Today’s agenda includes final services PMIs, US ADP data, and the Bank of Canada’s policy decision.

In the European session, the attention is on the final services PMIs for the UK and Europe. These reports are not expected to have a major impact on market prices.

In the American session, important data includes the US ADP report, the Canadian Services PMI, and the US ISM Services PMI. Notably, the “prices paid” component in the ISM PMI is expected to draw particular interest.

New Products Launch – Jun 04 ,2025

Dear Client,

To provide you with more diverse trading options, VT Markets will have a product launch. Please refer to the details:

Friendly reminders:

1. The above data is for reference only, please refer to the MT4/MT5 software for specific data.

2. The swap rate is subject to the MT4 and MT5 software.

If you’d like more information, please don’t hesitate to contact [email protected].

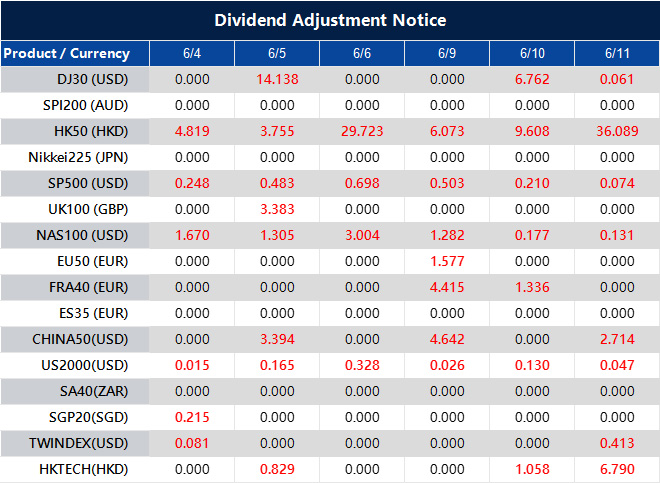

Dividend Adjustment Notice – Jun 04 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

A calmer atmosphere precedes European trading, with the dollar showing minimal volatility today.

The dollar has been fluctuating, making it hard to identify clear trends. There is still trade uncertainty, but signs suggest major changes may not happen soon. Yesterday, both the dollar and stocks gained, but today feels more cautious.

Changes in dollar pairs are minimal, with differences of less than 0.1%. This indicates a calm European trading session. With few events on the schedule, the trading day may be slow.

Activity may pick up later when the ADP employment report is released in the US. In other markets, S&P 500 futures have dropped by 0.1%. Gold prices are slightly up, now at $3,359, a 0.2% increase.

In simple terms, the dollar’s recent behavior has been unpredictable. Traders are looking for a clear direction, but that hasn’t happened yet. There’s speculation about major economic or policy changes, but it seems those sudden moves might not happen soon. This creates a steadier tone for the dollar and investors. Yesterday’s gains in the greenback and stocks have given way to a more cautious trading day today, with little movement in the early European session.

The lack of significant movement—less than a 0.1% change—shows that traders are waiting before making commitments. They likely prefer to sit on the sidelines until more data arrives. With few scheduled events until US markets open, there may be narrow price ranges. Unless sentiment shifts or unexpected news comes out, the trading session could continue at this slow pace.

The next important event will be the release of US private payroll data. This could bring back volatility. Jobs data are closely watched for what they might suggest about future monetary policy. If the numbers differ significantly from what’s expected, it could lead to reactions in foreign exchange, stocks, and bond markets.

In other news, the recent 0.1% drop in US index futures suggests less enthusiasm from equity investors. They are neither selling a lot nor buying aggressively. It’s a quiet indication that aligns with recent trends: inconsistent price action without a clear direction.

Gold is also climbing slightly again. At $3,359, it has gained 0.2%. While not a huge increase, it indicates that some investors are becoming more defensive. Such movements typically show that market participants are cautious, even if their appetite for risk isn’t fully diminished.

As we move through these hours, patience is necessary. Clear signals are lacking. When faced with inconsistency, it’s often better to be opportunistic than overly committed. Use short-term levels as your guide; avoid chasing trends. Wait for stronger confirmation during the North American session. One important data release could shift the short-term balance. Until then, it’s best to react rather than preempt.

