European stocks opened cautiously due to mixed performance among major indices amid uncertain trade talks.

European stocks started the day with caution due to slow-moving US-China trade talks in London. The major indices showed mixed results: Eurostoxx was down 0.2%, Germany’s DAX fell by 0.3%, and France’s CAC 40 dropped by 0.1%. The UK’s FTSE remained stable, while Spain’s IBEX increased slightly by 0.1%. Italy’s FTSE MIB decreased by 0.2%.

Traders are feeling cautious because there haven’t been many updates on the US-China negotiations. This uncertainty led to a mild decline in S&P 500 futures by 0.1%. Meanwhile, the dollar weakened across many currencies. The Australian dollar gained strength, with AUD/USD nearing the 0.6500 mark.

In summary, European stocks are trading carefully today. Investors are not jumping in quickly, mainly due to the ongoing, slow trade talks between the US and China in London. The lack of concrete outcomes makes people reluctant to make big moves in the markets, keeping the atmosphere restrained.

Looking at individual numbers, Germany and France show slight losses, while Spain has a tiny gain. The UK’s FTSE is flat. This cautious sentiment is also reflected in the US equity futures, which are gently dipping. The softness in S&P 500 futures indicates that traders prefer to manage their risks carefully. The dollar has weakened slightly against most currencies, whereas the Australian dollar is climbing and may test higher against the US dollar soon.

Next week, the unclear direction from Washington and Beijing might continue this slow movement in the markets. For those working with options and futures, now isn’t the time for wild guesses. Geopolitical uncertainty takes time to resolve, and volatility pricing is currently low—like the VIX, which hasn’t spiked. This means many traders are holding back instead of hedging aggressively.

Even if the slow movement in implied volatility looks tempting, it’s wise to avoid too much short gamma unless you’re sure about your entry points. Spreads in the major indices are tight for now but might widen if any significant news arises. Keep an eye on the premiums leading up to next Thursday’s expiries. If you need to make directional bets, doing so gradually is safer than making large investments at once.

The dollar’s weakness has given pairs like AUD/USD a solid base. As the Australian dollar approaches 0.6500, we need to watch key resistance levels closely. A breakout above this range, supported by stronger commodity or data signals, could result in moderate moves in options gamma. Generally, carry trades aren’t appealing right now, so unless there’s more confirmation from rates or equities, any upside may be limited to intraday spikes.

The energy sector is also worth noting. Recent crude inventory draws haven’t changed the overall sentiment, but expectations for seasonal demand could create a stronger foundation for related contracts. We’re keeping an eye on the commodity market since it influences volatility and broader inflation expectations, especially for inflation-sensitive options.

In the coming days, patience is key. Traders should avoid rushing into uncertain outcomes. Use the information that’s available—especially earnings revisions, inflation surprises, and rate cues—before making directional trades or straddles that require movement. Delta-neutral strategies may seem attractive during this waiting period, but unless there are clear signs of rebalancing or institutional positioning, there’s no rush. It’s better to focus on preserving capital while the market remains compressed. That’s the sensible strategy for this week.

A new Boeing 737 MAX has arrived in China, marking the resumption of deliveries as US-China trade tensions ease.

A Boeing 737 MAX has arrived in China, marking a positive shift in US-China trade relations. Previously, Boeing had halted deliveries to China in April due to rising tensions.

In May, Boeing announced it would begin deliveries again in June after the US and China temporarily reduced tariffs. This break from tariffs will last for 90 days, indicating progress between the two countries.

Impact of Tariff Easing

The arrival of this Boeing 737 MAX represents more than just one plane crossing a border. Its landing in China shows that the reduced tariffs between the US and China are having a real impact. Boeing’s decision in May to restart deliveries hinged on this 90-day tariff agreement. This pause is already showing positive results, especially in logistics. This development suggests a decrease in risk premiums for manufacturers heavily involved in international trade, particularly in aerospace and defense. It removes short-term uncertainty, which is important for markets. Prices had already begun to reflect a potential easing, and the confirmation through this delivery supports further short-term strategies. Investors should note that this isn’t just about one aircraft—it’s a sign of broader changes. The pause in tariffs reconfigures some hedging behaviors, especially for those tracking industrials or global exporters. With fewer obstacles at ports, some American manufacturers might report better revenue in the third quarter. Markets that depend on accuracy are likely to recognize this trend.Market Responses and Opportunities

