China’s Premier Li Qiang discusses new policy tools in Jakarta amidst economic and trade challenges

China’s Premier Li Qiang spoke at a symposium in Jakarta about the changing global economy. He said that China is looking at new policy tools and unconventional methods to adapt to these shifts.

He highlighted that the breakdown of industrial and supply chains along with rising trade barriers are affecting global economic growth. To address these challenges, China plans to boost its economic partnerships with more countries.

Amid lower US-EU trade tensions, WTI oil stays above $61.50, continuing its upward trend

WTI Oil prices are around $61.50 per barrel, benefiting from eased trade war concerns between the US and EU. US President Trump has postponed a 50% tariff on EU goods, originally set for June 1, to July 9.

EU Commission President Ursula von der Leyen has expressed a willingness to hold trade talks with the US and is asking for more time to reach a possible agreement. Earlier, there were threats of tariffs after an unfavorable trade proposal from Brussels to Washington.

Geopolitical Tensions Affecting Oil Prices

Geopolitical tensions are also supporting oil prices as Israel plans military action in Gaza. Worries about increased Iranian oil supply have decreased due to stalled US-Iran nuclear negotiations. However, an increase in oil output could limit price increases. OPEC+ may raise output by 411,000 barrels per day in July and might reverse its 2.2 million bpd production cut by the end of October. WTI Oil, a type of light and sweet crude oil mainly produced in the US, is affected by supply and demand, political instability, and OPEC decisions. Weekly API and EIA inventory reports also influence oil prices by indicating shifts in supply and demand. With WTI near $61.50 per barrel, recent market strength has largely resulted from reduced fears over transatlantic tariffs. The US decision to delay a significant 50% tariff on EU goods until July has eased risk sentiment. Investors are now hopeful for renewed discussions. Von der Leyen’s comments indicate that Brussels is open to trade talks if given more time, providing a temporary boost to market expectations.Short Term Trading Strategies

Nevertheless, postponing tariffs does not eliminate the threat. Resumed tensions in early July could create volatility, particularly if initial trade discussions fail. For energy contracts, any long positions should be approached with caution after the first week of July, especially with fresh data from EIA and API regarding inventory levels. Any calm sentiment could change quickly if rhetoric escalates or timelines slip without concrete outcomes. Geopolitical risks continue to influence market support. Israel’s strong statements about operations in Gaza highlight ongoing instability in the Middle East, but current disruptions in oil supply have not yet occurred. However, shifts in regional dynamics could tighten trading sentiment. Concerns about Iran boosting oil output have somewhat faded. US-Iran talks remain stalled, which reassures traders who were worried about oversupply earlier in the year. Iran’s lack of involvement in meaningful negotiations means Iranian oil remains sidelined, easing some downward pressure on crude prices. Nevertheless, this relief may be temporary. Production remains a concern. OPEC+ has indicated a 411,000 bpd output increase for July but is prepared to reverse the larger 2.2 million bpd cut by late Q3. Traders need to stay alert and track compliance and production updates, which can lead to significant market shifts. If OPEC+ accelerates its production plans, it could greatly affect spot prices and future contracts. The recent price increases are precarious—bolstered by diplomatic delays and temporary stability but vulnerable to supply decisions and sudden tensions. US inventory data will remain a key reference point as it often hints at discrepancies in expected versus actual demand. For short-term strategies, we are focusing on option premiums and implied volatility across contracts due to expire in late summer. The current backwardation isn’t severe, but new inventory builds or insights from OPEC ministers could widen intramonth spreads. Watching the Brent-WTI spread is also important, as it indicates transatlantic flows and export balance changes. Risk management involves being cautious with long or short positions, selectively adding protection or exposure based on shifting price drivers. Every change in geopolitical tone, inventory trends, and production quotas can weigh on positions. We are aligning closely with key data releases and real policy changes rather than just rhetoric. Create your live VT Markets account and start trading now.Neel Kashkari highlights the importance of uncertainty for US businesses and the Fed in a Tokyo speech

Minneapolis Federal Reserve President Neel Kashkari raised concerns about uncertainty impacting the Fed and US businesses. He highlighted the stagflation effects of tariffs and the risks involved if these tariffs continue.

Kashkari emphasized the need for clearer economic data by September and acknowledged the importance of upcoming trade negotiations. He also pointed out that immigration policy is causing businesses to rethink their investment plans.

