Rising crude oil prices linked to increased US-Iran tensions and military buildup in the region

Crude oil prices are climbing due to renewed tensions between the United States and Iran. US President Trump has warned Iran as military forces gather in the area. London Brent oil futures rose by $1.34, reaching $68.67 per barrel, while NY WTI increased by $1.93, settling at $65.14 per barrel.

Market volatility is expected to increase because of policy decisions from the BoE and ECB.

The ECB and BoE Interest Rates

On February 5, markets were quiet as investors waited for news from the Bank of England (BoE) and the European Central Bank (ECB). Key U.S. economic reports included weekly Initial Jobless Claims and December’s JOLTS Job Openings report.

Despite mixed economic data, the U.S. Dollar remained strong. Private sector employment rose by 22,000, less than the expected 48,000. The ISM Services PMI held steady at 53.8, showing solid activity in the service sector. The USD Index is around 97.70. Nonfarm Payrolls data will be released on February 11, while CPI data has been moved to February 13.

The ECB is expected to keep interest rates steady, focusing on their inflation outlook after a 1.7% annual rise in January HICP. EUR/USD is around 1.1800. The BoE is likely to maintain its bank rate at 3.75%. GBP/USD decreased by 0.2% to 1.3625. AUD/USD struggles to stay above 0.7000, and gold is trading below $4,950. Silver, despite earlier gains, is now below $81, down over 8%.

FAQs explain that central banks play a crucial role in maintaining stable prices by adjusting interest rates. They aim for inflation to stay near 2%, using tightening or easing of monetary policy as necessary. These banks are often independent from political influence, with their decisions made by a board comprising both ‘doves’ and ‘hawks.’

Historical Perspective and Predictions

Reflecting on February 2025, we were closely monitoring major central bank decisions from the BoE and ECB. The U.S. Dollar Index was stable around 97.70, with markets waiting for news. This waiting period before major announcements often creates trading opportunities in options markets.

Currently, the U.S. Dollar’s strength is fueled by a consistently strong job market, unlike last year’s mixed data. In January 2025, the ADP employment report showed a significant shortfall, but now we see a much stronger picture. For example, the January 2026 jobs report indicated the U.S. economy added 225,000 jobs, surpassing expectations of 180,000, keeping the Federal Reserve on a steady path.

For the Euro, there has been a notable change in the inflation narrative. In early 2025, the ECB was worried about a strong Euro as inflation dropped to 1.7%. Now, with the latest Eurozone core HICP inflation for January 2026 at 2.5%, the focus is shifting toward possible rate cuts later this year. This difference in policy from the U.S. suggests traders might want to consider strategies that benefit from a potentially weaker EUR/USD, currently at 1.07, well below the 1.18 seen a year ago.

The Bank of England is facing different challenges, making the Pound Sterling an intriguing case. While holding rates at 3.75% in February 2025, they now face stubbornly high domestic price pressures, with UK services inflation at 5.8%. This hawkish approach compared to the ECB suggests that long GBP/EUR positions may be favorable in the coming weeks.

Scheduling Changes and Market Impact

We should also remember last year’s scheduling changes, when Nonfarm Payrolls and CPI data releases were delayed. This serves as a reminder that logistical issues can create unexpected volatility in the markets. With the crucial U.S. inflation report for January 2026 coming next week, any surprises in the data will likely drive price movements.

The USD/JPY exchange rate remains influenced by interest rate differences, a theme that has strengthened since early 2025 when the pair approached 157.00. The significant gap between U.S. interest rates and those in Japan continues to support this pair. Traders should prepare for this trend to continue and consider using options for protection against unexpected policy shifts from the Bank of Japan.

Commodities like gold are facing challenges that weren’t as clear last year when prices hovered around $4,950. As central banks worldwide signal that high interest rates will persist to combat inflation, non-yielding assets become less appealing. This suggests investors should consider put options or short-selling futures to hedge against a potential drop in gold prices.

Create your live VT Markets account and start trading now.

Analyst Chris Turner highlights the euro’s resilience and expects important insights from President Lagarde.

The Euro has stayed stable despite market pressures, with focus shifting to the upcoming ECB press conference. President Lagarde’s comments about the Euro’s strength and potential inflation risks are crucial for EUR/USD movement.