Calhoun’s quick move to capitalize on this opportunity shows how manufacturers are eager to push through deliveries before policies could tighten again. This impacts those trading options on these companies, affecting their assumptions about implied volatility. The fixed income market may also reflect improved corporate yield curves in sectors benefiting from smoother trade. Looking at the 90-day tariff reprieve, it might seem short for corporate planning, but it’s still enough time for trading strategies linked to freight volumes, export data, or quarterly earnings. Timing is key here. We are already seeing adjustments in futures related to transportation and aerospace sectors. As companies navigate these tariff-free months, price discovery becomes more predictable, allowing for better management of risk compared to April when deliveries were stalled. However, it’s important to remember that this rhythm could change. For hedging, it makes sense to remain cautious towards the end of the calendar. The immediate future should be approached actively. Keep an eye on the 30- to 60-day time frames for both technical support levels and signs of increased shipping activity. This delivery has opened a door, but its width will depend on factors beyond market control. Current price actions suggest that engaging in the market is reasonable. When trading volumes increase, liquidity often improves, allowing for better planning. Create your live VT Markets account and start trading now.The upcoming week looks quiet, with important economic data releases from Australia, the U.K., and the U.S.

A quieter week is coming up after the NFP release, with Monday a public holiday in many European countries for Whit Monday.

On Tuesday, Australia will share the Westpac consumer sentiment index, while the UK will release data on average earnings index (3m/y), claimant count change, and unemployment rate.

Wednesday will concentrate on U.S. inflation data, and on Thursday, the UK will report its monthly GDP m/m. The U.S. will present the PPI m/m along with weekly unemployment claims.

On Friday, we’ll see the early University of Michigan (UoM) consumer sentiment and UoM inflation expectations.

Australia’s previous Westpac consumer sentiment rose by 2.2%. Recent events include a 25 bps rate cut by the RBA and disappointing Q1 national accounts, indicating economic challenges.

In the UK, the average earnings index (3m/y) is expected at 5.3%. The claimant count change is forecasted at 9.5K, with the unemployment rate at 4.6%.

For the U.S., the core CPI m/m is projected to be 0.3%, up from 0.2% last month. The CPI y/y is anticipated to rise from 2.3% to 2.5%.

This data will shed light on the effect of tariffs on consumer prices, especially on core goods.

The U.S. core PPI m/m is estimated at 0.3%, with the overall PPI m/m at 0.2%. The recent drop in headline PPI hints at hidden inflation pressures due to tariffs.

Looking ahead, this week’s lighter economic calendar will help clarify trends in rates and inflation after last week’s non-farm payrolls. With many European nations observing Whit Monday on Monday, we can expect lower trading volumes early in the week. This might lead to choppy trading before macro events pick up from Tuesday.

Australia’s consumer sentiment figures on Tuesday will provide insight into the public’s willingness to spend amid slowing growth. After a 2.2% increase last month, the response to weak Q1 data and the RBA’s recent quarter-point cut will be crucial. It’s more about trend shifts than absolute numbers. A negative result after last month’s rise would signal fading confidence and support a dovish stance from the RBA. If the figure falls below expectations, watch for lower yields on Aussie front-end rates.

UK labor data on Tuesday may influence the British pound and front-end gilt pricing. With earnings projected at 5.3% and unemployment at 4.6%, this may favor hawks. However, if real pay continues outpacing inflation, the Bank of England’s hiking plans could face scrutiny. If claimant numbers exceed the predicted 9,500, it may suggest a loosening job market, which could deter further tightening. In this scenario, expectations for rate hikes may weaken, especially if GDP falls short on Thursday.

