The NZD/USD pair consolidates around 0.5950, pausing its recent gains.

NZD/USD is currently trading at around 0.5930, moving within a stable range. The pair aims for the upper limit near 0.6000, with initial support from the nine-day Exponential Moving Average (EMA) set at 0.5913.

The Relative Strength Index (RSI) shows a slight upward trend, staying above 50. If NZD/USD breaks above 0.6000, it could target the six-month high of 0.6038, which was reached in November 2024.

WTI oil trades lower around $62.00 as markets evaluate the impact of Russia-Ukraine peace talks on supply.

WTI oil prices are currently under pressure, trading at about $62.00 per barrel after some recent increases. This drop is linked to possible ceasefire discussions between Russia and Ukraine, which could lead to a larger global oil supply.

A ceasefire might ease sanctions on Russia, potentially increasing its oil exports, especially in a market that is already oversupplied. Additionally, a downgrade of the US credit rating by Moody’s and weak economic indicators from China have added to the negative outlook.

Impact of Economic Factors on Oil Demand

China’s central bank has cut interest rates to historic lows to boost its economy, which may indirectly affect oil demand. At the same time, tensions continue between the US and Iran over nuclear issues. WTI Oil, or West Texas Intermediate, is a key benchmark for oil prices due to its high quality, which requires less refining. Key factors that affect WTI prices include global demand, geopolitical issues, decisions made by OPEC, and the strength of the US Dollar. Reports on oil inventories from the API and EIA can greatly influence WTI prices, with lower inventories suggesting higher demand. OPEC and OPEC+ decisions on production quotas also have a significant impact on supply and oil prices. OPEC is crucial in adjusting supply based on their production quotas. These various elements shape the global oil market and influence WTI pricing.Challenges in the Global Oil Market

Recent market trends show a more fragile environment for energy commodities. With WTI prices around $62.00 per barrel, there’s a noticeable shift in market feeling. A lot of this is due to renewed talks about a ceasefire between Russia and Ukraine. The market is starting to factor in the chance of easing tensions, which means Russian oil could be more freely available, leading to higher supply and lower prices if demand doesn’t match. The recent downgrade of the US credit rating by Moody’s also casts a shadow over riskier assets. It raises borrowing costs and could slow down industrial growth and energy use. When capital costs go up, investment typically falls, affecting fuel use in sectors like manufacturing and freight. Furthermore, economic weakness in China adds to the concern. With interest rates at all-time lows, it seems the People’s Bank of China is running out of traditional ways to boost demand. Despite their efforts, consumer confidence remains shaky. This is critical since China is a major crude importer. A decline in their demand will hurt upstream producers. The ongoing tensions between the US and Iran over nuclear issues also create uncertainty. These tensions can sometimes drive prices up due to supply fears, while at other times they create unpredictability. For those monitoring price volatility, continued uncertainty about Middle Eastern oil exports usually prevents prices from stabilizing, especially when optimistic expectations fall flat. For those following West Texas Intermediate futures, the evidence is leaning toward further price declines unless significant changes occur. In futures trading, timing and positioning are important, especially when expectations diverge from physical supply adjustments. Weekly inventory reports gain importance here. Any unexpected drop in inventories, especially in the EIA’s Thursday report, could create a temporary bounce, but one should be cautious about how long any rally lasts without supporting actions or supply reductions. Currently, the OPEC+ group must carefully consider its production plans. Setting quotas can help control overproduction, but it requires strict discipline. If key members do not comply or if external producers increase exports to take advantage of gaps, the effectiveness of their strategy could diminish quickly. Thus, it is crucial to analyze compliance levels alongside announced targets when looking at future price trends. Currency fluctuations also play a vital role. As the US Dollar strengthens amid global uncertainty, oil becomes more expensive for holders of other currencies. This can reduce demand from price-sensitive countries. The link between a strong dollar and weak commodity prices remains important. Overall, options and calendar spread positioning should be based on solid data rather than headline news. Previous scenarios show that expectations of rising prices often fade when the physical market indicates a surplus, combined with weak industrial demand and cautious central bank actions. Currently, near-term risks seem skewed toward decline unless unexpected geopolitical events suddenly tighten supply. Create your live VT Markets account and start trading now.US stocks rose as Emini S&P surpassed 5890, reaching the predicted targets of 5925/30 and 5950/60.