Today, the EUR/USD will be tested during the ECB press conference at 14:45 CET. If Lagarde talks about monitoring exchange rates or rising inflation risks, it could affect the Euro, but major changes are not anticipated.

Market Participants’ Outlook

If the Euro drops below 1.1770, it might move into the 1.1700-1.1720 range, but a significant decline is unlikely in the short term. This reflects ongoing assessments by market participants about future currency trends and economic data. The Euro has shown resilience, but the key challenge lies in the upcoming ECB press conference. Currently, EUR/USD is trading around 1.1250, and any remarks from the ECB President regarding the currency’s strength will be important for the market. Inflation in January 2026 has eased to 2.3%, making the bank’s stance on exchange rates especially important. Looking back, the Euro’s steady rise in the second half of 2025 made ECB policy decisions more complex. This history shows the bank is aware that a strong currency can tighten financial conditions and reduce inflation. We are closely watching for any mention of the ECB “monitoring exchange rates,” as this has previously indicated concern.Traders’ Strategic Approaches

Due to the upcoming event, implied volatility on one-month EUR/USD options has risen to 8.5%, up from a low of 7% last month. This suggests traders expect a more significant price movement than usual, making strategies like buying straddles or strangles appealing. These positions would benefit from a notable price shift in either direction after the press conference. The main downside risk would be any comments about increasing threats to inflation or growth, especially following a 0.1% contraction in Q4 2025 GDP. Such statements have historically weakened the Euro and could push EUR/USD below the 1.1200 support level. Traders who expect this may consider purchasing put options with a 1.1150 strike to control their risk. On the other hand, if the ECB shows concern over persistent wage growth, this could be seen as a hawkish signal. This would likely support the Euro and challenge recent highs around 1.1320. Traders betting on this possibility through call options would see their values rise. Create your live VT Markets account and start trading now.Concerns about Japan’s financial situation lead to Yen’s decline against a strengthening Dollar

The Japanese Yen is steadily losing value against the US Dollar. Concerns about Japan’s budget plans under Prime Minister Sanae Takaichi are driving this decline. Political uncertainty ahead of the national election and lower consumer inflation in Tokyo are also factors, pushing USD/JPY past 157.00, marking a two-week high.

Traders are wary of potential interventions from Japan or the US to stop the Yen’s drop. The Bank of Japan (BoJ) is gradually tightening policies, while the US Federal Reserve may cut interest rates. Reports on the US job market and the chance of the Fed becoming less aggressive could limit gains for the Dollar and help stabilize the Yen.

Prime Minister Takaichi’s proposals, such as suspending the 8% food consumption tax and comments on currency weakness, affect perceptions of Japan’s finances and put more pressure on the Yen. Tokyo’s headline inflation isn’t showing much demand-driven price increase, lessening the need for further BoJ rate hikes. Still, speculation about a BoJ rate increase in 2026 continues, especially when contrasted with potential US rate cuts.

The technical outlook for USD/JPY suggests more gains if key resistance levels, like the Fibonacci retracement, are surpassed. Last week, the Yen performed strongest against the British Pound, even though it struggled elsewhere.

With USD/JPY now trading above 157.00, it seems likely to continue rising in the short term. The Yen faces challenges from Prime Minister Takaichi’s spending plans and the uncertainty of the snap election on February 8. A win for the ruling LDP party is expected, which could lead to ongoing pressure on the Yen.

For options traders, this scenario indicates an opportunity to buy call options on USD/JPY to benefit from possible further gains, aiming for the 157.64 resistance level. The soft inflation data from Tokyo has pushed back the timeline for a BoJ rate hike, giving this strategy more potential. Looking back at interventions from late 2022, they happened at levels much lower than now, which may encourage traders.

However, there is a significant risk of sudden intervention by Japanese authorities, making it risky to hold long positions outright. To mitigate this, purchasing out-of-the-money put options could act as insurance against a sudden downturn. Current market trends show a 60% chance of a Federal Reserve rate cut by June 2026, which might limit Dollar strength and make the hedge necessary.

The differences between the central banks are significant. The BoJ is indicating a gradual approach toward tightening its policies in the first half of this year. While last week’s inflation data was weak, the service sector survey indicated growth, keeping future rate hikes on the table for the March meeting. This is in stark contrast to the Fed, where the market anticipates two more rate cuts in 2026.