Wednesday’s U.S. CPI numbers will be significant. With a predicted core inflation of 0.3% m/m and a year-on-year estimate of 2.5%, we’re seeing renewed concerns about core price stability. Last month’s number was 0.2%, so this small change will draw attention. The market will be particularly alert to categories affected by tariffs, like apparel and household goods. We shouldn’t expect widespread disinflation yet, especially with geopolitical risks affecting supply chains. Collectively, we’ll watch not just the final number but also how sticky these inputs seem—especially if service inflation picks up.

Thursday’s dual reports on U.S. PPI and weekly jobless claims will further illuminate the inflation landscape. A core PPI of 0.3% would align with CPI momentum. If both show upward risks, it could delay Fed rate cuts. Earlier, a drop in headline PPI led to assumptions of soft underlying inflation, but revised prices and freight costs may challenge that view. A print at or above expectations could boost support for longer-term Treasury yields.

Friday will conclude with initial figures from the University of Michigan, providing insights into sentiment and inflation expectations. These softer indicators are increasingly relevant as hard data shows decreasing momentum. Long-term inflation expectations have risen in recent quarters. If that trend continues, markets may need to rethink how anchored those expectations are. A surprising rise in expectations wouldn’t just reinforce core inflation persistence but could also reignite concerns about stagflation risks.

Traders using options and volatility products should remain agile. A complacent stance on macro volatility could quickly backfire if any indicators deviate from expectations. As we prepare for these key releases, especially the inflation data, a responsive approach might be more effective. We’ll compare expectations with actual results to evaluate adjustments in short-term rate curves. Holding a firm bias appears increasingly risky unless positioning is tight.

The USDJPY pair remains range-bound, with upcoming economic events likely to impact market direction soon.

The USDJPY pair is currently fluctuating as traders evaluate mixed signals while waiting for more data to provide guidance.

The US Dollar lost gains after a robust jobs report, despite rising Treasury yields on increased wage growth. Upcoming significant events, including US-China trade talks, the US CPI release, and the FOMC’s decision, are expected to impact the Dollar’s trajectory. For the Dollar to gain strength, it needs more bullish factors.

Meanwhile, the Japanese Yen is weakening due to the Bank of Japan’s (BoJ) reduction in bond buying. The central bank is looking for updates on US-Japan trade negotiations and inflation trends.

Daily Chart Analysis

On the daily chart, USDJPY is trading between 142.35 and 146.00. Buyers are targeting the resistance at 148.32, while sellers are looking to push below 142.35 towards 140.00. The 4-hour chart shows support at 144.32. Buyers hope for a rise to 146.28, whereas sellers are eyeing a dip to 142.35. The 1-hour chart does not add new information, as longer trends dominate. Key upcoming events to watch include US-China trade talks, US CPI, US Jobless Claims, US PPI, and the University of Michigan Consumer Sentiment report. Today’s analysis of the USDJPY exchange rate indicates a state of indecision among traders. Short-term movements have not convinced either buyers or sellers. There was a brief rally in the Dollar after strong non-farm payroll (NFP) data, but those gains quickly faded. Although Treasury yields rose in response to strong wage growth, the Dollar’s overall strength could not be maintained. This suggests that interest rate expectations may not be enough to support the Dollar right now. Fed Chair Powell and other officials seem hesitant to provide new support for the Dollar without reliable data to guide them. Current inflation reports, like the US Consumer Price Index (CPI) and Producer Price Index (PPI), are particularly significant. Any unexpected rise in these figures, especially in housing and services, could push rate shift expectations further out. Interest in US-China trade updates may influence overall market sentiment more than actual trade dynamics, but they could still prompt short bursts of momentum. Kuroda’s cautious decision to ease back on bond tapering has weakened the Yen, indicating Tokyo prefers to avoid tightening amidst uncertain inflation trends. With uneven wage growth and inconsistent inflation in Japan, the central bank feels no immediate pressure to change its approach. This leaves the Yen open to responses from external events rather than internal strength. Markets are watching both inflation data and US-Japan discussions closely. Progress or delays in those areas are likely to have quick effects on prices.Technical Insights and Market Outlook

