Interest rate expectations are mostly stable ahead of this week’s US economic data, but they could change significantly after the labor market reports.

By the end of the year, the Federal Reserve might cut rates by 55 basis points, with a 90% chance of a cut in the upcoming meeting. In contrast, the European Central Bank and the Bank of England are projected to keep rates unchanged, with a 99% probability.

The Bank of Canada and Reserve Bank Expectations

The Bank of Canada may reduce rates by 27 basis points, but there is a 53% chance they will keep rates the same. The Reserve Bank of Australia is expected to lower rates by 31 basis points, although there’s an 83% chance they will maintain the current rate. The Reserve Bank of New Zealand might cut rates by 38 basis points, while the Swiss National Bank is likely to keep rates steady.

The Bank of Japan could raise rates by 15 basis points, but there’s a 95% chance they will hold rates. Recent events have created a slightly hawkish outlook for the ECB and BoE, while the Bank of Canada appears more dovish. All eyes will be on the US labor data, particularly the ADP report on Thursday and the Non-Farm Payroll (NFP) report on Friday, as these will significantly impact interest rate predictions.

As we enter September 2025, the market anticipates significant rate cuts from the Federal Reserve before the year ends, showing a stark difference from other central banks. There’s a 90% chance of a Fed rate cut at the next meeting, unlike the European Central Bank and Bank of England, which expect no changes. This divergence will shape our trading strategies in the upcoming weeks.

US Labor Market Data Significance

The US labor market data, especially Friday’s NFP report, is crucial for confirming or challenging these expectations. Last week’s JOLTS report revealed a decline in job openings to 8.5 million, the lowest in two years. If the NFP number falls below the expected 150,000, it would strengthen the argument for Fed cuts and likely weaken the US dollar.

Given this uncertainty, we should consider buying volatility through options on major currency pairs like EUR/USD and USD/JPY. A straddle or strangle strategy could be beneficial if the NFP report surprises in either direction, causing a sharp market movement. The current expectation of a 55 basis point Fed cut is significant, and a strong jobs report would lead to a major market adjustment.

The policy divergence with Europe is clear, especially since August’s core inflation in the Eurozone was at 3.1%, exceeding the ECB’s target. This reinforces the belief that the ECB and BoE will remain steady, creating opportunities for EUR/USD and GBP/USD strength. We might consider call options if the US data confirms a slowdown.

In Canada, the economy is more fragile, with the second quarter 2025 GDP shrinking by 0.2%, signaling a technical recession. This dovish outlook for the Bank of Canada makes the USD/CAD pair very sensitive to the NFP data. A strong US report could push this pair significantly higher due to the widening economic gap.

A less headline-driven trade exists in the Pacific, where the Reserve Bank of New Zealand is likely to cut rates while Australia remains stable. This suggests the Australian dollar might perform better than the New Zealand dollar. We could look at positioning for a higher AUD/NZD exchange rate, since this trade isn’t heavily dependent on the US jobs data.

This scenario, with a clear central bank divergence centered around a few key data points, resembles the pivot we experienced in late 2023. Back then, a sudden shift in Fed expectations led to a sharp revaluation across asset classes. We must be ready for a similar rise in volatility following this week’s important reports.

Create your live VT Markets account and start trading now.

here to set up a live account on VT Markets now

Written on September 2, 2025 at 11:35 am, by davin

The GBPUSD pair is currently trading within a wide range, showing significant movement. Last week, the USD ended on a low note but has made a comeback this week, regaining most of its losses. Traders are watching the labor market closely, especially the upcoming NFP report. Right now, there’s an 89% chance of a rate cut in September, with an expectation of 55 basis points of easing by the end of the year. Strong economic data could change these expectations, while weak data may drive the dollar down further.

In the UK, the Bank of England’s (BoE) recent aggressive position has been supported by robust data, including the latest UK Consumer Price Index (CPI), which exceeded forecasts. Mixed but strong Flash PMIs show inflationary pressures are still strong. The BoE remains focused on inflation, especially as long-term yields in the UK rise, reflecting market impatience with inflation controls.

