Key Points

- SpaceX is not publicly traded, and there is no confirmed IPO timeline despite ongoing speculation.

- Elon Musk has consistently prioritised long-term mission goals over public market pressure.

- A Starlink IPO is more realistic, but only once revenue and cash flow stabilise.

Interest in a SpaceX IPO has grown alongside the company’s rapid rise in valuation and influence. As one of the most valuable private companies in the world, SpaceX sits at the centre of several powerful narratives — space exploration, satellite infrastructure, and next-generation technology.

That combination makes it a natural target for speculation.

Search trends around “SpaceX stock” and “SpaceX IPO” have surged, particularly as retail traders look for the next high-growth opportunity similar to Tesla or Nvidia. However, much of what circulates online tends to blur the line between possibility and reality.

To understand whether a SpaceX IPO is likely, it is important to separate speculation from what has actually been said and done.

Myth 1: SpaceX is Already Publicly Traded

SpaceX remains a privately held company, and this is one of the most common points of confusion.

Unlike publicly listed firms, SpaceX shares are not available on exchanges such as the Nasdaq or NYSE. Ownership is concentrated among founders, employees, and private traders who participate in funding rounds.

Recent private market valuations have placed SpaceX in the range of $150 billion to $180 billion, reflecting strong investor confidence in both its launch business and Starlink division.

However, this valuation does not translate into public accessibility. For most traders, SpaceX stock simply does not exist in a tradable form.

This disconnect between visibility and accessibility is one of the main drivers behind persistent IPO rumours.

Myth 2: A SpaceX IPO Has Already Been Announced

There is no confirmed SpaceX IPO date, and no official filing indicating that the company is preparing to go public.

Elon Musk has addressed this topic on multiple occasions, and his position has been relatively consistent. He has emphasised that taking SpaceX public too early could create pressure to prioritise short-term profitability over long-term objectives.

This matters because SpaceX operates very differently from a typical technology company. Its core activities likerocket development, reusable launch systems, and deep-space missions require heavy capital investment with uncertain timelines.

In public markets, companies are expected to deliver predictable earnings and quarterly performance. SpaceX’s business model does not naturally fit that framework.

Myth 3: SpaceX Will Go Public Soon

Speculation around a near-term IPO often resurfaces during periods of strong valuation growth or major announcements. However, there is little evidence to suggest that a full SpaceX listing is imminent.

The company continues to reinvest heavily into:

- Starship development.

- Launch capacity expansion.

- Global satellite infrastructure.

These projects are long-cycle investments that may take years to generate consistent returns.

Musk has previously indicated that a public listing would only make sense once revenue streams become more stable and predictable. At present, SpaceX’s value is still closely tied to future potential rather than fully realised earnings.

That makes it less suited to the expectations of public equity markets in the near term.

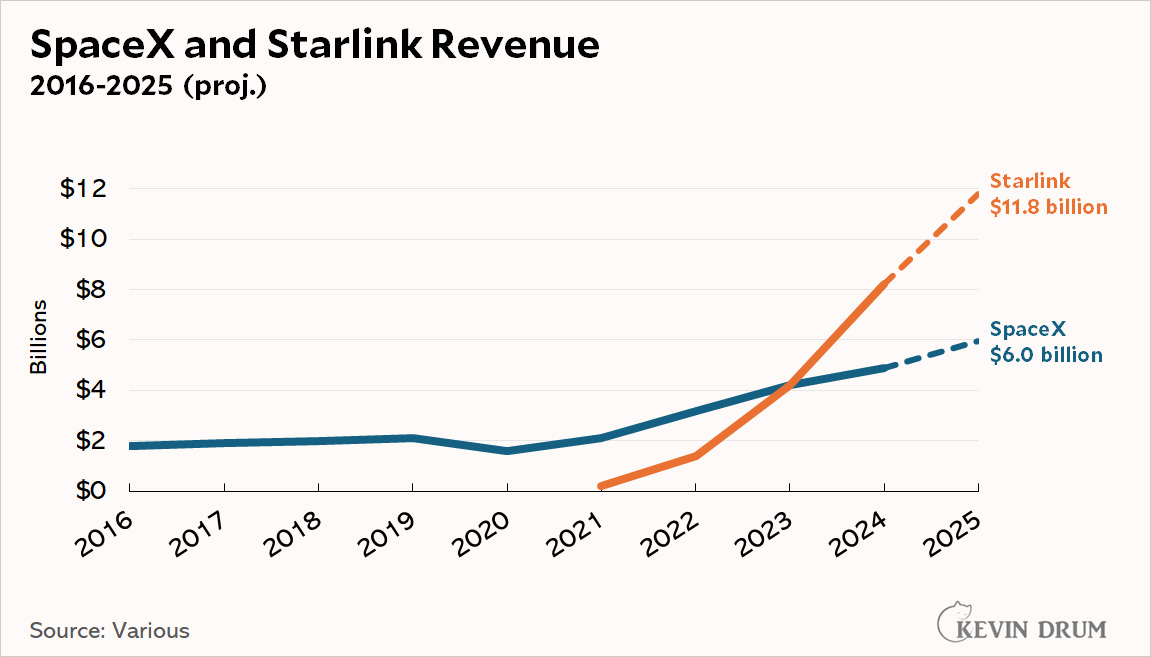

What’s Actually Likely: A Starlink IPO First

If any part of SpaceX were to go public, the most likely candidate is Starlink.