The daily chart shows a strong range between 142.35 and 146.00, indicating a lack of strong conviction from either side. Buyers are focusing on the 148.32 level, but they face uncertainty below 146.00. On the flip side, sellers will likely ramp up their efforts if 142.35 is breached, possibly targeting 140.00. A clear breakout in either direction could lead to swift price changes, given the time spent in this range. The 4-hour chart supports this view: 144.32 is currently a support level, with potential upside if buyers enter with enough strength. However, for a sustained move up, the price must exceed 146.28. Conversely, sellers are prepared to challenge lower levels, with a move down to 142.35 on the radar. A failure to hold above this level could lead to a return of Yen strength, at least temporarily. In shorter timeframes, like the 1-hour chart, the overall pattern remains unchanged—no drastic changes or surprises, just ongoing indecision. This typically occurs before significant economic data releases, resulting in tighter positioning and reduced liquidity. In the coming week, it’s crucial to monitor the timing and results of US economic releases. We should pay special attention to how inflation data aligns with consumer sentiment. The Michigan report could notably influence expectations about consumer demand. If sentiment starts to diverge from inflation trends, it might indicate deeper issues in growth expectations. Additionally, changes in initial jobless claims could highlight weaknesses in the US labor market—a metric closely watched by policymakers. From our perspective, it’s essential to be ready to act rather than react. The time for impulse trades may not be here yet. Instead, let’s stay focused on key price levels and remain patient until broader direction becomes clear through policy updates or data confirmation. Create your live VT Markets account and start trading now.Citigroup predicts 75 basis points of cuts this year and raises S&P 500 target to 6,300 from 5,800.

Citigroup expects the Federal Reserve to cut interest rates by 75 basis points this year. They predict three cuts of 25 basis points each in September, October, and December.

This forecast differs from market expectations. Currently, the market anticipates only about 46 basis points of cuts by the end of the year and no reductions during the summer. Citigroup’s view is shaped by the insights from the recent US jobs report.

In early 2026, Citigroup expects two more cuts of 25 basis points each. Additionally, they have raised their year-end target for the S&P 500 to 6,300, up from the previous forecast of 5,800.

The article highlights the growing gap between Citigroup’s predictions on US interest rates and what traders are pricing in. Citigroup believes rates will start to drop in September, totaling a 75 basis point reduction by year-end. In contrast, futures markets suggest only a modest decline of around 46 basis points by January.

This change in outlook follows a strong jobs report from the U.S. While the numbers appear solid, they might indicate a slowdown rather than an overheating economy. Slight declines in wage growth and labor participation could be driving this shift. We’ve seen similar nuances affect rate expectations in the past, where overall strong figures can hide more delicate changes beneath the surface.

Moreover, the upward revision of the S&P 500 target supports this forecast. The increase from 5,800 to 6,300 implies confidence in the market and suggests that inflation risks may be easing. This provides the Federal Reserve with space to support economic growth instead of tightening conditions.

Looking ahead to early 2026, Citigroup has penciled in two more rate cuts. This would raise the total decline since September 2024 to 125 basis points. If more institutions align with this outlook or if key data corroborates it, futures pricing might adjust accordingly. Until then, the disconnect between these forecasts and market beliefs creates short-term opportunities, especially in forward rate agreements or options on short-term rates.

From a strategic perspective, when a major bank outlines a series of rate cuts that contrast with common beliefs—and supports this with higher equity market predictions—it signals confidence in decreasing inflation without triggering volatility.

In the coming weeks, pay attention to rate-sensitive instruments like SOFR or Eurodollar futures. Watch for shifts in steepness between late-2024 and mid-2026 contracts. If others begin to embrace the idea of earlier policy changes, it could lead to realignment. This focuses on timing rather than direction, where convexity-based products may offer better entry points.

Even as various macro indicators like CPI, core PCE, and initial claims data emerge, the key task is to compare expectations with actual pricing. It is this gap that presents clear opportunities, especially if one thinks that final policy levels will stabilize lower—and sooner—than what most anticipate.

Today’s agenda has no data releases and instead focuses on anticipated positive US-China trade talks in London.

Today has no scheduled data releases, but the focus is on US-China trade talks happening in London. Comments from Friday suggested that there might be optimism about these discussions, hinting that reductions in tariffs could soon be announced to encourage further negotiations.