On the daily GBPUSD chart, the price has pulled back to the 1.3368 support level and is trying to rally towards the 1.3590 resistance. The 4-hour chart shows a clear bounce from this support, while the 1-hour chart points to the 1.3445 level as minor resistance. Upcoming US data releases to watch include ISM Manufacturing PMI, Job Openings, US ADP Employment, Jobless Claims, ISM Services PMI, and the NFP report.

The GBPUSD pair seems caught between two conflicting central bank strategies, creating this wide trading range. The US appears likely to cut rates, while the UK is still dealing with ongoing inflation. This conflict keeps the price between the key support at 1.3368 and resistance at 1.3590.

The August 2025 Non-Farm Payrolls report showed that the US added only 160,000 jobs instead of the expected 185,000. With the unemployment rate rising to 4.1%, the market’s prediction of an 89% chance for a Federal Reserve rate cut this month appears valid. This outlook is likely to support GBPUSD on any dips.

Meanwhile, the pound remains supported by persistent UK inflation, a major concern for the Bank of England. The last July 2025 CPI reading was a high 3.1%, significantly over the target, and the August services PMI came in strong at 52.5, indicating ongoing price pressures. This hawkish stance from the BoE is prompting buyers to enter near the 1.3368 support.

For derivative traders, this situation is perfect for range-bound strategies in the coming weeks. Selling an iron condor, with short strikes just outside the 1.3368-1.3590 range, could be effective. This strategy would benefit from time decay as long as the upcoming data does not cause any major breakout.

However, we need to be ready for a possible breakout due to this week’s US ISM Services PMI and further comments from Fed officials. Traders expecting a large move could consider buying straddles or strangles to take advantage of volatility, regardless of the direction. It’s important to set positions before the event since implied volatility will likely rise leading up to the release.

Looking back, the sharp currency swings during the 2022-2023 rate hiking cycle remind us how quickly trading ranges can break. While the current environment seems stable, conflicting economic data from the US and UK indicates that this period of calm is fragile. Therefore, we should manage risk carefully, as surprises from either central bank could lead to a significant market move.

here to set up a live account on VT Markets now

Written on September 2, 2025 at 10:35 am, by davin

Eurostat has released data showing that the Eurozone’s preliminary Consumer Price Index (CPI) for August increased by 2.1% compared to last year. This is slightly higher than the expected 2.0%. The previous CPI was recorded at 2.0%.

The Core CPI, which doesn’t include items like food and energy, rose by 2.3%, matching forecasts, but down from 2.4% before. Services inflation is at a steady 3.1%. These numbers are important for the European Central Bank’s (ECB) upcoming policy meeting.

ECB Meeting Predictions

With overall inflation rising to 2.1% and core inflation easing to 2.3%, the ECB has little reason to change its current policy. We expect the ECB to keep interest rates steady at its meeting next week. This could lead to a period of lower volatility in short-term interest rates.

Traders should think about strategies that benefit from this anticipated stability, like selling volatility on near-term interest rate futures. Current market pricing in €STR futures shows a low chance of a rate change before the end of 2025, reinforcing this view. Since July 2025, implied volatility on three-month EURIBOR options has dropped by nearly 15%.

For equity derivative traders, a steady ECB suggests that markets for indices like the Euro Stoxx 50 will remain within a range. Without a major catalyst for a breakout, using strategies like iron condors to sell premium could work well. The VSTOXX index, which measures Euro Stoxx 50 volatility, has fallen to 14.5, indicating this low-conviction environment.

Services Inflation Watch

The biggest risk to this outlook is the persistent services inflation, which is still high at 3.1%. Considering the stubborn inflation trends from 2023-2024, ongoing services inflation could lead the central bank to delay easing its policy longer than the market expects. This is a key area to monitor for signs of a rebound.

Given this persistent services inflation, betting on aggressive rate cuts in early 2026 may be too soon. A cautious strategy would be to use calendar spreads in rate futures, capturing the expected lack of movement in the coming weeks while remaining open to potential policy changes later on.

Create your live VT Markets account and start trading now.

here to set up a live account on VT Markets now

Written on September 2, 2025 at 10:35 am, by davin

ECB policymaker Gediminas Šimkus has shared his views on interest rates. He mentioned that while some economic risks are coming up, there are no immediate plans to change rates.