Emini Dow Jones Potential Movement

The EUR/USD stayed above 1.1250 as the US Dollar weakened. The GBP/USD found support and tested 1.3400 amid trade uncertainties. Gold prices remained above $3,200 despite some daily losses. Hopes for a possible ceasefire between Russia and Ukraine lifted cryptocurrencies, while mixed economic results in China in April were influenced by ongoing trade tensions. Equities tested familiar resistance levels before retracing to find support, aligning well with technical setups. The S&P e-mini hit the 5960/65 resistance area again. It briefly pushed above 5980 to touch 5993 but quickly retreated, hinting that buyers weren’t very committed, likely due to overbought conditions. The low of the day at 5893 matched the previous day’s low, creating what appears to be a near-term support level. If the price remains above 5950 or 5965, we could see another attempt to reach key levels like 6000 or even higher, depending on momentum. However, if it drops and stays below 5950, we might see early weakness, potentially testing the 5910 level again or even lower.Nasdaq Support Analysis

The Nasdaq reacted predictably. The region around 21200/21100 was on our radar, and prices bounced right off it, making these levels valid for future retests. Traders could have made over 400 points on long positions if managed within risk limits and with sensible stop-loss orders below 20950. Now, we need to watch how the index reacts if it breaks below 21100. The next key support zone would be 20840/820, and 20650/600 becomes important if the weakness persists. In the Dow e-mini, we moved from the 42470/430 range to a high near 42950. This movement met our expectations and indicated further upside towards 43100/150. However, if it falls back below 42300, it could put pressure on the index, dragging it down to 41950/850. Traders might then start adjusting their positions, especially if volatility rises. Shifting our focus to currencies, the Euro held comfortably above 1.1250, owing to consistent pressure on the Dollar. Buying interest is present, though not aggressive, and as long as this support holds, the pair could rise if the Dollar weakens. For Sterling, the 1.3400 level attracted interest due to recent trade policy uncertainty, particularly from the UK. Positioning around this figure may tighten for now as we await more clues from macroeconomic news or central bank updates. Gold continues to show strength, staying above $3,200 despite some daily fluctuations. Investors seem to be holding their positions as a hedge against broader tensions. Although there hasn’t been a breakout, we shouldn’t overlook its staying power, especially with ongoing concerns about global inflation. Digital assets found support from talks of peace between Russia and Ukraine. Soft remarks from Fed officials also provided a slight boost. In Asia, mixed economic data from China has left regional trade forecasts inconsistent. These numbers suggest that a full economic rebound isn’t imminent, and traders focusing on commodities should keep this in mind for long-term strategies. Looking ahead, technical patterns suggest we may see moderate trading ranges rather than sharp breaks. Support and resistance zones continue to create a viable trading structure. How these levels hold or fail will define trade setups. Recognizing when to maintain a directional approach versus reverting to range strategies could be crucial, especially with ongoing external developments. Create your live VT Markets account and start trading now.The US Dollar Index hovers near a week’s low, consolidating around 100.35

The US Dollar is having a tough time gaining strength as traders expect more interest rate cuts from the Federal Reserve in 2025. This follows recent reports showing softer US consumer and producer price indexes, along with disappointing retail sales figures.

The US Dollar Index is barely moving around the 100.35 mark, close to recent lows. The recent downgrade of the US credit rating is putting extra pressure on the dollar.

Factors Affecting The US Dollar

Reductions in US-China tariffs have eased fears of a recession, preventing traders from betting heavily against the dollar. Positive comments from Federal Open Market Committee (FOMC) members are also supporting the dollar. No significant economic data is set to be released on Tuesday, so attention will be on upcoming speeches from FOMC members, which may significantly impact the dollar. In currency trading, the dollar has performed unevenly, rising the most against the Australian Dollar. A heat map shows the percentage changes of key currencies against each other throughout the day. Navigating the risks and volatility in currency exchange is essential. Careful research is advised before making any investment decisions. The US Dollar is currently in a quiet phase, influenced mostly by changing expectations around interest rates. Recent inflation readings, including consumer and producer prices, have been lower than anticipated. These figures, combined with weak retail spending, have lessened interest in the dollar, as many traders are now betting that the Federal Reserve will cut rates in the coming year. The US Dollar Index remains around 100.35, close to its recent lows, and shows little sign of rising. Its troubles are compounded by a downgrade in the US national credit rating, which can shake investor confidence in the dollar’s strength. However, there are some positive signs. Easing US-China tariffs seem to have calmed some recession fears, preventing traders from heavily betting against the dollar for now. Additionally, comments from FOMC members suggest they may not rush to cut rates, which is keeping the dollar stable, at least temporarily.Monitoring Market Developments