Currency Movements

The US Dollar Index showed a slight rebound but was still down 0.30% for the day at 98.82. Over the past week, the US Dollar weakened against several major currencies, with the biggest drop against the New Zealand Dollar. EUR/USD stayed above 1.1400, supported by the ongoing weakness of the US Dollar. Meanwhile, GBP/USD was near a three-year high, benefiting from a weak Dollar, despite cautious market sentiment. Gold prices pulled back slightly from a recent two-week high. Kashkari’s statements highlight how policy choices beyond interest rates are increasingly affecting long-term expectations. When he mentions the stagflationary impact of tariffs, he refers to a troubling combination of slower economic growth and rising prices, which complicates monetary policy. Tariffs increase the cost of imported goods, putting pressure on consumers and raising input costs for businesses, potentially discouraging future investment due to uncertainty. He also indicated that we’ll have to wait until at least September for clearer economic data, suggesting that any policy decisions before then might be premature. The lack of clarity in trade talks encourages a cautious approach. Markets are very responsive to even small changes in negotiations, as tariffs influence both inflation and production, pulling monetary policy in opposing directions.Focus on Immigration Policy

Kashkari’s attention to immigration policy is noteworthy, as it’s not typically a key topic in monetary discussions. A reduced labor supply, especially in sectors already facing shortages, forces employers to either raise wages or limit operations. This situation puts pressure on inflation and can hinder growth if companies scale back. Kashkari’s comments suggest that businesses are already hesitating to build new factories or expand operations, which is an important point to consider. Examining how the markets are reacting, the US Dollar showed a slight increase but did not recover from its recent decline. A 0.30% drop today and broad weakness against major currencies indicate that market sentiment is driven more by overall uncertainty than short-term data. The NZD was the biggest gainer, reflecting regional confidence and the market’s tendency to move away from the Dollar when prompted. The EUR/USD remaining solid above 1.1400 is significant. Its strength is more about the weakness of the Dollar than the strength of the Euro. The same goes for GBP/USD, which is close to three-year highs. Although traders in sterling are cautious due to political uncertainties, they are still reacting quickly to soft Dollar flows. The recent dip in gold prices doesn’t signify a change in trend but is rather a natural cooldown after reaching two-week highs. Commodity responses often lag, and gold’s movements appear to follow shifts in Fed expectations. If market sentiment deteriorates or inflation increases again, gold prices could rise quickly. Given this backdrop, pursuing shorter-term strategies and revisiting hedging approaches makes sense. Options traders should keep an eye on implied volatilities, as periods of low data won’t last long. With September identified as a potential decision point by Kashkari, it seems reasonable to price in a premium for early to mid-autumn. Additionally, any directional trades should incorporate the expectation of slower capital spending by firms and higher price pressures, especially if key policy risks remain unresolved. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – May 26 ,2025

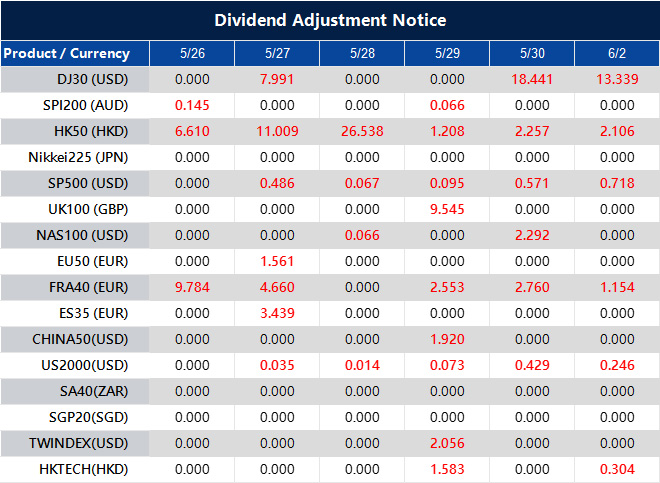

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The USD/CAD pair continues to decline, dropping below 1.3700 as USD selling persists.

The USD/CAD pair has continued its decline, slipping below 1.3700 and reaching its lowest point since October 2024. This drop is mainly due to a weaker US Dollar, driven by concerns about the US fiscal situation and expectations of lenient Federal Reserve policies.

The US Dollar Index (DXY) has fallen to a near one-month low. This change reflects worries about a projected $4 trillion increase in the US deficit over the next ten years. Softer inflation data in the US has fueled speculation that the Federal Reserve may cut interest rates to help boost economic growth.

