In January, the United States experienced a drop in weekly crude oil stock to 3.04 million.

The latest data on U.S. crude oil stocks shows a drop. As of January 16, crude oil inventories have decreased to 3.04 million barrels, down from 5.27 million barrels. This change indicates shifts in supply and demand.

New Zealand dollar climbs towards 0.5850 against the US dollar amid risk-on sentiment

The NZD/USD climbed close to 0.5850 during the Asian trading hours. This followed President Trump easing concerns about European tariffs. He also announced a framework for a deal regarding Greenland, which could bolster the New Zealand Dollar against the US Dollar.

Upcoming economic data will play a crucial role for the NZD. New Zealand is set to release its Q4 Consumer Price Index (CPI) inflation report on Friday. Analysts predict a 0.5% increase in quarterly CPI and a 3.0% rise from last year. Lower inflation could affect the Reserve Bank of New Zealand’s (RBNZ) decisions on interest rates.

Factors Influencing The NZD

The value of the New Zealand Dollar is impacted by various factors, such as the country’s economic performance and central bank policies. The economic health of China is important for the NZD because of New Zealand’s trading ties with China, particularly in dairy products. The RBNZ aims for inflation to stay between 1% and 3%, which influences its interest rate decisions and, in turn, the value of the NZD. Changes in economic data showing growth or decline can change the NZD’s value. Additionally, market sentiment can greatly influence the NZD. Periods of risk-taking can boost the currency, while uncertainty can lead to a decline. Reflecting on last year, in January 2025, the NZD/USD was hovering around 0.5850, driven by hopes of easing trade tensions from the Trump administration. That type of geopolitical risk has lessened, allowing us to focus more on core economic factors. Currently, the pair is trading around 0.6120, showing a new landscape for traders. A year ago, we were anticipating Q4 2024 inflation data to assess whether the RBNZ would raise interest rates. Now, the latest report for Q4 2025 indicates that annual inflation has cooled to 2.8%, comfortably within the RBNZ’s target range. This suggests the RBNZ is likely to maintain its cash rate at 5.5%, limiting upside potential from interest rate differentials and making long-dated call options less appealing.Current Market Sentiment

It’s important to let fundamental factors, like the health of the Chinese economy and dairy prices, shape our strategy. Recent data shows China’s Caixin Manufacturing PMI fell to 49.8, signaling a slight contraction. Additionally, the Global Dairy Trade index has decreased in the last two auctions. These signs indicate traders should remain cautious and might consider purchasing puts to guard against a potential drop in the NZD/USD. While early 2025’s favorable market mood provided temporary support for the Kiwi, current sentiment is more cautious due to fears of a global growth slowdown. The US economy continues to show strength, with weekly jobless claims consistently below 220,000, supporting the US Dollar. This situation suggests that selling rallies in the NZD/USD could be a wise strategy for the weeks ahead. Create your live VT Markets account and start trading now.Japan’s merchandise trade balance dropped from ¥62.9 billion to ¥-0.21 billion

Japan’s adjusted trade balance fell from ¥62.9 billion to ¥-0.21 billion in December. This change highlights shifts in imports and exports over the month.

In the currency market, the Japanese Yen declined as USD/JPY approached 159.00. At the same time, NZD/USD climbed above 0.5850 as concerns about risk eased.

Commodity Market Updates

In commodities, WTI crude oil stabilized above $60.50 due to easing geopolitical worries offsetting oversupply issues. Gold also remained above $4,800 thanks to reduced geopolitical tensions. Cryptocurrencies showed signs of recovery, with Canton, MYX Finance, and Pump.fun all reporting gains in the last 24 hours. Axie Infinity (AXS) rose by 8%, trading over $2.56 after a week of positive momentum. For traders looking at 2026, reviews highlight the best brokers for different needs, including forex trading, CFDs, and Islamic accounts. Guides focus on brokers that offer low spreads, high leverage, and platforms like MT4, particularly for regions such as MENA, LATAM, and Indonesia. Japan’s unexpected trade deficit is a key indicator, especially as USD/JPY nears 159. This isn’t a minor detail; it weakens the case for the yen. We should expect ongoing yen weakness in the coming weeks.Trade Strategy Insights