Šimkus takes a careful approach as the economy shows some weaknesses. Now that summer is over, we can expect more comments from ECB officials ahead of their policy meeting on September 11.

The European Central Bank has made it clear they won’t take immediate action, but it seems a rate cut may be considered later this year. With the September 11 meeting just over a week away, we should hear more from them. This strategy of holding rates steady now while hinting at future cuts creates a trading opportunity.

This cautious outlook is supported by recent economic data. August 2025’s inflation estimate for the Eurozone is 1.9%, which is below the 2% target and continues the downward trend since spring. Also, recent data shows German factory orders unexpectedly dropped, indicating the economy is slowing faster than expected.

For traders in interest rate derivatives, this suggests preparing for lower rates ahead. Interest in December 2025 Euribor futures is rising, as they would benefit from a rate cut before the year ends. This allows traders to focus on a likely downturn in the fourth quarter rather than just the expected hold on September 11.

The uncertainty before the announcement is also important. We might consider using options on the Euro STOXX 50 index to take advantage of expected volatility. For example, buying a straddle lets us profit from significant market movements in either direction after the ECB’s press conference.

In the currency market, this outlook adds pressure to the EUR/USD pair. We can use options to bet on the Euro weakening, particularly since the US Federal Reserve seems set to keep its rates steady for a longer time. A drop below the 1.06 support level we saw in July 2025 appears more likely now.

We’ve witnessed this pattern before, especially leading up to the first rate cut in June 2024. The ECB hinted at its plans for months before taking action, allowing the market to adjust gradually. This historical trend suggests that while September may see no changes, the overall direction is toward lower rates.

UK 30-year bond yields have hit their highest point since 1998. This is due to growing worries about government debt and spending. Currently, UK borrowing costs are the highest in the G7 countries. While this may seem like a UK issue, rising long-term yields are a global trend, driven not only by government spending but also by central banks’ softer policies.

Central banks are not focusing on controlling inflation, which affects bonds. In the UK, the Bank of England has been cutting interest rates despite having the highest inflation rate in the G7 and ongoing large deficits. This is creating strain in the bond market.

Higher Interest Rates As A Solution

Higher interest rates might unexpectedly solve this issue. Central banks may need to rethink their strategies and consider raising rates. For the UK, the current situation may be hard to reverse, and long-term rates might only drop through a tough recession that leads to contractionary policies.

Increasing rates could lower long-term yields by predicting an economic slowdown, higher unemployment, and reduced inflation. This situation goes against central banks’ goal of a smooth landing, which they had hoped would allow inflation to decrease gradually. The only other option might be a sharp economic downturn.

The UK’s 30-year gilt yield is now at 5.5%, a level not seen since 1998. This signals that the market is responding strongly. This comes shortly after last week’s news showed UK government borrowing forecasts went up by another £20 billion and inflation in August unexpectedly rose to 4.1%. The Bank of England’s rate cut in July, when inflation was still far above its target, is now seen as a major policy mistake.

For derivatives traders, this suggests a time of ongoing volatility, especially in UK assets. We should think about buying volatility through options on the FTSE 100 index or on the pound. The market is reacting to a policy blunder, and the VFTSE index, which measures FTSE volatility, has surged from 18 to 25 in the last month, indicating more turbulence ahead.

Divergence In Central Bank Policies

The gap between a relaxed Bank of England and a more cautious US Federal Reserve makes shorting the pound an appealing option. Although the US 10-year Treasury yield has risen to 4.8%, the Fed has not hinted at rate cuts, which weakens the pound. We are preparing for the pound to retest the 1.18 level against the dollar, akin to the lows experienced during the market turmoil in 2022.

The main idea is that only a harsh economic downturn can address this issue, suggesting we should brace for a recession to lower long-term yields. This leads us to consider trades that would benefit from economic hardship, like buying put options on UK banking and consumer-discretionary stocks. It may also be time to start anticipating aggressive rate cuts in the future, perhaps in late 2026, once the anticipated slowdown sets in.