If any announcements are made, they could affect the markets, so it’s important to stay updated. Any news could lead to market shifts.

Traders Should Note

Traders should remember that although there are no economic reports planned for today, many are closely watching the ongoing diplomatic talks. These meetings in London are gaining attention due to remarks made late last week. Sources familiar with the discussions believe that an agreement on reducing tariffs might be in the works, possibly in stages. If confirmed, lower trade barriers could significantly impact sectors related to international trade and supply chains, especially those sensitive to cost changes and shipping expenses. With updates likely throughout the day, there’s a higher chance of market volatility, especially in markets with high open interest and narrow spreads. Our strategy is to stay flexible and ready. We expect that any clear signs of tariff changes could drive movements in currency pairs and indices heavily involved in exports. Keep an eye on implied volatility to avoid getting caught in mispriced options. We also suggest not becoming too heavily invested in positions that depend on short-term stability. Currently, there seems to be little distracting the broader macroeconomic scene, which could make the outcome of these talks even more impactful. In this climate, even a small policy change could quickly alter pricing expectations.Positioning Standpoint

From a positioning standpoint, traders might find value in horizontal structures. Given the unpredictable nature of these talks and the uncertain timing of any resolution, using time spreads or gradually moving into verticals can help manage exposure without chasing reactive movements. We are carefully monitoring how correlations between different asset classes are changing, especially between stocks and the Treasury market. The rate market hasn’t shifted significantly, suggesting that equity and commodity derivatives may respond first if an official statement comes out. Historically, leaks or unofficial briefings often come before formal announcements. This is common and can lead to market adjustments before confirmation. Watching for spikes in trading volume and price fluctuations during off-hours can help identify credible emerging signals. In summary, although today doesn’t have scheduled data events, its significance shouldn’t be overlooked. We believe that being prepared—without overreacting—is crucial in the upcoming sessions. Create your live VT Markets account and start trading now.Week Ahead: Trade Tensions Take Centre Stage

Markets opened the week with cautious optimism following a strong finish the previous Friday. Investors were still digesting an encouraging US employment report, which revealed 139,000 jobs were added in May, comfortably exceeding the forecast of 125,000.

That headline figure helped lift equities to fresh highs, with the S&P 500 closing above the 6,000 mark. However, deeper inspection revealed a softer backdrop: revisions to past data resulted in a net decrease of 95,000 jobs over the previous two months, suggesting that while job creation continues, the pace may be moderating.

Wage data added complexity to the picture. Average hourly earnings rose by 0.4% on the month and 3.9% year-on-year, indicating that workers’ purchasing power remains ahead of inflation for the time being. This supports consumer spending and points to ongoing resilience in retail sectors as summer approaches. Still, questions remain over whether this can be sustained if uncertainty over trade policy begins to dent business sentiment.

Inflation, for now, remains contained. Headline CPI holds steady at 2.3% year-on-year, the lowest reading since early 2021, while core inflation has eased to 2.8%. These figures are within touching distance of the Federal Reserve’s 2% target, suggesting that pricing pressures are manageable for now. Crucially, neither wage gains nor tariffs have yet fuelled a fresh inflationary spike, though that balance may yet be tested.

Fed Remains Cautious

One reason inflation may appear subdued is the way businesses have front-loaded imports ahead of anticipated tariff increases. This strategy has bolstered inventories and helped cushion price pressures, but it could simply be postponing the real inflationary impact. Markets are alert to this possibility.

The Federal Reserve has so far resisted political pressure to act. Despite President Trump’s calls for a sharp 100 basis point cut, the Fed is standing pat. With unemployment low and inflation moderate, there is little case for immediate policy easing.

CME FedWatch data shows no chance of a rate cut at the upcoming June 17 – 18 FOMC meeting. Markets instead anticipate the first cut in September, potentially followed by a second before year-end, but only if the data warrants it.

This deliberate stance reflects the balancing act facing the Fed. Move too early and credibility is at risk; act too late and economic headwinds, such as tariffs, may bite harder. For now, the Fed remains guided by macroeconomic fundamentals rather than political demands.

