airstrikes on Iranian nuclear sites, escalating geopolitical tensions. President Trump announced that Iran’s facilities were “obliterated” and warned of more action unless Iran seeks peace. In response, Iran has pledged to retaliate, driving up demand for safe-haven assets. In the UK, retail sales fell by 2.7% in May, reversing a previous increase and putting pressure on the Pound. The Bank of England kept interest rates unchanged at 4.25%, with possible cuts in future meetings due to uncertain economic forecasts. The Pound Sterling is affected by the Bank of England’s policies and economic data. The Trade Balance is another factor that impacts the Sterling by influencing currency strength based on export and import differences. As GBP/USD trades lower around 1.3405 in early Monday sessions, new patterns are emerging that warrant attention. Increased demand for the Dollar, driven by geopolitical risks from US military actions against Iran, has led to higher volatility. This situation often pressures GBP-based pairs during uncertain times.Impact of Geopolitical and Economic Factors

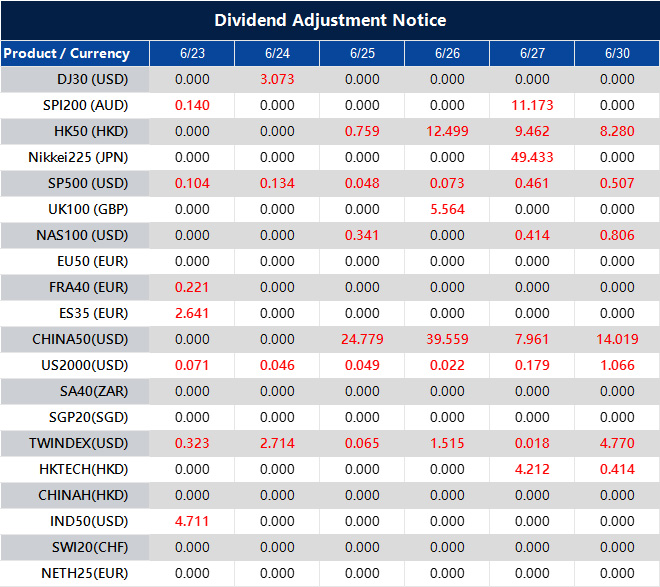

The recent airstrikes have prompted Washington to intensify its warnings of further military options, while Tehran has vowed to respond. Consequently, markets are pricing in greater instability, which historically benefits the Dollar in times of tension. Although the current pricing of Cable reflects this, there are deeper issues at play. In the UK, the economy experienced a significant drop in consumer spending last month. Retail sales plunged by 2.7% in May, marking a major reversal from previous resilience. This decline puts additional pressure on growth forecasts and complicates future monetary decisions. The Bank of England decided to keep interest rates steady at 4.25% in its latest meeting. However, with slowing growth data and flattening inflation, speculation about a rate cut before summer’s end is growing. Markets have taken notice, with short-term interest rate futures adjusting prices, impacting institutional demand for the Pound in yield-seeking contexts. Later today, the purchasing managers’ index (PMI) reports will be closely monitored by institutional investors. PMI data for both manufacturing and services, covering the UK and the US, can significantly shift market sentiment if they differ from expectations, especially with current tight trading ranges. The market’s reaction will likely set the tone for the week. Moreover, Britain’s trade data remains crucial. A widening trade deficit, whether due to increased imports or declining exports, puts added pressure on the domestic currency. In light of disappointing retail figures, weak trade performance further paints a fragile economic picture that many did not anticipate weeks ago. All this underscores the focus on interest rate direction. If US indicators show continued strength and the Federal Reserve maintains a relatively hawkish stance, the differences in monetary policies between the US and UK will be hard to overlook. In this environment of short-term volatility and data releases, it’s vital to reassess risks and fine-tune exposure. Movements in GBP/USD are now more closely linked to macroeconomic updates than to technical factors. Timing market entries based on high-probability outcomes may yield better results than relying solely on static price levels. This week is expected to remain volatile. Keeping an eye on data releases and geopolitical events is crucial, especially during US afternoon sessions when Dollar trading volumes increase. Currently, the directional trend favors the Dollar, but its persistence will depend more on the length of this wave of risk aversion than on previous price levels. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 23 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The People’s Bank of China sets the USD/CNY reference rate at 7.1710, an increase from 7.1695.

