Halifax reports a monthly decline in house prices, showing stability despite affordability challenges and interest rate uncertainties.

Data from Halifax, released on June 6, 2025, shows that UK house prices dropped by 0.4% in May. This was more than the expected 0.1% decrease. In April, prices actually rose by 0.4%.

Over the past year, house prices grew by 2.5%. This is lower than the expected 2.9% and down from a 3.2% increase. These slight monthly changes indicate a stable housing market, even though there’s been a small 0.2% decline in average prices since the start of the year.

FX options set to expire include various currency pairs with amounts tied to price levels.

The FX option expiries for June 6 at 10 AM New York time involve several currency pairs with specific amounts set to expire.

For EUR/USD, the expiries are:

– 1.1500 with EUR 3.19 billion

– 1.1400 with EUR 2.38 billion

– 1.1300 with EUR 1.28 billion

For USD/JPY, expiries are noted at:

– 146.00 for US$ 1.35 billion

– 142.00 for US$ 2.08 billion

GBP/USD shows:

– 1.3600 with GBP 413 million

– 1.3410 with GBP 896 million

In USD/CHF, expiries are at:

– 0.8300 for CHF 415 million

– 0.8250 for CHF 470 million

For USD/CAD, the amounts are:

– US$ 1.11 billion at 1.4040

– US$ 1.13 billion at 1.3600

AUD/USD has an expiry at:

– 0.6300 with AUD 1.64 billion

Finally, NZD/USD is at:

– 0.5590 with NZD 766 million

This data highlights upcoming foreign exchange option expiries, specifically showing prices related to significant open interest that will mature on June 6 at 10:00 AM New York time. Essentially, these are levels in different currency pairs where large sums of options contracts are set to expire. The expiry moment is crucial as it can keep the spot price—current trading level—close to these strike prices as traders adjust their positions.

For instance, in the EUR/USD pair, there are three key levels with many contracts ending: 1.1500, 1.1400, and 1.1300. The largest amount is at 1.1500, with over €3 billion associated with it. These amounts can attract price action as the expiry nears. While it’s not a strict rule, past experiences suggest this behavior tends to occur. This means that if the spot rate approaches a significant expiry level with high volume, the momentum might slow down or change direction temporarily.

In the USD/JPY pair, there are expiries of over $2 billion at 142.00, with another significant amount at 146.00. The distribution is uneven, with more emphasis on 142.00. This indicates that traders might prefer keeping prices around that area. Although it doesn’t guarantee the spot price will land exactly there, it does suggest less volatility just above or below these levels.

For GBP/USD, the largest expiry is found at 1.3410, with nearly £900 million. The next expiry is higher but smaller, suggesting any price movement would likely focus around 1.3410. Traders might adjust their positions to keep options settling in a favorable manner.

In USD/CHF, both 0.8300 and 0.8250 show expiring volumes, with a slightly larger amount at 0.8250. While these figures aren’t massive, they can affect short-term trends, especially in markets with lower trading volume.

In USD/CAD, there are two notable strikes—1.4040 and 1.3600—each having sizable dollar amounts. Their separation implies less pull towards either strike, leading to a wider price range and less direct movement.

The Australian dollar has an expiry at 0.6300, which, though moderate in size, could still influence market movements, especially if momentum aligns with this level.

For NZD/USD, the expiry at 0.5590 shows just over NZD 750 million. While smaller than others, it can still impact trading during quieter hours or sessions.

Considering all this, expiry zones act as short-term pressure points. They can either slow down or redirect price, particularly just before the options cut. It’s useful to watch if the price approaches these levels during the London or early New York sessions, allowing traders to capitalize on market flows.

Being reactive isn’t always effective. It’s usually better to wait and strategically outline risks around these levels. Large expiries don’t always cause immediate price changes, but they reveal what other traders might be monitoring.

This type of data doesn’t predict future movements but identifies areas where market behavior might change temporarily due to mechanical factors. Knowing where expiry clusters are helps manage entry and exit strategies more effectively, minimizing surprises during these periods—an insight gained through practical experience.

Japan’s April leading economic index misses expectations due to trade uncertainty and inflation concerns

Japan’s leading economic index for April was 103.4, missing the expected 104.1. The Japan Cabinet Office shared this information on June 6, 2025. The earlier number of 108.1 has been revised down to 107.6.

The coincident index recorded 115.5, a slight decrease from the previous 115.9, which was revised to 115.8. This drop in the leading index reflects ongoing trade uncertainties. The Bank of Japan is keeping a close watch on trade talks and inflation before deciding on interest rate changes.

