The UK’s total trade deficit narrowed to £4.34B in December, down from £6.116B previously

The UK’s total trade balance improved in December to £-4.34bn. This was up from £-6.116bn in the previous period.

A smaller UK trade deficit in December 2025 is a positive sign for the British Pound. It can point to stronger demand for UK exports, weaker demand for imports, or both. Either way, this tends to support the currency. We should consider positioning for GBP strength versus the US dollar and the euro in the coming weeks.

The UK’s three-month services index was flat at 0% in December, missing the 0.2% forecast

The UK Index of Services (3M/3M) was 0% in December. This was below the expected 0.2%.

The index tracks short-term changes in services output. It compares the latest three months with the previous three months. A 0% result means there was no growth over that period.

The 0.2% forecast suggested a small increase in activity. Instead, the flat reading shows services growth was weaker than expected in December.

The 0% growth rate for the three months to December 2025 is a clear warning sign. It suggests the economy entered the new year with little momentum. Missing expectations also points to underlying weakness that markets may not have fully priced in.

This stagnation, together with January 2026 inflation falling to 2.1%, makes a Bank of England rate cut more likely. Markets are now pricing in a possible cut by early summer. That is a big change from late 2025. As a result, we should expect the British Pound to weaken against major currencies such as the US Dollar and the Euro.

For UK equities, this outlook is negative, especially for the domestically focused FTSE 250. We should consider buying put options on the index to hedge against a possible downturn as earnings forecasts are cut. In the past, sharp slowdowns in services have often come before weaker stock markets, including during parts of the late 2010s.

In currency markets, the easiest move for Sterling still looks lower. Interest in GBP/USD put options expiring in April and May is rising. This suggests traders are positioning for a drop. Weak retail sales data for January has added to the bearish view.

Overall, this level of uncertainty often leads to higher volatility. We can use derivatives to position for larger price swings in UK assets over the next few weeks. One approach is to buy straddles on key services-sector stocks, which may move sharply after new economic data is released.

UK GDP grew 1.3% year on year in Q4, slightly above the 1.2% forecast

UK gross domestic product (GDP) rose 1.3% year on year in the fourth quarter. This was above the 1.2% forecast.

The release compares Q4 output with the same quarter a year earlier. The result beat expectations by 0.1 percentage points.

Because Q4 GDP was stronger than expected, the Bank of England has less reason to cut interest rates soon. Alongside January inflation, which is still high at 2.9%, this suggests the economy is holding up well. As a result, policymakers may sound more hawkish in the coming weeks.

For our positions, this supports a stronger British Pound. We see an opportunity in buying GBP/USD call options. The Federal Reserve is still signaling potential cuts later this year, which could widen the policy gap. In the second half of 2025, markets often underestimated UK economic strength, and similar Sterling trades worked well.

In interest rate markets, the upside GDP surprise suggests the SONIA futures curve may be mispriced. The market has been pricing in at least two rate cuts by the end of 2026, which now looks too optimistic. Selling the December 2026 SONIA futures contract is a prudent way to position for rates staying higher for longer.

This resilience is also supportive for UK-focused equities, especially the FTSE 250. Stronger domestic growth can lift earnings expectations, even if borrowing costs stay high. We think selling out-of-the-money puts on the FTSE 250 is a viable way to collect premium, based on the view that the data should help put a floor under the market.

UK manufacturing output rose 0.5% year on year in December, missing the 1.8% forecast

UK manufacturing output rose 0.5% year on year in December. This was below the 1.8% forecast.

This result shows slower annual growth than expected. It covers only manufacturing output and uses a year-on-year comparison.

Implications For Growth And Earnings

UK manufacturing output for December 2025 missed expectations by a wide margin, rising 0.5% instead of the forecast 1.8%. This points to a faster slowdown than we expected and supports the view that growth is cooling as we move into the new year. It also suggests added pressure on earnings, especially for industrial companies, in the next few quarters. This weak reading is reinforced by January 2026 inflation data, which fell unexpectedly to 2.1% and moved closer to the Bank of England’s target sooner than forecast. Online searches for “UK recession” have also risen 40% over the last three weeks, showing rising concern among the public and markets. Taken together, these signals raise the chance that the Bank of England shifts to a more dovish stance. In response, we see potential value in interest rate derivatives that benefit if the Bank holds rates or cuts them. Traders may consider buying short-term interest rate futures, such as the December 2026 SONIA contract, to position for lower rates later this year. In past slowdowns, markets have often priced in rate cuts quickly once the trend becomes clear, as seen in late 2007. The outlook for the British pound has also weakened. Slower growth and the chance of rate cuts usually make a currency less attractive. We would consider strategies that benefit from sterling weakness, such as buying GBP/USD put options or selling GBP futures against the euro. For equities, this release increases downside risk for the FTSE 100. Weaker manufacturing can hurt large industrial and materials firms in the index. Traders may look at buying FTSE 100 put options or selling futures, either as a hedge or as a short trade.Volatility Risk And Hedging

