UK house prices rose by 0.5%, exceeding expectations due to favorable conditions for buyers.

In May, UK house prices increased by 0.5%, exceeding the expected rise of 0.1% from the previous month. This information was released by Nationwide Building Society on June 2, 2025. This increase is a positive change from April, which saw a drop of 0.6%.

The report shows that mortgage approvals indicate strong market activity now that the stamp duty holiday has ended. Despite global economic uncertainties, the UK homebuying environment appears favorable.

Japanese Prime Minister reaffirms strong stance on US tariffs after Akazawa’s visit to Washington

Japan’s Prime Minister Ishiba has firmly stated that Japan will not back down on US tariffs. This declaration comes after Akazawa’s recent trip to Washington, which resulted in little progress.

No agreements have been made regarding tariff cuts, and Akazawa plans to return to the US later this week for more talks.

There are only 37 days left to find a solution. Both sides feel the pressure to reach a deal within this time frame.

With just 37 days remaining, Tokyo’s stance remains strong. Ishiba’s commitment not to yield on US tariffs highlights Japan’s aim to resist outside pressure while bolstering local support. His comments come right after Akazawa’s meetings in Washington, which ended without any advancements, showing a clear stalemate. This situation is already affecting derivative markets.

Currently, we see early signs of volatility, especially in options related to Japanese export-focused indices. The absence of an agreement suggests uncertainty will persist, leading to fluctuations in short-term expected volatility. Traders watching price movements through gamma and vega lenses may need to adjust strategies. The spread between implied and real prices has widened, likely in anticipation of news-driven changes.

Akazawa is getting ready to head back to Washington. Meanwhile, attention shifts to USD/JPY pairs and equity options sensitive to exports. Open interest in downside puts has quietly increased over the past day, likely from traders looking to hedge more tactically. As real-time news will significantly influence prices, a strategy that balances directional views with defined risks may help manage near-term exposure.

Traders should stay alert for the next ten trading sessions since negotiations could take longer than expected. The gap between what politicians say and what is economically necessary always creates uncertainty—something algorithms haven’t fully accounted for in trading volumes.

We should also watch for secondary effects. Currently, sector skews are expanding in the auto and tech-related options, hinting at a potential adjustment of earnings forecasts, even if tariffs stay the same. Markets often react before policy changes are confirmed, especially when negotiations stretch out without new developments.

Timing is crucial. As we approach the end of this 37-day deadline, the derivatives market will likely react strongly to even minor changes in statements from negotiators. Rising vega values may occur as traders prepare for sudden breakthroughs or setbacks in discussions. Skew patterns might shift if hedgers grow more concerned about downside risks.

We are monitoring positioning, both speculative and protective, and expect changes in futures basis and daily trading volume to provide early indicators. Remember, being patient does not mean being passive. In the coming weeks, a careful yet flexible strategy may yield better results as clarity remains elusive and risks grow.

EUR/USD has an expiry at 1.1350 today, potentially supporting price movements due to dollar weakness.

Today’s important forex expiration is at the 1.1350 level for EUR/USD, with significant expiries expected in the coming days. This could help support price movement, especially since the 100 and 200-hour moving averages are nearby at 1.1330-35.

The dollar is currently weaker as markets adjust to recent trade news. Trump’s tariffs have been reinstated temporarily, creating some negative sentiment around ongoing trade discussions with China.

Eur Usd Chart Levels

The key level that many traders are watching is 1.1350 for the EUR/USD pair, where several options will expire today. What makes this level important is its closeness to the 100 and 200-hour moving averages, which sit around 1.1330 to 1.1335. The combination of technical factors and option volumes often makes price movements more responsive in these areas, attracting scalpers and traders positioning around key expiries. The dollar has weakened, primarily due to how markets are responding to recent global trade events. The return of some tariff measures has caused investors to feel uneasy about the future of trade talks between Washington and Beijing. Traders see this change as a potential drag on US economic activity, leading to decreased demand for the dollar, particularly in pairs sensitive to broader market risks.Tactical Market Approach

