East West Bancorp reports $758.25 million in revenue and $2.52 EPS for the fourth quarter, showing year-on-year improvement

East West Bancorp (EWBC) announced its Q4 2025 revenue at $758.25 million, marking a 12.2% rise from last year. Earnings per share (EPS) reached $2.52, up from $2.08 during the same quarter last year.

Revenue beat the Zacks Consensus Estimate by 1.32%, while EPS exceeded expectations by 1.61%. Key figures show a stable net interest margin of 3.4% and an annualized net charge-off rate of 0.1%.

The efficiency ratio was 34.5%, slightly lower than the estimated 35.2%. The bank had a leverage ratio of 11% and an average balance of total interest-earning assets at $76.64 billion.

Total nonaccrual loans were $165.84 million, above the estimated $158.73 million. The total nonperforming assets reached $208 million, higher than the expected $192.73 million.

East West Bancorp’s adjusted efficiency ratio was 35.2%, while the total capital ratio stood at 16.4%. The Tier 1 capital ratio was 15.1%, exceeding the estimated 15%.

Noninterest income was $100.43 million, and net interest income was $657.82 million, both surpassing analyst expectations. Over the past month, East West Bancorp’s share price rose by 0.1%, compared to a 0.7% increase in the Zacks S&P 500 composite.

As of January 23, 2026, the Q4 2025 earnings report presents a mixed scenario for East West Bancorp. The bank exceeded analyst projections for both revenue and EPS, but some credit metrics signal caution. Such conflicting reports often lead to stock price stagnation or higher volatility rather than clear upward movement.

On the positive side, current profitability looks strong, and operational management remains effective. The efficiency ratio of 34.5% was better than expected, and net charge-offs were only half of what analysts feared. This indicates that, so far, loan losses are well-controlled.

However, it’s important to consider the increase in total nonperforming assets. At $208 million, this figure was significantly above analysts’ expectations of $192.73 million, suggesting that while losses are low now, more loans may be under stress. This creates a tension between the bank’s solid current performance and a potentially less certain future.

This situation is especially relevant in the context of the broader economic landscape from late 2025. The commercial real estate market remained weak, with national office vacancy rates hovering around 20%, putting pressure on the bank’s loan portfolios. This economic backdrop makes the rise in EWBC’s nonperforming loans more concerning.

Investors are also wary due to increased scrutiny of regional bank credit quality after the troubles of 2023. As a result, the market may temper its excitement over the earnings beat, focusing instead on the risks of future credit issues. The stock has underperformed compared to the S&P 500 over the past month, indicating this cautious sentiment.

Looking ahead, this mixed outlook suggests strategies that could benefit from a stable stock price or an increase in volatility. Selling covered calls on existing stock positions could be a smart way to generate income, as the rise in nonperforming assets might limit major gains. Alternatively, for those expecting a significant price movement once the market assesses these mixed signals, a long straddle could take advantage of a sharp swing in either direction.

The manufacturing business climate in France surpassed expectations, reaching 105 rather than 101.

The manufacturing sector in France showed improvement in January, reaching a reading of 105. This is better than the expected 101, indicating a positive outlook for manufacturing despite broader economic conditions.

This rise highlights the sector’s strength and might contribute to future economic growth in the area. Market participants will keep an eye on this trend, as it could influence future policies and economic activities.

French Equities Reaction

With the stronger manufacturing climate in France, we can expect a positive response in French equities. Traders might consider buying call options on the CAC 40 index or on individual companies like Schneider Electric or Airbus to take advantage of potential gains in the coming weeks. This encouraging sign from a major Eurozone economy points to economic resilience. This marks a significant change from last year, when the HCOB Manufacturing PMI for France struggled just below the 50 mark in the fourth quarter of 2025. The new reading indicates that companies are looking beyond earlier challenges and are feeling more positive about future orders and production. This shift in attitude could be a strong catalyst that derivative markets may have underestimated.Euro and ECB Stance