Economic Indicators Overview

The leading economic index helps us predict Japan’s economic trend over the next few months. A drop to 103.4, below the anticipated 104.1, suggests potential economic weakness ahead. The previously reported figure of 108.1 was revised down to 107.6, reinforcing the idea that optimism may have been too high. The coincident index shows the current state of the economy. It decreased slightly to 115.5 from a revised 115.8. Although this is just a small decline, it indicates that recent economic performance may be slowing. When both leading and coincident indicators drop at the same time, it often signals a cooling momentum. We should remember that the Bank of Japan’s policy decisions are influenced by how inflation behaves and the progress of trade discussions. The latest figures suggest there will not be quick changes in interest rates. Policymakers are taking their time, and that’s the right approach.Market Implications and Outlook

This weaker data from Japan suggests a cautious approach for investors. The lower-than-expected leading index reading may prompt revisions in interest rate exposure. Historically, when indicators dip early in a tightening cycle, yield curves tend to shift lower. Therefore, we should approach changes in interest-rate differentials with caution. In the coming weeks, markets will determine whether this soft data is a temporary blip or the start of a deeper slowdown. For now, we prefer to pay close attention to sentiment from Tokyo instead of chasing uncertain trends. The messaging from the central bank will likely be more influential than any new data. It’s important to note that recent adjustments are not just numbers—they also indicate delays. Revisions—like from 108.1 to 107.6—affect our baseline. While these changes may not grab headlines, they influence expectations, particularly in yen-related carry trades. We don’t anticipate chaos, but we are closely monitoring forward rates and risk premiums. The drop in these indices will likely keep a check on any aggressive re-pricing. Current spreads are telling their own story, indicating no expectation of sharp shifts. Overall, local rates and FX valuations are unlikely to change drastically unless a surprising new indicator emerges. Practically, this means we should adopt defensive hedges and avoid excessive exposure ahead of the Bank of Japan’s next meeting. Right now, we are more focused on how volatility markets are adjusting rather than on price movements. The price action might lag behind signals but not by much. Create your live VT Markets account and start trading now.European session has low-tier data, while the US may show important employment figures and trends.

In the European session, only a few minor data releases are expected, such as industrial production figures from Germany and France, along with Eurozone retail sales. These numbers are not likely to impact market pricing significantly.

Moving to the American session, important labor market reports will be released. Canada is predicted to report a decline of -12.5K jobs, a shift from the previous gain of 7.4K, with the unemployment rate increasing to 7.0% from 6.9%.

The Bank of Canada recently kept interest rates the same, opting to wait for more information regarding trade and inflation. Currently, a reduction of 31 basis points is forecasted by the end of the year, with potential cuts expected to start in the last quarter of 2025.

For the US, the non-farm payroll report is expected to show an addition of 130K jobs in May, down from 177K in April, while the unemployment rate is expected to remain stable at 4.2%. Average Hourly Earnings Year-over-Year is forecasted at 3.7%, a slight drop from 3.8%, but the Month-over-Month figure is expected to rise to 0.3% from 0.2%.

Data from the labor market indicates a slowdown in hiring attributed to tariff issues, but this is not severe enough to motivate rate cuts by the Federal Reserve. The market currently anticipates a reduction of 54 basis points by the end of the year, with the first cut likely in September. If upcoming data is positive, the Fed may have fewer reasons to cut rates, which would change market expectations.

The figures from Germany, France, and the Eurozone can help gauge trends in consumption and manufacturing activity, yet they are unlikely to cause significant shifts in market positions in the short term. These are lagging indicators. While they help economists build a clearer picture, traders often receive them too late to react effectively. Most of the market’s moves have already happened by the time these reports arrive.

Today’s main focus is on the North American data releases, particularly the Canadian jobs report and the US non-farm payrolls, which could lead to notable market movements.

The Canadian employment report anticipates a negative headline, indicating a cooling job market. A contraction of 12.5K jobs compared to last month’s minor gain would emphasize slower hiring. The unemployment rate’s rise from 6.9% to 7.0% supports this view and explains why the Bank of Canada is keeping rates stable. Policymakers are seeking more clarity from employment, trade, and pricing data before making changes. Market indications suggest one rate cut is likely by December, with more adjustments not expected until next year.

In the US, the labor market is more significant for market volatility. Job gains are expected to slow from 177K to 130K, while annual wage growth is forecasted at a solid 3.7%, despite a small drop. Monthly wages are expected to increase, presenting a mixed signal about inflation: easing year-on-year but firmer month-on-month. This could reduce premature calls for rate cuts from the Federal Reserve.

