Japan’s capital spending increases by 6.4% year-over-year, exceeding expectations, but company profits fall short.

Japan’s capital spending in Q1 2025 increased by 6.4% compared to last year. This was better than the predicted growth of 3.8% and a recovery from a slight decline of 0.2% in the previous year. On a quarterly basis, capital spending also rose by 1.6%.

When we exclude software, capital spending jumped 6.9% year-over-year, surpassing the expected increase of 5.3% and the previous rise of 3.1%.

The Bank of Japan has raised provisions for bond losses due to expected interest rate increases.

The Bank of Japan is preparing for possible losses on its bond transactions by increasing its provisions. This suggests that the bank expects interest rates to rise.

For fiscal 2024, the Bank has set provisions at 100% for the first time ever. This funding comes from the income generated by its bond and financial activities.

Typically, the Bank targeted 50% for provisions before fiscal 2024, reaching a maximum of 95% in fiscal 2018. Recently, provisions increased by 472.7 billion yen ($3.28 billion), following a 922.7 billion yen rise in fiscal 2023.

When the Bank of Japan raises rates, it affects the yen. Expectations of higher rates caused the yen to strengthen from July to September 2024, which led to changes in some yen carry trades and impacted global markets.

The Bank’s full provisioning clearly shows that it believes there is a significant risk of loss in its bond holdings if interest rates keep climbing. This is a proactive financial cushion made from earlier earnings to prepare for declining bond values, which often occur when rates increase.

Notably, the level of provisions has doubled in just two years. Even with elevated preparations in previous years, such as during fiscal 2018, the Bank never allocated its entire income to cover potential losses. This cautious approach suggests that the current situation is more than just routine accounting—it reflects serious expectations.

By fully committing income to counteract expected declines in market values, the rise in domestic rates is seen as not just a prediction but as active preparation. These changes indicate a clear policy intent.

This shift is important for those watching the derivative markets. Rising rates in Japan directly impact strategies built around stable or declining yen values. Expectations alone have already caused the yen to rise from July to September, leading to real consequences for leveraged positions tied to interest rate differences.

The effect on carry trades is not just a theory; it has happened. Increased exchange rate volatility followed suit, leading to adjustments in leveraged yen positions, and raising the cost of maintaining those positions. Funding strategies that relied on low yen borrowing costs have become riskier. Even traders not directly involved with the yen have felt the effects in cross-currency spreads and volatility in Asia-Pacific options.

Going forward, we should closely monitor volatility trends in the JPY market. Forward implied rates are no longer confidently predicting stable outcomes. This is influenced not only by market movements but also by hedging actions driven by rising uncertainty about interest rates.

Those involved in strategies that sell volatility or have short gamma positions might need to rethink their risk levels as we approach the next rate decision. Focusing on short-term resets and broader collars can be wise. It’s better to avoid aggressive premium seeking in yen-related derivatives until we hear an official policy signal from the Bank. While the income allocation is telling, the response in swaps, credit default swaps (CDS), and Japanese Government Bond (JGB) futures will really test the market’s conviction.

We should pivot from directional bets on yen appreciation to more effective hedges against rate-related shifts. Not every move needs to be extreme; timing and skew exposure will be crucial in the coming month.

Careful management of hedge ratios and delta exposures in multi-currency portfolios can help maintain a balance between protection and participation. We shouldn’t try to predict the exact announcement, but we can adjust our positions to reflect the clear shift in odds already indicated by the Bank’s provisioning.

The Australian manufacturing sector grew, despite a slight drop in output and moderate growth rates

The final Australian S&P Global Manufacturing PMI for May 2025 is 51.0. This is a drop from the preliminary reading of 51.7 and April’s 51.7. However, the sector is still growing.

