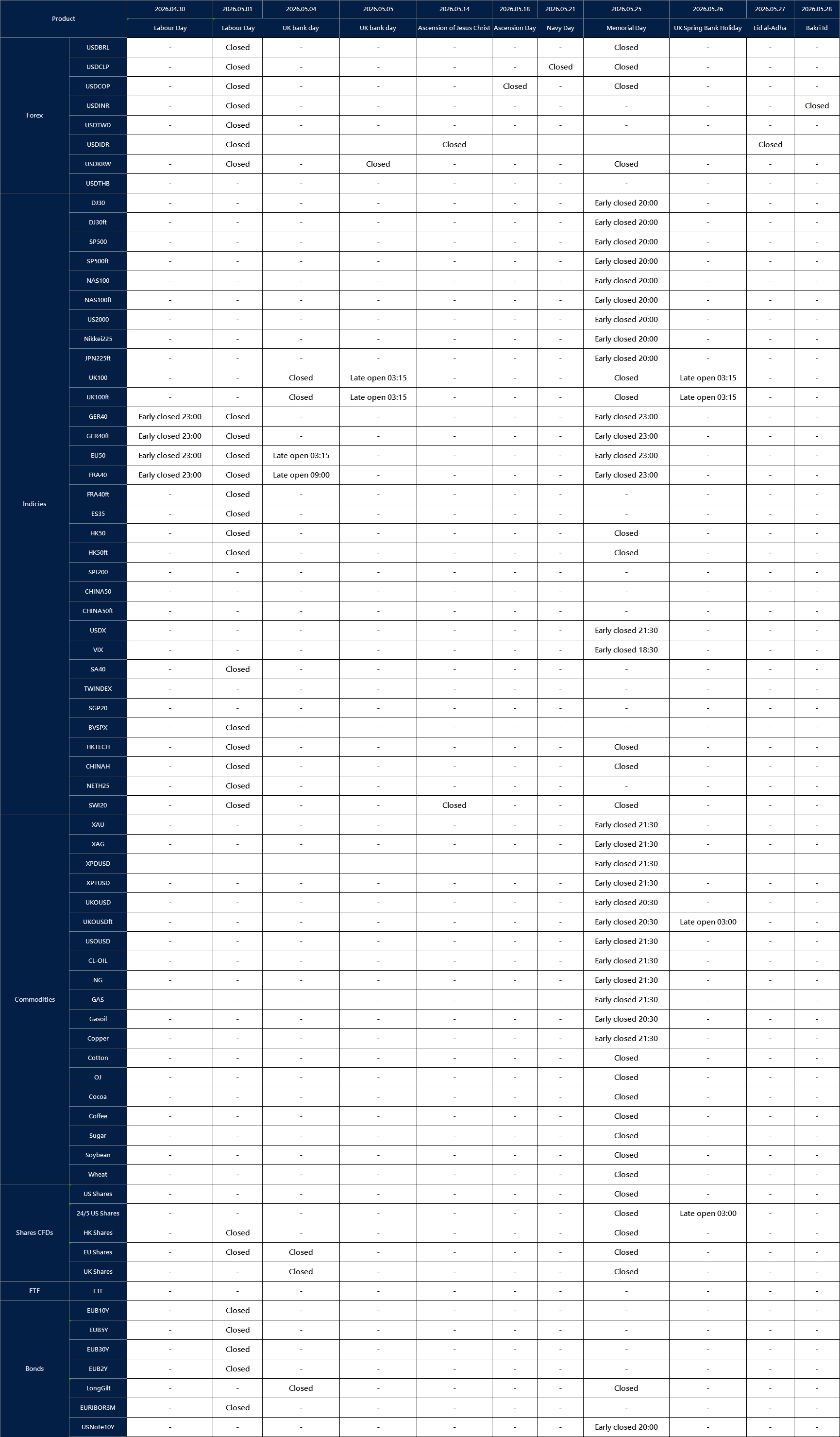

GBP/USD was steady for a second day, trading near 1.3530 during Asian hours on Tuesday. On the daily chart, the pair is moving sideways inside an ascending channel, which points to a bullish bias.

The pair remains above the nine-day and 50-day Exponential Moving Averages (EMAs). Both EMAs sit below the current price, supporting the upward trend.

Technical Indicators And Trend Context

The 14-day Relative Strength Index (RSI) is near 58, which is above the neutral level. It is not in overbought territory.

Looking back to late 2025, we saw a period where bullish sentiment for GBP/USD was strong, with the pair trading constructively within an ascending channel around 1.3530. At that time, key moving averages provided solid support, and the Relative Strength Index suggested buyers were in control. The technical picture then pointed towards continued upside momentum.

The situation has changed considerably as we now see the pair trading near 1.2850. The previous support levels have been broken due to persistent US dollar strength, overriding the technical bullishness we observed last year. This shift reflects a market now dominated by macroeconomic factors rather than the prior technical structure.

Recent data reinforces this view, with the latest US Non-Farm Payroll report showing a robust addition of over 250,000 jobs, strengthening the case for a hawkish Federal Reserve. On the other hand, UK inflation remains elevated at 3.1%, forcing the Bank of England to maintain a firm stance. This policy divergence is a key driver of the pound’s current valuation against the dollar.

Options Strategies And Key Risks

Given the prevailing downward pressure, derivative traders could consider buying put options with a June 2026 expiry to capitalize on potential further declines. A strike price around 1.2750 would offer a way to profit if the current trend continues in the coming weeks. This strategy also serves as a hedge for any existing long positions in the pound.

For those who anticipate that the pair will become range-bound between a strong dollar and a hawkish Bank of England, selling a strangle could be an effective strategy. By selling both a call option with a strike near 1.3000 and a put option with a strike at 1.2700, traders can collect premium from the expectation of low volatility. This approach profits if GBP/USD remains between these two levels until expiration.

We must remain vigilant, as the primary risk to these positions is a sudden change in tone from either central bank. The upcoming meeting minutes from both the Federal Reserve and the Bank of England will be critical to monitor. Any unexpected weakness in US economic data or a surprise drop in UK inflation could quickly reverse the current market dynamics.

{kind=link}