JPY bulls show weak commitment despite strong domestic CPI and rising Middle East tensions

The Japanese Yen is currently performing well against the US Dollar, but it remains close to its recent monthly low. In May, Japan’s Consumer Price Index (CPI) rose above the Bank of Japan’s (BoJ) target of 2%. This has led to expectations of future interest rate hikes, which is helping the Yen, especially amid rising geopolitical tensions.

However, the BoJ’s careful approach to cutting monetary stimulus means that rate hikes might not happen until the first quarter of 2026. Concerns about US tariffs on Japanese goods are also limiting the Yen’s potential gains. At the same time, the Federal Reserve’s economic policies are helping the USD/JPY pair.

Calm news from the Middle East boosts risk assets and positively impacts the US dollar and equities

News from the Middle East is currently quiet, leading to a preference for riskier assets instead of the US dollar. As a result, the USD is showing signs of weakness, and trading activity is limited.

The US has indicated that it may take up to two weeks to decide whether to support Israel against Iran, but this timeframe is uncertain. Such statements can be tricky because war can be unpredictable, which may cause anxiety in the coming days.

At the moment, risk assets are gaining popularity, with slight increases in equities. The overall market feels tense, but right now, riskier investments are favored.

The lack of new issues or developments in the Middle East is making investors more interested in riskier assets, like the Australian dollar or emerging market currencies. This shift has softened demand for the US dollar. Basically, when there’s no alarming news, traders start to move back toward more volatile assets in search of better returns.

Meanwhile, traders are closely monitoring statements from Washington. Although there’s a note about possible delays in military coordination, timeframes in geopolitics can be tricky. The moments leading up to significant announcements can feel prolonged, and uncertainty usually keeps market movements in check.

Even small changes in stock performance are often spotted early by derivatives markets. These slight gains indicate some underlying optimism, likely more because of the lack of bad news than the presence of good news. This cautious confidence has led short-term traders to explore the edges of trading ranges.

Currently, options pricing is showing hesitancy. Implied volatility hasn’t dropped significantly, but it hasn’t increased either. This middle ground is stable for now but could change quickly with new developments in politics or the economy. Derivative traders should stay alert. We’re observing that short-term investments are clustering near recent peaks, which suggests a continuing fragile appetite for risk.

Volatility sellers are relaxed but not overly confident. If actual volatility increases, a quick reassessment is likely. Therefore, we are paying close attention to market liquidity and depth in overnight and one-week periods. Any gaps could signal important changes.

A practical strategy we recommend is maintaining flexible delta exposure using straddles or strangles with low gamma, especially when the skew offers good premiums. This approach allows for expression of uncertainty without taking on too much risk. For those looking to hedge, employing vertical spreads can help manage costs while still protecting against potential downturns in the current market.

The weaker US dollar is providing a subtle boost to various currency trades, but we are approaching this with caution. We’re structuring trades with the expectation of modest follow-through rather than a complete collapse of the dollar’s strength. This means using call spreads instead of outright long positions on high-risk currencies.

Short volatility positions are still manageable, but complacency is risky. Regular adjustments for news-related risks are essential. As we near the end of the week, paying attention to price movements around options expiration levels will be particularly insightful.

It’s easy to think of calm as a moment before things become clear, but more often, it’s when positions get crowded or exposed. This is when opportunities—and risks—become more apparent as the market starts to move again.

Gold prices decline in Pakistan, according to market data

Gold prices in Pakistan fell on Friday. The price per gram decreased to 30,599.02 PKR from 30,754.37 PKR the day before. The price per tola also dropped to 356,900.50 PKR from 358,713.00 PKR.

The US Federal Reserve has decided to keep interest rates steady and expects two rate cuts by 2025. However, only one rate cut is predicted for 2026 and 2027 because of ongoing inflation worries.

