If trade negotiations fail, US Treasury Secretary Scott Bessent suggests tariffs may rise again.

US Treasury Secretary Scott Bessent mentioned on CNN that President Donald Trump has warned trading partners that negotiations could go back to past terms if they are not conducted in good faith. There are 18 upcoming deals with key trading partners, but no specific timeline has been given.

Currently, the US Dollar Index (DXY) is down 0.32%, sitting at about 100.75. Tariffs are taxes on imports that help local manufacturers compete with foreign products. They are often used alongside trade barriers and import quotas to protect domestic industries.

While both tariffs and taxes raise revenue for the government, they work in different ways. Tariffs are paid at ports of entry for imports, while taxes are paid at the point of sale for goods and services. Taxes target both individuals and businesses, whereas tariffs are the responsibility of those importing goods.

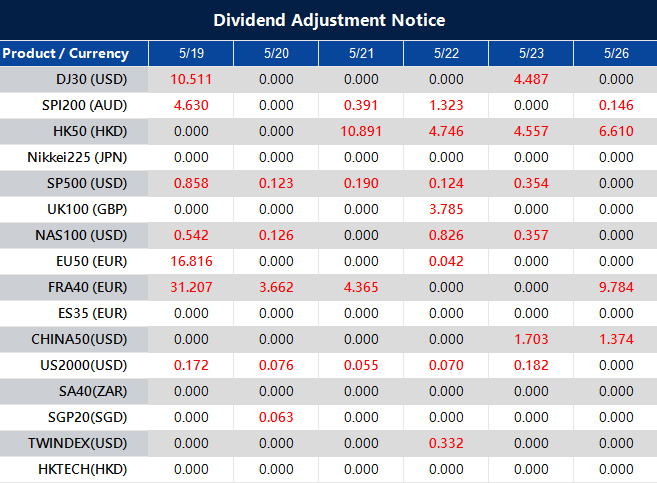

Dividend Adjustment Notice – May 19 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Week Ahead: Moody’s Downgrade Rattles Market Confidence

The trading week commenced under a cloud of fiscal unease after Moody’s became the final major credit rating agency to lower the United States’ sovereign rating, shifting it from AAA to Aa1.

Although the revised rating still signals strong creditworthiness, the symbolic impact is substantial. For decades, US Treasuries have served as the gold standard of global safety. It is an almost risk-free benchmark underpinning worldwide credit markets. That status is now being called into question.

Investor sentiment turned cautious in response. After-hours trading saw yields on the 10-year U.S. Treasury note climb to 4.48%, as risk premiums adjusted. The SPDR S&P 500 ETF dipped by 0.4%, a relatively modest decline, yet underscoring simmering concern beneath the surface. Markets are not yet in turmoil, but the erosion of trust has begun.

The rationale behind the downgrade is clear. The US national debt is forecast to grow from 98% of GDP in 2024 to 134% by 2035, while the annual budget deficit could swell from $1.8 trillion to $2.9 trillion over the same period. Compared with similarly rated economies, these figures are significantly elevated, prompting scrutiny over the country’s premium status.

The Treasury market, already under strain from increased issuance and declining foreign appetite, now faces further headwinds. Countries that once absorbed U.S. debt uncritically are reassessing. Broader shifts in global trade dynamics, tariff conflicts, and the gradual emergence of alternative reserve currencies continue to erode America’s central role in the global financial order.

For the everyday borrower, the implications are tangible. Treasury yields influence everything from mortgage rates to student loan terms. If institutional traders demand greater returns for the risk of lending to the US, banks and lenders will inevitably pass those costs down to households and businesses. Even a small uptick in yield curves can translate to hundreds of billions in added debt servicing costs over time. The result is tighter consumer credit, pricier capital, and diminished room for government stimulus during future downturns.

Politically, the downgrade highlights Washington’s persistent dysfunction. Moody’s had issued warnings as early as November, citing lawmakers’ repeated failure to resolve debt ceiling impasses or enact lasting fiscal reforms. The removal of Speaker Kevin McCarthy in 2023 and extended Congressional paralysis laid bare the governance challenges. Uncertainty surrounding the Federal Reserve’s independence has added fuel to the fire. Remarks by former President Trump regarding potential changes to central bank leadership have unsettled global markets.