A run of weaker growth data often comes before a rise in market volatility. During the 2019 slowdown, similar releases were followed by a sharp jump in the VFTSE index. For this reason, volatility-linked derivatives may be a sensible way to help protect portfolios against the higher uncertainty we expect in the weeks ahead. Create your live VT Markets account and start trading now.UK GDP rose 0.1% in December, matching expectations and easing concerns about economic momentum

UK gross domestic product rose 0.1% month on month in December. This matched the 0.1% forecast.

The report showed only a small monthly increase at year-end. No other figures were included in the statement.

Uk Growth Remains Barely Positive

The December 2025 GDP figure confirms the UK economy is barely growing. It met expectations and avoided any immediate market shock. This flat trend suggests big directional bets on UK assets are risky for now. We expect markets to stay range-bound while investors digest the lack of momentum. This weak growth leaves the Bank of England in a tough spot. January’s inflation report still showed CPI at 4.0%, which is twice the official target. Calls to cut rates to support growth now clash with the need to keep rates higher to bring inflation down. This policy uncertainty is likely to be a key driver of derivatives pricing in the weeks ahead. We expect continued activity in SONIA interest rate futures as the debate over the first rate cut heats up. The market is pricing in a greater than 60% chance of a cut by the June meeting, but that view is not firm. Any hawkish comments from policymakers could quickly shift expectations, creating opportunities for nimble traders. For FX traders, this backdrop may limit the pound’s upside. In 2025, similar periods of slow growth kept sterling from rising much, even when global sentiment was strong. Selling out-of-the-money GBP/USD call options could be a sensible way to position for that capped upside.Uk Equity Volatility And Positioning

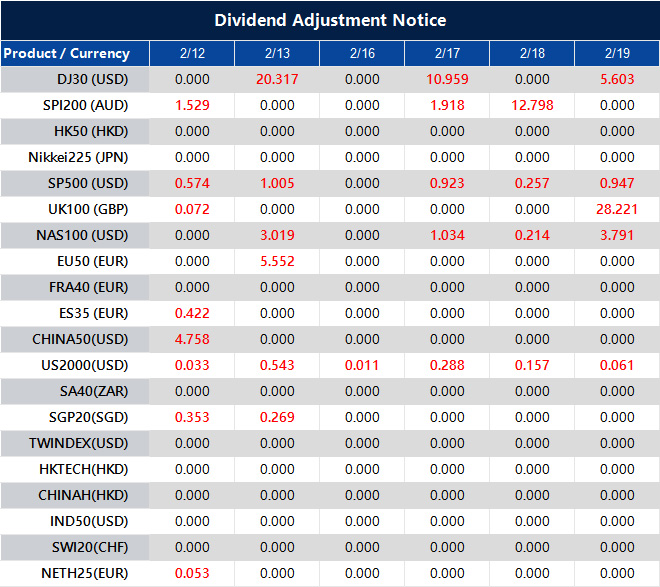

The outlook looks harder for UK-focused stocks, which may weigh more on the FTSE 250 than on the more global FTSE 100. With uncertainty still high, implied volatility may stay elevated. We see value in strategies such as FTSE 250 put spreads, which can benefit from a gradual decline while keeping risk defined. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Feb 12 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

UK industrial output fell 0.9% month on month in December, missing forecasts for no change

UK industrial production fell 0.9% month over month in December. This was weaker than the expected 0% change.

The -0.9% result for December 2025 points to a soft finish to the year for the UK economy. The downside surprise suggests the slowdown we were tracking was sharper than markets had priced in. This supports a more cautious stance on UK-specific assets going into Q1 2026.

This ongoing weakness in industry puts downward pressure on the British Pound. January 2026 data shows headline inflation fell to 2.3%, closer to the Bank of England’s target. That reduces the need to keep interest rates high. As a result, we should consider buying put options on GBP/USD, expecting the Bank may signal a shift toward rate cuts in the coming months.

For UK equities, the outlook is mixed. A weaker pound often helps the FTSE 100, since many of its companies earn revenue overseas and benefit when those earnings are converted back into sterling. In 2023, similar conditions coincided with FTSE 100 outperformance. Call options on the index could be a way to position for this effect.