Trade Tensions Take the Spotlight

Trade policy continues to loom large as the most significant potential catalyst for volatility. President Trump’s announcement that US – China trade discussions will resume in London brought brief relief to markets. Equities rallied on hopes for diplomatic progress, though companies remain hesitant. Many major firms have delayed investment and hiring decisions as they await clarity on tariff measures, a caution that may soon appear in earnings outlooks and capital expenditure data.

Markets find themselves in a delicate balance. Positive employment figures and subdued inflation offer support, but any misstep in trade negotiations could quickly undermine that stability. On 6 June, both the Dow and Nasdaq gained more than 1%, fuelled by the strong jobs print. Yet the rally could quickly reverse if talks stall or if inflation surprises to the upside once stockpiled goods give way to tariff-inflated costs.

Bond markets reflect this tension. Yields have ticked higher following the employment surprise, but softer data could see them retrace. The interplay between expectations for Fed policy and trade risks will continue to shape fixed income flows.

Prudence is prevailing. Traders are approaching mid-2025 with a mix of restraint and readiness. Should trade talks yield progress and inflation stay controlled, the argument for a rate cut later this year remains valid. However, if discussions falter and inventories shrink, consumers may begin to feel the pressure, forcing a repricing of risk across the board.

Market Movements This Week

In light of recent data and the Fed’s current stance, price action is being approached with a balanced perspective. While sentiment retains a cautiously positive tilt, several major markets are approaching key inflexion points.

The U.S. Dollar Index (USDX) climbed just above the 98.00 zone we’ve been monitoring. At this juncture, price appears poised to either consolidate near-term before pulling back, or continue higher into the 99.80–100.50 region. That next range becomes critical. Price action there will determine whether we’re shaping a broader bullish continuation pattern or setting up for a medium-term reversal. With the Fed holding steady and inflation in check, the dollar is trading more on positioning and global demand for safety than on yield dynamics alone.

EURUSD has slipped just below the 1.1520 zone, with 1.13564 now the key support. A break below may trigger broader downside, while a bounce could signal consolidation. We’re watching closely for structure confirmation at this level, maintaining a neutral stance until direction resolves.

GBPUSD sits just below 1.3600, with attention on 1.3460 and 1.3440 as key support levels. A break lower could trigger a broader correction, while a bounce may signal consolidation. With the dollar firm and risk sentiment cautious, we remain neutral-to-bearish until a clearer structure emerges at these thresholds.

USDJPY has been grinding higher, forming what could be a larger consolidation on the weekly scale. We are eyeing the 145.75 and 146.60 levels next. A rejection at either zone, with clear bearish structure, could offer a cleaner short-side play. However, the yen remains the weakest major currency structurally, and unless yields fall sharply, further upside is not off the table.

USDCHF also continues to lean into a consolidation phase. Our eyes are on the 0.8275 zone for signs of bearish exhaustion. If momentum stalls there and structure turns, we may see short setups develop, though the Swiss franc remains fundamentally driven by safe-haven flows, especially during tariff flare-ups.

AUDUSD and NZDUSD both printed new swing highs recently but have pulled back. For AUDUSD, 0.6460 becomes the pivot for any bullish setups. For NZDUSD, we’ll look to 0.5960. Both pairs are still largely tracking broader risk appetite and commodity sentiment. Watch copper and oil as secondary indicators.

USDCAD remains in a broader up-channel structure. If price consolidates into the 1.3750–1.3780 zone and fails to break higher, we will consider bearish opportunities. Crude oil stability could also cap further CAD weakness.

Speaking of oil, USOIL has finally begun to lift, but we remain cautious. The current move may be part of a larger consolidation. The 66.10 level is key. If price rejects there, we may see another corrective leg lower before more stable directional movement resumes. The market remains highly sensitive to geopolitical supply disruptions and trade-related demand forecasts.

Gold has been less convincing. Price failed to hold higher levels and has now revisited 3310. We anticipate a consolidation phase, with potential bearish setups at 3340. On a downward move, we are watching 3295 and 3265 for bullish price action support. Gold’s behaviour continues to reflect a lack of fear. There is no flight to safety just yet.