Now, let’s discuss market positioning. The 54 basis points projected for this year—beginning with a potential cut in September—could be overly optimistic if the job numbers are steady or improve. Stronger employment or wage data would likely mean the Fed delays action. Should there be any surprises, traders involved in rates or credit spreads must adjust their expectations quickly, as interest rate futures will shift.

Fed Chair Powell and his colleagues are not under immediate pressure. The hiring slowdown has been gradual, and despite challenges from tariffs, it hasn’t collapsed. Employment continues to grow, just at a slower pace. Until the economic situation becomes more concerning, the Fed can afford to watch without intervening.

Traders in interest rate derivatives, especially STIRs and swaps, need to be mindful of the risks linked to forward guidance. Sensitivity in the front end will stay high during the next few employment cycles, particularly if upcoming data contradicts the market’s softer outlook. The immediate bias seems to favor steady yields, but aggressive easing curves may put pressure on longer-dated bets.

While volatility in rates may not surge today if non-farm payrolls align with expectations, any unexpected changes in hiring or wage inflation could send clear signals, especially for curve steepeners and short-dated rate products. Traders must keep their positions flexible enough to adapt while remaining substantial enough to capture repricing if the Fed shifts its current stance.

China’s central bank unexpectedly injects 1 trillion yuan to ease rising liquidity concerns among banks

China’s central bank introduced 1 trillion yuan, about $139 billion, through three-month cash reverse repos. This marks a shift from their usual practice of month-end operations. The primary goal is to relieve concerns about interbank liquidity as borrowing costs rise and financial pressures increase. This comes just before a busy month for debt repayments.

In June, banks need to repay 4.2 trillion yuan in negotiable certificates of deposit. This significant cash injection comes early to prepare for these repayments. It also precedes government bond auctions, especially after a recent sale of 50-year bonds, which saw yields rise for the first time since 2022.

Anticipated Liquidity Support

Additional liquidity support is expected in June to help banks lend more and ensure smooth government debt issuance. This action is not just a routine cash operation; it’s a proactive approach to stabilize borrowing markets during tougher economic conditions. The People’s Bank of China speeded up both the timing and amount of their support, injecting almost $140 billion through an unusual window. They are using three-month reverse repurchase agreements, where banks sell securities to the central bank and agree to buy them back later. The aim is clear: make short-term cash more accessible as pressures begin to rise. The increase in financial stress didn’t happen overnight. With over four trillion yuan in short-term bank debts due in June through certificates of deposit, the central bank’s intervention was timely and strategic. Rising interbank borrowing costs indicate that banks are starting to protect their liquidity. This early cash injection is designed to prevent potential issues before they escalate. Interestingly, last month’s sale of 50-year bonds—rare due to their long duration—saw yields increase for the first time in a year and a half. This reflects a decreased appetite for long-term government bonds given current interest rates, as investors sought higher returns for such long maturities. This context shows why action is being taken now.Setting For Financial Control

This situation suggests a broader strategy for maintaining control. With more government bonds set for auction and signs of tighter credit conditions, this cash injection serves multiple purposes. It’s about preventing disruptions in the repo markets and stabilizing lending rates, while also ensuring smooth fiscal issuance in the coming weeks. By injecting liquidity early, authorities reduce the risk of pricing volatility when significant public borrowing occurs. This can be viewed as a signal to the financial system that the trends from April and May are being monitored. It also invites consideration of where short-term policy operations might head next, and whether long-term inflation expectations are truly stable, as some believe. With central planners willing to adapt their usual strategies, previous assumptions about timing and amounts may need to be reevaluated. Create your live VT Markets account and start trading now.Japan’s Ministry of Finance may change its bond strategy to focus on shorter maturities due to weakening demand.

Japan’s Ministry of Finance (MOF) is considering changing its strategy for issuing government bonds. This shift may involve focusing more on shorter bonds and reducing the amount of long-term debt. The reason for this is a rise in yields and a drop in investor interest in long-term bonds. This trend was highlighted by a recent 30-year bond auction, which experienced the weakest demand seen in 2023.

In that auction, the bid-to-cover ratio was only 2.92, down from 3.07 in the last sale and significantly lower than the 12-month average of 3.39. The MOF is reacting to these changes by reaching out to market participants with a questionnaire and planning a meeting with primary dealers following the Bank of Japan’s review of its bond-buying practices.

Analysts speculate about possible cuts in bond issuance, with hopes for reductions of ¥300–450 billion per sale. JPMorgan even predicts monthly cuts of ¥250–450 billion starting in July. However, if the MOF opts for smaller cuts—around ¥100 billion for super-long bonds—there is a danger of renewed selling pressure, which could push yields back to previous highs if expectations are unmet.