Canadian Dollar Strength

On the other hand, the Canadian Dollar has shown strength due to unexpectedly strong Canadian core inflation figures. This reduces the chances of an interest rate cut by the Bank of Canada, even as crude oil prices dip slightly. The Canadian Dollar is influenced by several factors, including interest rates set by the Bank of Canada, oil prices, the health of the economy, inflation, and trade balance. Generally, higher interest rates and good economic data support the CAD. Rising oil prices can improve the trade balance and strengthen the currency. Conversely, economic weakness can cause the CAD’s value to drop. With USD/CAD clearly moving below the 1.3700 mark and hitting a level not seen since October, we see not only downward pressure on the US Dollar but also a surprising strength in the loonie. There are two factors at play here: US fiscal challenges and inflation data suggest a softer approach from the Fed, while stronger Canadian inflation keeps the possibility of rate cuts from the Bank of Canada low. These trends indicate a change in sentiment. The drop in the US Dollar Index to a near one-month low shows that the market is not just reacting to inflation; it is also anticipating future stress on the balance sheet. The expected $4 trillion increase in the US deficit over the next decade raises long-term concerns about interest rates and the demand for the dollar. When inflation data weakens alongside fiscal warnings, the dollar faces additional pressure—something we saw again this week.Central Bank Dynamics

The situation benefits Canada’s rate-setting division. The Bank of Canada isn’t necessarily adopting a hawkish stance, but it doesn’t feel as pressured to act for growth. Strong core inflation figures have ruled out immediate policy changes. While a slight drop in oil prices usually weakens the CAD, better domestic data stability is outweighing this effect. This results in a delicate positioning environment. We are in a phase where traders need clarity, precision, and agility in response to central bank shifts. Market indicators suggest traders expect the Fed to adjust rates more quickly, which affects rate spreads. As macro spreads widen against the USD, trades based on relative value for the CAD look more appealing, especially as trends improve. Recently, the correlation between commodities and currency has weakened. Therefore, oil’s modest price drop hasn’t significantly impacted the support for the loonie as earlier trends would suggest. The CAD’s lack of a strong reaction to falling oil prices indicates that traders are focused on how central banks differ, and currently, Canada has the advantage due to its inflation profile. As we move forward, the likelihood of volatility increases around policy announcements and key economic reports. It’s crucial for traders not only to hedge against directional changes but also to manage the risks associated with volatility shifts. With expectations for US rate cuts gaining momentum, gamma positioning will likely become more aggressive. Upcoming data on CPI, employment, and central bank comments will be very important. We have observed that options markets are biased toward deeper downside strikes in the pair, showing trader positioning beyond just sentiment, especially for longer durations. This asymmetry suggests that the broader market views these levels as significant, possibly marking a recalibration point. It emphasizes the need for hedging strategies to consider not just the short-term but also longer calendar spreads or protection against volatility. Maintaining flexibility across different timeframes has become more beneficial than sticking to fixed delta positions. With rising expectations built into futures pricing, there’s now a stronger case for adjusting implied volatility assumptions. If the economic divergence continues, the risk of price adjustments may increase, especially as traders shift from predicting to executing strategies. Create your live VT Markets account and start trading now.As trade tensions ease, gold price stays below $3,335, attracting sellers’ interest

The price of gold has dipped slightly to $3,335 during Monday’s trading session in Asia. This decrease comes as worries about a global trade war ease. US President Donald Trump set a deadline of July 9 for a trade deal with the European Union, stepping back from his earlier warning of a 50% tariff starting June 1.

Traders are paying close attention to the US-Japan trade talks and other global economies, as these can influence gold prices. Concerns about inflation are resurfacing, especially after Moody’s downgraded the US credit rating from ‘Aaa’ to ‘Aa1’. This downgrade is likely to support gold prices.

Record Purchases by Central Banks

Central banks are buying gold to diversify their reserves. In 2022, they purchased a record 1,136 tonnes, valued at around $70 billion. This is the highest total on record, with countries like China, India, and Turkey leading the way in increasing their gold reserves. Gold prices are influenced by factors such as geopolitical tensions and the strength of the US Dollar. Generally, the price of gold increases when interest rates are low and the Dollar weakens. However, it tends to fall when the Dollar is strong. Gold and the Dollar often move in opposite directions, and gold is seen as a safeguard against inflation and currency depreciation. Looking more closely at recent changes, the small decline to $3,335 reflects more than just the easing trade conflict fears. The US administration’s announcement of a potential deal with the European Union by July 9 has lessened earlier concerns. By stepping back from a major tariff increase, the US government has provided a short-term reprieve for global markets. The bond market responded with slightly higher yields, and risk assets showed modest gains. For keen observers, the reaction in the gold market has been fairly stable. This isn’t surprising, as gold often reflects broader systemic anxieties rather than daily news. Although the thaw in trade tensions may have affected gold’s short-term momentum, the larger economic picture deserves more attention.Concerns Over US Sovereign Debt