Global Risk Sentiment

Global risk sentiment remains fragile due to trade uncertainties and geopolitical tensions, especially in the Middle East. Ongoing tensions between Iran and Israel, along with possible US involvement, raise fears of a broader conflict. The US Dollar retreated after recent market activities, which may help support commodity prices like gold. This situation suggests stability for gold prices, and some buying activity is expected as prices drop. Gold is often seen as a safe-haven asset during difficult times, and central banks are significant buyers. The price of gold is influenced by factors such as geopolitical stability, interest rates, and the strength of the US Dollar. Although the drop in gold prices seems small, it signals a shift in sentiment after the Fed’s recent announcement. By maintaining interest rates and indicating a slower timeline for cuts, the Fed showed concern about persistent inflation. Chairman Powell’s comments did not offer much hope for those anticipating quick monetary easing, as the projection for just one rate cut in 2026 and 2027 suggests.Geopolitical Risks and Market Sentiment

For traders of derivatives linked to commodities like gold, the Fed’s caution should prompt a reassessment of medium-term strategies. Although nominal yields haven’t dramatically increased, they remain elevated, limiting gold’s upside momentum in the short term, despite a weaker Dollar. Geopolitical risks are still high, particularly in the Middle East. Tensions between Tehran and Tel Aviv continue to dominate headlines, and potential American involvement keeps markets in a wait-and-see approach. This caution tends to increase demand for safe-haven assets, though recent reactions have been muted. Currently, we observe selective hedging rather than significant trading volume. Notably, the Dollar pulled back after the Fed’s announcement—possibly a minor correction or a reflection of revised rate expectations. This reduction has eased some pressure on Dollar-denominated assets, creating a supportive base for commodities. Gold tends to benefit when the Dollar weakens, as its price becomes more appealing internationally. A lower Dollar generally increases buying interest from non-US markets. Support levels are currently being tested, providing opportunities. While investments in physically-backed ETFs have slowed, market interest remains. Long-term buyers may not pursue recent highs but are often ready to re-enter at attractive price levels, especially if inflation persists and geopolitical tensions remain. If regional conflicts escalate, we can expect increased interest in defensive assets. Traders should prepare for wider bid-ask spreads in such scenarios, especially in times of low liquidity. Conversely, unexpected news from the next Fed meeting or signs of economic softening in the US could renew a dovish outlook, reviving bullish bets on gold. Sharp price changes are unlikely unless a clear trigger appears. For now, focus on where buying resumes. If prices test previous support zones and buying increases, it’s a reasonable opportunity for short-term trading. Caution is advised with leverage, particularly as macro risks rise and holiday trading volumes dwindle. Any short positions should be closely monitored and not left unattended if significant news breaks. Although gold remains within a broad trading range, we see early signs of accumulation at lower levels. Pay attention to shifts in open interest and how implied volatility reacts during significant intraday movements, as these often provide clearer insights than price alone. Also, keep an eye on the commitment of traders data—renewed long positions by large speculators often signal upcoming directional moves. Create your live VT Markets account and start trading now.The yuan’s reference rate is set at 7.1695, which is lower than the expected 7.1801.

The People’s Bank of China (PBOC) is the central bank of China and sets the daily exchange rate for the yuan. The yuan follows a managed floating system, meaning it can move up or down by 2% around a central rate that the PBOC decides each day.

The yuan’s previous closing rate was 7.1870. Recently, the PBOC added 161.2 billion yuan into the market through 7-day reverse repos at an interest rate of 1.40%.

PBOC’s Recent Actions

On that same day, 202.5 billion yuan worth of funds expired. This led to a total withdrawal of 41.3 billion yuan from the financial system. In simple terms, the PBOC actively manages the yuan’s value each day by setting a central rate and allowing slight fluctuations around it. This daily rate serves as a guide, letting the currency vary within a controlled range. The central bank’s recent liquidity strategy tells an important story. By pushing in 161.2 billion yuan with short-term reverse repos, which help alleviate short-term cash shortages, the PBOC also let 202.5 billion yuan mature. This resulted in a 41.3 billion yuan drop in available funds. These actions indicate that the bank is focusing on tighter conditions, aiming to manage speculation and control inflation rather than loosening monetary policies. For those tracking short-term interest rates and risks, these daily changes are significant. They may slightly raise short-term interest rates, impacting strategies like carry trades and overnight swaps. With the PBOC signaling tighter funding, it’s crucial to adapt strategies around yuan exposure in the coming days.Implications for the Economy