Meanwhile, fiscal policy remains contradictory. Trump’s proposal to extend the 2017 tax cuts would slash government revenue by $4 trillion over the next decade. Even with drastic reductions in Medicaid and food assistance spending, the plan is projected to add $3.3 trillion to the national debt. The so-called Department of Government Efficiency, a flagship initiative, has reportedly missed its initial objectives.

In this environment, the US risks drifting into a debt spiral. As interest payments rise, the share of the federal budget allocated to debt servicing grows, leaving less room for essential spending on infrastructure, education, and healthcare. Traders are already reacting. Bond yields are climbing. Equity markets are wobbly. Even the dollar, though still dominant, faces pressure as other economies begin to decouple from traditional US-centric models.

The coming days could prove pivotal. Should the 10-year yield surpass 4.5%, increased equity market volatility is likely. Defensive sectors such as healthcare and utilities may see inflows, while tech shares, often sensitive to interest rate changes, could suffer.

Market Movements This Week

The USD Index (USDX) remains delicately poised. Having fallen towards the 100.60 mark, the dollar now faces an important juncture. A rebound could take it to 101.40 or 102.40, but sentiment needs to stabilise first. A break lower could see the 99.80 region tested, which may trigger wider ripples across risk assets. With US credit quality now under examination, the dollar’s safe-haven credentials are on trial.

EURUSD is approaching the 1.1195 resistance level. A failure to breach this zone may lead to another test of 1.1105. A sustained rise beyond 1.1300 could signal broader shifts, possibly tied to softer US data or revised rate expectations.

GBPUSD is staging its attempt at higher ground. The 1.3320 level marks the next technical ceiling. If sellers defend this range, bulls may regroup at 1.3215. With UK CPI data due midweek—forecasted at 3.30% y/y compared to the previous 2.60%—volatility in the pair is likely, especially if inflation surprises to the upside. The market is already bracing for a possible rate recalibration.

USDJPY continues its ascent but remains cautious near the 145.00 level. A slide toward 144.65 or 143.80 is plausible if market sentiment sours or yields ease. The yen’s haven appeal remains muted but could return swiftly amid geopolitical shocks.

USDCHF, meanwhile, is trapped in a range. The pair is hovering close to key levels, with a possible bullish bounce eyed at 0.8300. Broader sentiment toward Europe’s monetary trajectory and risk flows into the franc will shape its next steps.

AUDUSD found its footing at 0.6370 and now eyes resistance at 0.6425. This week’s Australian cash rate decision looms large, with markets anticipating a cut to 3.85% from 4.10%. Should that scenario unfold, a retracement back toward 0.6295 could materialise. But if support holds amid a dovish surprise, the Aussie might find breathing room to stabilise.

NZDUSD has bounced from 0.5860, currently testing 0.5905. Failure here could send the kiwi back toward 0.58459. Commodity sentiment and global growth forecasts remain key drivers.

USDCAD continues its slow rotation. If the pair drifts lower, price action near 1.3940 or 1.3910 could offer renewed support. On the upside, resistance is being eyed at 1.4055 and potentially 1.4140. The Canadian dollar remains tethered to oil’s performance, which brings us to energy markets.

US crude oil (USOil) is stuck in a narrow range. A move toward 63.05 may invite selling pressure. Despite geopolitical tensions, lacklustre demand is keeping prices in check for now.

Gold rebounded sharply from $3,154 and is now hovering near $3,210. A clean move through this level may open the door for another test of $3,270, while failure could send it back toward $3,120.72. Its appeal as a hedge remains intact but is complicated by the dollar’s uncertain direction.

The SP500 is treading carefully after its recent rally. Bullish setups may emerge near 5740 or 5690, but if equities push higher too quickly, a reaction at 6100 could limit upside. With yields rising and the fiscal backdrop turning uncertain, the broader equity market may lack the momentum for a breakout, unless earnings or economic data offer fresh support.

Bitcoin remains tightly coiled just under $100,000. Support at 99,400 and 96,600 will be crucial if prices dip. A breakout would shift attention to new record highs. Traders remain hopeful, but wary.

Natural Gas continues to retreat after peaking at 3.45, now nearing 3.02. While this level might offer support, subdued demand and healthy inventories suggest any rally may be short-lived.