This situation is not solely a UK concern; it represents a broader global loss of faith in central banks’ commitment to combatting inflation. This is also why gold has surpassed $2,600 per ounce, as it serves as a safeguard against these policy choices. We see value in maintaining long positions in gold derivatives as a key part of our portfolio to protect against this widespread central bank complacency.

Create your live VT Markets account and start trading now.

Today, markets are feeling pressure as the dollar gains popularity amid rising bond yields. S&P 500 futures have dropped by 0.6%, and many investors may face margin calls as the broader markets show signs of stress.

In the gilts market, the 30-year yield has hit 5.69%, the highest level since 1998. This trend is visible across Europe, Japan, and the US. Today is a crucial day as these changes start to affect wider markets. As a result, the FX market is seeing strong activity with the dollar.

Major Currency Movements

EUR/USD has decreased by 0.6% to 1.1640, while USD/JPY has risen by 1% to 148.60. GBP/USD is down 1% to 1.3405, and USD/CHF is up 0.3% to 0.8030. This shift is impacting risk currencies like AUD/USD, which has fallen 0.7% to 0.6505.

Even though markets are under pressure, it’s crucial to stay calm. If long-term yields keep rising, corrections in equities may follow. The steepening of the US yield curve could hint at a policy error by the Fed, which might weaken the dollar in the future amid political challenges.

Gold, despite some recent losses, could attract renewed interest as conditions shift. Buyers may see opportunities in this evolving landscape.

The surge in government bond yields is now affecting all markets, leading to a major reassessment of risk. The US 10-year Treasury yield has surpassed 5.0%, a level known to cause market stress after the August 2025 inflation report unexpectedly hit 3.9%. With borrowing costs rising, investors are selling stocks and seeking the safety of cash.

Equity and Currency Strategies

This rise in fear is creating clear opportunities in the equity options market. The S&P 500 has already fallen 4% from its August highs, and the VIX volatility index has jumped from 14 to over 22. It may be wise to buy put options on major indices like the SPX for protection against a deeper correction if long-term yields continue to climb.

In currency markets, the immediate response has been a strong rally in the US dollar, with the Dollar Index (DXY) hitting a 10-month high of 107.50. While this dollar strength is hurting other currencies, we should be cautious about how long it will last. The rapid steepening of the US yield curve has occasionally indicated a central bank policy error, which could damage the dollar’s credibility in the future.

For those doubtful about the dollar’s long-term strength, using options provides a way to manage risk. Instead of shorting the dollar directly, we can buy medium-term call options on currencies like the Australian dollar or the euro. This allows traders to bet on a rebound when the current panic subsides without taking on the high risk of a spot position.

Finally, we’re keeping a close eye on gold, even as it initially struggles against the strong dollar. The current high-yield and stock market uncertainty mirrors the challenges seen in 2022, when gold eventually performed well as a safe haven. Traders should look for signs of a bottoming pattern and consider using call options on gold ETFs to prepare for a rebound as investors seek safety from bond and equity volatility.

Create your live VT Markets account and start trading now.

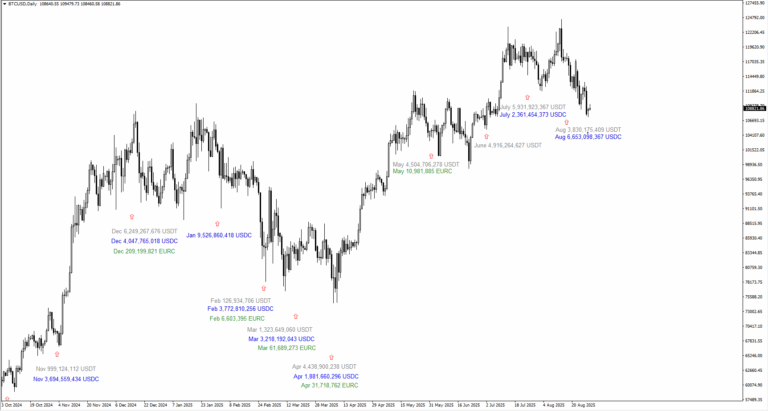

On 12 August, Bitcoin hit a record high of $124,492, only to fall back sharply to $107,340 by the end of the month.

Such dramatic reversals are nothing unusual for Bitcoin. The asset has always moved in cycles of euphoric surges followed by steep corrections, often flushing out excess leverage before testing just how firmly investors remain committed.

