The Australian dollar weakens against a stable US dollar following recent PMI data from China.

The Australian Dollar fell against the US Dollar as China’s RatingDog Manufacturing PMI slightly improved to 50.3 in January. Australia’s TD-MI Inflation rose to 3.6% year-over-year, with a monthly increase slowing to just 0.2%. Despite a 4.4% rise in ANZ Job Advertisements, the Australian Dollar stayed weak as the Reserve Bank of Australia kept the cash rate steady at 3.6%.

**US Dollar Resilience**

The US Dollar had little movement as traders waited for the upcoming ISM Manufacturing PMI data. It had previously strengthened after Kevin Warsh was nominated as the new Federal Reserve Chair, suggesting a cautious approach to monetary policy. US producer-side inflation remained at 3.0% year-over-year, supporting a stable policy rate. Core PPI also increased to 3.3%.

The AUD/USD pair showed some positive signs, trading around 0.6940, with main support at 0.6927. It might rise towards 0.7093, supported by the nine-day moving average. Australia’s Consumer Price Index held steady at 3.8% year-over-year in December, affected by PMI and employment data. Overall, the Australian Dollar faces pressure from both global and local economic indicators.

The US Dollar appears strong, and we believe this trend could continue in the coming weeks. Markets expect a high chance of a rate hike from the Reserve Bank of Australia tomorrow, but Kevin Warsh’s nomination as Fed Chair suggests a more careful US monetary policy. This shift in the US is currently overshadowing the Reserve Bank’s anticipated hawkish stance.

Recent US economic data supports this view. The January Non-Farm Payrolls report showed a solid addition of 295,000 jobs, far exceeding expectations. A strong labor market gives the Federal Reserve little reason to ease policy soon. Therefore, the most likely direction for the US Dollar looks to be upward for now.

**Australian Dollar Outlook**

From our perspective, the Australian Dollar has challenges, even if the RBA raises rates as expected. Chinese manufacturing data from January showed only slight improvement, and iron ore futures have stayed around $130 per tonne, not providing much of a boost. This indicates that buying put options on the AUD/USD, with strike prices below the 0.6900 support level, might be a wise strategy for potential downside.

The mixed signals from central banks are likely to create more market volatility in the near future. Looking back at data from late 2025, we saw Australian inflation and employment figures doing well, yet the currency struggled to gain ground. For traders expecting sharp price movements but uncertain about the direction, using a long straddle with options around the RBA’s announcement could be a way to capture significant moves either way.

Create your live VT Markets account and start trading now.

Deutsche Bank report shows 8.95% drop in gold prices due to Fed Chair nomination

Deutsche Bank’s report highlights a notable drop in gold prices, seeing an 8.95% decline—the largest since 2013. This volatility is linked to Kevin Warsh’s nomination as Fed Chair, which has created a more hawkish outlook and led to increased speculation in the gold market.

Recent Market Shifts

Gold and silver have both taken hits recently, dropping by 5% and 10%, respectively, amid the expected resolution of a partial US government shutdown. This shift signals a broader caution in the market. Gold experienced an 8.95% decline in just one day, contributing to a weekly drop of 1.87%. The fluctuations in precious metals are driven by speculative behaviors. The report, analyzed using an AI tool, has also undergone an editorial review. It emphasizes the insights from the FXStreet Insights Team, which gathers expert market observations to deliver thorough analysis. Gold’s sharp decline, its worst since 2013, responds directly to the expectation of a more assertive Federal Reserve. With the possibility of Kevin Warsh becoming Fed Chair, the market is rapidly adjusting to anticipated higher interest rates. This uncertainty has caused volatility to surge, making gold options premiums very costly for buyers. For those trading derivatives, this sudden shift in Fed expectations indicates ongoing challenges for gold. The CME FedWatch tool now predicts a nearly 90% chance of a significant rate hike in March, strengthening the dollar and putting pressure on non-yielding assets. Therefore, adopting bearish strategies, like purchasing puts on gold ETFs, might be wise as we prepare for potential further declines.Speculative Components and Volatility