Production And New Orders

In May, production fell for the first time in three months, and new orders increased at a slower pace. Stocks of purchases also went down as buying slowed down. On the bright side, some indicators suggest that output may grow in the coming months, thanks to rising export orders and better business confidence. Employment continued to rise, with firms actively hiring for open positions. Inflation pressures eased, marking the lowest costs in over a year, which may soon help boost demand. The report hinted that the recent slowdown might be linked to the election, making it potentially temporary. The May PMI reading of 51.0 keeps the manufacturing sector just above the line that divides growth from decline. Although it’s lower than the preliminary estimate and last month’s figure, it still indicates a slight softening in activity. However, the index remains above 50, which shows the sector still has some resilience, even if it’s a bit less than before. The drop in output, the first since February, shows a slowdown in production momentum. While it’s not drastic, this shift after previous gains suggests hesitation among manufacturers. This could be due to easing order backlogs or clients being cautious. Purchasing managers cut back on buying inputs, leading to a decline in stocks for the first time in several months. Demand seems less urgent, even though firms are optimistic about the future.Export Orders And Business Confidence

The rise in export orders is a positive sign. Focusing on foreign demand may help maintain activity levels if local conditions remain weak for a while. Business confidence has increased, according to survey results, but history suggests this doesn’t always lead to immediate volume gains; it often takes time to show in actual output. Labour conditions are tightening. Continued hiring indicates that firms expect strong enough demand to justify keeping or expanding their capacity. This hiring trend, alongside reduced cost inflation—the lowest in over a year—may create an environment where profit margins start to stabilize or improve. Lower input costs can also lead to better inventory management and price competition without hurting profits right away. There’s also a political aspect to this data. National elections can influence economic activity, partly due to uncertainty and partly due to expectations for new policies. It’s likely that some clients, especially in sectors that require heavy investment, postponed orders temporarily. Once policy clarity returns, we usually see those delayed decisions come back into play. Given these changes, we should expect mixed data in the near future. Past instances of stalled output growth without a broader decline have led to tighter implied volatility in manufacturing-driven markets. This suggests potential opportunities for strategies focused on stable conditions or lower-risk derivatives. Furthermore, employment growth combined with easing input costs may create a solid foundation for future price expectations linked to industrial production. We shouldn’t overlook export strength. While it may not immediately affect overall economic measurements, it is beneficial for products related to producer sentiment or shipping volumes. Changes in purchasing habits and stock reductions may result in a slower increase in forward indicators, indicating that mid-term derivative structures could benefit from later entry points. Lastly, decreasing inflation pressures, especially if they continue over time, might change yield curve expectations. If we continue to see this alongside stable hiring, fixed income derivatives related to products may need adjustments. Scenarios should be revisited to put greater emphasis on sustained growth in a disinflationary setting. Create your live VT Markets account and start trading now.Bessent believes that Trump will soon discuss trade issues with Xi.

U.S. Treasury Secretary Bessent stated that China is holding back products essential for the industrial supply chain. She expects a talk between Trump and China’s Xi to happen soon.

Details about when this conversation will take place were not shared. This situation affects trade and economic ties between the two countries.

Period Of Low Transparency

Bessent’s remarks point to a time of low transparency in global trade, especially concerning the industrial parts that support broader manufacturing. The possibility of a discussion between the leaders shows that there are serious concerns and could lead to changes in how countries manage their economic ties. Uncertainty like this can increase market volatility, especially in areas related to industrial production and trade logistics. If key materials or parts are delayed or restricted, prices can change quickly. Markets linked to commodities or manufacturing could start to adjust their expectations before any official agreement is made. It’s important to pay attention to guidance from both direct policy statements and other signs, like changes in tariffs, supply chain disruptions, or changes in inventory. Price trends in short-term interest rate futures may start to show expectations of slower economic activity, particularly if the market thinks negotiations might take longer than expected.Impact On Economic Friction

Traders involved in foreign exchange (FX) contracts should think about how economic friction could affect the strength of the dollar, especially if investors seek safe-haven assets. Movements in bond futures can also indicate expectations about trade resolutions; for instance, how curves steepen or flatten can show where agreement might be forming. While no date has been set, the chance of an official discussion opens up a speculative window. This could lead to changes not only in traditional equity and commodity markets but also in trades that depend on a stable supply chain. We should be ready for sudden price changes that often happen before official announcements. Markets tend to anticipate changes rather than simply react. Watching for volume spikes in sector-specific ETFs or calendar spreads can provide early insights into shifts in sentiment. Stay flexible in your positioning. Low liquidity in certain derivative products may lead to exaggerated price movements during these times. It’s wise not to depend on just one financial instrument or news headline when facing this kind of cross-border economic strain. Create your live VT Markets account and start trading now.China’s manufacturing PMI shows slight improvement, but contraction continues; non-manufacturing sector remains in expansion despite cautious sentiment

China’s National Bureau of Statistics reported that the manufacturing PMI for May 2025 rose to 49.5, up from April’s 49.0. However, this remains below 50, indicating contraction for the second month in a row. Large companies showed improvement with an expanding PMI of 50.7, while medium and small enterprises recorded lower PMI scores of 47.5 and 49.3, respectively. The production sub-index grew to 50.7, and new orders made a slight recovery to 49.8. Employment improved but stayed below the growth threshold at 48.1, while supplier delivery times were stable at 50.0.