There’s also a hidden message about the yuan’s future. A lower net injection, along with controlled fluctuations, can signal a push for stability—often leaning toward strength, especially when combined with higher fixing rates. Observing how the midpoint rate behaves in the trading week could reveal the central bank’s near-term intentions. It’s less about reacting to the overall liquidity numbers and more about understanding the balance between money entering and leaving the system. Whether the daily net figure is positive or negative should guide strategies for leverage and holding periods. Caution is advised when holding onshore yuan through local contracts, as the authorities might not want to encourage too much yuan weakness, even as the dollar strengthens. As we monitor these liquidity operations, it’s wise to reconsider the costs of maintaining open positions in yuan-linked contracts. Changes in repo dynamics, particularly with 7-day rates, may alter forward pricing, affecting short-dated options and other time-sensitive contracts. A broader approach to loosening measures from Beijing is unlikely unless visible financial stress emerges. In conclusion, it’s essential to pay close attention to the PBOC’s daily operations rather than waiting for larger macro updates or meetings. Create your live VT Markets account and start trading now.Australian dollar strengthens after China’s interest rate decision, despite rising tensions in the Middle East

The Australian Dollar has steadied after the People’s Bank of China kept its Loan Prime Rates at 3.00% for one year and 3.50% for five years. However, ongoing tensions in the Middle East could boost the US Dollar’s strength.

The Australian Dollar has shown some recovery, but Middle Eastern tensions may limit its growth. The AUD/USD pair is around 0.6480, with signs pointing to possible upward trends.

China’s Economic Indicators and Australia’s Employment

In May, China’s Retail Sales grew by 6.4% year-on-year, surpassing expectations, while Industrial Production increased by 5.8% year-on-year, falling short of forecasts. Australia experienced a slight job loss of 2,500 positions in May, keeping the unemployment rate steady at 4.1%. The US Dollar Index is around 98.60, showing a slight decrease. The Federal Reserve has chosen to maintain interest rates at 4.5%, although future cuts may rely on upcoming economic data. Tensions between the US and Iran persist, with reports hinting at potential US military action. Ongoing uncertainties about Iran’s nuclear program could impact future market movements, and traders are closely monitoring discussions from the US administration. Let’s focus on how different factors are interconnected. The Reserve Bank in Beijing’s decision to hold the Loan Prime Rates steady provided some predictability. What happened next? The Australian Dollar rose slightly, but this shouldn’t be mistaken for confirmed upward momentum. It simply bounced back within a previous range. When retail sales in China temporarily exceed expectations—like the 6.4% year-on-year increase in May—it usually indicates stronger consumer sentiment. However, the lower-than-expected industrial production growth at 5.8% offers a more sobering outlook. This balance between consumer spending and manufacturing output creates pressure on resource-linked currencies, particularly concerning export demand and overall investor interest in commodities, especially iron ore, which is crucial for Australia.US Dollar and Geopolitical Tensions