Approach expectations for upcoming sessions with caution. The risk of overreacting is low, but being too complacent could be unwise. The environment has calmed for now. Whether this continues into the afternoon may depend on the labor data and how it aligns with current views on inflation and economic momentum.

Australia’s Q1 2025 GDP rose 0.2% quarterly, but fell short of expectations due to revised estimates

Australia’s economic growth from January to March 2025 shows a GDP increase of +0.2% quarter-on-quarter. This is lower than the expected +0.4% and declined from +0.6% in the previous quarter. Year-on-year growth stands at +1.3%, matching last year’s rate but falling short of the forecasted +1.5%.

The GDP Chain Price Index indicates a drop in inflation to +0.5% from +1.4%. Final consumption rose by +0.2%, down from +0.5%, and per capita GDP growth decreased to -0.2%, compared to +0.1% previously. There is also a reported decline in productivity of 1%.

Household Savings And Government Spending

The household saving rate increased to 5.2% from 3.9%. Government spending saw its largest drop since 2017, affecting overall growth. In response to this data, yields are falling, suggesting potential rate cuts by the Reserve Bank of Australia. The Australian dollar had a minimal reaction to these economic figures, with only slight fluctuations. This recent GDP report shows a weaker domestic momentum in early 2025. The quarterly growth of 0.2% is below expectations and continues the slowdown from late 2024. Analysts expected higher figures, so this underperformance might lead to reevaluations of central bank predictions. Yearly output rose by 1.3%, but this is a stagnation when compared to the previous reading, indicating limited demand growth. One noteworthy point is that inflation is decreasing quickly, as seen in the GDP Chain Price Index which fell to 0.5%. This is the second consecutive quarter of slowing price growth, potentially supporting arguments for future rate changes by the Reserve Bank. Spending trends in both public and household sectors show significant changes. Final consumption, usually a key part of GDP, only grew by 0.2%—half of last quarter’s growth. This decline in consumer spending likely reflects growing caution amid economic uncertainty. However, the household saving rate increased to 5.2%, suggesting that people are holding onto their funds, possibly due to worries about lower income growth or uncertain returns on investments. A notable detail in the report is the sharp 1% drop in productivity, continuing a trend of weakness in output per labor input. This decrease is linked to the decline in per capita GDP, which fell by 0.2%. Although overall output is still growing, the person-to-person growth isn’t keeping pace.Government Spending And Market Reactions

Government spending, often a stabilizing factor when households reduce spending, fell at its fastest rate since 2017. This timing is problematic; with private demand already waning, the public sector’s decrease adds more strain on total output. When government cuts occur alongside low productivity and subdued consumption, the downward pressure on the economy increases. So far, market reactions have been minimal. While yields showed some movement, hinting at possible future rate cuts, the currency response was low. Typically, significant shifts in FX happen when economic data comes in like this, but today was different. Perhaps traders already priced in this information or are waiting for clearer policy signals. For those involved in managing interest rates or inflation strategies, the main point is that today’s data has implications for future meetings rather than just the numbers themselves. The economy isn’t fully stalled, but growth appears slower than anticipated at the start of the year. Investors should adjust their expectations for lower terminal rates and consider softer productivity factors when pricing risk around income-linked assets. We think the data highlights that, while growth is still slightly positive, ongoing issues with productivity and per capita measures suggest a cautious approach is needed. Tight monetary policies in this context could lead to overreactions. We will closely monitor employment signals in the upcoming reports. Timing is crucial—more than just signals. Create your live VT Markets account and start trading now.The PBOC sets the USD/CNY midpoint at 7.1886, lower than the expected rate of 7.1977.

The People’s Bank of China (PBOC) is the central bank and sets the daily midpoint for the yuan’s exchange rate. It uses a managed floating exchange rate system, which allows the yuan to vary within a +/- 2% band around a set central rate.

The last recorded exchange rate for the yuan was 7.1878. The PBOC also introduced 214.9 billion yuan into the financial system through 7-day reverse repos, with an interest rate of 1.40%.

On the same day, 215.5 billion yuan were scheduled to mature. This means there was a small net drain of 0.6 billion yuan.

This mild liquidity reduction shows that the PBOC aims to maintain stability. The small difference between matured repos and new injections reflects careful management rather than a major change in policy.