Key Events This Week

On Tuesday, May 20, the market turned its attention toward the Pacific and North America, with two releases drawing early focus. Australia’s cash rate decision came in with a forecast of 3.85%, down from 4.10% previously. This anticipated rate cut reflects increasing pressure on the RBA to ease financial conditions amid a slower domestic economy. Meanwhile, Canada’s Median CPI y/y was forecast to hold steady at 2.90%, matching the prior figure. Any deviation from this inflation forecast would challenge the Bank of Canada’s stance, but with no surprises expected, the pair held ground, consolidating as markets awaited structural direction. Tuesday’s movements were light but preparatory—zones were marked, and momentum traders kept their entries tight.

On Wednesday, May 21, the spotlight shifted to the United Kingdom, where the CPI y/y was forecast to jump to 3.30%, up from 2.60% previously. This sharp expected rise underscores the lingering stickiness of inflation in the UK economy, particularly in core services. However, with broader economic growth faltering and labour conditions beginning to cool, a spike in inflation might not translate directly into rate hikes. Should the actual figure match or exceed the forecast, short-term momentum may favour GBP strength—but upside would likely be capped without a broader shift in the BoE’s tone.

On Thursday, May 22, a wave of PMI data swept through Europe and the United States, offering a barometer for economic sentiment across sectors. Germany’s flash manufacturing PMI was forecast at 48.8, slightly improved from 48.4 previously, while services PMI was expected to rise to 49.6 from 49.0. Though both remain in contraction territory, the marginal increase hinted at a stabilising tone. In the UK, flash manufacturing PMI was forecast at 46.2 (up from 45.4) and services PMI at 50.0, up from 49.0. This would signal a tentative return to growth in services, though manufacturing continues to lag.

Lastly, the U.S. released its own PMI flash readings: manufacturing expected at 49.9, down from 50.2, and services slightly lower at 50.7 from 50.8. These softer forecasts suggested the Fed may remain in a holding pattern. Thursday shaped up as the most technically active day of the week—tight ranges began to widen, and macro narratives re-entered the charts.

Create your live VT Markets account and start trading now.

Chinese officials claim the economy is steadily improving despite various challenges and pressures.

An official from China’s National Bureau of Statistics stated that the economy is growing steadily despite current challenges. Demand for productivity is increasing, and employment remains stable.

The economy is facing obstacles, yet it continues to develop positively. China is also working to diversify and strengthen trade with countries involved in the Belt and Road initiative.

Recent data from April shows that China’s industrial output rose by 6.1% from the previous year, exceeding the expected 5.5%. However, this is a decrease from March’s growth of 7.7%. In contrast, China’s apparent oil demand fell by 5.6% year-on-year in April.

The report from the National Bureau of Statistics indicates a trend that, while rocky, still provides some reassurance. Growth is slowly increasing. Employment levels are close to targets. Furthermore, there are efforts to enhance trade connections, especially through the Belt and Road initiative. This strategy helps strengthen resilience beyond domestic factors, even as internal consumption fluctuates.

Industrial data from April shows something important. Output grew more than expected, hitting 6.1%, which was above the forecast of 5.5%. This may indicate that manufacturing is picking up momentum. However, the decline from March’s 7.7% suggests inconsistency. While factories are active, growth is not uniform. There’s a steady rhythm, but it still varies.

On the other hand, oil demand presents a different picture. It decreased by over 5% during the same month, indicating that either there is enough inventory or that some industrial areas are slowing down. Such a drop typically does not align with a robust economy. It raises caution for sectors heavily reliant on fuel, such as transportation, construction, and machinery production. There may also be seasonal changes, such as businesses tightening up before a new quarter.

From our perspective, this situation calls for careful assessment. The contrast between increasing output and falling energy demand is concerning. One positive trend does not guarantee a broader recovery, especially when key commodities are declining. Strategies that depend heavily on raw materials should be re-evaluated due to this decline in energy demand. This does not necessarily mean weakness across all sectors, but there is uncertainty about sustained demand overall.

Given the data, it’s reasonable to expect that positions linked to commodities reflecting industrial activity, especially energy consumption, may require adjustments. Taking a more active approach to hedging or adjusting expiration dates towards the end of summer may help mitigate risks. Volatility related to trade could resurface, especially with new deals or policy changes from Belt and Road partners.

The drop in apparent oil demand also suggests that traders should consider sectors sensitive to fuel imports or logistical issues. If reduced consumption continues into May, long-term investments in refinery margins or maritime transport could be at risk. This situation may not reverse quickly, so it is better to manage risk carefully now rather than react hastily later.

It’s important to note that even though industrial data exceeded expectations, the gap between market predictions and actual results is narrowing. This suggests that analysts are adjusting their forecasts rather than expecting major increases. For volatility exposure, this could mean more minor fluctuations rather than large swings.