Looking at Australia’s own situation, employment numbers showed a slight decline with 2,500 jobs lost, yet the unemployment rate held steady at 4.1%. This indicates a level of stability or resilience within the domestic job market. Nonetheless, the small reduction in employment doesn’t provide the impetus for aggressive policy changes from the Reserve Bank of Australia. Meanwhile, the Fed decided to keep rates steady at 4.5%, a largely anticipated move. The key question now is whether we’ve reached peak rates and when a shift towards easing may begin. The Fed is framing future decisions based on economic data, keeping options open but not yet acting. The US Dollar Index around 98.60 suggests a minor pullback rather than a downward trend. It’s a calm period, but awareness is high. With the possibility of new military actions in the Middle East surfacing again, the broader implications cannot be ignored. Any escalation in this region, especially affecting energy supplies, could give the Dollar a solid boost. Historically, such situations lead to increased demand for safe-haven assets, often benefiting the greenback. Concerns about Iran’s nuclear ambitions do not exist in isolation; they directly impact commodity prices and overall market sentiment. As discussions among policymakers intensify, reactions in treasury and derivative markets are likely to become sharper. There’s no neutral ground here—traders will remain cautious until there’s more clarity. In summary, market pricing will heavily depend on interest rate expectations and geopolitical developments. We are watching both ends of the spectrum: short-term bets related to oil prices and long-term options reflecting central bank strategies. In options markets, we see minor adjustments in premiums, indicating a wait-and-see approach rather than strong directional trends. Overall, while the AUD/USD has gained some ground, the broader picture—soft job numbers, uncertainty around China’s manufacturing, and risks of US military involvement—suggests it’s wise to adjust risk profiles for potential challenges rather than pursue short-term gains. Volatility isn’t absent; it’s just compressed and may emerge quickly. Create your live VT Markets account and start trading now.The People’s Bank of China keeps the Loan Prime Rate steady, meeting market expectations and promoting stability

The People’s Bank of China has kept its 5-year Loan Prime Rate at 3.50%, which matches expectations and last month’s rate. Likewise, the 1-year Loan Prime Rate remains at 3%, consistent with forecasts and the previous month.

Last month was the first time the Loan Prime Rates were cut since October. The 1-year rate went down from 3.1% and the 5-year rate fell from 3.6%. Additionally, the 7-day reverse repo rate was reduced by 10 basis points to 1.4% earlier that month. This shows that Loan Prime Rates are becoming less important as tools for monetary policy.

The People’s Bank of China is now concentrating on the seven-day reverse repurchase agreement rate as its main tool for monetary policy. This shift started in mid-2024 and aligns China with global practices. Major institutions like the U.S. Federal Reserve and the European Central Bank typically rely on a single short-term policy rate to manage market expectations and liquidity.

The People’s Bank of China has chosen to keep rates steady for now, resisting pressure to make further cuts soon. This decision follows last month’s unexpected rate decreases, which gave the market a brief boost. While unchanged 1-year and 5-year Loan Prime Rates may seem like inaction, they likely indicate a careful recalibration.

Zhou’s bank has shifted its attention from the longer-term Loan Prime Rates, which were once used to influence broader credit costs. By stabilizing these rates, it suggests that the phase of broad credit easing is paused, not abandoned. Meanwhile, the 7-day reverse repo rate has become the main tool for managing market liquidity and communicating policy intent. With this shorter-term rate already adjusted last month, it aligns more closely with strategies used by major Western central banks.

The key takeaway is this focus on short-term rates. This strategy emphasizes flexibility and precision. Short-term tools allow policymakers to respond quickly to domestic conditions without changing broader rate benchmarks. When the focus is on overnight or seven-day tools, it usually signals an aim to keep markets well-supplied with cash instead of aggressively addressing slow demand.

If current rates remain unchanged, capital costs across various periods should not see surprises. However, the shape of the rate curve may shift slightly, especially with ongoing liquidity injections in the market. Recent data from China does not suggest an urgent rise in inflation or credit demand, so there is no expectation for aggressive tightening at this time. Instead, we might observe gradual adjustments around liquidity, as authorities seek to avoid sudden changes in funding conditions.

Economic charts from the last six months show limited fluctuations. While the policy approach is stable, it may be hiding concerns about weaker domestic demand. This could lead cash-rich institutions to explore slightly riskier options, especially if forward guidance remains stable for too long.

Traders should watch for minor changes in liquidity tools and monitor interbank funding pressures closely. An increase in repo volumes or small rate changes could indicate subtle shifts in direction. Even though headline rates remain steady, the underlying message may still evolve. Changes often begin quietly before they are obvious.