Liquidity Still Flowing

Liquidity conditions remain supportive. Between November 2024 and August 2025, over $67 billion in new stablecoins entered circulation across USDT, USDC, and EURC.

December 2024 alone added $10 billion, followed by $9.5 billion in January, while July and August combined delivered another $18 billion.

By late August, stablecoin supply had reached fresh records: USDT $167.3 billion, USDC $70.6 billion, DAI $5.4 billion, and FDUSD $1.45 billion – totalling close to $245 billion. Smaller issuers push the total above $275 billion.

This stockpile of liquidity is ‘dry powder’ that could be redeployed into Bitcoin when sentiment improves.

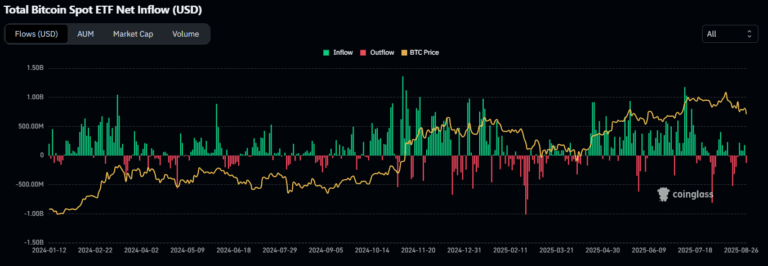

Institutions remain the other driving force. July was particularly strong, with US spot Bitcoin ETFs attracting $6 billion of inflows and crypto ETFs as a whole securing $12.8 billion – a record. This helped propel Bitcoin through the $120,000 barrier.

But August reversed the trend. Spot ETFs saw heavy outflows, including a single-day redemption of $2.6 billion from BlackRock’s IBIT, pulling Bitcoin down by $16,000.

The picture is one of timeframes. Daily ETF flows are erratic, monthly flows steer momentum, and cumulative flows define the long-term trajectory. Despite August’s setback, net institutional buying for 2025 remains intact.

The outlook is cautious: more withdrawals are possible if volatility stays high, yet the broader current still favours accumulation rather than abandonment.

Seasonal Trends Suggest Q4 Strength

Bitcoin’s seasonal pattern points to resilience in the final quarter. Historically, August and September have been weak, while October and November usually deliver strong gains.

On average, October has returned more than 20%, and November over 40%. With August already in the red, the pattern holds. If Bitcoin can ride out September without breaching support, conditions favour another rally into year-end.

Still, history only rhymes – it doesn’t guarantee repetition. Broader macroeconomic forces could always disrupt the seasonal narrative.

At present, Bitcoin is grappling with the $110,000 barrier, now acting as resistance after previously serving as support. Liquidity data shows strong selling pressure clustered between $109,000–110,000, as trapped longs seek to exit.

On the downside, liquidity pockets build up at $108,000 and $107,000. A move above $110,000 could restore momentum, while failure might send prices towards $105,000 or lower.

Traders Prepare For Volatility

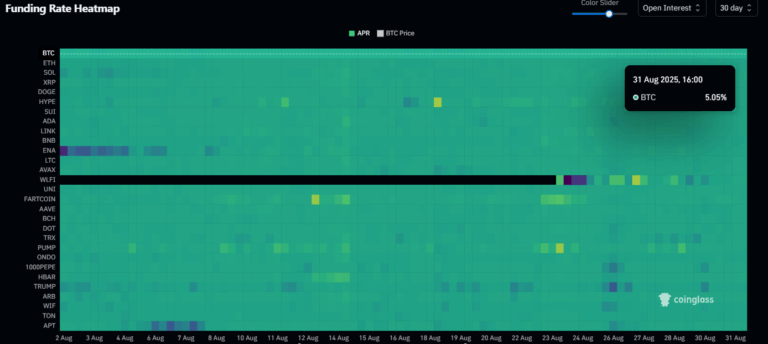

Market sentiment has cooled, but not collapsed. The Fear and Greed Index stands at 40, signalling caution rather than panic. Perpetual futures funding rates are only marginally positive, suggesting modest long positioning but no overheating.