This data might bolster the euro since it reduces the pressure on the European Central Bank to consider rate cuts. With Eurostat showing core inflation steady at around 2.4% at the end of 2025, this strong activity in France makes a more aggressive ECB stance likely. We might see opportunities in long EUR/USD futures contracts, betting on the euro strengthening against the dollar. Historically, in mid-2023, unexpectedly strong service sector data in the Eurozone led to a multi-week rally in European indices before a market correction. This suggests that the current manufacturing data might spark a similar short-term trend, making it a good time to establish long positions in derivatives tied to European cyclical stocks. It is essential to see if this strength is confirmed by the upcoming German IFO Business Climate report. Following this positive surprise, implied volatility on French stocks may temporarily rise before stabilizing if a clear upward trend takes shape. This presents an opportunity for traders to sell volatility. Selling put options on strong French industrial companies at a lower strike price could be a smart strategy to earn premiums while adopting a cautiously optimistic outlook. Create your live VT Markets account and start trading now.XAG/USD rises to new highs over $99.00 during Asian trading hours

Silver prices climbed to a new high of $99.39 per troy ounce on Friday, trading around $99.10 during Asian market hours. The XAG/USD pair stays above the rising nine-day EMA, bolstered by a strengthening 50-day EMA, indicating a continued upward trend.

Technical indicators, like the 14-day RSI at 74.66, point to overbought momentum, which might lead to a pause in price growth. Despite these conditions, the uptrend continues unless the price falls below the short-term moving average. If silver holds above $99.80, it could reach $100.00.

If the price decreases, support may form around the nine-day EMA at $92.42. A drop below this level could lead to further declines toward the channel’s lower boundary at about $82.00, with additional falls potentially bringing the price near the 50-day EMA at $73.14.

Silver is important in various fields, like electronics and solar energy. Its price is affected by changes in the US Dollar, industrial demand, geopolitical issues, and economic situations in the US, China, and India. Silver often moves alongside gold, with the Gold/Silver ratio indicating their relative worth.

Looking back, silver prices peaked around $99.39 last year, showing a strong upward trend on the daily chart. At that time, the 14-day RSI above 74 indicated the rally was too strong, leading to a significant price consolidation in the second half of 2025.

As of January 23, 2026, silver is trading near $75.00, aligning with the important 50-day moving average support from last year’s high. Following recent softer US inflation data at 2.8% for December 2025, market consensus is leaning toward a Federal Reserve interest rate cut in the second quarter. This scenario makes long-dated call options on silver an attractive strategy, as lower rates often benefit non-yielding assets.

The outlook for industrial demand remains positive, which was a major factor previously. Reports indicate that global solar panel installations rose by 22% in 2025, a trend likely to continue as energy policies shift toward renewable sources. Silver is a key component in photovoltaic cells, ensuring steady industrial use that supports prices.

Additionally, the gold-to-silver ratio has increased significantly since the 2025 price peak, now around 88:1, well above its historical average. This suggests silver may be undervalued compared to gold, providing a potential opportunity for traders looking for assets with greater upside. There is a chance that a reversion to the mean could spark a substantial rally in silver.

With prices holding near the critical long-term support level of $73.14 highlighted in last year’s analysis, traders should keep a close eye on this area. A definitive break below this level could indicate more weakness, making protective put options a wise hedging strategy. However, as long as this support remains intact, the technical and fundamental outlook seems positive for the upcoming weeks.

BoJ Governor Kazuo Ueda explains reasons for keeping the interest rate at 0.75% during press conference

Bank of Japan (BoJ) Governor Kazuo Ueda decided to keep the key interest rate at 0.75% during the January policy meeting. Japan’s economy is recovering moderately and growing, supported by a government economic package.

Inflation is expected to rise slowly, with consumer prices likely to increase gradually. Wages and inflation are expected to rise together, and inflation expectations for the medium to long term are also increasing.

Japan’s Financial Stability

Despite uncertainties in the global economy and trade policies that could affect import prices, Japan’s financial system remains stable. Predictions for Japan’s GDP growth in upcoming fiscal years have improved slightly. The BoJ intends to normalize its monetary policy by assessing the effects of the interest rate hike in December. Governor Ueda highlighted the importance of monitoring how foreign exchange rates affect prices. The USD/JPY has seen gains, reflecting market expectations regarding BoJ policies. Yen volatility continues due to market speculations about potential political changes and economic policies. The BoJ might indicate further tightening based on economic forecasts, but upcoming elections add uncertainty to their policy decisions.Explaining Economic Terminology