If trading structured options or futures tied to short-term rates, observing overnight SHIBOR and repo market trends might provide clearer signals than the prime rates themselves. These small movements show real-time demand for cash and can indicate the central bank’s level of comfort with current liquidity. The appeal of short-dated instruments may stay strong unless there is an unexpected reversal in flows.

As a practical strategy, monitoring the spread between short-term and medium-term instruments could give early signals. If tighter repo windows appear, that would be a more dependable indicator than any carefully crafted press release. The PBOC’s communication isn’t always straightforward, so market responses can provide insight into institutional thinking.

The time of long forward rate guidance in China seems to be fading. We’re now in a period where even small moves are significant. Whether this is a chance or a warning—well, it depends on your perspective.

Gold prices in India have declined, according to recent data analysis from various sources.

Gold prices in India fell on Friday. The cost per gram decreased from 9,388.94 INR to 9,341.84 INR. A tola of gold also saw a drop, from INR 109,510.80 to INR 108,961.30.

Gold is commonly bought as a safe investment and a way to protect against inflation. Central banks, especially in emerging economies, are significant buyers and acquired 1,136 tonnes in 2022.

Gold’s Relationship with Other Assets

Gold typically moves in the opposite direction of the US Dollar and US Treasuries. When these assets lose value, gold often increases. Its price is affected by global events, interest rates, and shifts in currency values, notably the US Dollar. Pricing is based on adjusting international rates to the Indian Rupee and local standards. Although prices change daily, there may be slight differences from local rates. Factors like market conditions and currency exchanges influence gold prices, so thorough research is essential before investing. The recent decline in gold prices, seen in both per-gram and per-tola rates, may be a response to broader economic changes, particularly the strengthening of the US Dollar and stable Treasury yields. As gold usually moves against these trends, this dip follows typical patterns. Those monitoring price movements for short-term trading should assess whether this drop is just a pause or signals a trend change in the coming weeks. Historically, central banks in non-Western countries have accumulated gold, and the addition of 1,136 tonnes in 2022 was intentional. Policymakers recognize gold’s defensive advantages. This institutional demand tends to be focused on the long term and does not directly affect daily prices but can provide support during deeper declines. However, unless there’s an outside shock, this demand won’t significantly impact short-term price movements.Impact of Exchange Rate Changes

Exchange rate volatility is also important to consider. When the Rupee weakens, even steady or slightly falling international prices can lead to higher local prices. Currently, domestic rates are decreasing, suggesting either a stable or stronger Rupee or a sharper decline in global prices compared to exchange rates. We need to closely follow central bank statements and US macroeconomic updates to see if this trend continues or reverses. Price movements related to the Dollar are a key factor. If data continues to indicate a tight monetary policy in the US, then a hawkish stance from Washington could further suppress non-yielding commodities. A cautious approach might involve gradually entering the market rather than expecting immediate support. There’s no gain in overcommitting when key support levels haven’t been tested adequately. Additionally, geopolitical factors can create volatility in precious metals. Upcoming elections and possible international tensions should be monitored. While they may not immediately affect gold prices, they can trigger sharp reactions if risk sentiment changes. During such times, liquidity and leveraged positions can lead to unpredictable price behavior, impacting spreads and pricing during off-hours. It’s better to refine entry points rather than react impulsively. Indian gold prices reflect more than just global rates; local premiums, taxes, and spikes in consumer demand — especially during festivals or seasonal changes — should be taken into account. While these factors can offset broader trends, current seasonal demand isn’t strong enough to counter external pressures. Patience is key; wait for signs of stabilization or capitulation before adjusting your strategy. Recent data suggests we are in a phase where sentiment is shifting and expectations are adjusting, particularly among funds sensitive to interest rate changes. Therefore, it’s important to monitor sentiment indicators and shifts in open interest alongside price movements. This combination often provides earlier signals of change than price alone. Create your live VT Markets account and start trading now.The GBP/USD pair is rising, meeting initial resistance at the nine-day EMA of 1.3501.