Where policy remains supportive and export routes remain open, we’ll identify which sector tends to diverge. Our focus will be on trends, not just breakpoints. For now, any adjustments should happen gradually and thoughtfully.

Christine Lagarde discusses the decline of the US dollar, linking it to uncertainties in US policies during an interview.

Christine Lagarde, the President of the European Central Bank (ECB), spoke about the changing value of the dollar in uncertain times, noting its unexpected drop. This decline comes from doubts about U.S. policies among some financial market participants.

She pointed out that Europe is seen as a stable economic and political region, even with ongoing challenges to the rule of law and trade in the U.S. This view likely supports the Euro, which has slightly increased, with EUR/USD trading close to 1.1175.

Key Functions of the European Central Bank

The ECB, located in Frankfurt, Germany, oversees monetary policy and interest rates for the Eurozone. Its goal is to maintain price stability and keep inflation around 2%. The ECB uses methods like adjusting interest rates and, during crises, implementing Quantitative Easing (QE). QE generally weakens the Euro as it involves buying assets from banks. On the other hand, Quantitative Tightening (QT) happens when economies recover and inflation rises. QT means stopping bond purchases and halting reinvestments, which usually strengthens the Euro. These strategies are essential for the ECB to manage the Eurozone economy effectively. Lagarde’s remarks suggest that geopolitical views, not just economic data, can influence currency markets in ways that models may not fully recognize. When she mentioned the dollar’s unexpected weakness, she indicated a loss of confidence—not necessarily in the dollar itself, but in the political systems that guide it. This kind of shift takes time. It reminded us that currencies also depend on belief systems, not just statistics. Her comments on doubts about U.S. policy are important. We see this as a sign that confidence is shifting back toward Europe, even with its own challenges. Right now, Europe appears to be the more stable option, especially given the recent turmoil in U.S. institutions. This perception, backed by slightly better Eurozone data, has led to increased interest in the Euro, which is now trading in the 1.1175 range against the dollar. While it’s not a strong rally, it shows noticeable improvement.Eurozone Economic Strategies and Their Impact

The European Central Bank focuses on maintaining price stability using various tools to achieve a 2% inflation target. Typically, rate adjustments are its primary method. Higher rates usually draw in capital, enhancing the Euro’s value. When the economy needs stimulation, the ECB actively engages in asset markets. Through QE—essentially a liquidity boost—they inject euros into the economy by purchasing financial assets. However, this strategy can reduce the Euro’s value due to the increase in currency circulation. Recently, though, we’ve seen a reduction in QE. As inflation nears its target, the ECB’s approach has shifted. They’re no longer making large reinvestments, and bond holdings are starting to decrease—a process known as Quantitative Tightening. Fewer bonds are being rolled over, which typically leads to a stronger Euro. When spending slows and rates remain high, the Euro often benefits from this tighter environment. Currently, multiple factors are in play: global trust issues, a cautious ECB nearing the end of its reinvestment era, and a Euro gaining slightly more attention. These shifts are crucial moving forward, as changes in policy can create and remove opportunities quickly. Traders dealing with derivatives should closely monitor not just usual price and rate indicators, but also timing. If ECB tightening continues—especially during stable market conditions—the Euro might gain more solid ground. The opportunity for options that benefit from low-volatility increases may not last long. Additionally, it’s crucial to watch developments in the U.S., especially regarding fiscal discussions and Federal Reserve policy clarity. If confidence in the U.S. weakens while the ECB tightens and Eurozone indicators improve, we could see a quick tilt toward the Euro. The market will pick up on this before it makes headlines. Being prepared and responsive to data is more critical than ever. With Lagarde emphasizing messages of stability, it’s important to pay close attention to shifts in sentiment—especially in key forward-looking metrics, such as five-year breakevens and cross-asset correlations. Planning derivative trades ahead of these points, especially considering the yield spreads between Bunds and Treasuries, could offer better insights. Increasingly, positioning data shows more participants beginning to invest in Euro-related assets. This doesn’t mean it’s without risk. Trade volumes and spikes in volatility could still surprise us, especially if central bank comments or political events change the outlook. For now, though, there is some actionable upside for the Euro while longer-term policy trends develop. We are positioning ourselves with that in mind. Create your live VT Markets account and start trading now.S&P 500 E-mini futures trade below 5947.0, signaling bearish setups with identified downside targets

Today’s S&P 500 analysis by tradeCompass uses volume profile, liquidity pools, and VWAP to determine market direction. Currently, the market is bearish, with prices below 5947 and a prevailing price currently at 5931.00, which is about a 0.75% drop from Friday’s close.