In the non-manufacturing sector, the PMI was 50.3, showing slight expansion but falling short of the expected 50.6. Construction activity dipped to 51.0, while services edged up to 50.2. Strong performance was seen in industries like rail, air transport, postal services, telecoms, and IT, all scoring above 55.0. In contrast, real estate and capital markets remained below 50. New orders increased slightly but were still weak at 46.1, with contributions from construction and services. Input and selling prices continued to decline, although at a slower pace. Employment remained weak at 45.5, but business expectations, despite a slight decrease, stayed optimistic at 55.9. China plans to unveil new financial policies in mid-June 2025 as anticipation builds for further economic stimulus.

Underwhelming Momentum in Manufacturing

Looking at the May numbers from the National Bureau of Statistics, we see a mix of small improvements but an overall lackluster performance. The manufacturing PMI stands at 49.5, an improvement from April’s 49.0, but it still indicates the sector is contracting, just at a slower pace. A PMI below 50 shows a decline in general activity. Notably, large companies reported growth with readings above 50, while medium and smaller firms struggled. This gap creates complicated signals across production levels and demand. The production sub-index increased to 50.7, giving a hint of optimism, yet new industrial orders rose only slightly to 49.8. While this represents some improvement, it does not signal a full return of demand. Employment remains a challenge. With a figure of 48.1, job losses are still occurring, though the decline is less severe than in the previous month. Stronger hiring would signal a more consistent recovery. In the non-manufacturing sector, there are signs of growth, but it’s not particularly impressive. The PMI at 50.3 shows slight expansion but falls short of expectations. When forecasts were for 50.6, a number just above the break-even point suggests weaker service momentum than policymakers envisioned. The decline in construction activity to 51.0 does not provide much reassurance, especially given the sector’s importance in past recovery efforts.Divergence in the Service Sector