Moody’s downgrade of US sovereign debt to Aa1 is significant, indicating worries about long-term fiscal management and government stability. Even if policymakers downplay this rating cut, markets are likely to react, leading to higher borrowing costs and questioning the Dollar’s status as the world’s reserve currency in the future. This situation is changing how investors approach inflation hedging. After months of fluctuating price pressures, inflation now seems more persistent. This change is making institutional investors rethink their portfolio strategies. The derivatives market has responded with new products like forward rate agreements and long-term futures. Central banks, particularly in Asia and the Middle East, have been active buyers of gold. Their increased purchases—over 1,100 tonnes in 2022—show strategic concern over Dollar exposure. This large-scale accumulation by countries like China and India indicates a significant reassessment of faith in the stability of fiat currency. The established relationships remain strong. Gold’s price continues to rise when real yields drop and the Dollar weakens. This inverse relationship is a reliable guide for traders. Traders in the derivatives market should note the noticeable gap between future interest expectations and actual inflation. Recent pricing discrepancies in swaps and options suggest that some investors may not be adequately hedging against ongoing inflation risks. This opens up opportunities for more cautious strategies, especially using options related to metals and volatility connected to future Consumer Price Index (CPI) data. Emerging market central banks are taking the lead in proactive gold purchases, supporting bullion prices even when short-term optimism or dollar strength might temporarily soften them. Historically, when these institutions adjust their purchasing patterns, it’s usually for long-term security rather than short-term profits. Keeping an eye on trade policy and credit metrics in major economies is essential. A pattern is forming: periods of eased geopolitical tension lead to brief declines, but underlying fiscal and inflation concerns maintain demand that doesn’t just vanish. For those looking to manage short-term investments or balance long-term risks, clarity in strategy is crucial—avoid overreacting to temporary calm. Continue to monitor currency volatility. In times of changing central bank policies, these measures can provide early insights into shifts in interest rates. Stay flexible in your strategic approach, but consider protective options when valuations appear imbalanced. Create your live VT Markets account and start trading now.EUR/USD approaches 1.1400 as Trump delays tariff deadlines during Asian trading hours

EUR/USD is rising, trading at about 1.1390 during Monday’s Asian session. This boost comes after US President Donald Trump extended the deadline for a 50% tariff on EU imports to July 9. Ursula von der Leyen, President of the European Commission, indicated the EU’s willingness to negotiate, although a final deal still needs time. Meanwhile, US markets are closed for Memorial Day.

On Friday, Trump warned about potential 50% tariffs on EU imports, criticizing Brussels’ trade proposal and suggesting these tariffs could start on June 1, 2025, due to stalled negotiations. The currency pair is also benefiting from a weaker US Dollar, as ongoing economic uncertainties continue. Trump’s proposed bill could increase the fiscal deficit and impact bond yields and borrowing costs.

US Economic Outlook Concerns

The economic outlook for the US looks shaky. Moody’s has downgraded the US credit rating from Aaa to Aa1, predicting that federal debt could rise to 134% of GDP by 2035, up from 98% in 2023, with a budget deficit approaching 9% of GDP. Federal Reserve officials, worried about Trump’s tariff threats, seem reluctant to change interest rates. Chicago Fed President Austan Goolsbee has suggested delaying any changes, while Kansas City Fed President Jeffrey Schmid advocates a data-driven approach. With EUR/USD around 1.1390, we see clear momentum influenced by recent political moves on both sides of the Atlantic. Trump’s decision to push the tariff deadline to early July brought short-term optimism to the currency pair. This pause suggests that negotiations are still alive, even if not resolved. Von der Leyen’s remarks show that Brussels is ready for talks, but the need for more time indicates that clear outcomes are still lacking. With the US on a market holiday, liquidity is lower, which could lead to more extreme price movements in the coming days. We should be cautious of sharp reversals in this low-volume environment, especially in early European trading. On Friday, Trump’s tariff threats led to a brief period of risk aversion, but markets have since adjusted. Traders are now more focused on the general weakness of the US Dollar, which is supporting the euro. If Trump’s proposed trade measures are enacted, they could widen the budgetary gaps in the US further, something that bond markets are closely monitoring. Rising deficits typically drive up yields, as the government must borrow more when rates are stable.Federal Reserve and Market Sentiment