It’s crucial to note that the recent rise in gold was significantly driven by speculation. Reviewing the Commitment of Traders data from January 2026, we observe that managed money net-long positions were at their highest in over two years, suggesting an overcrowded trade. This sell-off is clearing out weak investors, which may keep prices trending lower in the near term. The rise in implied volatility offers a potential opportunity. The Cboe Gold Volatility Index (GVZ) recently hit 35, a high not seen since the banking turmoil of 2024. For those who feel the peak of the panic is over, selling options to take advantage of these high premiums could be a solid strategy in the coming weeks. This scenario has happened before, notably during the ‘taper tantrum’ of 2013. Just a hint of the Fed tightening policies led to months of decline in precious metals as speculative positions were unwound. This historical context suggests that we might be entering a new trend for gold rather than experiencing a temporary setback. Create your live VT Markets account and start trading now.Sweden’s Manufacturing PMI rises to 56, up from 55.3

The Manufacturing Purchasing Managers’ Index (PMI) for Sweden increased to 56 in January, up from 55.3 the month before. This points to growth in Sweden’s manufacturing sector.

Various reports highlight economic trends. China’s economy is struggling, and the Euro is under pressure against the US Dollar, even with good manufacturing data from the Eurozone.

US Dollar Shows Signs of Recovery

The US Dollar is showing signs of recovery, impacting many markets. Silver prices have dropped as demand for this safe-haven asset declines. Additionally, some currency pairs are fluctuating. The EUR/JPY is around 183.50, even with positive Eurozone PMI data. Meanwhile, EUR/USD and GBP/USD are at low levels because of the US Dollar’s strength. Market analysis looks into potential influences and movements while considering the best brokers in 2026. This includes recommendations for top forex platforms, brokers with low spreads, and options for trading major currency pairs like EUR/USD and Gold. Investors should think carefully about their decisions. The information provided is not a recommendation and is meant for informational purposes only. Any associated risks fall on the investor.Market’s Attention on US Dollar Strength

The market is now focused on the US dollar’s strength, largely due to speculation about a more aggressive Federal Reserve. This “Warsh effect” indicates a quicker pace of interest rate hikes than we expected a few weeks ago. As a result, we see significant pressure on currencies trading against the dollar, including the Euro. Though Sweden’s manufacturing PMI increased to 56, signaling good industrial health, it isn’t enough to offset the dollar’s momentum. Even positive data from the Eurozone isn’t lifting the EUR/USD pair, showing that the market is centered on US monetary policy. Recent data supports this perspective, with the US Dollar Index (DXY) exceeding 105 for the first time since late 2024. All attention is on the upcoming US ISM Manufacturing PMI, expected to show solid expansion around 57.8, emphasizing the gap with other economies. This is a shift from the sentiment we saw in late 2025, where a softer dollar was prevalent. For currency traders, this suggests positioning for further EUR/USD weakness, possibly using put options to aim for a break below the 1.1800 level soon. The Swedish Krona’s strength against the dollar will likely be limited, but it may perform better against the Euro. This makes shorting the EUR/SEK pair an appealing trade to separate Sweden’s positive data from the dollar’s dominance. The current situation is also challenging for commodities, with both gold and silver continuing their recent declines. A strong dollar and the possibility of higher US interest rates lessen the appeal of non-yielding assets, similar to what we observed during the Fed’s aggressive rate hikes in 2022. Derivative strategies could include shorting gold futures or buying puts as long as the dollar rally persists. In interest rate markets, futures now anticipate over 100 basis points of Federal Reserve hikes for the rest of 2026. This is a significant shift from the balanced outlook we had at the end of last year. This change suggests that volatility will stay high, and traders should consider positions that benefit from rising short-term US rates. Create your live VT Markets account and start trading now.Switzerland’s real retail sales increased by 2.9% in December, exceeding the expected 2.5% growth.

In December, Switzerland’s retail sales rose by 2.9% compared to the previous year, exceeding the expected 2.5%. This shows that the retail sector is performing better than anticipated.

In the currency markets, EUR/USD is currently weak, hovering around 1.1850. This weakness comes from a strong US Dollar, especially after news about Kevin Warsh’s potential nomination as Fed Chair. GBP/USD has slipped below 1.3700, fueled by uncertainty regarding Warsh’s leadership.