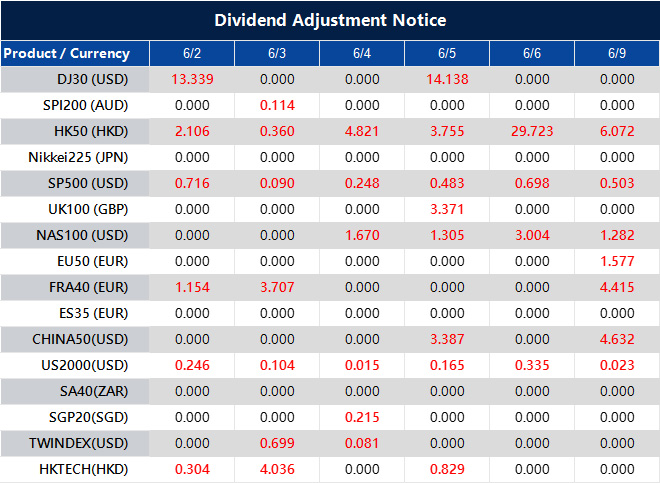

We are approaching the market from a tactical perspective, considering both the impact of options and short-term sentiment. With a number of expiry levels focused around the current price, and more expected later in the week, even small changes in market tone could increase volatility. Historically, when prices interact with dense option clusters near moving averages, this often leads to price consolidation or quick rejections on either side, which usually fade as the expiry passes. Powell’s recent comments didn’t significantly alter the overall market tone, and the economic data calendar is light in the near term. This makes it easier for headlines or technical patterns to influence market activity. When liquidity is low, these expiries often have a bigger impact than usual. Therefore, traders should be cautious about price movements around the discussed levels. Taking on a position that doesn’t align with expiring adjustments could be ineffective this week. Many traders we spoke with are adjusting their order placements slightly earlier than normal, due to strike levels exerting pressure during the London and New York trading sessions. Finally, market flows are primarily driven by events and are short-term focused. Our view is that any retests of significant levels will attract some hedging interest before trading resumes its normal course after expiry. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 02 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Oil prices increase even with OPEC+ output rise, while the US dollar weakens due to market tensions

Oil prices climbed on Monday as OPEC+ announced a production increase of 411,000 barrels per day for July, following similar hikes in May and June. This increase comes amid rising geopolitical tensions after Ukraine’s drone attacks on Russia. U.S. Senators are also suggesting sanctions that could tighten energy markets even more.

The U.S. dollar weakened overall, while the yen gained strength after the Bank of Japan raised its provisions for potential losses on Japanese Government Bonds. This decision, including a 100% provisioning ratio for fiscal 2024, signals readiness for higher interest rates, encouraging confidence in yen assets.

Federal Reserve Governor Christopher Waller indicated he is open to rate cuts later this year, suggesting that inflation from tariffs should not control monetary policy. He emphasized that if tariffs stay low and core inflation declines, rate cuts might be appropriate.

Asian factory activity in May faced hurdles due to trade tensions and excess supply from China. Manufacturing PMIs in Japan, South Korea, and China showed contraction, but Japan’s PMI improved slightly to 49.4. However, business confidence grew, and employment increased as companies anticipated a recovery in demand.

China rejected U.S. claims regarding trade deal violations as “groundless” and affirmed its compliance with the Geneva agreement. In response to U.S. export controls and visa revocations, Beijing argued that these actions have shaken trade relations.

In Poland, the nationalist Nawrocki won the presidency, aligning with right-wing policies and contrasting with recent pro-EU leadership.

The events suggest a clear trend in the markets, especially related to macroeconomic shifts and energy products.

Oil prices benefited from cautious production increases and geopolitical risks. OPEC+’s addition of 411,000 barrels per day reflects caution rather than aggressive expansion. Following Ukraine’s drone strikes on Russian territory, risk premiums have risen, introducing potential threats to both supply and investor sentiment. The possibility of more U.S. sanctions, hinted at by Senators, adds supportive pressure on prices. For traders dealing with crude derivatives, this raises challenges for short positions and may make longer-term call options more appealing, provided implied volatility matches realized fluctuations.

In currency markets, the dollar’s decline stood out. This drop is less about domestic weakness and more about relative strengths elsewhere. The yen gained ground, not through intervention, but because of increased provisions from the Bank of Japan. By adjusting their reserve strategy and fully covering JGB losses, the BoJ signaled a willingness to consider rate increases. This approach reflects growing confidence in the economy’s ability to handle higher debt costs. Although rate hikes are not imminent, this development supports long positions in yen.