Economic terms are clarified, including interest rates and their effects on currencies, such as how the Yen responds to BoJ decisions. The global economic climate and its potential effects on gold prices and market behavior are also considered. The Bank of Japan has kept interest rates at 0.75%. However, they may raise rates if the economy continues to improve. Governor Ueda is clearly worried about the weak Yen’s impact on prices, indicating that foreign exchange rates are a key focus. This cautious yet assertive approach suggests that they are currently patient but likely to tighten policies further. The immediate market reaction showed the Yen weakening, with USD/JPY approaching 158.60, as traders sought a stronger commitment to a near-term rate hike. This trend could lead the pair to test multi-decade highs near 159.50 seen last week. As long as the BoJ remains patient, derivative traders might prefer strategies that profit from further, gradual Yen depreciation. Recently, Tokyo Core CPI data, an important indicator for national inflation, came in at 2.5% for January. This rate is still above the BoJ’s 2% target, indicating that inflation pressures are not easing quickly. This persistent inflation strengthens the case for the BoJ to act sooner, adding risk for those heavily betting against the Yen. Attention is now on the upcoming “Shunto” spring wage negotiations, which Governor Ueda pointed out as essential for a potential rate hike around April. Major unions are seeking pay raises over 5.5%, building on strong negotiations in 2024 and 2025. Strong wage growth would likely lead to another rate hike, boosting the Yen. We should also consider the risk of direct intervention in the currency market by the Ministry of Finance. In 2024, officials intervened to buy Yen when USD/JPY exceeded 160, causing sharp reversals. With the pair nearing this crucial level again, the risk of intervention is high and could happen suddenly. Current speculative positioning shows that shorting the Yen is a very popular trade, making it susceptible to a sharp reversal. Given the BoJ’s assertive tone and the rising risk of intervention, traders should brace for increased volatility in the coming weeks. Strategies like buying straddles or strangles on USD/JPY, which benefit from large price changes, might be wise. Create your live VT Markets account and start trading now.The US Dollar Index stabilizes below 98.50 after recent declines amid risk aversion

The US Dollar Index is currently below 98.50. This is due to traders feeling cautious and waiting for the US S&P Global PMI report. After dropping by 0.5% in the last session, the Index remains around 98.30 in the Asian markets.

The US GDP grew by 4.4% in Q3 2025, slightly exceeding expectations and a previous reading of 4.3%. Initial Jobless Claims fell to 200,000, which is lower than the predicted 212,000.

PCE Price Index Update

The PCE Price Index rose to 2.8% annually in November, compared to 2.7% in October, reflecting a 0.2% monthly increase. The Core PCE Price Index also met expectations at 2.8%, following October’s 2.7%. Geopolitical tensions between the US and Europe are creating challenges for the US Dollar. There is speculation about a possible agreement between the US and NATO regarding mineral rights, as a Danish pension fund plans to pull out of US Treasuries. The Federal Reserve is likely to keep interest rates steady, with a 95% chance of a rate cut in December. The Fed affects the USD mainly through its monetary policies, including quantitative easing and tightening. The US Dollar is the world’s main reserve currency, representing over 88% of foreign exchange transactions, with average daily trading reaching $6.6 trillion.Market Reactions And Strategies

The US Dollar Index is around 98.30 and shows weakness despite the strong GDP figures for Q3 2025. With the US S&P Global PMI data expected today, we could see short-term volatility. This might mean that buying straddles or strangles on major currency pairs like EUR/USD could be a smart strategy for trading the upcoming data. The market expects a December rate cut, with a 95% chance factored in. However, this seems out of sync with the November core PCE data, which held steady at 2.8%. The aggressive rate hikes in 2023, when inflation was high, suggest the Federal Reserve might hesitate to ease policies just yet. This difference could create opportunities in interest rate futures, especially for betting against such a dovish outlook. The rising geopolitical tension with Europe, especially with the Danish pension fund selling US Treasury holdings, is a major factor in the current risk aversion. Since European countries held over $1.5 trillion in US debt by late 2024, more divestment could put additional pressure on the dollar. To hedge against this uncertainty, consider buying call options on gold or the Swiss Franc, which usually perform well in such situations. We need to balance the strong economic indicators, like low initial jobless claims of 200,000 and solid GDP growth of 4.4%, with the prevailing cautious market sentiment. This split suggests the dollar’s current weakness may not last long. A longer-term bullish position on the dollar could be taken by purchasing DXY call options that expire in the next quarter. Create your live VT Markets account and start trading now.AUD/JPY strengthens around 108.55 as Yen weakens after BoJ’s decision

The AUD/JPY exchange rate is currently around 108.55 in early European trading. The Japanese Yen is losing strength against the Australian Dollar because the Bank of Japan has decided to hold its interest rates steady.