What this article indicates is a clear change in how Japan plans to manage its government debt. The Ministry of Finance is responding to a noticeable drop in investor interest in long-dated bonds, especially highlighted in the recent 30-year auction, which had a bid-to-cover ratio close to three. This is a significant decline from the previous auction and the yearly average, indicating that investors are hesitant to commit money for long periods, possibly due to uncertainties about inflation, interest rates, or the Bank of Japan’s changing policies.

Recently, the MOF has taken steps to engage directly with the market. They circulated a questionnaire and set up discussions with primary dealers. This engagement shows they are trying to understand market reactions to potential changes in their bond issuance strategy. This suggests that any adjustments will aim to avoid major surprises at first. However, markets can be unpredictable, even with clear signals.

If the MOF follows through with significant monthly cuts, as JPMorgan suggests, that would represent a major shift. Still, the actual changes from the MOF could be more cautious. If reductions are more modest—around ¥100 billion—then current expectations in the rates market might begin to fade, causing yields to rise again.

For traders dealing with duration risk, this situation is crucial. While the idea of issuing fewer long-dated bonds might seem positive, it depends on whether it meets market expectations. If the MOF’s actions appear hesitant or indecisive, the bullish outlook weakens significantly. Past experiences show that markets often penalize uncertainty.

Hamada mentioned that for the market to react positively, expected cuts must be “meaningful.” That’s a valid point, as there is little room for half-measures. Expectations are already above ¥100 billion, and any announcement below that threshold could be viewed negatively. This is especially true now that the Bank of Japan is reviewing its bond purchases, adding complexity to an already sensitive market.

Looking forward, we have several factors at play. Questions linger about how much the Bank of Japan will withdraw from the market. The central bank has been a consistent buyer, and any changes will affect yield levels. Depending on how closely the MOF and the central bank coordinate, bond yields in the long term may either stabilize or become more volatile.

In the shorter-term space, if the MOF increases issuance, rates could face downward pressure, especially if demand remains strong. Some traders may decide to take on more risk with short-term bonds, particularly if pricing aligns with future expectations. However, those invested in super-long contracts or leveraged positions on 20- to 30-year JGBs may need to rethink their strategies, especially if supply remains consistent.

Market reactions will depend on not only the size of the supply changes but also how clearly the MOF communicates its intentions. A detailed issuance calendar, even if conservative, could help lessen selling pressure and promote better-informed positioning. In contrast, vague or minimal guidance could lead to market misalignment, where sentiment drives price changes rather than fundamentals.

Also, we must consider how institutional buyers—like insurers and pension funds—will respond. Their interest in ultra-long bonds has historically helped stabilize the market, but this support seems to be weakening. If these buyers continue to scale back, liquidity may worsen in specific areas, potentially widening spreads.

In summary, the coming weeks will be crucial, determined by both the tone of communication and the actual numbers. For now, we will keep a close watch on spreads, auction schedules, and implied volatilities. What’s important is not just what the MOF decides, but how it presents those decisions to a market that is already expecting more than slight adjustments.

JP Morgan revises prediction for ECB’s next rate cut to September

JP Morgan has changed its forecast for the European Central Bank’s (ECB) interest rate moves. The bank now expects the next rate cut to happen in September instead of the previously predicted July.

The ECB’s next policy meeting is on July 24, 2025, and it could have an impact on future economic decisions.

Changing Economic Signals

The shift from July to September indicates a shift in how economic indicators have been viewed recently. Early predictions suggested a quicker rate reduction, but new data hasn’t given central bankers the confidence to act fast. For example, inflation rates are still higher than desired, and wage pressures in some eurozone countries are keeping prices steady. Additionally, unemployment remains low, reducing the urgency for immediate policy changes. Differing opinions on whether current inflation levels will last have led strategists to adjust their forecasts. Policymakers seem to prefer taking their time, wanting more data before deciding on easing financial conditions that could spark unwanted inflation. They seem to favor confirming trends over relying on temporary relief signs. For those involved in derivatives, this delay alters how we plan in the near and mid-term. Expectations for rate cuts this summer need to be toned down, and preparing for the September meeting is now more important. Volatility in interest rate futures and options may rise as market participants update their strategies. The period from now until late September will be crucial, with increased market sensitivity to small changes in CPI and policy discussions.Market Reactions