On Monday, the People’s Bank of China (PBOC) announced the USD/CNY central rate at 7.1710, up from the previous rate of 7.1695. This is lower than the Reuters estimate of 7.1914.

The People’s Bank of China aims to maintain stable prices and exchange rates while fostering economic growth. It also focuses on financial reforms to enhance its financial market.

Influence of the Chinese Communist Party

The PBOC is owned by the People’s Republic of China and is affected by the Chinese Communist Party. The current governor, Mr. Pan Gongsheng, also serves as the Secretary of the CCP Committee. The PBOC uses various monetary policy tools, including the Reverse Repo Rate, Medium-term Lending Facility, and Reserve Requirement Ratio. The Loan Prime Rate is crucial in shaping loan and mortgage rates, as well as the Chinese Renminbi’s exchange rates. China’s financial sector has 19 private banks, with WeBank and MYbank as notable digital lenders. In 2014, China allowed privately funded banks to operate, diversifying its state-dominated financial sector. The PBOC’s setting of the USD/CNY central rate at 7.1710 suggests a careful intervention. Although slightly higher than the previous rate, it’s well below the market expectation of 7.1914. This indicates a subtle effort to counteract depreciation pressures on the Renminbi while managing volatility. A rate below expectations usually signals that policymakers are wary of the yuan weakening too much, especially given the fragile consumer confidence and low export activity. The central bank’s decision shows a desire for stability. Instead of allowing the currency to drop further, they chose a more stable reference point. This can indicate a reluctance to let capital outflow concerns grow or to cause speculative issues. The central rate serves as a guiding tool. When markets receive a lower value than expected, it suggests a careful strategic approach. Gongsheng plays a key role in both policy implementation and party alignment, linking political goals with economic tools. Monetary decisions are generally influenced by domestic targets like GDP and employment, as well as managing systemic risks. The use of policy instruments like the Medium-term Lending Facility and Reverse Repo supports this approach.Adjustments and Financial Sector Dynamics

Recent cautious liquidity adjustments indicate that while easing may happen, it’s done with consideration of currency pressures. Although there’s ongoing talk of broad stimulus, the actions taken appear targeted, aiming to boost areas like infrastructure lending or support for small and medium-sized enterprises (SMEs) without causing broad inflation. This is evident in the stable Loan Prime Rate, which helps guide borrowing costs for households and businesses downwards. China’s financing model has evolved over time. The emergence of banks like WeBank and MYbank, along with the introduction of privately funded institutions since 2014, shows a willingness for reform. However, these new players still play a peripheral role, with state-linked lenders and policy intermediaries remaining dominant. In this context, any shifts in liquidity or capital flows need careful monitoring. While tools like the Reserve Requirement Ratio could change if growth declines sharply, current strategies focus on measured adjustments. This includes managing expectations regarding exchange rate flexibility, which is vital for exports and offshore derivatives. Practically, this means we should expect currency guidance to be used more openly, especially if foreign exchange reserves decline or trade data falls short of expectations. The Renminbi will likely be kept within specific limits rather than allowing quick, sentiment-driven changes. In the short term, anything related to USD/CNY fluctuations or offshore Renminbi instruments should be approached with caution, as Beijing isn’t ready for sharp disruptions. They appear focused on managing volatility rather than letting the market dictate outcomes. Thus, forward pricing or hedging strategies should account for tighter currency controls rather than unexpected shifts. We should also be alert to where foreign exchange pressures might arise if global sentiment on emerging markets changes. Monitoring signals from official sources and market indicators — especially swap rates and repo spreads — will help us understand how tightly liquidity is being controlled underneath the surface. Create your live VT Markets account and start trading now.WTI oil price nears $75.50 per barrel after US strikes on Iranian nuclear sites

The price of West Texas Intermediate (WTI) oil went up over 2%, reaching about $75.50 per barrel. This increase is due to U.S. military strikes on three Iranian nuclear facilities, raising concerns about oil supply.

U.S. President Donald Trump mentioned that the strikes hit Fordow, Natanz, and Isfahan, coordinated with an Israeli operation. Tensions with Iran could escalate further, as Tehran has promised to retaliate.