This is the anatomy of a reset: excess optimism has been flushed, leverage cut back, but no full capitulation. It leaves room for stabilisation, though also signals hesitancy as traders wait for clearer signals.

August has tested conviction, but the cycle’s pillars remain: ample liquidity, positive net institutional flows, and favourable seasonal trends into year-end.

The key question now is whether Bitcoin can defend the $107,000 level and reclaim $110,000. Success could set the stage for another test of $124,000 before 2025 ends; failure risks a slide towards $105,000.

Market Movements Of The Week

The new week opens with the US Dollar Index locked in a holding pattern. Prices have lingered around the same area since Friday, showing little appetite for a decisive move.

Traders are watching the 97.409 swing low, a level that, if broken, could pull the index lower toward 97.35.

For now, the lack of momentum signals indecision, but any sharp shift in data or sentiment may push the dollar out of its narrow corridor.

In Europe, the single currency mirrors the dollar’s pause. EURUSD trades close to Friday’s levels, though the charts suggest that a lift toward 1.1755 would be the next zone to monitor.

Sterling also sits in a pivotal position. GBPUSD dipped but failed to crack through 1.35435. If buyers step in and drive it higher, the 1.3555 mark becomes the line to watch for signs of strength.

Across the Pacific, USDJPY drifts lower, and eyes are set on whether 146.208 will give way. A break beneath that level could invite deeper downside.

USDCHF also trends down, with traders marking 0.7960 as the key checkpoint.

The Australian dollar is testing nerves at 0.6550. Sellers have held ground here, but if the price edges upward, 0.6570 offers the next area of interest. New Zealand’s dollar is climbing instead, with 0.5920 as its near-term target.

North America tells a mixed story, as USDCAD trades around 1.3735. Consolidation is evident, and should the pair slip lower, the 1.3700 handle could come into play.

Commodities, meanwhile, are showing more rhythm. Oil appears to be consolidating after recent swings. Traders have an eye on 66.45, where bearish price action could reassert itself should prices rise.

Gold, by contrast, has found traction. After pausing around 3,420 dollars, it pressed higher, with the next challenge set at 3,470 dollars.

Silver continues its own march upward, with momentum favouring the bulls. If a consolidation phase emerges, the 38.75 level will serve as the staging ground for the next push.

Natural gas is also climbing, having rebounded from 2.80. The market now leans toward testing 3.04. Energy traders will be alert to whether this move holds or fades under fresh supply pressures.

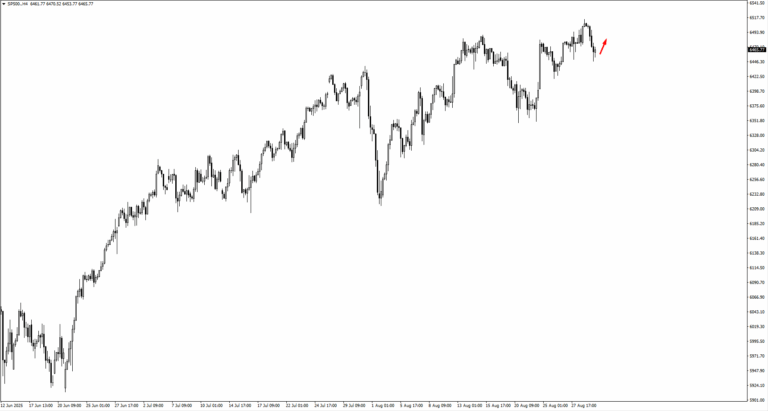

In equities, the S&P 500 retreated from the psychological 6,500 mark before settling. If it manages to rise again, traders are watching the 6,485 area for the quality of price action. A close above 6,497 could open the path to 6,630 or even 6,730.

Nasdaq tells a similar tale. It slipped from 23,780, but the focus now shifts to 23,600. Should it close above 23,700, momentum would likely swing back to the upside.