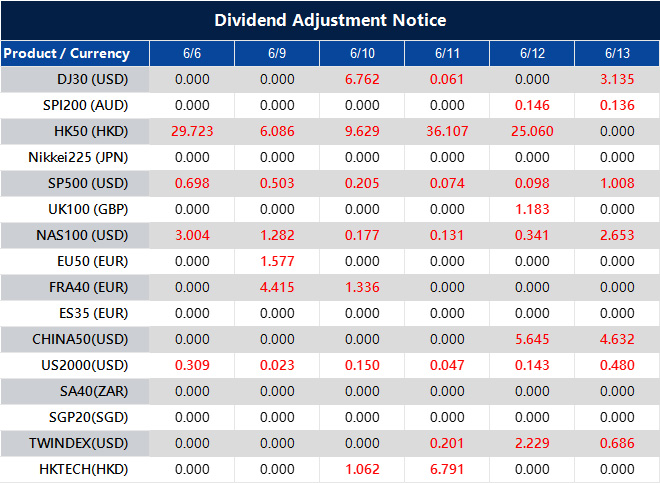

Lagarde and her team likely won’t diverge much from the consensus, but any slight changes in their tone—like a more cautious stance or hints at future guidance—could lead to big reactions in interest rates and foreign exchange markets. Currently, monetary conditions are already tight compared to historical standards, and without a clear direction, it’s challenging to manage duration confidently. We must be more precise with timing and exposure. While the expected easing cycle is still in place, its pace is now in doubt. Strategies involving flatteners or steeper curve plays may need adjustments; those looking to buy short-term volatility should rethink their strike selections. Strategies based on a July cut in short-dated contracts should adapt as trading volume shifts toward later dates. Ultimately, movements in the markets this summer will depend more on concrete data releases than statements from policymakers. Pricing models should move from prediction-based to response-based. With fewer assumptions and more control over scenarios, we shouldn’t expect the markets to remain quiet until the ECB meets in September. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 06 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Lagarde’s video address in Marseille provides little encouragement for traders about interest rates

European Central Bank President Christine Lagarde will give a video message this Friday at an event in Marseille, France. This event celebrates the 75th anniversary of the International Confederation of Popular Banks.

On Thursday, Lagarde discussed the ECB’s choice to lower key rates by 25 basis points, which was expected. She highlighted a slowdown in the services sector and pointed out that the easing cycle may be coming to an end.

Recent reports from the ECB show that most members of the recent meeting preferred to keep rates steady in July. Officials expect that rate cuts may be paused in the following month.

Lagarde’s comments indicate a changing approach that has been developing over time. Although the rate cut this week was anticipated, the noteworthy aspect was the hint that the push for more reductions might be weakening. By mentioning the slowdown in the services sector, she recognized that an area previously seen as stable is now showing signs of weakness.

The meeting minutes and subsequent interviews suggest that policymakers are adopting a cautious wait-and-see strategy. This highlights that they are more focused on ongoing inflation than on fragile growth. Inflation remains stubborn in certain areas of the economy. This is why the message was not about a steady decline in rates, but a clear intent to pause.

During the recent ECB meeting, the consensus was to keep rates unchanged in July. This isn’t speculation; it comes from a summary provided shortly after the meeting. Notably, even those open to future rate cuts emphasized the need to wait for more data on wages and profit margins expected later this summer. There is a growing desire for stronger confirmation before making any decisions.

For those managing short-term positions, the clarity about July reduces uncertainty. However, the focus now is less on the upcoming meeting and more on being flexible for developments in September. Volatility may return around that time, especially if wage trends don’t improve. Following Lagarde’s remarks, forward rate markets showed a slight tightening in expectations for further cuts this year.

Traders should view the ECB’s shift not as a reversal, but as a cautious step back after testing the waters. Exposure to summer meetings should be limited, as most of the Governing Council members seem unwilling to make new commitments. With mixed growth signals and persistent inflation in services and energy, the balance of risks has shifted towards caution.

While headline inflation has decreased, core inflation remains resilient. This is where the current debate lies—beneath the surface. In the upcoming weeks, the risks are more about surprises from wage or margin updates rather than from central bank statements. The little forward guidance left is now more reactive than proactive.

When considering pricing spreads and strategies for contracts related to the euro area, it’s time to adjust expectations toward longer pauses instead of steady reductions. The current situation does not signal a return to neutrality anytime soon. We see more value in having options rather than making directional bets through July and early August. This highlights the reluctance to make moves without new supporting evidence.

Musk acknowledges better relations with Trump in a tweet, boosting US equity futures

US equity index futures rose when evening trading on Globex began. This increase is linked to reduced tensions, highlighted by a Twitter exchange between Musk and Ackman.

Their conversation indicates a move toward unity. The market reacted positively, showing an optimistic outlook after their dialogue.