In this bearish trend, the market is trading below the critical level of 5947, suggesting a negative outlook. A short entry zone is identified around 5933–5934, near today’s VWAP. Bearish targets are set at important liquidity zones: 5916.0, 5908.5, 5900.0, 5864.0, and 5838.0, based on volume profile and VWAP.

Bullish Outlook and Targets

If the market reverses and moves above 5953.5, a bullish outlook may be activated, ending the current bearish scenario. Potential bullish targets are: 5966.0, 5974.0, 5977.0, and 5994.0. These points align with significant liquidity levels and may attract market participants’ interest. The tradeCompass tool accommodates various trading styles by pinpointing where institutional movements are likely. This analysis is meant to guide rather than predict, requiring traders to apply their own strategies for entry, stop loss, and position size. This analysis provides a clear view of potential price reactions in the S&P 500 futures, based on current positioning compared to institutional reference points like VWAP and known liquidity levels. With prices below 5947, selling pressure persists, as volume shows committed sellers below this threshold. The concept is that when the market stays beneath a recent support level and respects it as resistance, that former support becomes a tighter short zone. The recommendation to consider short trades around 5933–5934, particularly with the price near today’s VWAP, arises from the expectation that the auction remains skewed below value and sellers maintain control. We’ve noted that when prices repeatedly struggle to rise above the intraday average or reclaim a broken structure, it often leads to tests of lower demand areas. The focus on 5916.0 and nearby lows like 5908.5 and 5900.0 indicates congested volume areas, highlighting places where liquidity previously dried up and buying interest might return.Downside Pressure and Volume Analysis

If selling intensifies, the mention of 5864.0 and 5838.0 highlights levels where longer-term participants have historically defended price. These levels are not arbitrary; they are based on past volume activity where future orders likely wait. This analysis emphasizes recognizing reactive zones that have provided resistance in the past. Conversely, the rationale for abandoning a short position above 5953.5 is strong. If prices move back above this level and hold, it suggests a failed breakdown. Such action often leads to a quick reversal, inviting former shorts to cover while new longs enter. This could open a path toward fresh liquidity at 5966.0 and 5974.0. Above these, levels like 5977.0 or even 5994.0 may become battlegrounds, not due to their magical properties but because buyers and sellers have frequently clashed at these points. For traders focused on derivatives, a range-based approach around these defined levels is essential for execution. Pre-plan your orders. Don’t just rely on price levels; wait for confirmation and changes in order flow, especially during quieter trading times or before key data releases. Once price interacts with a level, base your decisions on what the price indicates—not on instinct. If there’s a failure to break through or a strong rejection, recognize that signal. We use the tradeCompass data as a filter, overlaying it with our risk tolerance and trade timing. These zones minimize noise, but patience in waiting for market intent is crucial to transforming short-term wins into well-developed trade ideas. Use these zones to define your exit points and how much you might lose if wrong; otherwise, you risk flipping your positions without conviction. As of now, with VWAP trending downward and volume increasing beneath yesterday’s close, we should heed this signal instead of anticipating reversals every time price stalls. Whether a macro trigger or a short-covering rally shifts sentiment, let that change come with volume and a hold above the invalidation level. In the meantime, we remain cautious but ready. Create your live VT Markets account and start trading now.Retail sales in China grew by 5.1% year-on-year, and industrial production increased by 6.1%.

China’s retail sales for April grew by 5.1% compared to last year, falling short of the expected 5.5% and down from March’s 5.9%. Industrial production rose by 6.1% year-on-year, beating the expected 5.5% but easing from last month’s impressive 7.7%.

Fixed asset investment saw a 4% increase year-to-date through April, slightly below the projected 4.2% and unchanged from March’s results. These numbers kept the Australian Dollar stable against the US Dollar at around 0.6400.