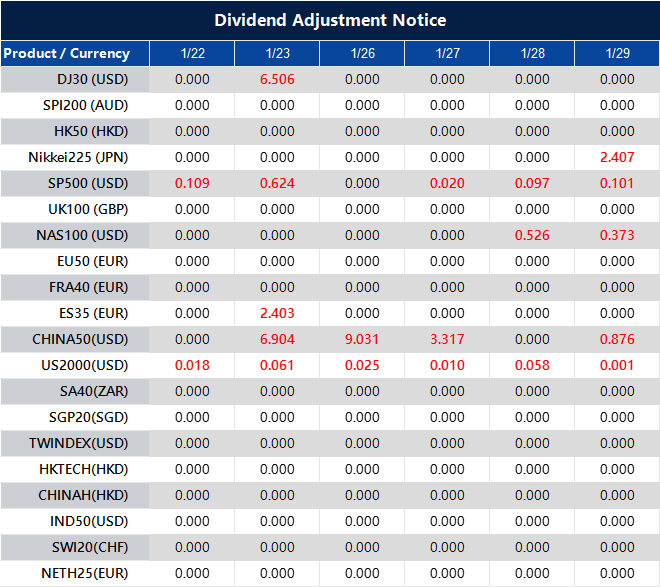

We remember similar trends from 2022, when rising energy import costs and a weak yen led to a record annual trade deficit of nearly ¥20 trillion. With WTI crude staying above $60, we see the same pressures now affecting Japan’s import costs. The main issue is the significant difference in monetary policies. The Bank of Japan’s policy rate is close to zero, while the US Federal Reserve’s rate is above 3%. This interest rate gap makes selling the yen for dollars a profitable “carry trade.” This trend is unlikely to reverse soon, giving a consistent boost to USD/JPY. As a result, our clear strategy is to take long positions in currency pairs like USD/JPY and EUR/JPY. However, we must be cautious as the yen weakens past levels that previously prompted government intervention from 2022 to 2024. The risk of a sudden intervention by the Ministry of Finance is much higher now. To manage this risk, buying call options on USD/JPY could be a smart move. This strategy allows us to benefit from further yen weakness while limiting losses to the premium paid if the government intervenes. It gives us the potential for profit while controlling our risk amid volatility. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 22 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The People’s Bank of China sets the USD/CNY rate at 7.0019, differing from 7.0014

The People’s Bank of China (PBOC) has set the USD/CNY central rate at 7.0019 for the upcoming trading session. This is slightly higher than yesterday’s rate of 7.0014 and above the Reuters estimate of 6.9697.

The PBOC’s main goals are to keep prices stable, manage exchange rates, support economic growth, and push for financial reforms. To achieve these goals, the central bank uses several tools, including the seven-day Reverse Repo Rate, the Medium-term Lending Facility, the Reserve Requirement Ratio, and the Loan Prime Rate.

China’s Banking Sector

The state owns China’s central bank, with the Chinese Communist Party Committee Secretary influencing its management. Currently, there are 19 private banks in China, including digital banks like WeBank and MYbank. In 2014, China allowed private banks to join its primarily state-controlled financial sector. Although there are not many of them, these private banks play a small role in the financial system. The People’s Bank of China has set the yuan’s reference rate lower than expected, crossing the important 7.00 mark against the dollar. This move shows a willingness to allow the currency to depreciate, likely to support the economy. It suggests we should adjust our short-term currency strategies. This decision aligns with recent economic data. Full-year GDP growth for 2025 is projected at 4.8%, which is below the government’s target. Additionally, December’s export data showed a slight year-over-year decline, and the latest Caixin Manufacturing PMI is just above 50, indicating weak expansion. These figures explain why authorities might prefer a weaker yuan to boost the competitiveness of Chinese goods abroad.Central Bank Policy Direction

Remember the central bank’s actions in late 2025 when it lowered the Reserve Requirement Ratio for major banks to increase liquidity in the market. Today’s currency fixing seems to follow that accommodative policy. This trend suggests that further yuan weakness is possible and part of a broader support strategy for the economy. In the coming weeks, we should consider preparing for a higher USD/CNY rate. This could involve buying USD call options or CNH put options to benefit from a potential upward movement while managing our risk. The difference between the market estimates and today’s fix is a strong indication that we should be cautious about holding onto the yuan right now. Now that the 7.00 level has been crossed in the daily fix, we should watch for resistance around the 7.10 mark, a level tested back in 2024. Expect increased volatility in the pair as the market reacts to this policy signal. We will seek opportunities in instruments like vanilla options or forward contracts that could benefit from this potential trend. Create your live VT Markets account and start trading now.Australian Bureau of Statistics reports unemployment rate drops to 4.1%, exceeding expectations

Australia’s unemployment rate fell to 4.1% in December, down from 4.3% in November, and better than the expected 4.4%. There was an increase of 65.2K jobs, bouncing back from a loss of 28.7K jobs in November, surpassing the forecast of 30K.

The participation rate slightly increased to 66.7% from 66.6% in November. Full-time jobs rose by 54.8K following a drop of 65.3K, while part-time jobs added 10.4K in December, lower than the previous month’s increase of 36.6K.