Adding to the tension, Moody’s has downgraded the US credit rating, highlighting long-term debt concerns. Though the downgrade from Aaa to Aa1 may not immediately affect capital flows, it confirms that debt is rising faster than revenue. They predict debt-to-GDP will exceed 130% in a decade, and with the deficit already at 9% of GDP, the US may need to reduce spending or increase revenue—options that seem politically unlikely before the election. Goolsbee from the Chicago Fed appears cautious about adjusting monetary policy too quickly, pointing to mixed signals in domestic data and trade tensions. Schmid echoes this caution, insisting that any policy actions must rely on incoming data. This suggests that policy will remain stable in the near term rather than become more accommodative, especially as inflation remains persistent. Traders may benefit more from focusing on high-frequency data like CPI, job reports, and real yields over the next two weeks, rather than relying too much on central bank guidance. The price action of EUR/USD will depend on whether interest rate expectations change based on new data. From a position management perspective, we prefer strategies that reflect sideways trading in the short term, with a potential upside if risk appetite improves and US yields stay steady. Keep an eye on German and French economic data this week. If those reports fall short, they could halt the euro’s rise, but likely won’t trigger a major reversal. We need to stay alert to any headlines from Washington or Brussels—unexpected policy changes could affect our strategies. Avoid passive exposure near critical technical levels unless confirmed by significant volume or strong directional movements. Keep tight stops in place—it’s too risky to rely on outdated correlations. Create your live VT Markets account and start trading now.The People’s Bank of China sets the USD/CNY central rate at 7.1833 for trading.

On Monday, the People’s Bank of China (PBOC) set the USD/CNY central rate at 7.1833, down from the previous rate of 7.1919. This change reflects the bank’s strategy for managing the value of the Chinese currency against the US Dollar.

The PBOC is a state-owned entity, not an independent body. Its main goals include keeping prices stable, ensuring steady exchange rates, promoting economic growth, and executing financial reforms.

Monetary Policy Tools

The PBOC uses a variety of monetary policy tools that differ from those in Western economies. These include the seven-day Reverse Repo Rate, the Medium-term Lending Facility, foreign exchange interventions, and the Reserve Requirement Ratio. The Loan Prime Rate is China’s benchmark interest rate. China has embraced private banks, with 19 currently operating within its financial system. Notable examples include WeBank and MYbank, which are backed by major tech companies like Tencent and Ant Group, thanks to regulations introduced in 2014. The recent adjustment of the USD/CNY midpoint by the PBOC to 7.1833, down from 7.1919, may seem small, but it has significant meaning. This daily rate shows an intention to relieve some depreciation pressure on the renminbi while avoiding undesired volatility. The focus here is on the trends and frequency of these changes, as they can provide clues about future policy directions. The PBOC does not act alone; it operates within the context of national goals. Its objectives—price stability, control of foreign exchange rates, and boosting domestic demand—align with long-term government plans. Because of this connection, its actions often reflect a mix of economic signals and strategic priorities of the government, something that can be overlooked in the West, where central banks usually have more independence.Unique Financial Ecosystem

What differentiates the PBOC is its wide range of tools. Instead of relying mainly on a headline interest rate to steer the economy, officials use various methods. The seven-day reverse repo rate is closely monitored and acts as a short-term gauge of liquidity. The Medium-term Lending Facility provides insights into medium-term policy outlook, with single operations here capable of quickly altering rate expectations. The Reserve Requirement Ratio, which dictates how much cash banks must hold, is crucial for long-term adjustments. Each tool serves a distinct purpose and must be considered separately. The rise of private banks, especially those backed by Tencent and Ant Group, changes the landscape. China’s banking model was mostly state-run, but since the 2014 reforms, there’s been more room for technology-driven lenders. Now, 19 licensed private banks offer digital lending and credit to small businesses and consumers. This diversification enhances financial access but also indicates Beijing’s cautious approach to allowing market competition under governmental oversight. As we look ahead, it’s essential to monitor not just the official rates but also the underlying movements in policy that reveal when the PBOC feels pressure and how it reacts. While the yuan is expected to remain stable, forward and swap pricing can indicate shifts in Beijing’s comfort. When managing currency pairs involving the yuan or similar currencies, observing the pace of reverse repo activity and any changes in the Reserve Requirement Ratio can provide valuable insights. Even subtle adjustments can precede significant shifts in economic strategy. Careful analysis of these details can reveal opportunities for better pricing. Create your live VT Markets account and start trading now.GBP/USD rises above 1.3550, reaching its highest level since February 2022 in Asian trading

The GBP/USD pair has risen above the mid-1.3500s, reaching its highest point since February 2022. The British Pound is benefiting from strong UK Retail Sales figures and higher inflation data, which may affect the Bank of England’s decisions on monetary policy.