The S&P 500, on the other hand, continues its upward momentum. As we move higher, the 6100 level becomes the next key area. Reaction there will determine if the breakout holds or stalls. We approach this zone with caution given stretched sentiment and headline-driven volatility.

Bitcoin tested the 99,600 area and may now consolidate before attempting a move toward 107,550. Crypto markets remain highly reactive to risk appetite, regulatory headlines, and liquidity conditions. For now, structure remains bullish, but stretched.

Natural gas (Nat Gas) is showing upward momentum, but we expect resistance at 3.60. A clean bearish pattern at that level would mark a possible swing short opportunity.

As always, we monitor price zones for confirmation. Structure must align before entry. With macro sentiment holding firm but risks rising, it’s the reaction, not the forecast, that defines the trade.

Key Events This Week

Attention turns sharply to the US CPI report on Wednesday, June 11. Forecasts point to a year-on-year headline inflation rate of 2.5%, up from the prior 2.3%. A hotter-than-expected print could reignite concerns that the recent cooling in inflation may be stalling. That would likely push back expectations for a September rate cut and may firm the US dollar while weighing on risk assets. Conversely, a softer number would reinforce the recent disinflation narrative, potentially boosting equities and high-beta currencies.

On Thursday, June 12, the macro spotlight shifts to the UK and the US simultaneously. The UK GDP month-on-month figure is projected at -0.1%, down from the previous 0.2%. A downside print may weigh further on sterling, particularly if paired with risk aversion or dollar strength. Meanwhile, the US PPI is forecast at 0.2%, rebounding from last month’s -0.5%. This release will be closely watched for early signs of producer-level cost pressures feeding into consumer prices, especially in light of tariff implications.

Friday, June 13, rounds out the week with the University of Michigan Consumer Sentiment reading, forecast at 52.5 versus 52.2 previously. Though a secondary-tier release, sentiment data will offer insight into whether higher wage growth is translating into consumer confidence, or if political and trade concerns are beginning to weigh on expectations.

Create your live VT Markets account and start trading now.

In early European trading, Eurostoxx and German DAX futures fell, while UK FTSE futures gained slightly.

Eurostoxx futures dropped by 0.1% during early European trading as caution builds before US-China trade talks. German DAX futures also fell by 0.1%, while UK FTSE futures saw a small rise of 0.1%.

These market changes follow last week’s gains, and there was positive sentiment on Wall Street last Friday. The focus is now on the US-China negotiations in London, but the timing for these talks is still unknown. Recently, China made a goodwill gesture, which many see as a positive sign before the discussions, though a compromise is still uncertain.

Traders are being careful ahead of the US negotiations with the Chinese delegation, leading to a subdued market tone. Futures are moving sideways, volatility is decreasing, and risk appetite is low. This contrasts with the more optimistic trading seen last Friday in the US.

We are noticing a slight pullback in continental indices after last week’s rally, which was driven by strong earnings and data suggesting resilient consumer demand and housing. The small decline in Eurostoxx and German contracts indicates that much of the recent optimism is already factored into the market. Without new catalysts, a retracement is expected.

Beijing’s goodwill gesture has been acknowledged, but the uncertainty around negotiations remains. With the talks moving to London, the lack of a clear agenda or timeline is causing many participants to hold back. Ignoring the talks entirely would be a mistake. Traders involved with cyclical stocks linked to industrial demand and export flows are keeping their positions light or hedged, waiting for more clarity from the discussions.

This sentiment is reflected in options data: implied volatility for shorter-term contracts is easing, indicating no strong expectations for sudden market shocks in the near term. For directional trading strategies, momentum is unlikely to last without macro developments beyond the current diplomatic situation.

In the UK, the small rise in futures can be attributed to some positive earnings surprises and relief from currency movements. A weaker pound has slightly helped multinational companies’ revenue prospects, even amid overall geopolitical caution. However, traders with positions sensitive to the pound should keep an eye on Bank of England comments, especially as inflation data is released.

Chancellor Scholz’s government hasn’t indicated any major policy changes that could significantly affect risk profiles. Recent economic surveys reveal a slow recovery in German manufacturing, leading some traders to reduce leverage or focus on spreads between sectors showing stronger earnings momentum, like tech and healthcare, compared to industrials.

