EUR stays near 1.1865 against the USD as holiday-thinned trading precedes a week full of data releases

EUR/USD traded near 1.1865 on Monday and was mostly unchanged. The move came after weak Eurozone industrial production data and thin trading volumes.

Eurozone industrial production fell 1.4% in December, versus a 1.5% drop expected. November was revised down to 0.3% growth from 0.7%.

On a yearly basis, output rose 1.2%. That was below the 1.3% forecast and down from 2.5% in November. EUR/USD stayed stuck in its recent range.

Trading was quiet because many Asian markets, including Japan, were closed for the Lunar New Year. US markets were also shut for President’s Day.

Later, markets were set to hear from Federal Reserve Vice Chair for Supervision Michelle Bowman and ECB Governor Joachim Nagel. These speeches came before a busier week of data.

On the 4-hour chart, EUR/USD held above a rising trendline near 1.1855, with extra support at 1.1833. MACD sat just below zero, and RSI was just under 50.

A break below 1.1833 would put 1.1775 in focus. Resistance was seen at 1.1890, then 1.1925.

Looking back to this time last year, in February 2025, EUR/USD was steady near 1.1865 even as Eurozone factory output looked weak. Trading was also very quiet, helped by holidays in the US and Asia. That low-volatility setup is very different from today’s market.

The Eurozone’s underlying weakness seen in the December 2024 data has continued. The latest December 2025 figures show industrial production fell 0.7% month-on-month, according to Eurostat. This ongoing softness helps explain why EUR/USD is now struggling to hold above 1.09, far below the levels discussed a year ago.

In early 2025, attention was on softer US CPI data, which gave the Fed room to consider rate cuts. By February 2026, the picture has reversed. US inflation remains sticky, running at 2.9% year-on-year last month, which has kept the Fed on hold. At the same time, the ECB is sounding more open to cuts. This policy gap continues to pressure the euro.

For derivatives traders, this calls for a different playbook than last year’s range trading. With major inflation and jobs data due from both economies in the coming weeks, EUR/USD straddles may offer a way to benefit from a volatility jump, regardless of direction. Implied volatility is near 8.2%, well above the sub-6% levels seen in the quiet February 2025 period, suggesting traders expect larger moves.

The technical backdrop has also weakened a lot over the past year. The 1.1833 support level watched in February 2025 is now far above the market and would likely act as major resistance. Today’s key level is around 1.0850, and a clean break below it could lead to more selling.

USD/JPY rebounds to around 153.25, stays below the 200-day EMA, and recovers from 38.2% Fibonacci support

USD/JPY rose on Monday after weak Japan Q4 GDP data pushed the yen lower. A small lift in the US dollar and a better risk mood also helped the pair bounce from an over two-week low set last Thursday.

The pair stayed above the rising 200-day exponential moving average (152.54). It also rebounded near the 38.2% Fibonacci retracement of the April 2025 to January 2026 move, at 152.11.

Technical Levels Keep Bias Cautious

Different policy outlooks between the Bank of Japan and the US Federal Reserve capped further gains. A mixed technical setup also argues for caution. The MACD line remained below the signal line. Both stayed below zero, and the bearish histogram grew. The RSI was 38, under the midline, pointing to weak upside momentum. Resistance sits near the 23.6% retracement at 154.96. A daily close below 152.11 could open the door to a deeper pullback. A break above 154.96 could support more gains. Japan’s economy unexpectedly shrank by 0.4% in the final quarter of 2025. That helps explain why USD/JPY rebounded from below 152.50. Weak growth tends to hurt the yen because it reduces the chance that the Bank of Japan will tighten policy soon. We see this as the main reason the pair held firm at the start of the week. This differs from the United States. January 2026 inflation came in at 3.2%, a bit higher than expected. Sticky inflation keeps pressure on the Federal Reserve to hold rates where they are, which supports the US dollar. This policy gap is limiting upside in the pair and keeping a lid on the recent rebound.Options Strategies For A Range

For derivatives traders, this back-and-forth can favor range-bound strategies. With support near 152.11 and resistance near 154.96, selling an iron condor with strikes outside this area could be one way to collect premium. This works best if the pair stays between these levels in the weeks ahead. We are also watching the 200-day moving average near 152.54, which has acted as support during the pullback from the January 2026 highs. Selling put options around the 152.00 strike could offer bullish exposure while generating income. This is profitable if the pair holds above this key long-term support zone. However, bearish signals like the MACD suggest sellers are still active. A clean break below 152.11 could speed up the drop, which may make long puts appealing for downside exposure. A sustained move above 154.96 would instead suggest the uptrend seen through most of 2025 is returning, which would favor bullish approaches like buying calls. Create your live VT Markets account and start trading now.Geoff Yu says tighter global conditions and weaker risk appetite are pressuring EM carry and driving outflows

BNY says tighter global financial conditions and weaker risk appetite are pressuring emerging market (EM) FX carry trades. Positioning in carry trades seems to have peaked, and high-yielding currencies are seeing outflows.