Australian Dollar Performance

The Australian Dollar had mixed results against major currencies, showing strength against the US Dollar but fluctuating against others like the Euro, Pound, and Yen. It dipped by 0.14% against the US Dollar, while remaining stable or slightly lower against other major currencies. The latest Chinese economic data presents a mixed view. Retail sales in April grew by 5.1%, slightly below the expected 5.5% and a significant drop from March’s 5.9%. This indicates that consumers may be spending less after a period of increased activity. On the other hand, industrial production rose by 6.1%, surpassing forecasts but down from the surprising 7.7% rise the month before. Fixed asset investment also grew by 4% through April but showed no month-to-month change and fell short of expectations. Despite these mixed signals, the markets remained calm. The Australian Dollar showed little reaction to the softer retail numbers, indicating that investors had anticipated some disappointment, especially in consumer spending. With weak private-sector demand, the focus seems to be shifting towards industrial strength and government-led investment.Implications for Traders

The Australian Dollar fell slightly—approximately 0.14%—against the US Dollar but held steady against the Euro, Pound, and Yen. This behavior suggests there’s currently no significant repositioning happening. The Dollar remains near 0.6400, which has become an informal support level. We might see tighter ranges if there are no broader catalysts. For derivatives traders, the latest Chinese data points to a gentler growth trajectory, particularly in areas tied to post-pandemic recovery. This could impact commodity demand, especially for key Australian exports like resources and energy. Changes to yield expectations or trade balances may arise, so it’s essential to watch for any forward-looking indicators from Beijing regarding potential support measures. Aussie pairs are currently reflecting these trends without major reactions. It’s important to monitor implied volatility levels, as subdued premiums indicate stable positioning and modest near-term movement expectations. However, any headline suggesting a policy shift or a sharper slowdown could change that quickly. Levels are crucial. If the 0.6400 level faces downward pressure, keep an eye on whether trading volume increases. A sustained break below this level may require some repricing, especially affecting interest-sensitive markets. Conversely, if the pair remains strong and Chinese authorities indicate stimulus, we could see renewed interest in short-term bullish positions. For now, we are keeping a close watch. The current figures haven’t caused significant changes but have introduced uncertainties into the recovery narrative. We’re not changing our exposure yet but are focusing on next month’s data and any signs from policymakers regarding this slowdown. If consumer strength continues to weaken and investment remains flat, we may need to adjust our approach. Pay attention to changes in skew for insights on where option writers anticipate growing risks. Create your live VT Markets account and start trading now.China’s industrial output rises 6.1% year-over-year in April 2025, exceeding expectations but falling short of previous results

In April 2025, China’s economic data showed mixed results. Industrial production grew by 6.1% compared to last year, exceeding expectations of 5.5% but down from 7.7% in the previous month.

Retail sales increased by 5.1% year-on-year. This was below the expected 5.5% and less than the 5.9% growth from March. The unemployment rate was 5.1%, slightly better than the predicted 5.2%, matching the previous month’s figure.

From January to April, fixed investment rose by 4% year-on-year, just short of the predicted 4.2%. Retail sales during this period grew by 3.7%, slightly up from 3.6% earlier.

Industrial production for the same months rose by 6.4% year-on-year, below the earlier rate of 6.5%.

The April 2025 data shows a mixed economic performance in China, with some strengths but also signs of weakness. Industrial production exceeded expectations at 6.1% year-on-year, but this indicates a slowdown from the 7.7% in March. This slight cooling shouldn’t be ignored, as it suggests that even if production is strong, there might be less demand or changes in inventory.

Retail sales dropped below expectations and lagged behind the previous month. The 5.1% increase was lower than forecasted and less than March’s growth. This decline is concerning, as domestic spending should ideally support the economy, especially when external conditions are uncertain. The overall increase in spending from January to April rose faintly to 3.7%, indicating some hesitation among consumers or changes in their income and confidence.

The jobless rate fell to 5.1%, just above expectations and matching the previous month’s rate. While this is somewhat positive, it shows that employment is stable but not growing. This steadiness is comforting, but it doesn’t promote much economic expansion, especially if consumer spending remains low.

In terms of investments, fixed asset investment from January to April rose by 4%, falling short of expectations. This suggests that businesses may be hesitant to commit to long-term plans, or infrastructure development hasn’t picked up enough beyond government-led projects.

Over the same period, industrial output increased by 6.4% year-on-year, just below previous figures. This small slowdown reinforces the monthly data, showing that while output is strong, the growth rate isn’t climbing as quickly as before.

For those analyzing risks in the derivatives markets, here’s an important takeaway: the weak retail numbers and slowing production growth indicate waning confidence in domestic demand. This can limit pricing power for some sectors and negatively affect profit margins. A tight labor market and stable employment offer some protection, but it isn’t enough to improve overall sentiment.