There is no major economic news expected on Tuesday, shifting focus to upcoming speeches from Fed officials. In quieter market conditions, these speeches can greatly influence movements. When comparing the dollar to other currencies, the results are mixed. It has gained the most against the Australian dollar, likely due to recent weaknesses in commodities and demand from China. A heat map visually displays these changes, helping traders understand currency performance. Currently, the market is in a phase where careful strategies are essential. With the dollar stuck in a narrow range, swings in value are increasingly tied to comments from monetary authorities rather than data itself. This makes short-term price movements harder to predict and more sensitive to subtle messages. As things stand, trades made without clear momentum carry a higher risk of reversal, especially in pairs where interest rate differences are changing. Knowing that central banks are sticking to their guidance makes their speeches crucial for shaping expectations. Traders should stay alert and ready to react. Create your live VT Markets account and start trading now.After the May policy announcement, RBA Governor Bullock hinted at possible future adjustments.

The Reserve Bank of Australia has lowered the benchmark interest rate by 25 basis points to 3.85%, down from 4.1%. This move is part of their strategy to control inflation and comes amid discussions about rate changes and market stability issues.

Following this announcement, the Australian Dollar responded by trading lower. The AUD/USD pair is now around 0.6430, marking a decrease of 0.39% for the day. The decision was made collectively, showing discussions about various rate cut options.

Factors Influencing The Australian Dollar

Several key factors influence the Australian Dollar. These include the interest rates set by the RBA, iron ore prices, and the economic condition of China. When iron ore prices are high or when Australia has a strong trade balance, the AUD tends to strengthen. Changes in China’s economy can also affect the value of the Australian Dollar. Strong growth in China increases demand for Australian exports, boosting the AUD. On the other hand, slower growth in China can weaken the currency. Iron ore, which is Australia’s biggest export, greatly influences the AUD. When iron ore prices rise, the AUD usually follows suit, especially if Australia’s trade balance is positive. A positive trade balance means there is more demand for Australian exports, which strengthens the currency. The Reserve Bank’s decision to lower rates to 3.85% indicates a move towards easing financial conditions to tackle inflation, which remains above target. By reducing borrowing costs, they aim to support economic activity while controlling price pressures. Recent inflation data has been high, but signs of a cooling labor market and declining retail spending likely prompted this more cautious approach.Market Reactions and Expectations

Market expectations had already indicated a potential easing, meaning traders had anticipated this decision to some extent. However, the immediate drop in the Australian Dollar suggests that traders may have underestimated the magnitude or timing of this change. The AUD/USD’s slip below 0.6450 indicates that interest rate differences are becoming more significant, especially as other central banks, notably the US Federal Reserve, maintain tighter policies, putting additional pressure on the Australian currency. This reflects the AUD’s continued sensitivity to commodity price changes and demand from China. It’s not just about watching iron ore prices anymore; they now signal current and future demand trends. China’s GDP growth targets, manufacturing output, and construction data are now major factors affecting the AUD, particularly given China’s cautious approach to monetary easing. Iron ore remains a key indicator of Australia’s export strength, and with ongoing geopolitical uncertainty affecting global risk sentiment, it may be wise to adopt short strategies during negative news cycles, especially when Chinese demand data falls short of expectations. However, caution is needed if iron ore prices hold steady despite poor economic data, as this could give rise to misleading signals. Traders in derivatives are experiencing high implied volatility, indicating uncertainty over upcoming data releases such as China’s PMI, inflation reports, and supply chain issues, which could lead to significant market adjustments. If implied volatility decreases without any real improvement in trade data or commodity flows, it may suggest overly optimistic market sentiment rather than true progress. With the RBA’s rate decision now in the past, future expectations are becoming crucial for trading. Risk reversals in AUD options are showing a preference for more downside, indicating both trading opportunities and caution in current market conditions. Traders should be ready to alter short-term strategies, as even small economic surprises from China or commodity exporters can lead to sharp market movements, especially around key support levels below 0.6400. In this environment, new buyers entering AUD positions will likely depend on improvements in Chinese data or further coordinated actions from Australian policymakers. Essentially, this is a time where tactical positioning could perform better than long-term strategies. It’s essential to stay aware of market liquidity and variability around major global economic data, as we approach the next few weeks of trade balance and employment statistics. Create your live VT Markets account and start trading now.Crude Oil Steadies As Market Evaluates Diplomatic Developments

Crude oil prices saw little movement on Tuesday, with July contracts for West Texas Intermediate (WTI) edging down to $61.97, while Brent futures for July hovered around $65.35. The market remains in a state of indecision, balancing between international diplomatic efforts, robust demand across Asia, and a somewhat unclear economic outlook from both China and the United States.