Latin American currencies look especially vulnerable because holdings are high, which raises the risk of a sharp unwind. The report adds that further interest rate rises may be needed to reduce the chance of disorderly moves.

Global Portfolio Positioning And Allocation Trends

EM allocations in global portfolios remain low. The report notes that low weightings, cheaper valuations, and supportive exchange rates—especially in APAC—could help drive a gradual increase in allocations. The key factor to watch is US-driven changes in financial conditions. The report says support from expectations of US Federal Reserve easing may be close to its limit if US data strengthens. The outlook for FX carry trades is worsening as global financial conditions tighten. After January’s US jobs and inflation reports came in hotter than expected, markets have reduced expectations for near-term Federal Reserve rate cuts. That argues for caution when holding high-yielding EM currencies. We are most concerned about Latin American currencies, where our positions grew large after strong performance through much of 2025. The Mexican peso has already weakened beyond 18.00 per US dollar this month, a level not seen in about six months. That may be an early sign of an unwind. We should consider buying put options on the peso or the Brazilian real to hedge against a steeper drop.Positioning And Hedging Considerations

The main challenge for EM will be US-led adjustments. With the Fed likely to stay on hold, the US dollar may have more room to rise. The risk of a “disruptive unwinding” means we should expect higher volatility in these currency pairs in the coming weeks. Even so, we see better opportunities in Asia, where positioning is less crowded and valuations look more attractive. For example, India’s manufacturing sector remains strong, with January PMI rising to a four-month high of 56.9. This could support a strategy of being long selected Asian currencies while holding short positions in Latin America. Create your live VT Markets account and start trading now.FedEx shares closed higher at $374.72, beating broader indices as Nasdaq slipped despite S&P gains

FedEx (FDX) closed at $374.72, up 1.42% on the day. The S&P 500 rose 0.05%, the Dow gained 0.1%, and the Nasdaq fell 0.22%.

Over the past month, FedEx shares rose 17.98%. The Transportation sector gained 8.02% over the same period, while the S&P 500 fell 1.99%.

The next earnings update is expected to show EPS of $4.06, down 9.98% from a year ago. Revenue is forecast at $23.46 billion, up 5.89% versus the same quarter last year.

For the full year, analysts forecast earnings of $18.38 per share and revenue of $92.6 billion. That would be an increase of 1.04% in earnings and 5.32% in revenue compared with last year.

Over the past month, the consensus EPS estimate rose by 0.11%. FedEx has a Zacks Rank of #3 (Hold), on a scale from #1 to #5.

FedEx trades at a forward P/E of 20.1, in line with the industry average of 20.1. Its PEG ratio is 1.8, compared with the industry average of 1.87.

The Transportation – Air Freight and Cargo industry has a Zacks Industry Rank of 86, which puts it in the top 36% of 250+ industries. Zacks data shows that industries in the top 50% tend to outperform the bottom half by 2 to 1.

After an 18% jump over the last month, the stock could be more volatile going into earnings. Traders are weighing two forces: strong momentum versus a forecast near-10% drop in EPS. That mix increases the chance of a big move if results beat or miss expectations.

The broader economy also matters. January 2026 U.S. consumer spending came in stronger than expected, which supports the projected 5.9% revenue growth. Also, FedEx’s cost-cutting efforts during 2025 could help offset weaker profits. The market may focus more on improving efficiency than on the near-term dip in earnings.

Implied volatility in FedEx options is already rising. That means traders are pricing in a multi-percentage-point move after earnings. Historically, FDX has moved about 6% after earnings, though it dropped 11% after the earnings miss in Q3 2025. Because large swings are possible in either direction, strategies like long straddles or strangles may fit traders who want exposure to volatility.

If you expect the uptrend to continue, a bull call spread can be a lower-cost way to position for more upside while limiting risk. It’s often cheaper than buying calls outright, which matters when options are expensive. This approach fits a view that revenue growth and recent operational improvements will matter more than the expected drop in EPS.