Zhou and the central bank team seem to signal continuity by keeping the 7-day reverse repo rate at 1.40%. This suggests they do not plan to speed up easing despite challenging trade and manufacturing conditions.

The midpoint fix, set earlier, is important for predicting exchange rate movements. With the yuan closing at 7.1878, it serves as a key point for pricing options and near-term futures. The +/- 2% band remains, providing some flexibility, but any significant move towards the edges needs attention.

Even slight tightening indicates we shouldn’t expect a surge of new liquidity soon. This could keep overnight repo and interbank borrowing rates steady or slightly rising, depending on local business demand.

From our perspective, a balance between liquidity inputs and maturing operations means that even small net changes carry weight. It’s about the underlying message: Li is indicating we’re not changing course just yet.

Daily rate fixes and short-term operations are crucial as they impact volatility models and inform policy responses. If they remain stable, without widening spreads or signs of hurried actions, it suggests little chance of a change in direction.

Consequently, we can expect short-dated FX option volatilities to stay steady unless there are clear signs of changing liquidity plans or cross-border flows. Traders managing interest rate differences may adopt rangebound strategies for now.

When we consider the shift in premiums, these are better signals for potential currency changes than the spot rate alone. Since the central bank adjusts liquidity with precision—like nudging rather than jerking a lever—it’s understandable that stability prevails.

Managing repo volumes this precisely often conveys a calm message: everything is going as planned with no rush or disruption. Keep an eye on the term structure and local funding demand, especially after tax periods, as these will impact future positioning.

Lastly, be aware that when funding is just tight enough to deter speculative actions but not enough to cause significant issues, it creates a boundary worth monitoring closely.

Raphael Bostic, President of the Atlanta Fed, discusses the impact of monetary policy on businesses and individuals.

Federal Reserve Bank of Atlanta President Raphael Bostic will speak on Wednesday, June 4, at a monetary policy event. The event will take place at 12:30 GMT (08:30 US Eastern time) at the Federal Reserve Bank of Atlanta.

Bostic will give both welcome and closing remarks at the Fed Listens event, titled “How Monetary Policy and Macroeconomic Conditions Affect Individuals and Businesses.”

Monetary Policy Outlook

Bostic recently discussed the current monetary policy and indicated that no changes are expected. He stressed that “patience” is essential right now. His comments suggest a desire to keep monetary policy steady for now. By emphasizing “patience,” he signals a preference to observe economic conditions before making adjustments to interest rates. The lack of expected changes indicates that key decision-makers believe inflation and employment figures are stable enough to remain the same. This steady approach affects our strategy for directional exposure. When a central bank leader repeatedly expresses a hands-off stance, especially before a macro-focused event, it’s significant. These discussions typically reinforce existing guidance instead of introducing major changes. The title of this event indicates that personal economic resilience and business sentiment will be key topics, rather than immediate adjustments to monetary policy. Timing is also important. As this event happens midweek and ahead of critical economic data later in the month, there could be some market reactions if Bostic’s tone changes. However, given his consistent communication style, any shift from the expected message would likely require significant changes in economic indicators, which we haven’t seen yet.Market Strategies and Implications

This suggests we should continue focusing on pricing volatility rather than making strong directional bets. With no expected rate changes, contracts tied to short-term policy decisions might stay within a narrow range, limiting breakout chances. We can still find value in instruments related to medium-term uncertainties or through strategies that take advantage of temporary price fluctuations. Bostic’s role at both the beginning and end of the event indicates he wants to guide perceptions, suggesting the message will remain close to current policy. Paying attention to slight changes in his tone, especially regarding confidence in future guidance, could aid in formulating short-term strategies. But until we see new inflation data or job market updates, the prevailing scenarios will likely lean towards maintaining the existing pricing. From our perspective, a careful approach with controlled risk is better than making bold directional moves. The current environment calls for caution over aggression. While headlines may fluctuate during the event, it’s expected that they will reaffirm current pricing trends rather than disrupt them. Create your live VT Markets account and start trading now.Japan’s services PMI at 51.0 signals slowed growth and inflation pressures in the sector

Japan’s Services PMI for May 2025 was recorded at 51.0, an increase from the preliminary estimate of 50.8 but a decrease from April’s 52.4. The Composite PMI rose slightly to 50.2 from the preliminary 49.8, but still dropped compared to April’s 51.2.