On the other hand, the US Dollar is struggling due to worries about the budget deficit and expectations of further interest rate cuts by the Federal Reserve in 2025. These issues are pushing the USD down, helping the GBP/USD pair to climb.

Upcoming US Macroeconomic Data

Upcoming US data like Durable Goods Orders, Prelim GDP, and the PCE Price Index could influence the Federal Reserve’s interest rate decisions, affecting the USD and the GBP/USD pair. The Pound Sterling, being the oldest currency, accounts for 12% of foreign exchange transactions. The Bank of England’s decisions, especially on interest rates, have a major impact on the Pound’s value. Economic indicators such as GDP and trade balance also influence how strong the Pound Sterling is. This article shares information without encouraging specific investment actions, highlighting the need for individual research before making investment choices. It emphasizes that investing carries risks and that individuals are responsible for their decisions. The GBP/USD has risen past the mid-1.3500s, marking a level not seen since early 2022. This isn’t a random change; stronger-than-expected inflation and solid retail sales in the UK have fueled sentiments that the Bank of England might keep rates high for a while or be cautious before any cuts. Traders are considering that inflation pressures may last longer than anticipated, particularly in services and energy. Retail data shows that consumers are still spending despite rising borrowing costs. This indicates steady demand in the economy, which might delay any decisions on rate cuts. This scenario suggests the Pound could see further gains in the short term. However, it’s important to recognize that one strong data point can quickly alter expectations. In the US, the Dollar is under consistent downward pressure. Concerns about fiscal responsibility, especially the growing budget deficit, are contributing to this decline. Traders are worried about the long-term implications for yields and the overall attractiveness of US assets. Meanwhile, it’s becoming clearer that the Federal Reserve may begin easing in 2025, which adds to the Dollar’s weakness.All Attention Now Turns To The Next US Data

All eyes are now on upcoming US data. The core PCE price index and revised GDP figures will be crucial in seeing if the market is getting ahead of the Fed. If inflation continues to ease while growth slows, the idea of rate cuts might become even more established in market positioning. This could boost interest in higher-yielding or more stable currencies, supporting the Pound in the near term. In our view, any weakness in the Dollar likely correlates with this data and expectations. Durable goods orders may be volatile, but downward surprises would reinforce existing policy speculations. As always, short-term positioning should be flexible, and any leverage should be carefully managed given the increased volatility around data releases. We should also note that the strength of the Pound isn’t only due to economic surprises. Some support comes from positioning; after a long period of underperformance, a structural adjustment seems to be occurring. This can last longer than usual market fundamentals suggest. Looking ahead, even small changes in trade balance or GDP expectations in the UK could impact currency movements more significantly than usual. Since rates are seen as near their peak, any signs of persistent inflation or stronger demand could heavily influence expectations of when easing might start. In the coming weeks, closely monitoring macroeconomic indicators and central bank statements will be crucial. The positioning bias is uneven; while shorting the Dollar is increasingly common, it carries risks, especially if hawkish sentiments arise or data unexpectedly improves. Rapid policy adjustments can happen, and recent history shows how quickly consensus can shift if numbers don’t align with expectations. It will be critical to manage exposure tightly and reassess risk levels at key technical points. We anticipate rising volatility around major data releases. Create your live VT Markets account and start trading now.Japan’s chief trade negotiator seeks to advance tariff talks with the US before an upcoming meeting.

Japan’s top trade negotiator, Ryosei Akazawa, is working to push forward tariff discussions with the United States. The goal is to reach an agreement by the Group of Seven summit in June. There are already some positive reports about the negotiations, especially regarding cooperation in shipbuilding.

The USD/JPY pair is currently up by 0.14%, trading at 142.75. The value of the Japanese Yen (JPY) is affected by the country’s economic performance, the policies of the Bank of Japan, differences in bond yields, and overall global risk sentiment.