Pound Stabilizes After Four-Week Low

The GBP/USD rose for the second consecutive day, trading close to 1.3500 during Asian hours on Friday. The pair showed a bullish trend, with the 14-day RSI above 50. However, it remained below the nine-day EMA, indicating weaker short-term momentum. On Thursday, GBP/USD bounced back above 1.3450 after a dip near 1.3400. This movement occurred as US markets paused for a holiday, easing some pressure on the US dollar. The Pound stabilized after hitting a four-week low of 1.3383, gaining strength following the Bank of England’s rate decision. Geopolitical uncertainties added pressure on the pair, while the US Dollar continued to rise. The BoE’s choice to keep rates unchanged, influenced by rising oil prices and tensions in the Middle East, reflects a weakening UK labor market. This raises concerns about potential rate cuts, keeping the financial landscape in focus. Sterling’s slight recovery, spurred by the Thanksgiving lull and reduced USD buying, doesn’t necessarily signal renewed optimism about the UK economy. It seems more like a temporary release of pressure due to thin liquidity and lower market participation rather than a solid bullish outlook. The Bank of England’s decision to maintain rates was not surprising, but the cautious tone caught attention. The divide among policymakers highlights worries about wage growth and slowing hiring trends, which are starting to affect monetary policy. Interestingly, the increase in GBP/USD happened despite no policy changes, showing how quickly sentiment can shift when market activity is low.Brent Highlights Inflation Expectations

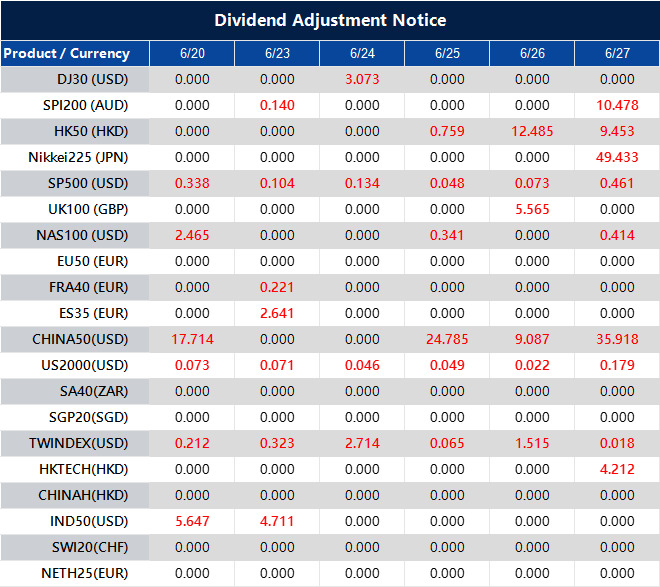

The RSI remaining above 50 suggests continuing demand, but the failure to break above short-term averages dampens enthusiasm. This scenario indicates that traders have a slightly positive outlook but lack strong commitment—momentum appears weak. In short, the appetite for trading is careful, not aggressive. Brent prices remaining high have drawn attention to inflation expectations again, particularly in the energy market. While this typically supports rate-sensitive pricing, the BoE’s caution suggests that inflation alone may not warrant rate hikes, especially with the labor market softening. This brings discussions about potential rate cuts into sharper focus as we approach year-end. With GBP/USD hovering around 1.3500, a solid trading range is forming between 1.3400 and 1.3550. Breaks outside this range could encourage bolder trading, but as things stand, rallies are struggling to gain traction. For those monitoring the derivatives market, implied volatilities can be quite useful here. The demand for downside protection hasn’t surged, indicating that market participants are not anticipating drastic changes—at least, not yet. Still, there’s a notable lean toward GBP puts, particularly for shorter-term contracts. Recently, the yield gap between UK gilts and US Treasuries has narrowed, but this lack of correlation shows that broad dollar sentiment is still a major driver. GBP/USD seems to react more to external flows than domestic data. Caution is advised not to overemphasize BoE narratives unless they diverge significantly from expectations. The geopolitical backdrop adds another layer of complexity. While oil’s influence on headline inflation is significant, it seems that risk appetite is becoming more reactive rather than anticipatory. Movements in GBP/USD that align with oil price shifts tend to be temporary, fading quickly as larger macro themes come back into play. In terms of positioning, there is no strong evidence yet of a fundamental shift in sentiment. Commitment of Traders data shows that large speculative accounts are holding balanced positions, reducing both long and short bets slightly. This suggests that major players are taking a wait-and-see approach. As we enter December, quieter trading periods can lead to exaggerated price movements. This uncertainty promotes a focus on gamma flows and event-driven swings, with expectations for ranges to hold unless a significant catalyst shifts sentiment. That catalyst could come from NFP reports, inflation data, or unexpected central bank comments. The strategy here may be to trade around clear levels, observe shifts in implied volatility, and avoid getting caught up in broader macro narratives that aren’t currently influencing price action. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 20 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Improved short-selling access in South Korea boosts chances for future market classification upgrades