The manufacturing PMI for May 2025 was finalized at 49.4, up from April’s 48.7, but it still shows a contraction. The service sector’s growth has slowed due to a decline in demand, marking the weakest new business growth since November.

Employment growth in the services sector was the lowest since December 2023. Business sentiment improved compared to earlier this year, but it remains low relative to the post-pandemic standards.

High input costs are continuing to drive inflation, keeping pressure on prices. Stagnation in manufacturing and rising costs have nearly stopped private sector growth, leading to a decrease in the composite PMI to 50.2.

Current figures indicate that Japan’s broader economy is cooling. Services may still be growing, but at a slower pace, and the drop from April suggests that demand is weakening more than expected. Service providers are facing dwindling client orders, with fresh orders growing at their slowest rate in six months. This likely reflects consumer caution, possibly due to ongoing pressure from rising prices.

In manufacturing, the outlook is not very encouraging either. Although the finalized figure rose from April, the sector is still in contraction. A PMI below the 50.0 mark, even slightly, shows that factories are experiencing reduced output and demand. This indicates a clear stagnation in industrial activity.

On the employment side, the situation is also weak. Hiring in services has slowed. Although job creation hasn’t decreased outright, the current data is the lowest since late 2023, signaling a lack of confidence in future orders and revenue. Companies often reduce hiring when they feel uncertain about future activity levels. This makes the slight improvement in sentiment hard to interpret; while businesses hope for stronger conditions, they aren’t increasing their workforce accordingly.

Inflation is a significant factor holding back modest progress. High input costs, influenced by regional supply issues and energy prices, show little sign of decreasing anytime soon. These costs are being passed on where possible, likely reducing discretionary demand in services. This leaves only a slight increase in the composite index, which is just above 50, primarily due to slowing service growth, not any positive impact from industry.

For those monitoring short-term interest rates or currency fluctuations, these readings help set expectations for potential monetary policy changes. The central bank is unlikely to act quickly while growth is slow and inflation persists. This situation often leads to cautious trading activity.

Demand for protection against downside risks may increase, reflected in short-dated option skews, and implied volatility could rise, especially with risk-linked yen pairs. We should consider that weak business conditions in both services and manufacturing might affect pricing expectations. This could influence the forward rates market with slightly stronger views on rate path extensions, despite inflation concerns.

Overall, it’s wise not to react hastily to these developments. While PMI figures are below seasonal averages, they don’t indicate a severe downturn. Strategically positioning for the next cycle requires careful risk assessment, especially as liquidity may become tighter into mid-summer.

Officials suggest a regional uranium enrichment consortium in Iran could aid a U.S. nuclear deal.

Iran is exploring a nuclear deal with the U.S. that focuses on a regional uranium enrichment group. For this deal to work, the enrichment must take place inside Iran.

Experts urge caution about being too hopeful regarding the deal’s potential. If the agreement succeeds, it may boost Iranian oil supply, negatively affecting oil prices.

Uranium Enrichment Conditions

The latest draft of the proposed nuclear deal indicates that Tehran might agree to international oversight of its uranium enrichment, as long as the activities occur in Iran. This demand ensures that Iran maintains control, a longstanding issue in past negotiations. Analysts remain cautious, as previous similar attempts have faltered at crucial points. If discussions progress and a framework becomes clearer, energy markets could start to anticipate longer-term scenarios. This could mean more Iranian crude entering the market, putting downward pressure on benchmark oil prices, even before actual shipments begin. This situation ties supply directly to geopolitical factors, impacting more than just the energy sector. Last week, Mehdi outlined Tehran’s expectations, emphasizing a desire for control and economic relief. The main motivation for Iran is financial. Lifting some current restrictions could unlock new revenue streams, leading to increased supply that markets hadn’t considered just a month ago. We have started to see some forward contracts reflecting this potential. There’s been a rise in put option activity on Brent for later this year, along with a decrease in implied volatility over the past few sessions. This kind of activity often occurs ahead of confirmation events. Traders are not betting on immediate changes but are positioning for a medium-term shift that would lower price expectations through winter.Negotiation Dynamics