Factors Behind Employment Growth

More jobs for those aged 15-24 played a key role in these changes. Male employment rose by 49,000, while female employment increased by 17,000. Total hours worked went up by 0.4%, matching the growth in jobs. After this employment news, the Australian Dollar strengthened, with the AUD/USD rising 0.40% to 0.6788. The AUD gained the most against the Japanese Yen. The Reserve Bank of Australia is set to meet on February 3 to discuss monetary policy for the year. Although employment data was mixed, it hints at some easing for the RBA, keeping in mind the ongoing inflation concerns. Australian employment statistics are closely monitored as they affect currency values and can influence central bank decisions.Economic Impact and Market Reaction

The December 2025 employment report has significantly changed the economic outlook. The unemployment rate dropped to 4.1%, and job growth surpassed expectations, contradicting earlier beliefs that the labor market was cooling. This unexpected strength indicates the Australian economy might be more robust as we approach 2026. This report puts pressure on the Reserve Bank of Australia ahead of its meeting on February 3rd. With inflation at 3.4% in November 2025, the strong employment figures complicate any consideration for rate cuts by the RBA. Currently, there’s a 45% chance of a rate hike at the upcoming meeting, a sharp increase from just 15% before the report. For traders, this indicates it’s time to prepare for a stronger Australian Dollar. We might look at buying AUD/USD call options with strike prices above the present resistance of 0.6830, aiming for a move towards 0.6870. This strategy offers a manageable risk while capitalizing on potential gains ahead of the RBA decision. The case for a stronger AUD is also backed by external factors. Iron ore prices, a vital Australian export, have climbed over 5% in the last month to more than $140 per tonne. This historical trend supports a stronger AUD, aided by recent data showing unexpected growth in China’s manufacturing sector in early January. The last crucial element will be the Q4 2025 inflation report, due on January 28. If this report also shows high inflation, it will likely prompt the RBA to act, reinforcing the argument for a more aggressive stance. We will closely monitor this release as key support for our positive outlook on the Aussie dollar. Create your live VT Markets account and start trading now.GBP/USD pair fluctuates above 1.3400 as traders await US economic data

The GBP/USD pair is currently trading in a tight range above 1.3400 with little movement. Traders are waiting for the US PCE Price Index and Q3 GDP data to guide their decisions.

Factors easing trade tensions benefit the USD, while mixed market signals call for careful trading. A key technical level is the 200-day Simple Moving Average around 1.3365-1.3360.

Impact of Trade Comments

Comments from the US President have boosted the prospects for the USD, while expectations regarding Federal Reserve policy influence GBP/USD trends. In December, the UK’s Consumer Price Index (CPI) rose to 3.4% year-on-year, reducing the likelihood of immediate interest rate cuts by the Bank of England (BoE). Nonetheless, the market still expects possible BoE rate cuts by 2026. These factors have led to restrained trading of GBP/USD, keeping the pair within a specific price range. A table outlines the USD’s strength against the Euro. A disclaimer in the article reminds readers to be cautious about making investment decisions based on this information. As we approach the end of January, the GBP/USD pair remains stuck around the 1.2700 mark. This sideways movement arises as traders assess conflicting signals from the UK and US economies. Key economic data expected in the coming weeks may trigger a breakout from this range.Technical Analysis and Strategy

The US Dollar is gaining support, building on late 2025 gains. The final Q3 2025 GDP growth was a solid 2.1%, and the December 2025 PCE Price Index showed inflation at 2.9%. While inflation is cooling, it is still persistent, creating uncertainty about the Federal Reserve’s future actions and keeping the dollar appealing for now. In contrast, the British Pound is having trouble finding direction, despite recent inflation data. The Office for National Statistics reported that December 2025’s CPI was 4.0%, higher than the 3.8% forecast and significantly up from previous months. Although this reduces the chances of a quick BoE rate cut, the market still anticipates at least a quarter-point cut by the end of 2026 due to a weak growth outlook. Given this uncertainty and range-bound behavior, traders dealing in derivatives should explore low-volatility strategies. Selling options straddles or strangles near the 1.2700 level could be a smart way to earn premiums while the pair consolidates. These positions will benefit from time decay unless the exchange rate experiences a substantial, unexpected move. From a technical perspective, the pair remains above its 200-day Simple Moving Average, which is currently around the 1.2650 area and acts as an essential support level. A significant drop below this level would indicate a bearish turn, prompting traders to reconsider any range-bound strategies. Looking ahead, the upcoming first estimate for US Q4 2025 GDP and the BoE’s policy meeting in early February are crucial events. Traders should monitor these releases closely as they may provide the stimulus needed for the next directional move in GBP/USD. Create your live VT Markets account and start trading now.Part-time employment in Australia fell to 10.4K in December, down from 35.2K previously

The Decline of the Japanese Yen

The Japanese Yen is losing value due to concerns about government spending and positive market sentiment ahead of the Bank of Japan’s meeting. The GBP/JPY has nearly reached 213.00, while the EUR/JPY is strengthening around 185.50, as people anticipate the Bank of Japan’s upcoming rate decision.