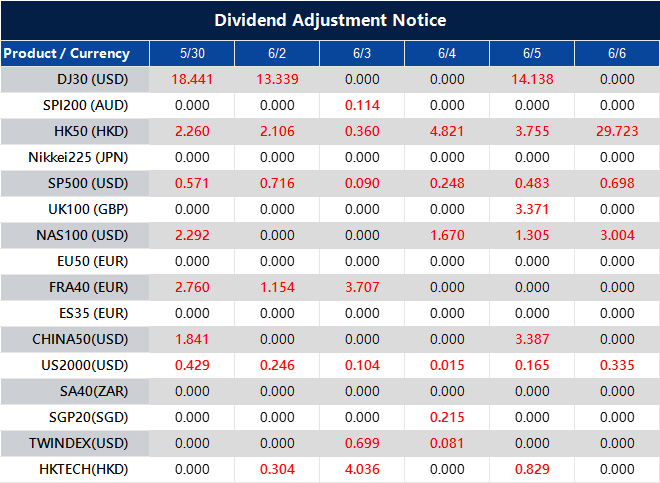

Examining the service sector further reveals a split between declining and thriving categories. Transport and tech-related areas, such as air, rail, IT, and postal services, are performing well with scores in the mid-50s, indicating strong activity. Meanwhile, real estate and financial services, especially capital markets, are still contracting and struggling even before any new credit or fiscal policy is announced. New orders in the service and construction sectors increased slightly, but at 46.1, they indicate customers are still hesitant. Demand is not robust, and any improvements seem inconsistent. Input and selling prices are also decreasing, but the decline is slowing down. This ongoing price deflation may indicate softer consumption or reluctance to restock materials, a trend to keep an eye on. Workforce numbers remain concerning in the service sector as well. A reading of 45.5 is weak and shows that businesses are not hiring. Even if intentions are steady, actions have not followed through. Despite this, future expectations remain high, suggesting that companies are hopeful but not yet ready to act. A score of 55.9 reflects confidence, but unless new policies lead to real changes, this optimism may not hold much weight. Overall, the key takeaway is the gap between sentiment and actual performance. There is clear anticipation for government support, with further measures expected in mid-June. This might involve coordination with monetary or lending policies. Until those measures are in place, traders should focus on actual data rather than just forecasts. Market responses in equities and rates may remain subdued until we see significant improvements in investment and consumption numbers. Recent months hint at a fragile recovery, but not one that is reliable yet. For now, fluctuations in certain futures contracts suggest that traders are being cautious until stimulus plans are clearly defined and implemented. It’s important to watch for updates on infrastructure spending, measures supporting private businesses, and incentives aimed at boosting consumer demand. Keeping an eye on sector-specific performance—especially in real estate, services, and logistics—will provide the best short-term insights. Changes are happening at a gradual pace, but they remain uneven; trading strategies should reflect this reality. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – May 30 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