A major source of uncertainty lies in the ongoing US-Iran nuclear negotiations. Tehran’s Deputy Foreign Minister warned that talks could stall should Washington insist on fully ceasing uranium enrichment, one of the key sticking points in reviving the 2015 nuclear deal.

A successful deal could unleash an estimated 300,000–400,000 barrels per day of Iranian supply, according to StoneX.

Elsewhere, physical demand in Asia remains strong. Refineries across the region ramp up post-maintenance production, supported by favourable refining margins. Singapore’s refining margins, a key regional gauge, averaged over $6 per barrel in May, up sharply from April’s $4.40. This reflects healthy profit levels likely to sustain near-term buying interest.

However, upward momentum is limited, as traders weigh broader macroeconomic concerns. The recent downgrade of US sovereign debt by Moody’s has added to existing worries about global growth prospects, particularly for the world’s top oil consumer. Alongside disappointing industrial production and retail sales figures from China, questions are mounting over the resilience of the global oil demand recovery.

BMI’s forecast further reinforces this caution, with analysts now expecting a 0.3% year-on-year decline in China’s 2025 oil consumption. “Even if China adopts stimulus measures, it may take time to have a positive impact on oil demand,” they warned in a note.

Energy markets are also keeping a close eye on any potential developments in Russia-Ukraine peace talks. According to ING, any diplomatic breakthrough could result in sanctions being eased, potentially allowing Russian oil back onto international markets, thereby further pressuring supply dynamics.

Technical Analysis

WTI crude is currently rangebound, consolidating after rebounding from the support level at $60.983 and touching a recent high of $62.683. Price action on the 15-minute chart has flattened out, with candles compressing just above the 30-period moving average. The short-term moving averages (5 and 10) are converging, signalling a loss of directional momentum.

The MACD histogram shows waning bullish momentum, with a potential crossover developing near the zero line—suggesting buyers may be losing steam. However, price remains above the mid-range support zone near $61.80, hinting at stability for now. Resistance stands at $62.30–62.70, while a break below $61.80 could expose the lower bound near $61.07.

If bulls can reclaim and close above $62.30, we may see renewed upside attempts. Otherwise, the bias remains neutral to slightly bearish intraday.

Cautious Forecast

With prices oscillating between $60.98 and $62.68, WTI remains firmly within a consolidation zone. A push towards recent highs seems unlikely without clearer signals from either diplomatic developments or key economic data. Traders are encouraged to stay nimble, keeping a close eye on Washington and Beijing, as well as any tangible progress on the geopolitical front.

Create your live VT Markets account and start trading now.

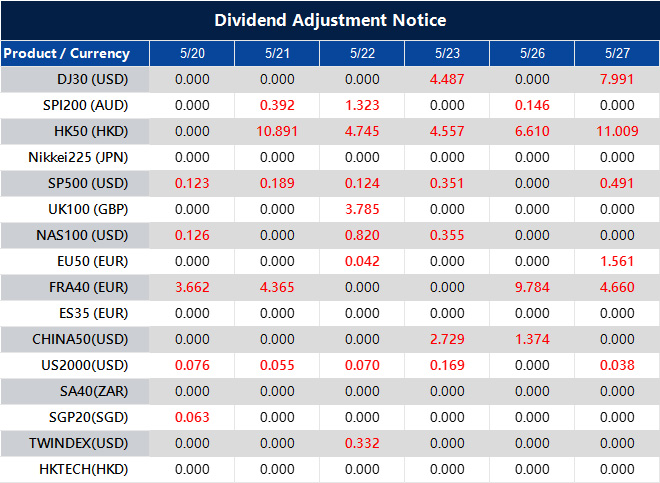

Dividend Adjustment Notice – May 20 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Selling pressure increases on AUD/JPY near 93.00 as the RBA’s interest rate decision is revealed

**Speculation on BoJ Interest Rate Hikes**

The AUD/JPY is currently trading near 93.00, down 0.55% during Tuesday’s Asian session. This follows the Reserve Bank of Australia’s (RBA) decision to reduce the Official Cash Rate by 25 basis points to 3.85% in May.