Gold and Cryptocurrency Market Trends

In commodities, gold prices have dropped to monthly lows around $4,400. This decline is due to profit-taking and the strengthening US Dollar. Meanwhile, Cardano’s price has dipped below $0.28, part of a broader decline in the cryptocurrency market, with Bitcoin falling below $75,000. There are discussions about the Best Brokers in 2026, focusing on top brokers for Forex and gold trading, along with their advantages and disadvantages across different regions. The content contains forward-looking statements that involve risks and uncertainties. While it serves as informative, accuracy isn’t guaranteed. FXStreet is not responsible for any investment choices made based on this information. The market is clearly reacting to the nomination of a new, more hawkish Fed Chair. The US Dollar Index has risen by 1.5% in the past five trading days, reaching its highest level since November 2025. This strength makes buying call options on the dollar or selling futures on weaker currencies like the Euro and Pound an appealing strategy for the upcoming weeks.Profit Taking in Gold Market

Gold is experiencing predictable profit-taking, pulling back from its recent high above $4,550 an ounce. This mirrors the pattern seen during the 2013 “Taper Tantrum,” where expectations of tighter monetary policy led to declines in precious metals. Traders might want to consider buying put options on gold futures, anticipating further drops as the market adjusts to higher US interest rates. Pay attention to the strong data emerging from Switzerland, where retail sales have exceeded expectations. This fundamental strength, along with a record-low unemployment rate of just 2.1%, makes the Swiss Franc robust. There’s an opportunity to short the EUR/CHF pair, taking advantage of the strong Franc compared to a Euro that’s struggling despite its own positive news. All eyes are on the upcoming US ISM Manufacturing PMI data later today. A strong reading would support the hawkish Fed narrative and could spark a significant market movement, while a weaker outcome might cause a rapid reversal. With currency market volatility up 20% in the last week, using straddles or strangles on major pairs like EUR/USD can help profit from big movements in either direction. Create your live VT Markets account and start trading now.The US Dollar Index stays stable above 97.00 after previous gains, nearing PMI data release.

The US Dollar Index is holding steady above 97.00 as we await the release of the ISM Manufacturing PMI data. This Index measures the US Dollar’s value against six major currencies and has stabilized after a rise of over 1% in the previous session, trading around 97.20 during Tuesday’s Asian hours.

The Dollar is gaining support as concerns grow about the Federal Reserve’s policy direction, especially after Trump’s nomination of Kevin Warsh as Fed Chair. Warsh is seen as leaning towards lowering rates, though not as aggressively as some other candidates.

Expected Changes by Fed

Warsh is expected to trim the Fed’s balance sheet, which could impact market liquidity. Two rate cuts are still likely this year under his leadership, but the FOMC remains unsure about the pace of these reductions. Sentiment in the markets is improving as the US Senate moves forward with a government funding package, reducing the risk of a shutdown. US producer price index (PPI) inflation held steady at 3.0% year-over-year in December, beating forecasts and reinforcing the Fed’s current policy. The US Dollar is the official currency of the USA and is a leading global currency. It significantly influences currency markets and was backed by gold until 1971. The Federal Reserve’s policies directly impact the dollar’s value, affecting interest rates and involving measures like quantitative easing or tightening. Currently, the US Dollar Index is trading around 104.50, a notable change from the 97.00 level common in 2025. This strength exists despite ongoing debates about the Federal Reserve’s next steps. Traders should consider this higher baseline as it impacts calculations for currency-related derivatives.Recent Economic Indicators

Looking back at last year’s market, there was speculation about appointing a new Fed Chair and expectations of two rate cuts. In early 2026, the Federal Reserve has made several adjustments, leading to increased uncertainty about future moves, with a focus on economic data. This shift from a clear easing stance has altered the risk profile for the dollar. Last year’s producer inflation data showed core PPI stubbornly at 3.3%, but this has since eased. The latest Consumer Price Index (CPI) report for January 2026 indicates core inflation has moderated to 2.4%, approaching the Fed’s target. While this is a positive development, it raises questions about whether the Fed will keep its current approach or signal changes ahead. With the transition from a clear easing path to a data-driven strategy, interest rate market volatility has increased, as shown by the MOVE index hovering around 120. Derivative traders should develop strategies to manage potential fluctuations in the dollar and Treasuries. Being prepared for sudden policy announcements is now more important than it was in 2025. Attention is shifting from last year’s funding agreements to the new Congress’s upcoming fiscal debates. Discussions about the budget and debt ceiling could bring new risks that did not exist in 2025. These political issues are likely to affect market sentiment, causing sharp movements in the dollar, regardless of Fed policy. Create your live VT Markets account and start trading now.In January, forecasts predicted a 0.3% increase in UK Nationwide housing prices, and that goal was met.