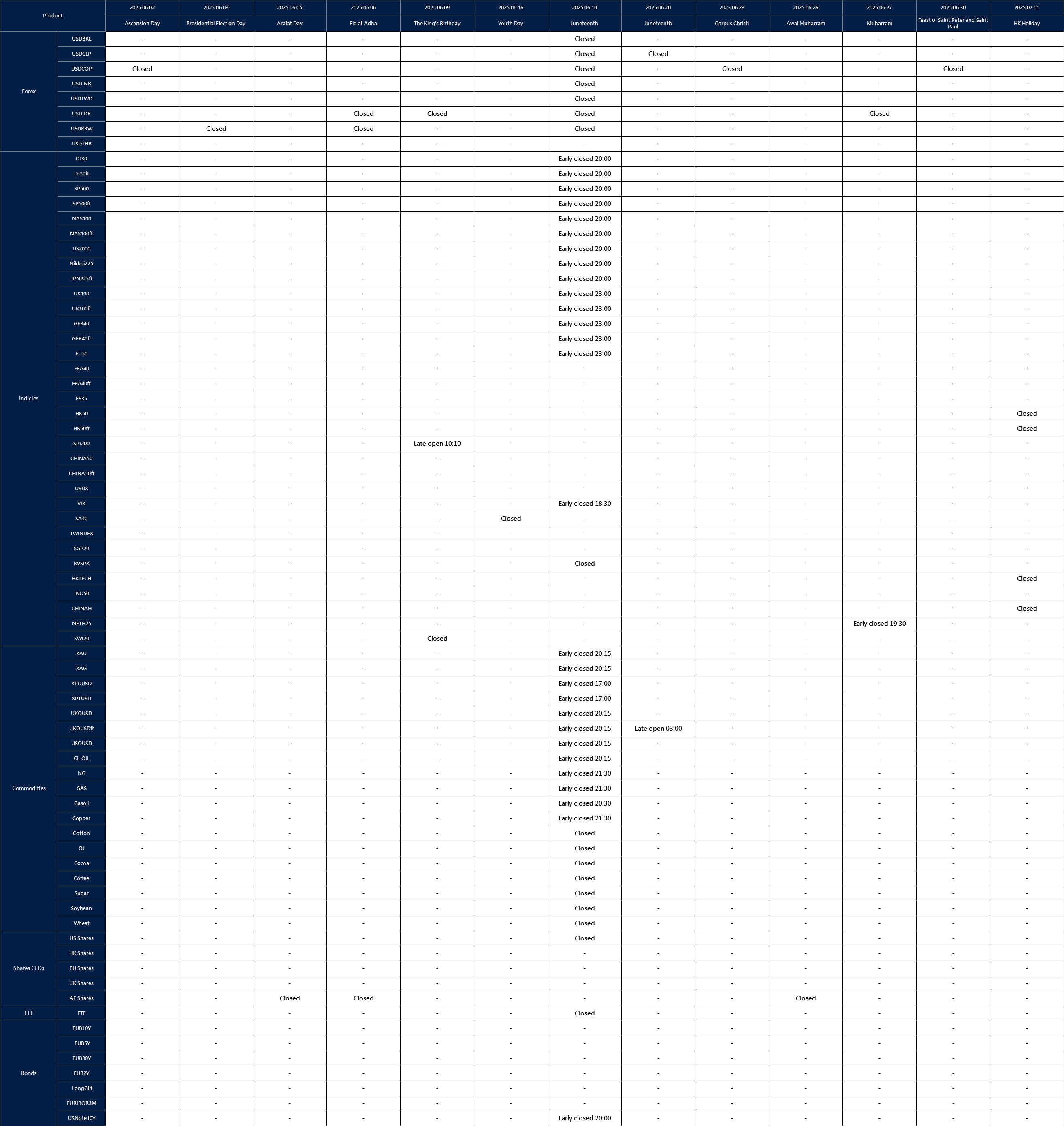

Notification of Trading Adjustment in Holiday – May 29 ,2025

Dear Client,

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the affected products:

Notification of Trading Adjustment in Holiday

Note: The dash sign (-) indicates normal trading hours.

Friendly Reminder:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

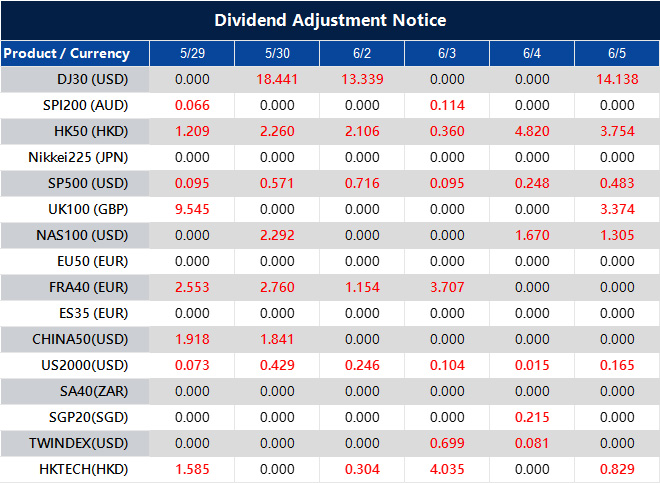

Dividend Adjustment Notice – May 29 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

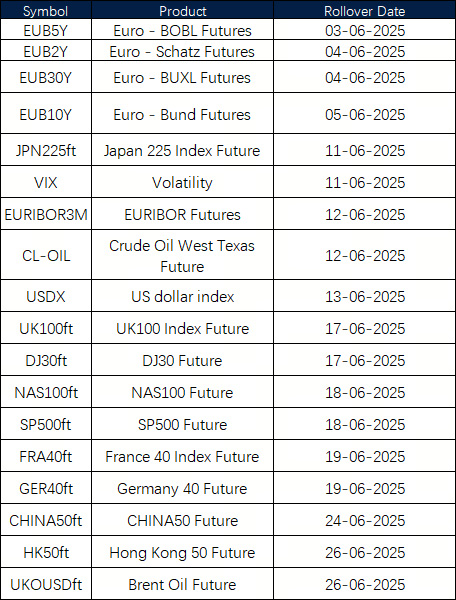

June Futures Rollover Announcement – May 29 ,2025

Dear Client,

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

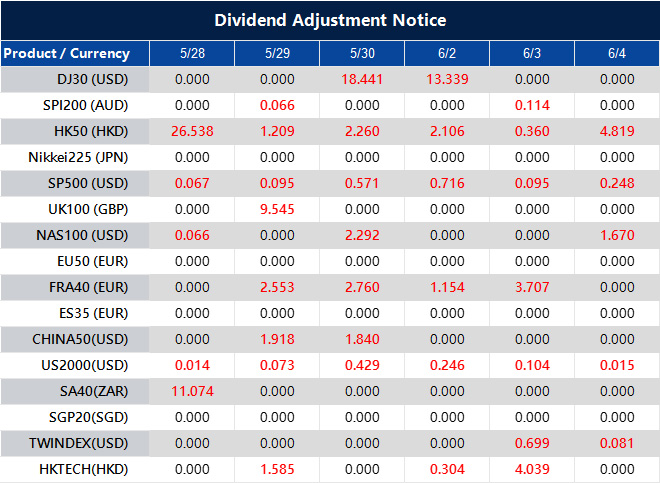

Dividend Adjustment Notice – May 28 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

{kind=link}