Waller from the Fed mentioned that trade or tariff-driven inflation won’t automatically prompt a defensive response from policymakers. He pointed out that as long as core inflation decreases and tariff increases stay limited, there could be opportunities to lower rates. This is significant because it indicates that economic fundamentals will shape policy decisions more than political factors. If futures markets have already priced in a dovish outlook, examining skew and tail risks in rate-linked contracts becomes important.

Asian industrial data showed weakness, but there was a key point: even though PMIs for Japan, Korea, and China are below 50, some positive signs emerged. Employment in Japan rose, and business outlooks improved slightly. With less pessimism about domestic demand, it might be worth considering relative value strategies, such as favoring Nikkei-linked investments over China-focused ones. However, China’s manufacturing oversupply remains a challenge and won’t disappear with talk alone.

Regarding U.S.–China trade tensions, China’s swift denial of recent accusations about adherence to Geneva conventions and export-control violations was notable. The U.S. move to impose additional visa limits and controls is seen as an escalation affecting regional capital flow assumptions. For those investing in Asia-Pacific derivatives, it’s essential to account for longer-term impacts: sanctions may not cause immediate volatility, but they can distort yields and performance among ADRs and local listings.

Eastern European politics also influenced market sentiment. Nawrocki’s election in Poland signals a shift back to conservative policies. Although executive power is not absolute, this change contrasts with Warsaw’s recent pro-EU stance. Currency futures related to regional pairs might soon reflect these new leanings—possibly more evident in cross-border capital flows or smaller bond markets than in major sovereign pricing. Nonetheless, this growing divergence, with Brussels likely trying to maintain policy unity, could add fresh strain to euro-related sentiment indices.

Jamie Dimon claims China will not yield to US trade pressures at a forum

JPMorgan CEO Jamie Dimon spoke about urgent issues at the 2025 Reagan National Economic Forum. He highlighted the need for the US to enhance its trade strategies and pointed out various domestic problems, including permitting, regulations, and taxes.

Dimon also emphasized the importance of managing immigration, education, and healthcare effectively, while reinforcing military alliances. He recognized China’s mixed role as both a potential rival and a country achieving some successes.

Future Concerns For The United States

Dimon warned about the future of the United States, stating that without maintaining its military and economic leadership, it could lose its reserve currency status in 40 years. After returning from China, he observed that China is not afraid of the US and cautioned against thinking they will simply accept American leadership. His comments conveyed a sense of urgency: the US must not be complacent about its economic and political systems. Dimon pointed to failures in key government functions—excessive red tape, slow permit processes, and policies that discourage business investment. His concerns about taxes and regulations suggest that current policies may hinder innovation and growth. He also addressed ongoing issues like immigration, healthcare, and education. These are not just social problems; they are critical for the workforce. A decline in talent quality or insufficient healthcare will result in a less competitive labor force, negatively impacting businesses and markets. His mention of military partnerships highlights the connection between national strength and market stability for those who take a long-term view.A Strategic Signal

The most significant takeaway from his talk is his warning about the US dollar. Suggesting a 40-year countdown to losing reserve currency status is not mere speculation; it’s a strategic alert. When a nation’s economic or military strength weakens, global institutions begin to reassess risks. This shift affects asset allocation, capital flow across borders, and the world’s trust in currencies. When Dimon comes back from China stating they aren’t intimidated by the US, it implies more than just geopolitics. It relates to pricing dynamics, profit pressures, and market volatility. The concern is not just about short-term shocks; it’s about reshaping the global order, which is crucial for those of us focused on macroeconomic exposure. The upcoming weeks require proactive planning, not guesswork. We should be strategically hedging rather than waiting for signs. We need to consider options linked to currency exposure, especially those with longer durations. Also, keeping an eye on volatility trends in indices that are sensitive to global trade can provide valuable insights. As we prepare for Q1, it makes sense to adjust our expectations of implied versus realized volatility based on interest rate predictions. The rhetoric we hear is often a precursor to policy changes. Costs will change quickly if expectations shift regarding monetary stability. Inaction is not an option. The warning signs are clear. Create your live VT Markets account and start trading now.Japan’s corporate capital spending rose 6.4% in Q1, pointing to strong domestic demand despite GDP decline.