Upcoming US labor reports, including today’s JOLTS Job Openings data, will be vital. A strong report could challenge the idea of a slowing US economy, supporting the Dollar and possibly pushing USD/JPY higher. Conversely, a weak report would reinforce the expectations of Fed cuts and could halt the rally.

UBS economist notes uncertainty for the Bank of England as UK inflation is likely to decline

UBS economist Paul Donovan talks about the uncertainty around the upcoming meeting of the Bank of England. This unpredictability stands in contrast to the more predictable European Central Bank.

Donovan notes that issues in data collection led to mistakes in December’s inflation figures. Still, the underlying inflation rate in the UK is likely to decline over time.

This drop in inflation might lead to interest rate cuts in 2026. However, UBS does not expect the Bank of England to lower rates right away.

Today’s Bank of England meeting highlights this uncertainty as they kept rates steady, even with the trend of falling inflation. The latest Consumer Price Index (CPI) reading for January was 2.8%, continuing the downward shift from the peaks we saw back in 2025. This creates a gap between decreasing inflation and a cautious central bank, leading to opportunities for derivative trading.

This indecision is increasing market volatility, which is essential for options traders in the upcoming weeks. Implied volatility for three-month GBP options has risen to 8.5%, showing that the market is anxious about when the first rate cut will happen. This situation suggests that buying options could be a smart move to take advantage of potential price changes around future data releases.

We are closely monitoring interest rate futures, as the market now fully expects a 25 basis point cut in the August meeting. However, strong wage growth, recently reported at 5.5%, is keeping the Bank on hold for now. This makes short-term SONIA futures very sensitive to upcoming job and inflation reports.

For the moment, the relatively high interest rate is supporting the pound sterling, keeping it strong against currencies where rate cuts are expected sooner. We should be on the lookout for this support to weaken as we approach a UK rate cut, shifting from the steady hold we saw during much of 2025. Any unexpectedly weak economic data could lead to a swift repricing against the pound.

Deutsche Bank analysts note a rise in the ISM services index and inflation indicators

The ISM services index rose to 53.8, reaching its highest level since late 2024. The prices paid component also climbed to 66.6, hinting at possible inflationary pressure in the US.

The ADP private payrolls report came in weaker than expected, showing only 22,000 jobs added instead of the 45,000 anticipated. Despite this, Treasury yields increased slightly, with 10-year yields reaching 4.28%.

Dollar Index Movement

The Dollar Index moved up to the 97.80 range, indicating a positive US economic outlook. Treasury yields varied: the 2-year yield fell by 1.6 basis points, while the 10-year and 30-year yields rose by 1.0 and 2.3 basis points, respectively. Looking back to early 2025, the market faced mixed signals. While the ISM services index was high, the ADP payrolls report surprised many with its weakness. This scenario created a volatile environment for interest rates. The high prices paid component from January 2025 served as a clear warning sign, as core inflation stayed above 4% for most of last year. Now, we’re seeing some relief, with data from late 2025 showing inflation pressures easing. For instance, the latest Core PCE reading for December 2025 came in at 3.4%, down from its mid-year highs.Market Shifts and Strategies

Back in early 2025, the Dollar Index hit 97.80 and peaked above 101 later that year as the Federal Reserve kept rates steady. However, the situation has changed. The index is now around 95.50, as the market anticipates policy easing. CME FedWatch futures show over a 70% chance of a rate cut by the June 2026 FOMC meeting. This scenario suggests preparing for a weaker dollar and lower long-term interest rates in the coming weeks. Options strategies, like buying puts on the Dollar Index or call options on Treasury bond futures, could be effective. Implied volatility in interest rate markets has increased, so traders should be cautious about the costs of these positions. Create your live VT Markets account and start trading now.Victory Capital Holdings reports $374.12 million in revenue for the last quarter, marking a 61% year-on-year increase; EPS rises to $1.78 from $1.45.

Victory Capital Holdings reported a revenue of **$374.12 million** for **Q4 2025**, which is a **61% increase** from last year. Their **earnings per share (EPS)** rose to **$1.78**, up from **$1.45** in the same quarter last year.