The Australian Dollar has weakened as attention shifts to RBA Governor Michele Bullock’s upcoming press conference. The RBA is concerned about rising global trade tensions affecting the economy, noting a lower forecast for global growth due to US tariff policies.

There’s increasing speculation about possible interest rate hikes from the Bank of Japan (BoJ) this year, which is supporting the Japanese Yen. BoJ Deputy Governor Shinichi Uchida anticipates that inflation in Japan will rise, implying that further rate increases might follow if the economy and prices improve.

The RBA’s goal is to manage monetary policy to ensure price stability and economic welfare, mainly through interest rate changes. Higher interest rates generally strengthen the Australian Dollar, while quantitative easing (QE) and tightening (QT) are additional measures the RBA can take to influence the economy.

Macroeconomic indicators like GDP and employment rates affect currency values. A strong economy typically leads to higher interest rates. Even though rising inflation often weakens a currency, it can now attract capital and boost it by leading to interest rate increases.

**RBA’s Influence on AUD/JPY Trades**

The AUD/JPY pair is slipping toward 93.00, showing a clear loss of momentum linked to the RBA’s recent decision. By lowering the Official Cash Rate to 3.85%, the central bank broke away from the trend seen recently, adopting a more cautious stance amid external uncertainties. This shift in rates signals a response to market uncertainty, which is reflected in the weakening of the Aussie.

As speculation grows, it’s important to consider not just the RBA’s actions but also their future plans. Concerns over global trade tensions, primarily driven by US tariff strategies, complicate the macro landscape. The RBA’s current stance appears somewhat defensive, and investors are keenly watching for signs of further easing. Bullock’s comments in the press conference suggest that the board is more focused on external risks than domestic factors. If these worries persist, rate increases from the RBA may be limited for now, possibly indicating a longer pause.

Turning to Japan, inflation expectations are becoming clearer. Uchida’s remarks offer direction for the BoJ, which has typically been slow to respond. If inflation pressures continue to build, we may see a quicker normalization of policy. With inflation likely remaining above 2% and markets expecting the BoJ to adapt, the Yen could continue to attract capital in the coming months. Market pricing shows that even cautious rate hikes are being taken seriously now.

Given this context, it’s wise to reassess the approach to carry trades. The narrowing yield gap between the Australian and Japanese currencies is becoming practical, not just theoretical. As Australian rates trend lower or stabilize, and Japan’s policy may shift, long positions in both currencies may lose appeal. The risk-to-reward ratio in these trades could diminish quickly if the BoJ acts sooner than anticipated.

We should also pay closer attention to employment data and inflation metrics for better positioning. In past cycles, inflation that exceeds predictions has led to rapid shifts in market pricing. This creates volatility that short-dated options traders can take advantage of. However, key macro events like Australia’s employment numbers or Japan’s wage growth will become crucial turning points. Any surprises here will not only influence spot rates but also affect implied volatility and positioning on both sides.

It’s evident that the usual connections between rates, inflation, and currency strength are changing rapidly. Policymakers are reacting to post-pandemic economic shifts: higher inflation no longer signifies a weakening currency. Nowadays, a surprise in CPI might signal a tightening approach rather than a wage squeeze, altering how we analyze fundamentals.

In this light, we are adjusting our assumptions about term structures. For the Aussie, traders should consider the accumulation of premium in long-dated options against falling rates. A flatter yield curve could make longer expiry options more appealing for reactive trading. On the Yen side, any indication of a rate hike or balance sheet tightening may lead to sharp short-term volatility. A short gamma position here can be risky without proper hedging.

Practically, this means shifting strategies away from static long AUD/JPY trades held mainly for carry purposes. Momentum trades aimed at capitalizing on yield differentials must now factor in political risks, macro downgrades, and unexpected policy changes, all of which increase short-term risk. We have started to rebalance towards more dynamic setups, including spreads designed to profit from mismatches between realized and implied volatility. The skew is becoming more significant than the spot rate.

Traders focused on mid-term outcomes should watch upcoming BoJ policy comments closely. To remain adaptable, it’s advisable not to rely too much on simultaneous moves between these two currencies. Both central banks are charting different paths after months of alignment. If this divergence is clear enough, it could open up opportunities, but only for those who are flexible and have a solid understanding of rate expectations.