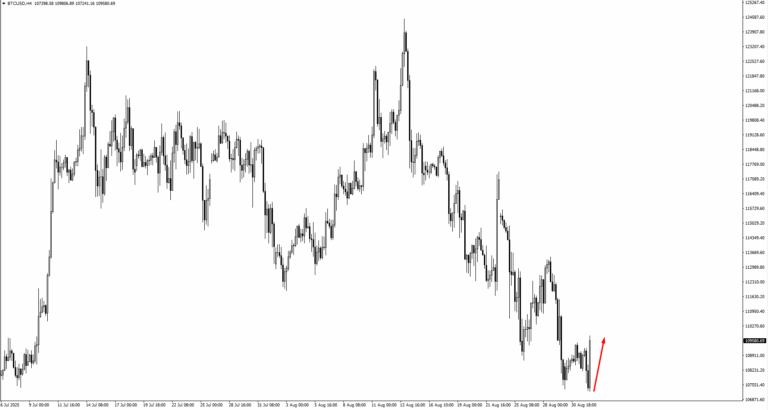

Bitcoin holds the spotlight among digital assets. It found footing at 107,245 but remains fragile. If the price makes a lower low, the market will eye 105,700 and even 101,400 as the next potential landing spots.

Ethereum has its own test ahead, with the 4,585 mark acting as the key pivot for traders seeking confirmation of renewed strength.

Among individual stocks, UnitedHealth shows potential consolidation. If support holds, bulls may look to 270 for a fresh entry, with intrinsic value estimates climbing as high as 410 on recent earnings.

Novo Nordisk, trading above 55.37, also signals the possibility of a fresh leg higher. Analysts now place its intrinsic value around 90, suggesting that investors still see more room in its climb.

The week is set against a backdrop of fragile confidence. Many assets hover around support or resistance, waiting for data or sentiment to tip the balance.

Key Events Of The Week

Activity starts to pick up on Tuesday, 2 Sep, when the US releases its ISM Manufacturing PMI. Forecasts point to a reading of 48.9, slightly higher than July’s 48.0.

Wednesday, 3 Sep, brings a pair of releases that could move different corners of the market. Australia’s GDP is expected to show growth of 0.5 percent quarter-on-quarter, an improvement over the previous 0.2 percent. In the US, JOLTS Job Openings are projected at 7.24 million, down from 7.44 million. The labour market remains a focal point for traders and policymakers alike.

Thursday, 4 Sep, shifts attention back to US services, with the ISM Services PMI forecast at 50.5 compared to the previous 50.1. This sits just above the expansion line and could reinforce the picture of an economy slowing but not yet stalling. Traders will be watching whether the reading provides relief for the dollar or continues to paint a cautious outlook.

Friday, 5 Sep, closes the week with the headline jobs report. Non-Farm Employment Change is expected at 74,000, just above the prior 73,000. The unemployment rate is forecast to tick up to 4.3 percent from 4.2 percent. Together these figures underline a gradual softening in the labour market.

The stock market is facing challenges as bond yields rise, leading to a 0.5% drop in S&P 500 futures. European markets are also feeling the impact, with the DAX falling nearly 1% and the CAC 40 switching from gains to losses.

In France, 30-year bond yields have crossed 4.50% for the first time since 2011, a trend also seen in the UK. Rising bond yields are making their way to Japan and the US, where the US yield curve is steepening. This situation poses difficulties for the stock market and suggests a potential correction ahead.

At the same time, gold prices are falling as traders seek safety in the US dollar. Gold has decreased to $3,478 after earlier increases. With high and steepening yields, purchasing gold during dips could be a good long-term investment strategy.

As the S&P 500 faces pressure from rising bond yields, we believe that stock prices may decline in the short term. The US 10-year Treasury yield reached 4.75% in August 2025, marking its highest level in over a decade. This indicates that increased borrowing costs are affecting corporate profit expectations, suggesting that protective strategies may be wise in the coming weeks.

For traders, this could mean buying put options on major indices like SPY and QQQ to either profit from or protect against another downturn. Volatility is also increasing, with the VIX index rising over 15% in the past week to trade above 22, indicating that market turbulence is likely. In this environment, long volatility positions, like VIX call options, seem more appealing.

We’ve seen this pattern before during the “Taper Tantrum” in 2013, when a sudden rise in Treasury yields caused a sharp drop in the stock market. The current steep rise in the yield curve, with long-term rates increasing faster than short-term ones, is similar to that time. This historical context supports a defensive or bearish approach to equities now.