The Bank of Japan has kept the rate at 0.75%, which is the highest it’s been in 30 years. A proposal from board member Hajime Takata to raise rates again did not receive support, even though the bank seems to be leaning towards tighter policies.

Economic Growth Potential

The outlook from the Bank of Japan is positive, with projections for economic growth in 2025 and 2026. Their stance reflects an expectation of a moderate economic recovery. According to technical analysis, AUD/JPY remains above its 100-day EMA at 102.07, indicating strong bullish momentum. However, the Relative Strength Index (RSI) is at 77.21, suggesting that the pair may be overbought. Any pullbacks may aim for the Bollinger middle band at 105.85, with further support at 103.62. The expanding Bollinger bands indicate rising volatility and the potential for trend acceleration. Since 2013, the Bank of Japan has changed its monetary policy approach by moving away from ultra-loose policies. This decision was driven by the weaker Yen and rising inflation above their 2% target.Yen’s Weakness and AUD’s Strength

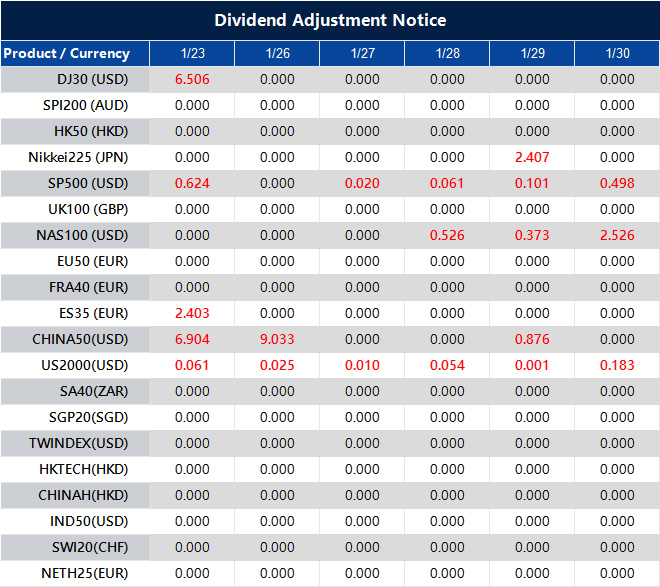

The AUD/JPY exchange rate is climbing around 108.55 after the Bank of Japan announced it would keep interest rates at 0.75%. This decision was anticipated and confirms the Yen’s weakness as the BoJ seems less aggressive than other central banks. This ongoing policy divergence continues to influence the pair. While the trend appears bullish, caution is warranted since the daily chart indicates overbought conditions. The RSI is above 77, a level that often signals a price correction or a consolidation phase. Buying at these high levels poses significant risks of a pullback to the 105.85 support level. The Australian dollar is benefiting from strong commodity prices. Recent data from January 2026 shows iron ore prices stable above $140 per tonne. Coupled with the Reserve Bank of Australia’s hawkish tone throughout late 2025, this provides a solid backing for the AUD’s strength. In contrast, the BoJ’s careful approach is evident. Japan’s latest inflation report from December 2025, showing core CPI at 2.1%, has allowed the BoJ to pause its rate hikes. After three rate increases in 2025, this pause indicates the central bank is waiting for more information before considering further tightening. This uncertainty is currently putting pressure on the Yen. In the upcoming weeks, it would be wise to consider derivative strategies that safeguard against a short-term pullback. Options like buying calls with a higher strike price or using call spreads could allow for continued upside while managing costs and risks. However, selling uncovered puts is risky given the market’s current overextended state. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 23 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Gold prices increase in the Philippines, according to market data.

Gold prices in the Philippines rose on Friday, according to FXStreet. The price per gram increased from 9,337.37 PHP to 9,412.67 PHP. Meanwhile, the price per tola went up from 108,909.30 PHP to 109,787.40 PHP.