The revenue exceeded the **Zacks Consensus Estimate** of **$371.92 million** by **0.59%**, and the EPS surpassed expectations by **7.23%**, which was projected at **$1.66**. Analysts pay close attention to revenue and earnings changes as indicators of a company’s financial health.

Victory Capital’s total assets under management reached **$313.78 billion**, matching the **$313.77 billion** average estimate from three analysts. Key categories, including **Fixed Income**, **Money Market/Short-term**, **Alternative Investments**, and various **U.S. Equity sectors**, all met analyst expectations.

The total net client cash flows were **-$2.11 billion**, slightly more than the **-$2.08 billion** estimated by two analysts. Revenue from investment management fees hit **$301.35 million**, beating the analyst estimate of **$291.33 million** and showing a **63.9% increase** from last year. Fund administration and distribution fees totaled **$72.77 million**, reflecting a **49.9% year-over-year growth**, though this fell short of the **$80.58 million** analyst estimate.

Today is **February 5, 2026**, and we’re examining Victory Capital’s latest earnings, which present a mixed picture for traders. The company reported a significant EPS surprise of **over 7%**, a positive sign. However, this good news is overshadowed by a small miss in net client cash flows, which came in at **-$2.11 billion**.

This report follows a period of market instability in late **2025**, when uncertainty about interest rates pushed the **VIX**, a key measure of market volatility, to an average of **21**. Many investors moved to cash during that time, providing context for the outflows across the asset management sector. This trend suggests that the outflows may be more about the overall market environment rather than specific issues with the company.

The initial price reaction to the earnings beat may create opportunities for bearish derivative strategies. As the market’s initial enthusiasm may fade, the focus could turn to the ongoing issue of client outflows, a challenge for many active managers. Traders might consider buying **put options** for the **March 2026** expiration to take advantage of a potential downturn after this initial excitement.

Currently, the implied volatility for **VCTR options** is likely high, making premium-selling strategies, such as a **covered call**, attractive for stockholders. Historically, after the **Q2 2025** earnings report, the stock gave back its initial gains within three weeks. A similar pattern may occur now, rewarding those betting against sustained momentum.

We are also closely monitoring the revenue mix, as strong growth in high-margin investment management fees contrasts with the miss in administration and distribution fees. This difference indicates strength in core products but potential weaknesses elsewhere, adding to the uncertainty. This internal conflict supports strategies like **straddles or strangles**, which profit from significant price movements in either direction over the coming weeks.

USD/CAD pair strengthens near 1.3690 while remaining bearish below the 100-day EMA

USD/CAD rose to about 1.3690 in early European trading on Thursday. The pair is still under the 100-day EMA on the daily chart, indicating a bearish outlook. Immediate resistance is at 1.3750, while initial support is at 1.3490. Kevin Warsh is expected to become US Federal Reserve Chair in 2026, which boosts the USD. The market believes the Fed will keep interest rates steady in March, with total cuts ranging from 50 to 75 basis points by the end of the year.

Geopolitical tensions could push crude oil prices higher, which may benefit the Canadian Dollar (CAD) since Canada is a major oil exporter. The daily chart shows that USD/CAD continues to face bearish pressure as the 100 EMA moves downward. The RSI is at 46, showing signs of stability. If the price breaks above 1.3750, targets are set at 1.3813 and 1.4012, while further declines could reach as low as 1.3490.

The CAD is influenced by several factors including Bank of Canada (BoC) interest rates, oil prices, economic conditions, inflation, and trade balance. Generally, higher oil prices and strong economic indicators are good for the CAD. When inflation rises, it may lead to higher interest rates, attracting foreign investment. Economic strength also encourages investments and interest rate increases, boosting the CAD.

Currently, USD/CAD is taking on a bearish trend while being below the 100-day moving average around 1.3690. This situation suggests downward pressure, with strong resistance at 1.3750 and initial support at 1.3490. This indicates potential weakness in the pair in the short term.

Meanwhile, the US dollar is getting solid support from recent data. The Consumer Price Index (CPI) for January 2026 revealed inflation rose to 3.2%, lowering the chances of a Federal Reserve rate cut in March to below 10%, according to the CME FedWatch Tool. Speculation about a hawkish Fed chair replacing Jerome Powell in May also strengthens the dollar, limiting losses for USD/CAD.