On the other hand, the projected EPS decline could support bearish trades. Buying puts or using bear put spreads is a direct way to bet that the market will punish weaker profitability, especially after a sharp rally. This case would strengthen if competitors issue negative updates or if shipping volume forecasts are cut in the days ahead.

Sterling-dollar holds near the 20-day EMA at around 1.3640 as it awaits UK jobs figures for the December quarter

GBP/USD traded near 1.3640 in early European trading on Monday. Moves were muted as traders waited for UK labour market data due on Tuesday. The key period is the three months to December. The ILO Unemployment Rate is expected to stay at 5.1%, while Average Earnings Including Bonuses are forecast to rise 4.6% year on year.

Earlier this month, the Bank of England kept its policy rate unchanged at 3.75%. The vote split 5–4. The Bank also repeated that policy is likely to follow a “gradual downward path”.

Uk Data In Focus

In the US, the Dollar was broadly steady after January inflation cooled more than expected. Expectations for the Federal Reserve’s March and April meetings were largely unchanged. From a technical view, GBP/USD was near 1.3648 and stayed above the 20-day EMA at 1.3619. The 20-day EMA is now flat. The 14-day RSI is around 55 after slipping from previously overbought levels. Price action has tightened into a symmetrical triangle. Resistance sits near 1.3675, while support is close to 1.3600. GBP/USD is also described as trading quietly around 1.2650 ahead of tomorrow’s UK labour report. This mirrors the calm trading seen in early 2025, when the pair also moved sideways before a major release. It suggests traders are waiting for fresh data before choosing a direction.Options Market Volatility

Markets expect the UK unemployment rate for the three months to December 2025 to hold near 4.2%. The main focus is wage growth, forecast at 5.7%. The Bank of England is watching wages closely because they can keep inflation high. If wages come in well above expectations, it could make it harder for the BoE to cut its 4.5% Bank Rate in the months ahead. Meanwhile, the US Dollar remains firm after last week’s report showed core inflation still running at 3.8% in January. As a result, markets now think the Federal Reserve may wait until at least June before making its first rate cut. This gap between central bank paths is helping keep GBP/USD trapped in a tight range. This sideways phase, similar to what we saw in 2025, has pushed down short-term implied volatility in the options market. That makes trades that benefit from a large move—such as buying a straddle—cheaper than usual. A straddle can profit if tomorrow’s data triggers a sharp breakout in either direction. For traders with a clearer view, wage growth above 6% could support buying call options in search of a move above 1.2750. On the other hand, wage growth below 5.5% could support buying put options. That would reflect expectations for a more dovish BoE and could open the door to a test of support near 1.2500. Create your live VT Markets account and start trading now.WTI hovers near $63, slipping to $62.80, as traders cautiously await geopolitical developments in Asian trading

WTI traded near $62.80 per barrel in Asian hours on Monday, after opening above the previous close. Price moves were limited because US markets were closed for Presidents’ Day. Trading in Asia was also lighter due to Lunar New Year holidays in China, South Korea, and Taiwan.

Focus is on the second round of US-Iran talks in Geneva on Tuesday. Tehran said it may accept nuclear concessions if the US addresses sanctions. President Donald Trump warned of possible strikes if talks fail, and the US has increased its military presence in the region.

Geopolitical Risks And Market Focus

US-brokered Russia-Ukraine talks are also set to resume on Tuesday. Expectations for a fast deal are low, and a near-term return of Russian oil to global markets looks unlikely. Slovak Prime Minister Robert Fico said Ukraine is delaying the restart of a pipeline that carries Russian oil to Eastern Europe. He said the delay is meant to pressure Hungary over its position on Ukraine’s EU membership. Supply is also in focus after Reuters reported that OPEC+ is leaning toward restarting output increases from April, after a three-month pause. The move is tied to planning for peak summer demand. WTI is a US crude benchmark produced in the United States and distributed through the Cushing hub. US inventory reports from the API and EIA can move prices. Their numbers are within 1% of each other about 75% of the time. A year ago, in early 2025, oil was holding near $63 a barrel as markets waited for US-Iran talks. Those talks later failed, which helped create the more tense backdrop seen today. With WTI now near $82, the drivers behind prices are clearer.Key Indicators To Watch