Although gold is currently declining as investors rush into the US dollar, the underlying surge in yields signals long-term economic stress. This makes buying gold during these dips an attractive strategy for long-term investors. We have already observed a 10% rise in open interest for December 2025 gold call options over the past week, suggesting that traders are preparing for a rebound.

The US dollar is currently the safest option, attracting investment from other asset classes. The US Dollar Index (DXY) just surpassed 107 for the first time this year, confirming its strength. As long as there is instability in the bond market, positioning long in the dollar against other major currencies remains a key strategy.

The pound is declining as UK long-term yields rise. The 30-year yield has reached 5.68%, the highest since 1998. This puts pressure on leaders to create a plan for market stability and rebuild trust.

Long-end yields have been increasing in the UK, US, and euro area. In the US, 10-year yields have gone up by 4 basis points to 4.270%, and 30-year yields are up 5 basis points to 4.965%. This supports the USD/JPY, which is up by 0.7% to 148.20.

Currency Performance

In currency performance, the pound is weak, with GBP/USD down 0.5% to 1.3483. Other major currencies are also slightly falling against the dollar, suggesting a cautious start to trading.

The sharp rise in yields may negatively impact broader markets and risk sentiment. We need to keep an eye on how equity markets react as the day progresses.

The pound is under significant pressure as UK long-term borrowing costs rise. The 30-year Gilt yield hitting 5.68% seems to follow a delay after the August ONS data showed headline CPI unexpectedly rising to 3.1%. Now, the market looks to leaders like Keir Starmer and Rachel Reeves for a plan to boost confidence.

This situation brings back memories of the Gilt market crisis from autumn 2022, after the Truss government’s mini-budget. Traders are increasingly worried about the UK’s debt sustainability, especially with concerns over financing green energy subsidies. This history suggests that the pound is likely to keep declining.

Risk Management Strategies

Given the negative outlook, we recommend buying GBP/USD put options to profit from or protect against further declines. The pair has already fallen to 1.3483, and momentum could push it towards the next key support level at around 1.3350 in the coming weeks. Implied volatility in sterling options has risen to a three-month high, indicating increasing uncertainty.

This issue is not unique to the UK, as US 30-year yields are also nearing 5%, which strengthens the dollar overall. The Federal Reserve’s slightly hawkish tone last week is contributing to this trend, making long dollar positions appealing against various currencies. This is evident in USD/JPY, which has climbed above 148.

The quick rise in “risk-free” rates will likely affect equity markets as well, increasing the discount rate for future earnings and lowering valuations. We should stay cautious and consider defensive strategies, such as buying put options on the FTSE 100 index. If global risk sentiment continues to worsen, UK stocks may be particularly vulnerable due to the pressures on currency and yields.

Create your live VT Markets account and start trading now.

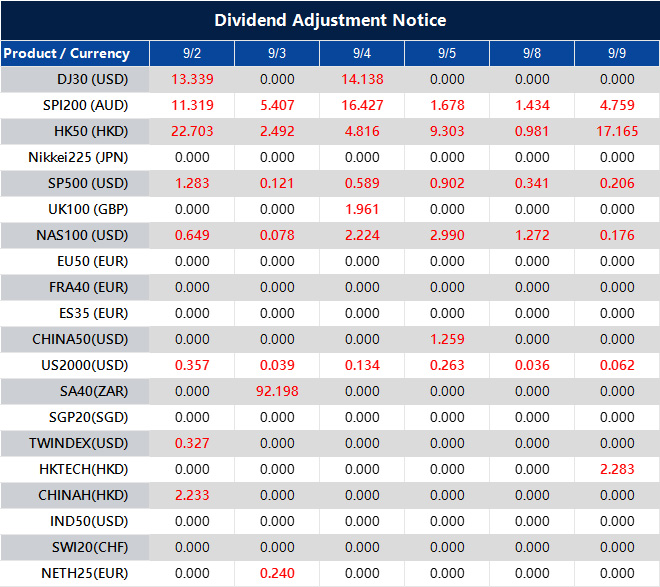

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on September 2, 2025 at 8:31 am, by anakin