Therefore, we should pay attention to the volatility that arises from these data discrepancies. If consumer spending continues to struggle, we may see further price adjustments, especially in consumer-facing industries. Additionally, a decline in industrial momentum could warrant caution with investments connected to cyclical growth, particularly if May’s data confirms this trend.

Monitoring interest rate positioning is also crucial, especially regarding future expectations for demand recovery. If upcoming data continues to fall short of forecasts, especially in retail and investment, we might see adjustments in pricing.

There’s little margin for error when decisions are based on shaky readings. It’s best to focus on how monthly data changes are reacting to economic indicators. This perspective helps to understand the mood of the market better and where adjustments may be needed in uncertain times ahead.

Gold approaches $3,250 due to rising safe-haven demand amid US economic concerns

Gold prices have been rising due to increased demand for safe investments following a downgrade of the US credit rating. This downgrade is based on projections that US federal debt will rise to 134% of GDP by 2035, up from 98% in 2023.

Currently, the market value of gold is about $3,230 per troy ounce amid worries about the US economy. The credit rating was lowered from Aaa to Aa1, which reflects rising debt levels and increased interest payment burdens.

Challenges to the US Fiscal Position

This downgrade comes after similar actions by other agencies, with deficits expected to grow due to higher spending, increased debt costs, and lower tax revenue. Last week, gold prices fell by over 3% as optimism grew over a potential US-China trade agreement and a possible US-Iran nuclear deal. Disappointing US economic data has increased expectations for rate cuts by the Federal Reserve. The Consumer Sentiment Index dropped to 50.8 in May, marking the fifth straight month of decline, while predictions expected it to rise to 53.4. Investing in gold is considered a safe choice during uncertain times and a way to guard against inflation. Central banks hold significant amounts of gold. A strong US Dollar typically keeps gold prices stable, while a weaker Dollar can lead to higher prices. The recent rise in gold prices is linked to the downgrade of US credit. This change in credit rating reflects serious concerns: forecasts indicate federal debt may rise to 134% of GDP by 2035, compared to 98% today. This situation increases the cost of borrowing for the US government, as investors reassess risk. The repeated downgrades from various agencies highlight growing worries about ongoing deficits, high spending, and decreasing tax revenue. When confidence in the US government’s finances falters, gold prices often increase as investors seek to protect their portfolios from currency risk and asset depreciation.Concern Over Economic Indicators

The US economy is sending mixed signals, with consumer sentiment metrics dropping consistently. In May, the index fell to 50.8, while a slight improvement had been expected. This decline over five consecutive months suggests deeper concerns rather than just temporary issues. If consumers cut back on spending, corporate profits and investments could decline. The Federal Reserve uses such data to guide its rate policy, so the market is shifting toward expectations of rate cuts in the coming months. Recently, gold prices fell about 3% as optimism grew over easing tensions in two major areas: US-China trade talks and potential agreements with Iran. These signs of stability reduced demand for safe-haven assets, even if just temporarily. However, with increasing debt costs and expectations of rate cuts, support for gold remains strong. Historically, gold thrives when interest rates are low because the appeal of holding non-yielding assets increases. Additionally, fluctuations in the US Dollar affect gold prices. A strong Dollar can limit gold’s price rise since it makes gold more expensive for foreign buyers. But when the Dollar weakens, gold prices typically increase. Looking ahead, it’s clear that fiscal risks and interest rate expectations will continue to evolve. As traders, we need to monitor these changes in the fixed-income markets and their effects. If the Federal Reserve makes a clearer shift in policy, gold may react even more pronouncedly. Central banks continue to buy gold for their reserves, indicating ongoing demand amidst global inflation pressures. There is a fine balance between declining consumer confidence, shifting rate expectations, and political instability abroad. In the near term, market volatility will depend on upcoming economic data, Treasury auctions, and possible government interventions. These factors may lead to significant fluctuations in gold options across different time frames, especially with implied volatility near seasonal highs. Create your live VT Markets account and start trading now.Uchida plans to continue raising interest rates if Japan’s economy and prices meet expectations, despite trade uncertainties.

Deputy Governor Uchida of the Bank of Japan said that interest rates will rise if the economy and prices improve as expected. However, there is still a lot of uncertainty regarding trade policies worldwide.

Japan’s underlying inflation is expected to pick up again after a period of slow growth. Uchida recognizes that recent price hikes are impacting consumer spending negatively.