Create your live VT Markets account and start trading now.

RBA’s interest rate decision meets expectations at 3.85% in Australia

The Reserve Bank of Australia has decided to keep interest rates at 3.85%. This decision aligns with earlier predictions and acts as a steady sign for the economy.

The EUR/USD pair rose above 1.1250 during the European session. This increase is due to a weaker US Dollar caused by economic uncertainties and changing US tariffs.

GBP/USD and Stability

In other markets, GBP/USD stayed above 1.3350 despite the struggling USD. This stability occurs amidst global trade concerns and expectations of upcoming economic data. Gold prices saw slight losses during the day but remained above $3,200. Optimism for a ceasefire in the Russia-Ukraine conflict helps support this stable position in a positive trading environment. Solana (SOL) showed signs of recovery after launching the Alpenglow consensus protocol, which aims to replace the existing Proof-of-History and TowerBFT mechanisms. In China, April’s economic data indicates a slowdown linked to trade war worries. However, the manufacturing sector showed strength, preventing a more significant decline.Short-Term Economic Direction

With the Reserve Bank maintaining rates at 3.85%, this pause reinforces expectations for the short-term economic direction. This suggests that inflation pressure doesn’t yet require further tightening, though caution is still necessary. Sticking to forecasts helps in calculating hedging costs and adjusting rate agreements across portfolios. Currently, the yield curve shows limited sensitivity to minor inflation changes, but this could change quickly if labor or housing data diverges from expectations. Hoffman’s recent activity in the EUR/USD pair provides valuable insights, primarily influenced by weaknesses in the US economy rather than changes in Europe. Tariff adjustments and fiscal uncertainties place pressure on the US Dollar. If further US data disappoints, especially in services or nonfarm job growth, we could retest the 1.1280-1.1300 range. Options pricing indicates a higher demand for upside calls, signaling that buyers are preparing for a potential EUR breakout. If the EUR/USD stays near 1.1250, establishing short-volatility positions below key levels could be beneficial in the coming week. The stability of GBP/USD above 1.3350 reinforces the confidence in the pound observed since Q1. While the US isn’t offering much resistance, the UK still faces challenges with sticky domestic prices. The market is divided between a hold and a slight hike from the Bank of England, keeping implied volatility high around key economic reports. Directional exposure is closely linked to rate expectations—any hawkish comments from Broadbent could push the exchange rate above 1.3450 with low volume. Despite some fading daily demand and slight losses, gold prices staying above $3,200 is a mix of reassurance and caution. Currently, the war premium from Eastern Europe isn’t strong, but safety flows return quickly with increased volatility. While physical buyers haven’t surged, ETF flows have stabilized. If this medium-range stability continues, we should be cautious of sellers becoming overly confident, especially before any sudden macro changes. Keeping short durations on gold-linked derivatives seems wise under these conditions. The rise in Solana following the Alpenglow protocol launch shows that technical innovation still matters, particularly for how traders view efficiency. It doesn’t resolve the network reliability issues but hints at changes in public valuation standards. Derivatives related to decentralized assets will need tighter stop orders in the short term as their correlation with tech indices weakens. Given that sudden volume spikes can cause cascading adjustments, leveraged trades in DeFi products should focus on slippage risks. In China, April’s softer data added some pressure but did not negate positive momentum; manufacturing managed to stand strong despite tariff challenges. This indicates selective resilience rather than overall stability. As traders, this shows us more about specific sector health than macro stability. If material costs fall while demand remains, there’s a case for reevaluating short positions on commodities linked to Chinese production, particularly base metals. Futures on copper, for instance, may find stronger support near recent lows if industrial stocks signal ongoing factory activity. Overall, what we’re seeing in these markets isn’t a systemic reaction but rather tactical rebalancing. Timing trades around data releases is crucial while volatility remains contained within the current range. Create your live VT Markets account and start trading now.NZD/USD hovers around 0.5900, facing downward pressure after PBoC cuts rates

NZD/USD dropped after the People’s Bank of China reduced its one-year Loan Prime Rate from 3.10% to 3.00%. During Tuesday’s Asian session, the pair is trading around 0.5920, influenced by this interest rate change in China.

China’s recent adjustments include cutting its Loan Prime Rates. The one-year LPR is now at 3.00%, while the five-year LPR is at 3.50%. These changes have a considerable impact on the New Zealand Dollar due to the strong trade relationship between New Zealand and China.