The failure of the 2025 Geneva talks has kept a risk premium in the market. OPEC+, which once considered raising output, later changed course to support prices. Last month, the group agreed to extend its existing production cuts. That keeps about 2 million barrels per day off the market through the second quarter. In the coming weeks, inventory data will be a key sign of near-term market balance. Last week, the Energy Information Administration (EIA) reported a surprise drop in US crude inventories of 3.1 million barrels, versus expectations for a small build. Another draw would suggest strong demand. That could support prices and make call options more attractive. On the demand side, conditions also look stronger than a year ago. The International Energy Agency’s latest forecast sees global demand rising by 1.3 million barrels per day this year. Much of that growth is expected to come from China and India. This suggests that price dips could be brief and may attract buyers. Create your live VT Markets account and start trading now.DBS’s Philip Wee cuts US dollar forecast amid doubts over Fed leadership, de-dollarisation and US midterm political risks

DBS Group Research’s Philip Wee has cut US Dollar forecasts against most major and Asian currencies. He points to uncertainty over Federal Reserve leadership and independence, ongoing de-dollarisation, and rising US political risk ahead of the November midterm elections.

He says the Dollar no longer benefits as much from interest rate gaps or the idea of US economic exceptionalism. Instead, he believes institutional credibility and politics are now driving currency moves.

Shifting Drivers Of Dollar Performance

DBS expects two Federal Reserve rate cuts in 2H26. The note also says de-dollarisation will continue. The article says it was produced with help from an AI tool and reviewed by an editor. It also notes that the FXStreet Insights Team selects market views from outside experts and from internal and external analysts. We are cutting our US Dollar forecasts because the greenback is no longer supported by rate differentials or by narratives of US economic exceptionalism. Instead, institutional credibility and political risks are becoming the main drivers. We now expect two Federal Reserve rate cuts in the second half of 2026. This change follows data showing the growth gap between the US and other major economies is narrowing. For example, US GDP growth in Q4 2025 was 1.9%, while the Eurozone recovery came in at a stronger-than-expected 1.6%. That smaller gap reduces a key advantage that previously supported the dollar. It suggests the dollar’s strength from better economic performance is fading.What Traders May Watch Next

We expect the Fed to start cutting rates later this year, but other central banks may not follow. The European Central Bank, for example, kept rates unchanged at its January 2026 meeting, citing persistent underlying inflation. This reduces the dollar’s yield advantage. As policy paths diverge, one of the dollar’s main supports weakens. The slow move away from the dollar also remains a steady headwind. IMF data on central bank reserves released in late 2025 showed the dollar’s share of allocated reserves fell to a new low of 57.9%. This points to a long-term structural shift that is gradually weighing on the currency. For traders, this outlook may favor strategies that benefit from a weaker dollar, especially heading into the uncertain November midterm elections. Examples include buying puts on dollar-tracking ETFs like UUP or using futures to take short positions against currencies supported by more hawkish central banks. Given the higher volatility seen during the 2022 midterm cycle, preparing for wider price swings may also make sense. With these forces in play, implied volatility in dollar pairs may rise in the months ahead. Traders may want to watch options pricing for chances to hedge, or to position for, choppier markets. In this environment, political and policy uncertainty may matter more than simple measures of economic strength. Create your live VT Markets account and start trading now.WTI trades near $63, easing to $62.80 as cautious traders await further geopolitical developments in Asia

WTI traded near $62.80 a barrel during Asian hours on Monday. It opened above the prior close, then slipped slightly. US markets were closed for Presidents’ Day. Trading in Asia was also slow as China, South Korea, and Taiwan observed Lunar New Year holidays.

A second round of US-Iran talks is set for Tuesday in Geneva. Tehran has signaled it may offer nuclear concessions if the US addresses sanctions. The US has warned it could strike if talks fail and has increased its military presence in the region.

Key Geopolitical Talks Ahead

US-backed talks between Russia and Ukraine are also due to resume on Tuesday. Expectations for a fast breakthrough are low, and a near-term return of Russian oil flows to global markets looks unlikely. Slovakia’s Prime Minister Robert Fico said on Sunday that Ukraine is delaying the restart of a pipeline that carries Russian oil through Ukrainian territory to Eastern Europe. Supply concerns also weighed on prices. Reuters reported that OPEC+ is leaning toward restarting output increases from April, after a three-month pause, ahead of peak summer demand. OPEC has 12 member countries and sets production quotas at meetings held twice a year. WTI (West Texas Intermediate) is a US crude benchmark traded through the Cushing hub. Weekly inventory reports from the API and EIA can move prices. Their results are within 1% of each other about 75% of the time. With WTI holding near $63 a barrel, the calm market may offer a chance to prepare for a large move. Major talks involving the US, Iran, Russia, and Ukraine take place this Tuesday, February 17, and could trigger volatility. We see this as a period to plan for a breakout, not to rely on sideways trading. Because the outcomes of these meetings are hard to predict, options strategies that benefit from a sharp move may fit best. Implied volatility for March WTI options has risen to 38%, showing growing concern about the US-Iran negotiations. Traders may consider straddles or strangles, which can profit from a big move in either direction.Options Positioning For Volatility