By contrast, domestically focused firms in the FTSE 250 are more exposed to the slowdown shown in the production data. This is consistent with January 2026 retail sales, which fell 1.5% as consumer spending weakened. Put options on the FTSE 250 would be a practical hedge against this domestic fragility.

The next key catalyst is the preliminary Q4 2025 GDP release, due next week. If it confirms an economic contraction, markets may price in a rate cut by mid-2026 more firmly. That would add support to bearish views on the pound and on UK domestic stocks.

UK manufacturing output fell 0.5% month on month in December, missing expectations for no change

UK manufacturing output fell 0.5% month-on-month in December. This was below the 0% forecast.

December 2025 manufacturing data showed a 0.5% contraction. That is a clear miss versus expectations and supports the slowdown seen late last year. This weakness keeps the outlook for the British pound bearish. We should consider positioning for further downside in GBP/USD, using options to cap risk.

Recession Risks And Equity Hedges

This drop adds to rising recession fears. The Office for National Statistics (ONS) recently confirmed the UK entered a technical recession in the second half of 2025, with Q4 GDP down 0.3%. In this context, buying put options on the domestically focused FTSE 250 could be a sensible hedge against further weakening. The FTSE 250 has often lagged during UK recessions, including 2008, which makes it a useful stress indicator. The weak data also increases pressure on the Bank of England to cut rates sooner. January inflation stayed firm at 3.1%, but the slowdown in activity may still force policymakers to act. Derivatives markets now price an 80% chance of a cut by June 2026, so rate futures are a key area to watch. The unexpected miss in manufacturing also points to higher volatility in UK assets in the coming weeks. For traders who expect bigger moves but are unsure of direction, a long straddle on major UK bank stocks could be an effective approach. This strategy can benefit from a large move as markets weigh a weakening economy against stubborn inflation.Volatility Strategies For Uk Assets

Create your live VT Markets account and start trading now.UOB analysts say GBP/USD remains range-bound after the rally failed, with a brief dip below 1.3600 possible but not 1.3550

GBP/USD had a volatile session. It rose to 1.3712, then fell to 1.3610 during the New York session. It later closed near 1.3628.

In the near term, there is a risk of a brief dip below 1.3600. However, a deeper move down to 1.3550 is not expected.

Near Term Levels And Momentum

For the decline to continue, the pair would need to stay below 1.3675. Minor resistance sits at 1.3650. Over the next 1–3 weeks, upward momentum appears to be fading. The pair is expected to trade in a range between 1.3550 and 1.3700. This piece was produced with the help of an Artificial Intelligence tool and reviewed by an editor. It was published by the FXStreet Insights Team, which selects market observations from external sources and adds notes from internal and external analysts. The recent GBP/USD volatility—spiking to 1.3712 and then dropping sharply—suggests the uptrend is losing strength. The initial jump likely followed the surprise rise in the UK’s January inflation data, which came in at 2.3% last week, slightly above expectations. We now expect a period of sideways trading.Options Positioning For Range Trading

The sharp drop from the highs was driven by a stronger-than-expected U.S. jobs report. The report showed the economy added more than 250,000 jobs, supporting a stronger dollar. Even so, the move lower has not turned into sustained downside momentum. This points to a push-and-pull between the two currencies and supports our view that GBP is unlikely to trend strongly in either direction in the near term. For derivatives traders, this shift favors strategies that benefit from limited price movement and lower volatility in the weeks ahead. If GBP/USD stays between 1.3550 and 1.3700, selling options—such as short straddles or strangles—may be attractive. These trades can benefit from time decay as long as the pair remains inside this expected range. In the fourth quarter of 2025, GBP/USD moved gradually higher on hopes that the Bank of England would cut rates more slowly than the Federal Reserve. A sustained break below 1.3550 would challenge the range-trading view and suggest the dollar is becoming the dominant market theme again. Traders should also watch resistance near 1.3675. If the pair cannot break above it, the sideways bias remains in place. Create your live VT Markets account and start trading now.EUR/USD slips to 1.1860 for a third session as US jobs data reduces expectations of Fed rate cuts

EUR/USD fell for a third straight day and traded near 1.1860 in early European hours on Thursday. Traders are watching US weekly Initial Jobless Claims, followed by Friday’s US CPI inflation report.

The US dollar strengthened after new US labour data lowered expectations of a March Federal Reserve rate cut. US Nonfarm Payrolls rose by 130,000 in January versus a forecast of 70,000. The Unemployment Rate edged down to 4.3% from 4.4% in December, compared with an expected 4.4%.