MSCI has announced that South Korea’s short-selling situation has improved, easing concerns ahead of the upcoming market classification review.

Right now, MSCI categorizes South Korea as an emerging market, even though it meets many criteria for developed markets. There is hope that South Korea may soon appear on MSCI’s watch list for a potential upgrade.

In March, South Korea ended a five-year ban on short selling. This decision responded to worries from foreign investors and MSCI. During its annual review, MSCI moved South Korea’s short-selling status from “–” (improvements needed) to “+” (no major issues, improvements possible).

The main takeaway from the report is that the removal of long-standing short-selling restrictions has caught MSCI’s positive attention. Until recently, short selling had been partially banned, which many institutional observers viewed as a barrier to a freer market. This change aims to bring South Korea’s regulations in line with developed market standards and to address pressure from global index providers.

While the upgrade in short-selling metrics doesn’t mean everything is perfect, it indicates that the basic infrastructure and regulations are no longer problematic for international evaluators. The timing of this change before a broader market review increases the chances that Korean stocks could be viewed more favorably in a future index reassessment.

For those analyzing regional indices and their weightings, this shift changes the assumptions we use. The enhanced short-selling conditions suggest that any issues caused by regulatory interference are now less concerning. It also clarifies how market dynamics may function during periods of volatility, which is crucial for leveraged or paired strategies.

When MSCI makes changes like these, they signal to global investors that previous obstacles have lessened. This means that a market that was hard to hedge may soon become more accessible, affecting borrowing costs and the availability of counterparty agreements. This will flow into option pricing models, volatility expectations, and overall risk assessments.

With this reclassification, we can now evaluate Korean derivatives without worrying about artificial limits on downside risks. This will enable more refined execution in strategies such as arbitrage or sector rotation as liquidity conditions improve in the coming weeks. Market players who had previously held back due to these restrictions may start to re-enter the market, leading to more pronounced price movements around corporate earnings or economic reports.

Lee from the Financial Services Commission previously suggested that Korea aims to reform more than just regulations; they want to enhance both appearance and function. Now that this regulatory piece better aligns with what we expect from developed markets, derivatives traders should assess how trading patterns may adjust, especially in the tech and large-cap industrial sectors.

We need to keep a close eye on borrowing rates. If they start to narrow, it will further indicate that price discovery is becoming clearer. This, in turn, will enable better pricing for structured products and volatility exposures, particularly in monthly roll strategies.

Now is the time to recalibrate our exposure metrics for Korean assets across all model portfolios that hold derivatives on regional indices. If the market progresses toward MSCI’s upgrade path, we may see spikes in tracking errors between futures and the spot market as flows adjust to potential index shifts. This could impact both hedged positions and strategies that depend on short-term liquidity.

This is a valuable moment for regulatory clarity, allowing for proactive adjustments rather than waiting for widespread confirmation of changes to the watch list.