The UK Nationwide Housing Prices data for January 2026 shows a 0.3% increase from the previous month, which aligns with market expectations. This growth indicates steady progress in the housing sector, showing resilience despite possible economic challenges.

Experts suggest that the stability in prices may be due to ongoing demand, driven by low-interest rates and buyers’ continued interest. Future economic data will be closely monitored for any signs of changes in the housing market.

Market Stability Analysis

The housing price rise of 0.3% in January shows that the market is stable, just as we expected. Since this change wasn’t surprising, we don’t anticipate any sudden market shifts. This stability eases concerns about a sharp economic decline. This consistent data gives the Bank of England less reason to quickly cut interest rates. With UK inflation remaining stubborn at 2.4% at the end of 2025, the Bank will likely proceed cautiously. Therefore, those trading in interest rate derivatives may find that bets on significant rate cuts in the near future are becoming less probable. For currency traders, this news should support the pound. A steady housing market, combined with the potential for UK interest rates to stay higher for longer compared to other areas, strengthens the case for GBP. We might see traders reducing their short positions against the pound.Impact on Stocks and Future Data

This stability also benefits UK-focused stocks, especially in the banking and construction sectors. After the uncertainty of 2025, this consistent performance could increase investor confidence in domestic companies. This might suggest looking at call options on the FTSE 250 index, which is heavily linked to the UK economy. After experiencing a slowdown in the housing market post-rate hikes over the past few years, this calm period is a notable change. We will closely watch the upcoming UK jobs and inflation data, as these figures will provide important insights for the Bank of England’s future decisions. Create your live VT Markets account and start trading now.In January, the UK Nationwide’s annual housing prices surpassed forecasts by 1%, reaching 0.7%.

UK housing prices rose by 1% year-on-year in January, exceeding expectations of 0.7%. This increase comes amid various financial updates affecting several markets and sectors.

Silver prices took a significant hit recently, marking their largest daily plunge since 1980. Meanwhile, the Euro has remained steady despite positive PMI data from the Eurozone. The Pound Sterling weakened as market sentiment changed following the nomination of a new US Federal Reserve Chair, with the USD/GBP exchange rate falling below 1.3700.

Cryptocurrency Market Trends

In the cryptocurrency sphere, Cardano’s prices dropped under $0.28, continuing a downward trend. Bitcoin also fell, dipping below $75,000 due to increased selling pressure. Several brokers are preparing for 2026, highlighting those with low spreads and those best suited for specific currency pairs like EUR/USD. Investors should thoroughly research due to the risks associated with market investments, understanding potential losses and the volatility involved. January’s UK housing price increase of 1% year-on-year suggests some strength in the UK economy, which is surprising given the global market conditions. This marks a notable shift from the negative trends seen throughout much of 2024 and early 2025.Impact Of New Federal Reserve Chair Nomination

Currently, the nomination of Kevin Warsh as the new Federal Reserve Chair is a major market influencer, pushing the US Dollar up across the board. His hawkish reputation indicates that we might see higher interest rates sooner than expected. This has led to a risk-off environment, diverting attention from the Fed’s previous cautious stance. For currency traders, this development strengthens the case for shorting GBP/USD, particularly as it has fallen below the significant 1.3700 level. This level served as important support in late 2025, so a continued drop may signal further losses. Considering the conflicting UK housing data, put options on the Pound Sterling could be a strategic way to trade this scenario while managing risk. Gold is also under pressure from the strong dollar, pulling back from recent record highs around $4,400. This mirrors reactions seen in the early 1980s when a hawkish Fed policy led to a significant downturn in precious metals. We can expect continued weakness in gold and silver as long as the market anticipates a more aggressive US central bank. Overall market anxiety has likely driven up implied volatility, making options pricier. The CBOE Volatility Index, or VIX, is likely trading above its 2025 average of 15, reflecting current uncertainty. This environment suggests careful sizing of any derivative positions, as sharp price movements are anticipated in the upcoming weeks. Create your live VT Markets account and start trading now.Retail sales in Germany rose 0.1%, surpassing forecasts and avoiding a decline

Germany’s retail sales for December saw a small rise of 0.1%, beating expectations of a 0.2% decline. This suggests a slight recovery in consumer spending during that month.