FXStreet offers a wealth of information on various markets, including trends in currency pairs like EUR/USD and GBP/USD. They provide detailed guides for choosing brokers in 2026, focusing on important factors like spreads, regulations, and platform features. This content highlights the need to do thorough research before making financial choices.

Recent jobs data from Australia indicates a notable drop in part-time employment, which is concerning. This decline is reminiscent of the unexpected hiring slowdown we experienced in late 2025, which led to a significant fall in the Australian dollar. We should consider buying put options on the AUD/USD, expecting further declines as the market responds to this news.

Yen Futures Strategy

As the Bank of Japan’s policy decision nears, the Yen continues to weaken amid a broader positive market sentiment. This trend of Yen weakness before BOJ meetings was consistent in 2025, as the central bank hesitated to tighten its policy significantly. Therefore, selling Yen futures or buying call options on pairs like EUR/JPY could be a smart move to take advantage of the ongoing momentum.

Gold is remaining above the historically high price of $4,800, but its appeal as a safe investment is decreasing. After persistent inflation in 2025 pushed prices to these levels, any signs of economic stability could lead to a sharp correction. Selling out-of-the-money call options could allow us to collect premiums while betting that gold’s rally has peaked for now.

The US Dollar is strengthening ahead of important economic data, and the British Pound is also holding steady after UK inflation came in higher than expected. This creates a tense situation where the next major US data release could lead to a significant price movement. We can prepare for this volatility by setting up straddle options on GBP/USD, which would profit from a large price change in either direction.

Create your live VT Markets account and start trading now.

In December, Australia’s full-time employment increased by 54.8K, recovering from a previous decline of -56.5K.

In December, Australia saw an increase of 54.8K in full-time jobs, bouncing back from a previous drop of -56.5K.

This rise in full-time employment stands out against global currency changes, such as the USD/INR holding its ground, the Japanese Yen weakening, and the GBP/JPY rising. These shifts reflect broader financial trends, particularly UK inflation affecting the GBP/USD and the cryptocurrency market’s performance.

Gold Drop and Cryptocurrency Recovery

At the same time, gold prices have dropped due to reduced demand for safe assets. However, some altcoins are showing signs of recovery in the cryptocurrency market, approaching important resistance levels as selling pressures ease. The market on the previous Wednesday showed a general increase in assets, with stocks, bonds, gold, cryptocurrencies, and crude oil all rising. Axie Infinity surged by 8%, driven by higher whale buying activity. Investors should conduct thorough research and consult professionals due to the inherent risks. The information provided is not intended as specific recommendations, and individual analysis is crucial. FXStreet and its authors are not responsible for any errors or losses related to this information.Australia’s Job Market and Its Impact on the RBA

The significant shift in Australia’s full-time employment in December 2025, from a loss of over 56,000 jobs to a gain of nearly 55,000, points to a surprisingly strong labor market. This development is likely a game-changer for the Reserve Bank of Australia (RBA), raising the chances of a tougher monetary policy in the coming months. It contradicts earlier market expectations of a slowing economy. This strong jobs report follows the Q4 2025 inflation rate of 3.1%, which has brought underlying price pressures back into focus for the RBA. With employment and inflation both increasing, the current pricing for rate cuts in 2026 seems off. We suggest that traders think about selling Australian bond futures or buying options that benefit from rising short-term interest rates. The policy differences between central banks are becoming clearer, especially compared to the Bank of Japan, which is sticking to its dovish approach. This situation makes long AUD/JPY trades particularly appealing, and we recommend looking at call options to take advantage of the expected gains. The yen’s weakness and the strengthening Australian dollar create a solid opportunity. Historically, we’ve seen similar patterns in 2022, where strong employment data led to aggressive actions from central banks, causing notable currency fluctuations. With iron ore prices stabilizing above $130 per tonne in early January 2026, the case for Australian dollar strength is looking stronger. As a result, traders should also brace for more volatility in AUD/USD, making strategies like options straddles worthwhile. Create your live VT Markets account and start trading now.In December, Australia’s actual unemployment rate was 4.1%, which was lower than expected.

In December, Australia reported an unemployment rate of 4.1%, which is lower than the expected 4.4%. This shows a positive trend in the job market compared to earlier forecasts.

The drop in unemployment signals an improvement in Australia’s labor market. The numbers reveal a stronger job market than many had predicted for the month.