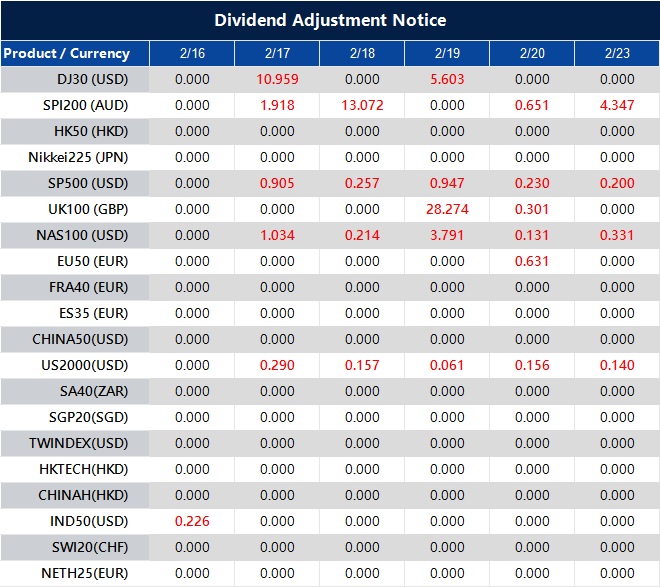

On the supply side, the case for lower prices is strengthening. That supports buying puts as a hedge or a directional trade. The latest EIA report showed a surprise inventory build of 2.3 million barrels last week. Reports also suggest OPEC+ may approve an output increase from April. If geopolitical risks fade, added supply could push prices back toward the low $60s. At the same time, upside risk remains significant if talks break down. Prices jumped above $70 in the third quarter of 2025 after an earlier round of Iran negotiations collapsed unexpectedly. A similar outcome—especially alongside warnings of possible military action—could make call options or bull call spreads perform well. The market’s caution also shows in CFTC positioning data, which indicates money managers cut net-long exposure for a second straight week. The Russia-Ukraine pipeline issue adds uncertainty, but the main focus is the US-Iran meeting in Geneva. We expect the current holding pattern to end quickly once the outcome becomes clear. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Feb 16 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

DBS’s Philip Wee cuts dollar forecast against major and Asian peers amid Fed uncertainty and political risks

DBS Group Research cut its US Dollar forecasts against most major and Asian currencies. It pointed to rising uncertainty around Federal Reserve leadership and independence, ongoing de-dollarisation, and US political risks ahead of the November midterm elections.

The note said the Dollar is getting less support from interest rate gaps and from the US economy outperforming other countries. It added that institutional credibility and politics are now driving currency moves.

DBS expects two Federal Reserve rate cuts in the second half of 2026. It also expects de-dollarisation to continue.

The report was attributed to DBS Group Research’s Philip Wee. FXStreet said the item was produced using an AI tool and reviewed by an editor, and that its Insights Team selects market observations and adds analysis.

The dollar is no longer being held up by high interest rates or a uniquely strong US economy. Instead, the market is focusing on the credibility of US institutions and on political risk. This shift suggests positioning for possible dollar weakness in the coming weeks.

Recent data has strengthened the view that the Fed could cut rates twice in the second half of 2026, after January inflation cooled to 2.8%. For traders, this makes strategies like buying put options on the U.S. Dollar Index (DXY) more appealing. A move down toward 100 on the index now looks more realistic.

As the November midterm elections get closer, political noise and uncertainty around government spending may rise. Early polling points to a tight race for Congress, which often increases market volatility. Strategies such as buying option straddles on major pairs like EUR/USD could benefit from large moves in either direction.

The gradual shift away from the dollar is another factor. Central bank reserve data for the end of 2025 showed the dollar’s share of global reserves falling to 58.1%. This long-term trend supports holding assets that tend to do well when the dollar weakens. That includes being long other currencies such as the Swiss franc, or using futures to gain exposure to gold.

The debt-ceiling standoff in 2023 showed how political gridlock can limit dollar strength. Today’s setup feels similar. That suggests any dollar rallies may be brief and could offer chances to build short positions. It also fits the view that the period of US exceptionalism may be pausing.