Japanese companies increased their capital spending by 6.4% in Q1 compared to last year, bouncing back from a slight drop in Q4. This shows that local demand is strong, even with wider economic challenges. Data from the Ministry of Finance reveals a 1.6% rise in capital expenditure when adjusted for seasonal changes, indicating steady growth.

These positive numbers help offset weaker consumer spending and exports, which contributed to a preliminary 0.7% drop in annual GDP for Q1. Continued business investments, especially in technology, are attempts to tackle labor shortages caused by Japan’s ageing population. Corporate sales rose by 4.3%, and recurring profits went up by 3.8% year-on-year.

However, there are concerns about potential risks from U.S. tariffs that could impact export-focused companies and their future investment strategies. The revised GDP figures, coming out on June 9, will reflect this capital spending data. Japan’s capital spending for Q1 2025 grew by 6.4%, beating expectations of a 3.8% rise.

In simple terms, Japanese businesses are clearly investing more in themselves. A 6.4% increase in capital spending year-on-year is impressive, especially compared to the previous quarter’s drop. This is a bright sign — companies are not retreating; they are looking ahead, despite domestic and global challenges that could impact overall confidence.

Looking closer at the figures, the 1.6% growth from the previous quarter shows this spending isn’t just a one-time spike; it shows ongoing commitment. The uptick in investments, combined with higher sales and profits, means many businesses are still finding ways to grow, even as households cut back and exports face difficulties.

The Ministry’s data is crucial for adjusting GDP figures to be released soon. Since capital spending is a significant part of GDP, these stronger-than-expected results will likely lead to an upward revision. The initial Q1 GDP reading showed a 0.7% drop, but this new investment data could improve those estimates. While it may not completely change the picture, it shifts the focus from worrying decline to cautious stability.

Nonetheless, we must be aware of external threats. U.S. trade barriers might affect Japanese businesses, particularly those that rely on exporting machinery and vehicles. If new restrictions emerge, companies that planned to expand might reconsider those intentions, impacting various financial positions linked to industrial performance and stock market indices.

Key metrics to consider include the continued increase in corporate profits, which are up 3.8% from last year, indicating a healthy backdrop for investments. Companies have also been increasing spending on automation, which not only helps address labor shortages but also shows confidence in long-term projects. In the derivatives market, paying attention to these structural changes can influence strategies.

Economy Minister Matsuno, along with other cabinet members, has noted stable corporate behavior. This reassurance, supported by data, tends to bolster expectations for future government stimulus or monetary action.

In the short term, the revised GDP figure could trigger changes in implied volatility. Positions anticipating a deeper contraction may need adjustments. The response speed will depend on how strong the upward revisions are compared to current market prices. It’s important to remember that even though the GDP headline was negative, companies haven’t stopped spending.

Monitoring the machinery and construction sectors is crucial, as they often indicate future industrial momentum. Any hedges based on lower spending may require tighter management now. With Q1 capital investment exceeding forecasts by 260 basis points, there’s good reason to expect market positioning to adjust upward rather than decline.

Considering the ongoing export risks, we might prefer trades that offer asymmetric protection, especially in options related to sectors less affected by global trade issues. The trend toward technology investment is significant and is now reflected in earnings. This commitment to productivity through investment also helps establish clearer benchmarks for financial modeling. Adjusting risk assessments to reflect improved corporate sentiment, rather than solely reacting to consumer data, may produce more reliable signals.

The Bank of Japan announces full loss provision for bond transactions in fiscal 2024.

The Bank of Japan has announced that it will set aside 100% of potential losses from bond transactions for fiscal 2024. This decision aligns with a Nikkei report indicating that the Bank is preparing for potential losses on Japan Government Bonds (JGBs).

The Bank’s action comes as it expects interest rates to rise. By increasing its provisions, the Bank of Japan seeks to reduce the risks linked to bond transactions.