Jafari, a key negotiator in initial discussions, spoke mid-week about possible breakthroughs but mentioned several conditions. His comments were purposeful, indicating groundwork is being carefully laid. This caused a momentary market adjustment, evident in the steepening of the back end of the curve around March contracts. It suggests a slight change in positioning—still not a complete trend reversal, but movement is occurring. Given this context, we need to focus on scenario-based tracking. We should prepare for a softer oil market in early 2025 and keep fewer high-beta energy positions for shorter periods. What made sense before for longer-dated calls in energy-exposed assets now requires more flexible rotations into sectors less affected by headlines. Analysis of options data shows increased hedging interest in commodity-sensitive stocks, particularly with weekly expirations over monthly ones, likely due to greater event risk. This doesn’t indicate a full retreat from the reflation trade, but there are clear signs of caution. Companies that depend on tight spreads in energy markets may need to reconsider margin expectations. With policy and political timelines remaining uncertain, it’s wise to maintain flexible hedging strategies. This may involve using options ladders and calendar spreads to prepare for potential shifts when any official news emerges. We’re already seeing significant volume being directed towards September and November maturities, especially in gasoil and distillates. In this scenario, timing is more crucial than simply having a directional conviction. If a deal gains momentum and barrels return to the market faster than anticipated, volatility might not just persist—it could spike briefly before stabilizing. Being early will not yield the same rewards as in the past if the policy trigger happens mid-cycle. Create your live VT Markets account and start trading now.Economists expect the Bank of Canada to keep interest rates steady despite economic pressures.

The Bank of Canada is set to keep its key interest rate at 2.75% this week. Out of 13 economists surveyed by the Wall Street Journal, 11 believe there will be no change.

Even though unemployment is rising and domestic demand is falling, the GDP growth in Q1 was better than expected. This was driven by spending to avoid tariffs, showing some economic stability. Officials are paying attention to core inflation, which reached 3.15% in April, exceeding the Bank’s 2% target and showing its fastest rise in almost a year. The U.S. has also increased tariffs on steel and aluminum, important Canadian exports, which adds caution to inflation forecasts.

While a rate cut is unlikely this week, most economists think there may be cuts later this year if conditions remain poor. Any potential changes in policy could start in July.

The official announcement will come at 09:45 AM Eastern Time, followed by a news conference with Bank of Canada Governor Macklem at 10:30 AM.

The earlier context suggests that interest rates may pause despite some weak indicators like unemployment and soft consumer demand. However, the strong GDP figure, driven more by stockpiling than real growth, softens the view of weakness. Prices, especially those that the Bank monitors closely, are still high. The rise in April indicates that inflation isn’t decreasing as quickly as some may want. Traders should see the gap between weakened demand and steady inflation as a key point.

Policymakers are keeping a close eye on underlying price changes when considering any adjustments. This means their responses will rely on data rather than being swayed by general sentiment or seasonal changes. The mention of one-time tariff-avoidance spending suggests that the Q1 growth may not indicate a lasting recovery but rather a temporary effect from inventory changes.

Bond markets likely view this week’s meeting more as a fine-tuning than a major shift, with the Governor’s comments after the meeting possibly giving clearer signals. Market participants should adjust short-term prices based on any hints about future rate cuts. We expect a tone that balances weak domestic spending with persistent inflation.

Macklem’s comments about 45 minutes after the rate decision may provide additional insight, especially if his guidance changes. He will aim to shape future expectations while keeping options open. Traders will focus on subtle language—any indications of changes in focus will be significant.

Since many expect rate cuts later in the year, dates after July are becoming more important. Current forward guidance is uncertain, but by mid-summer, it will be clearer if inflation is decreasing enough for looser policy. For now, traders should reassess rate expectations after carefully reviewing both the written statement and the news conference. Keep an eye out for mentions of domestic consumption as a weakness and whether this concern overshadows risks from external shocks.

Underlying volatility, especially in short-term plays, could benefit from a wider range of tolerance. If inflation metrics remain steady into the June reports, the likelihood of a change increases.

The economic situation—a mix of weak demand and high prices—limits the ability for significant cuts or large increases. Markets can expect careful steps assessed over time. Macro exposures may respond more to language than to actual moves, so positioning should be reconsidered if it’s too heavily weighted in one direction. Any change in communication style could matter more than a small adjustment in the overnight rate.