On the other hand, the Canadian dollar is benefitting from rising crude oil prices, a major Canadian export. Geopolitical issues have pushed WTI crude prices above $85 a barrel, giving strong support to the loonie. The Bank of Canada is maintaining interest rates at 4.5%, as Canadian inflation remains higher than desired.

We should also consider the market volatility of 2025, where sentiment on interest rates changed quickly with single data points. Last year, the pair experienced sharp reversals when employment data surprised analysts on both sides of the border. This history warns us to be cautious about the current technical trend and its stability if unexpected economic news arises.

Given these mixed signals, a straightforward directional trade carries high risk. Derivative traders should explore strategies that take advantage of the pair staying within a certain range, as strong technical resistance and fundamental support may keep it contained. An options strategy focused on the key levels of 1.3490 to 1.3750 could be a wise way to manage the opposing pressures in the weeks ahead.

Germany’s factory orders unexpectedly surged by 7.8% month-on-month, defying the expected decline of 2.2%

Germany’s factory orders jumped 7.8% in December compared to the previous month. This was a surprise, as analysts expected a 2.2% drop. In November, factory orders were revised to show a growth of 5.7%.

Year-over-year, industrial orders also rose by 13%, up from a previous increase of 10.6%. This suggests that manufacturing activity in Germany is picking up.

Due to this strong data, the Euro received some support, with EUR/USD trading slightly higher at around 1.1800. The Euro performed particularly well against the Australian Dollar.

The currency heat map illustrates percentage changes among major currencies. By selecting the Euro from the left column and the US Dollar from the top row, you can see the percentage change for EUR/USD.

We observed a similar pattern at the end of 2025, when Germany’s factory orders rose by 7.8% month-over-month in December. This helped the EUR/USD pair reach around the 1.1800 level at that time. The data surprised many by showing growth instead of a decline, highlighting the strength of Germany’s industrial sector.

This week’s industrial production figures for January 2026 confirm this trend, showing a solid 1.2% increase compared to a forecast of just 0.5%. This follows last week’s German IFO Business Climate index, which rose to 91.5, the highest in ten months. These figures indicate that the manufacturing sector is not just recovering, but is actively expanding as we enter the new year.

With this positive momentum, buying short-term call options on the Euro seems like a smart move for the coming weeks. This strategy allows traders to profit from a potential rise in EUR/USD while keeping risks well-defined. Implied volatility is currently low, making it an affordable way to position for further Euro strength.

For a more cautious approach, consider using bull call spreads on EUR/USD futures. This strategy lowers the initial cost by selling a higher-strike call while buying a lower-strike call. It fits a market outlook where we expect gradual gains rather than sharp movements.

These strong economic results will be significant for the European Central Bank (ECB), especially since the latest Eurozone Consumer Price Index (CPI) data for January showed a 2.4% increase. Although this is down from last year’s highs, it remains above the ECB’s target, restricting their ability to cut rates. These positive German figures support a cautious but hawkish stance, which should continue to bolster the Euro.

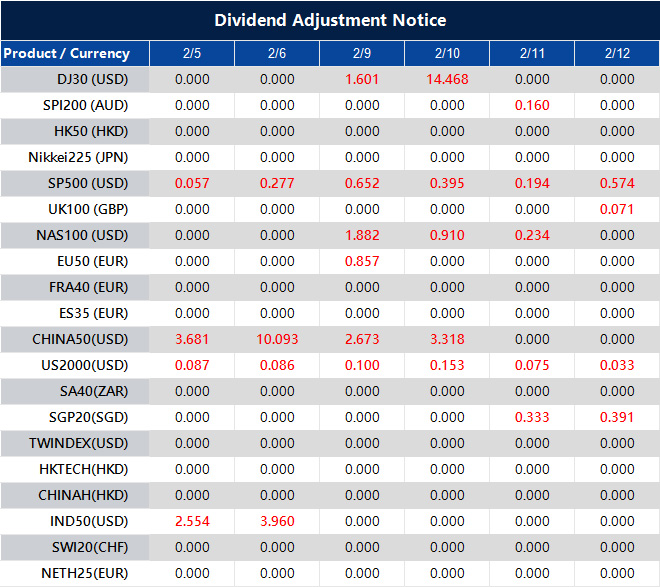

Dividend Adjustment Notice – Feb 05 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].