From a derivatives perspective, the current market suggests a preference for lateral movement rather than sudden breakouts. This environment favors traders who rotate between delta-neutral structures and shorter gamma exposure across correlated indices. Sticking with liquid assets can help lower execution risks in the current market mood. It’s wise to be cautious but not overly paralyzed—this is a practical approach for now.

In May, Japan’s economy watchers index increased to 44.4, boosted by better household retail activity.

Japan’s economy watchers’ survey index for May was 44.4, an improvement from April’s 42.6. This slight increase reflects a better outlook among households and more retail activity.

However, business trends declined, affected by changes in the manufacturing sector. On a positive note, the outlook for employment improved, with the index rising to 44.8 from April’s 42.7.

Consumer Sentiment And Business Confidence

The data indicates a slight boost in consumer mood on the high street and some growth in household spending, yet businesses, especially in manufacturing, feel uncertain. The diffusion index, which shows the percentage of respondents seeing better conditions, rose as consumers became more active, likely due to warmer weather and promotions attracting more shoppers. Nonetheless, production sectors face challenges tied to supply chain issues and shifts in global demand. Factory orders and export sentiment are weaker than expected, possibly leading to lower capital spending and hesitance in hiring in the coming months. The increase in the outlook index suggests people feel more secure in their jobs or see a slight improvement in job opportunities. This is often a lagging indicator; it doesn’t always lead to increased consumer spending, but it could indicate less hesitation in household spending if the trend continues. For traders focusing on volatility, this information could influence expectations around domestic demand and impact the yen’s value as more data becomes available.Market Dynamics And Strategic Adjustments

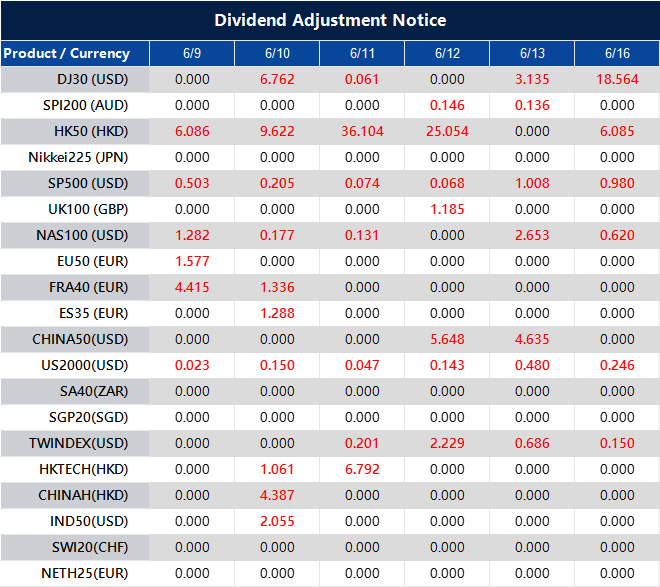

We see opportunities for relative value plays since short-term consumer resilience might not align with medium-term business caution. If retail data continues to strengthen without a similar rise in industrial output, the gap between consumption-focused investments and industrial ones could grow. This divergence is particularly important during the low-summer months when minor news can cause significant market movements. As market participants, we should view these indices not as definitive signals but as pieces of a broader picture that includes monetary policy, inflation trends, and local dynamics. With the Bank of Japan maintaining a unique position compared to other central banks, a sustained gap between employment expectations and manufacturing caution could open opportunities for adjusted hedging in interest-sensitive structures. Instead of making strong positions based solely on current sentiment, the data suggest better results by shifting focus to consumption-heavy sectors using short-term instruments while staying cautious on industrials until clearer signs of recovery appear. Balancing this with volatility metrics, which continue to lag behind actual moves, might allow for lower-cost entries into convexity trades within regional equity options. Throughout this period, household-led improvements are likely to fade faster than corporate recoveries solidify. We could analyze this gap by comparing small-cap performance to exporters or looking at upcoming inflation forecasts. The key lies not in the headline figures, but in how consistently consumer spending outpaces business sentiment through early summer. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 09 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].