Gold prices in the Philippines reflect international market trends, adjusted to the local currency at the USD/PHP exchange rate. These rates are updated daily and reflect current market conditions, though actual local prices might differ.

Gold as a Safe Investment

Gold has long been seen as a reliable investment, especially during tough economic times. It’s also viewed as protection against inflation and currency loss. Central banks, particularly in emerging economies like China and India, increased their gold holdings by purchasing 1,136 tonnes in 2022. Gold prices often rise when the US Dollar weakens, as they tend to move in opposite directions. Geopolitical tensions and changes in interest rates also affect gold prices. A strong Dollar usually keeps gold prices down. The recent price rise in gold reflects uncertainty in the market. Persistent inflation throughout 2025 has led to disagreements about the Federal Reserve’s interest rate plans. For traders, gold’s connection to the US Dollar is crucial to watch in the coming weeks. We should also note the ongoing demand from official sources, which helps maintain higher prices. The World Gold Council reported that central banks worldwide added over 950 tonnes to their reserves in 2025, following record purchases in previous years. This steady buying trend, mainly from emerging markets, suggests that any price drops will likely find solid support.Effect of Rate Expectations on Gold

Gold, which doesn’t generate income, is highly sensitive to interest rate changes. This creates opportunities for derivatives traders. The unexpectedly strong US jobs report from December 2025 reduced the chances of a rate cut in the first quarter, temporarily halting gold’s price rise. This mixed market outlook is increasing implied volatility, making strategies like options straddles potentially profitable for traders anticipating big price swings in either direction. We should also keep an eye on gold’s relationship with riskier investments. The S&P 500’s surge to new highs in late 2025 has drawn some investments away from precious metals. Signs of weakness or profit-taking in stock markets could lead to a quick move toward gold as a safe haven. Holding long-term gold call options may be a good hedging strategy against possible stock market downturns. Create your live VT Markets account and start trading now.Singapore’s Consumer Price Index meets expectations at 1.2% year-on-year in December

The Singapore Consumer Price Index (CPI) for December is 1.2%, matching what experts expected. This number shows how consumer prices have changed over the year and reflects the cost of everyday goods and services in Singapore.

A steady CPI indicates stable inflation, which may influence future decisions by the Monetary Authority of Singapore (MAS). Economists analyze such data to understand the current economy and predict future trends.

Importance of CPI Data

CPI data is crucial for local decision-makers, traders, and those tracking inflation to adjust their strategies. It acts as an essential economic indicator, offering insights into consumer behavior and signaling possible economic growth or problems. Future economic events and data will continue to shape Singapore’s financial landscape and the global economy. The December 2025 CPI figure of 1.2% aligns perfectly with expectations, reducing the chances of market fluctuations. This confirms that inflation in Singapore is under control, suggesting current market trends are likely to remain stable. With this steady inflation data, the Monetary Authority of Singapore (MAS) has little reason to change its currency policy soon. Recall that during its last meeting in October 2025, the MAS decided to maintain a gradual appreciation of the Singapore dollar. Current data makes any policy changes unlikely at the next meeting in April.Global and Local Economic Context

Looking at the global situation, recent US inflation data showed a slight decrease to 2.8%. This lowers the chances of sudden interest rate changes by the US Federal Reserve, helping to stabilize capital flows and keep currency markets, including the Singapore dollar, calm. For derivative traders, this stable environment suggests low volatility will continue. One-month implied volatility on USD/SGD options is currently at about 3.5%, near historical lows. This scenario favors trading strategies that benefit from steady price movements, like selling option straddles for premium collection. We expect no significant surprises in the Singapore dollar in the coming weeks. This forecast is backed by Singapore’s fourth-quarter 2025 GDP data, which showed a moderate year-on-year growth of 2.1%. The combination of steady growth and low inflation is often referred to as a “Goldilocks” scenario, meaning central bank actions are less likely. Therefore, we anticipate the Singapore dollar will trade within a stable range against its major partners. Create your live VT Markets account and start trading now.Gold prices increase in the United Arab Emirates, according to recent data sources

Gold prices in the United Arab Emirates rose on Friday, according to FXStreet data. The price climbed to 585.22 AED per gram, up from 580.57 AED the day before.

For a tola, the price increased to 6,825.95 AED from 6,771.68 AED. Gold prices in the UAE are adjusted daily to reflect international rates and converted to AED.