Understanding The 100 Percent Provision

The information is clear: the Bank of Japan is preparing for potential losses on government bonds next year. A 100% provision means the Bank is ready for losses that could match the worst expectations from its bond holdings. This decision is not random; the Nikkei’s report supports that this is a thoughtful response to expected changes in interest rates. Generally, bond values drop when interest rates rise. If the market anticipates rising rates due to inflation or changes in central policy, older bonds with lower interest become less attractive, leading to price declines. This is a concern for the Bank, which holds a large amount of these bonds. By setting aside enough funds to cover potential declines, the Bank demonstrates caution and prepares for unexpected market fluctuations. This situation is more than just an internal accounting measure. Central banks do not adjust their financial provisions lightly. Such actions indicate a readiness for significant interest rate changes—not just rumors but actual planning. For those involved with derivatives linked to interest rates or fixed-income products, it’s important to act now. Adjusting positions should happen immediately, not waiting for future policy meetings, as the probabilities have already shifted. Understanding this outlook requires not just reading sentiment but recognizing strategic changes. We must adapt our risk approach, moving from waiting for signals to proactively preparing.A Shift In Monetary Policy Approach

Kuroda’s successor is clearly adopting a different strategy. The previous gentle approach is disappearing. There is now more substance to the yield curve control adjustments. Policies that once seemed symbolic may soon become more direct. Although monetary tightening remains subtle, it is becoming a higher priority. In the upcoming meetings, it’s wise to revise pricing models with a reduced focus on flat rates and adjust volatility expectations accordingly. Positions that relied on stable yields may need adjustments or hedges. Additionally, we might see liquidity in some JGB futures contracts diminish quickly if counterparties tighten their balance sheets. The distinction between the central bank’s protective measures and the broader market implications was once clearer. Now, the Bank’s balance sheet sends strong signals. If they are planning for total write-down coverage in the near future, our current risk positions must reflect that risk is no longer just theoretical—it is anticipated. Create your live VT Markets account and start trading now.Rumors suggest Powell will resign on Monday, but there’s no evidence to support this claim.

Rumors have surfaced about Jerome Powell resigning as Chair of the Federal Reserve. Some suggest that Donald Trump plans to lower interest rates. However, these claims are viewed as unfounded and seem aimed at influencing Bitcoin trading.

Currently, there is no proof to back these rumors. Powell has stated he will serve until his term ends in May 2026. Recent legal rulings also restrict Trump’s power to remove him. Federal Reserve officials suggest that interest rates will likely stay steady for the next meeting.

These early-week rumors appear to be speculative attempts to impact pricing in sensitive markets. Although they are popular in social media and among retail commentators, they lack support from official sources. Powell’s term is confirmed to run until mid-2026, and the legal framework limits the ability to remove central bank appointees. This means it is unlikely there will be any major changes to the Fed in this administration or the next.

Clarida has previously emphasized the importance of Fed independence. Any credible challenge to this independence would show up in Treasury futures immediately. However, this hasn’t occurred. The two-year note is trading within its average range, and options do not indicate increased volatility due to leadership uncertainty. Thus, we can treat these rumors as background noise for now.

For those involved in rate-sensitive derivatives, clarity is found in the minutes and statements from the FOMC. Jefferson and Waller have both suggested that current inflation levels don’t support any immediate policy changes. With Powell still in charge and legal barriers to his removal in place, scenarios that would favor steepening the yield curve seem without foundation.

What matters now is positioning for the next CPI release and how implied volatility shifts as we approach the Fed’s meeting. We’re seeing long-duration investment flows concentrated around the middle of the curve, while gamma has mostly remained flat across various rate expirations. Caution in the market has led to weaker collars and wings, indicating that participants do not expect sudden changes from leadership changes. This is significant and should be monitored closely.

This week’s contracts suggest that carry is stable unless new dot projections prompt a repricing, which hasn’t occurred yet. As pricing continues to rely more on factual data than sensational headlines, we need to stay aware of the potential for discounted volatility linked to deeper rate hikes, but only when tied to credible indicators. Until that time, short flies and mid-curve volatility fades remain sensible strategies.

Australia’s inflation gauge experiences its biggest drop in over two and a half years, as job ads also decline

In May 2025, ANZ Job Advertisements dropped by 1.2% compared to a previous decline of 0.3%. This suggests a decrease in job opportunities across Australia during this time.

The Melbourne Institute’s monthly inflation gauge showed a 0.4% decline month-on-month, marking the largest drop in 33 months. On a yearly basis, inflation fell from 3.3% in April to 2.6%.