In other market news, Bitcoin dropped below $75,000, down 11% from the previous week. Cardano also declined, trading under $0.28, with a correction of over 15%.

Federal Reserve Chair Nomination

Kevin Warsh’s nomination as the Federal Reserve chair raised concerns in European currencies and gold. The EUR/USD remains weak, hovering around 1.1850, and gold has fallen to new monthly lows. In additional market changes, the Pound Sterling weakened, while USD/INR declined due to the Reserve Bank of India’s efforts to support the Indian Rupee. The financial community is closely watching the upcoming US ISM Manufacturing PMI data for further market insights. Looking back at early 2025, when Kevin Warsh was nominated for Fed Chair, we saw a big rally in the US Dollar. During that time, the EUR/USD fell near 1.18, and GBP/USD dropped below 1.37 as traders anticipated a more aggressive central bank. This serves as a useful guide for how markets react to a hawkish Federal Reserve. Announcements like this can lead to sharp price fluctuations. For example, volatility spiked in that week of 2025, with the VIX climbing above 20. We can expect similar movements in the weeks ahead as key central bank speeches occur. Traders might consider using options, like buying straddles or strangles on major currency pairs before significant announcements to capitalize on volatility.Impact Of US And Eurozone Inflation

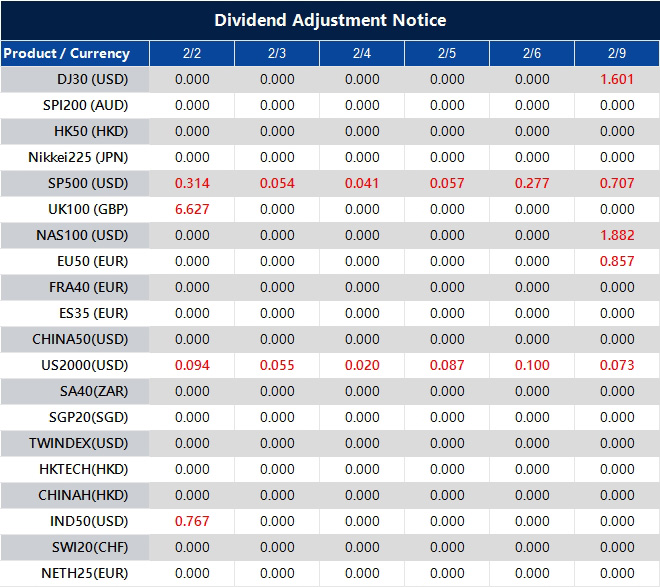

At that time, the slight better-than-expected German retail sales did not help the Euro, as the Fed’s policy was the main focus. However, today’s situation is different. Recent Eurostat data for January shows Eurozone inflation steady at 2.8%, keeping pressure on the ECB. In contrast, the latest CPI report from the US indicates inflation has cooled to 3.1%, suggesting the Fed’s aggressive stance from last year might be ending soon. The significant drop in gold during the “Warsh effect” in 2025 was due to a stronger dollar and rising yield expectations, making non-yielding assets less appealing. This inverse relationship is important to monitor in the coming weeks. With the dollar index down nearly 2% since last November, call options on gold could offer upside potential if the Fed adopts a calmer approach. Similarly, the pound faced challenges last year, but the UK’s economic situation has improved. The latest report from the Office for National Statistics reveals that UK inflation remains the highest in the G7 at 4.0%, which compels the Bank of England to maintain a hawkish stance. Unlike in 2025, the pound may now show greater strength against the dollar, making it worthwhile to consider selling put options on GBP/USD to earn premium. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Feb 02 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In December, retail sales in the Netherlands increased to 4.5% year-on-year, up from 3.9%

Retail sales in the Netherlands increased by 4.5% in December compared to last year, up from 3.9% previously. This growth is occurring alongside broader trends in global finance.

The USD/CHF is holding steady near 0.7730 as we await the US ISM PMI data release. On the other hand, the USD/JPY has dropped below 155.00, forming a descending channel pattern.