Starlink differs from the rest of SpaceX in one key way: it generates recurring revenue. The satellite internet service has expanded rapidly, serving millions of users across multiple regions and building a more traditional subscription-based business model.

Source: Jabberwocking

This creates a clearer path toward IPO readiness.

Musk has suggested that Starlink could eventually be spun off as a separate entity once:

- Cash flow becomes more predictable.

- Operational scaling stabilises.

- The business reaches a more mature stage.

From a market perspective, Starlink fits the profile of a typical IPO candidate far more closely than SpaceX’s launch operations.

This is why many analysts view a Starlink IPO as the more realistic scenario, rather than a full listing of SpaceX itself.

Why Starlink Still Matters

Even with the fresh SpaceX IPO headlines, Starlink remains the most useful part of the story for traders to understand.

Starlink is no longer just a futuristic side project. In its 2025 progress report, the company said it connected more than 4.6 million new active customers in that year alone and expanded service to 35 additional countries and territories. It also said Direct to Cell service is now commercially available in the United States and New Zealand, supported by a constellation of more than 400 satellites.

That matters because public markets understand recurring services better than they understand long-horizon engineering ambition. Rocket launches, reusable systems, and deep-space projects are powerful narratives, but recurring connectivity revenue, mobile partnerships, and scaling subscriber growth are easier for investors to price.

What Traders Can Actually Watch Instead

If SpaceX itself still sits out of reach for now, the better question becomes: where does the same theme show up in listed markets?

The first bucket is telecom adoption. T-Mobile has the clearest live commercial connection to Starlink through T-Satellite. When the Starlink story strengthens, this is one of the first listed names traders may want on the watchlist.

The second bucket is satellite communications peers and rivals. AST SpaceMobile says it is building direct-to-cell broadband to end dead zones. Iridium describes itself as a global mobile voice, data, and PNT satellite network and is pushing forward with NTN Direct.

These names do not give direct ownership of SpaceX or Starlink, but they do sit in the same commercial conversation around satellite connectivity, coverage, and next-generation network infrastructure.

The third bucket is space infrastructure. Rocket Lab describes itself as an end-to-end space company. That makes it a cleaner “space economy” read-through than stretching into unrelated tech stocks that only have a weak thematic link. CFD shares of companies like Virgin Galactic (SPCE) may also appeal to traders looking to dabble in the space sector.

The fourth bucket is thematic ETF exposure. Where available on the product list, space-focused ETFs can offer a broader basket approach. Roundhill’s MARS ETF says it invests in companies building the space economy, and its March 2026 factsheet lists Rocket Lab, AST SpaceMobile, EchoStar, Globalstar, and Viasat among its top holdings. Procure’s UFO ETF and VanEck’s JEDI ETF also explicitly frame themselves around space, satellite, and communications exposure.

SpaceX may still be private today, but the price action around satellite communications and the wider space economy is already visible in listed markets. Track relevant shares, ETFs, and market themes on the VT Markets app.

What a SpaceX IPO Could Mean for Markets

If SpaceX were to go public, it would likely be one of the most significant listings in modern market history.

At current valuation levels, an IPO could:

- Rank among the largest technology listings ever.

- Attract substantial institutional capital.

- Influence index weightings and fund allocations.

Beyond size, it would also carry narrative weight. SpaceX sits at the intersection of several major themes:

- Advanced technology.

- Infrastructure expansion.

- Long-term innovation.

A public listing would reinforce these themes and potentially draw further capital into adjacent sectors.

Bottom Line

SpaceX IPO rumours are driven more by investor interest than by confirmed plans.

The company remains private, with no official listing timeline. While a Starlink IPO is a realistic possibility in the future, a full SpaceX public offering appears unlikely in the near term.

For now, SpaceX continues to prioritise long-term growth and innovation over public market participation—making it one of the most closely watched private companies in the world.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

FAQs

Is SpaceX publicly traded?

No, SpaceX is a private company and is not listed on any stock exchange.

Has SpaceX officially announced its IPO?

Reuters has reported that SpaceX is aiming to file soon and may reserve a large share of the offering for retail investors, but final details are still not confirmed publicly.

Why does Starlink matter so much to this story?

Because Starlink has real commercial scale. It added more than 4.6 million new active customers in 2025, expanded to 35 more countries, and now has Direct to Cell service live in the United States and New Zealand.

What public assets are closest to the Starlink theme?

T-Mobile is one of the clearest public links through its T-Satellite with Starlink service. Traders can also watch satellite communications names such as AST SpaceMobile and Iridium, plus space infrastructure companies and relevant ETFs where available.

Why has SpaceX not gone public?

SpaceX remains private to maintain long-term focus, avoid short-term market pressure, and retain operational flexibility.

Start trading now – Click here to create your real VT Markets account