Consumer confidence in New Zealand rises from 98.4 to 101.5, showing improved sentiment

New Zealand’s consumer confidence increased to 101.5 in December, up from 98.4 in November, according to a report by ANZ and Roy Morgan. This boost in confidence shows that consumers have a positive view of the economy.

The data comes from a survey that looked at people’s financial situations, expected economic growth, and their feelings about making big purchases. A rise in consumer confidence usually points to better spending and economic conditions in the coming months.

In October, total net TIC flows in the United States dropped from $190.1 billion to -$37.3 billion.

Total net Treasury International Capital (TIC) flows in the United States dropped significantly in October. The figure fell from $190.1 billion to a negative $37.3 billion, signaling a reversal in capital inflows.

In other economic news, the Japanese Yen declined during intraday trading after the Bank of Japan raised interest rates. Meanwhile, gold prices continued to decrease despite expectations of a Federal Reserve rate cut due to decreasing US inflation.

Interest Rate Impacts on Currency Pairs

The EUR/JPY rose in value as the Bank of Japan lifted interest rates to 0.75%. The GBP/JPY also went up, surpassing the mid-208.00s after the Bank of Japan’s 25 basis points rate increase. The price of WTI crude oil fell, struggling to stay above $56.00. This drop came amid talk of a possible peace agreement between Russia and Ukraine. The Australian Dollar held steady, backed by a strong Reserve Bank of Australia policy outlook. On the cryptocurrency front, Ripple maintained a support level at $1.82, although there were concerns about low retail demand. Top losers in the crypto market included Pump.fun, Pudgy Penguins, and Hyperliquid, all experiencing double-digit declines as the November US Consumer Price Index unexpectedly dropped to 2.7%.Economic Indicators and Investment Strategies

The drastic shift in U.S. capital flows for October 2025—from a $190.1 billion inflow to a $37.3 billion outflow—serves as an important warning. This trend could mean foreign investors are offloading U.S. assets, leading to potential pressure on the dollar if it continues into November and December. Derivative traders might consider positions that profit from a weaker dollar, such as buying puts on the dollar index or calls on pairs like EUR/USD. With U.S. inflation cooling to 2.7% in November, below market expectations, the argument for Federal Reserve rate cuts in early 2026 is gaining strength. Historically, markets often react well in advance of the Fed’s decisions, a trend observed in late 2023 and early 2024. Thus, positioning in interest rate futures that bet on a lower federal funds rate by the second quarter of 2026 may be a wise strategy. The Bank of Japan’s rate hike seems to have been fully anticipated, resulting in a “buy the rumor, sell the fact” response reflected in the yen’s weakness. This outcome makes yen-funded carry trades attractive again, where investments are made in higher-yielding currencies while borrowing in a lower-interest currency. Selling yen futures or buying call options on pairs like GBP/JPY, which is currently performing well, seems like a sensible approach for the upcoming weeks. Gold’s decline below $4,350 is puzzling, especially with decreasing inflation data. However, it highlights significant profit-taking and liquidation by short-term traders, which might present a buying opportunity for those with a longer-term outlook. The environment of expected rate cuts remains beneficial for non-yielding assets, suggesting this is a temporary dip. Long-dated call options on gold could be an intriguing bet on a future rebound. In the energy sector, crude oil’s struggle below $56 per barrel is largely tied to geopolitical factors rather than supply and demand basics. A potential peace agreement in Ukraine could remove the substantial risk premium built into oil prices since the conflict intensified in the early 2020s. Traders should brace for further price drops, as a formal agreement could lead to a quick sell-off toward the $50 mark, making puts on WTI futures a relevant hedge. Create your live VT Markets account and start trading now.In October, U.S. net long-term TIC flows totaled $17.5 billion, falling short of expectations.

The United States had net long-term Treasury International Capital (TIC) flows of $17.5 billion in October, which is much lower than the expected $122.7 billion. This drop might show that foreign investors are less interested in U.S. assets, raising concerns about how the U.S. will fund its budget deficit.

This information is crucial for understanding investor confidence and might impact future monetary and fiscal policies. Lower inflows could influence the Federal Reserve’s talks about interest rates and overall economic strategies.

Impact on U.S. Financial Markets

Market analysts are closely watching how this data could affect U.S. financial markets and the value of the dollar in the upcoming weeks. It highlights the need to balance U.S. economic conditions with foreign investor sentiment to ensure economic stability. The October TIC data shows foreign investment at only $17.5 billion, compared to the expected $122.7 billion, which is a significant red flag. This drop in foreign capital is especially troubling since the Congressional Budget Office recently confirmed that the fiscal year 2025 budget deficit is over $2.1 trillion. This imbalance raises serious questions about who will buy our debt, which could push Treasury yields higher soon. We anticipate a weaker U.S. dollar as less foreign money comes in to buy our assets. The U.S. Dollar Index (DXY) has already fallen from around 106 in late October to below 103 this week, supporting this trend. Traders might consider buying put options on the dollar or establishing long positions in currency pairs like EUR/USD through futures contracts.Challenges for the Federal Reserve

This weak demand for U.S. debt creates challenges for the Federal Reserve, as their tight monetary policy depends on a stable bond market. Recent comments from officials indicate they expect to keep interest rates steady until at least 2026, but a funding crisis could drive long-term yields up regardless of their decisions. We see a chance to gain from rising interest rate volatility by using options like straddles on Treasury bond ETFs such as TLT. This issue isn’t new, but it has sped up a trend that began in 2024 when major foreign creditors started consistently selling off U.S. debt. If higher yields are required to attract capital, this will increase borrowing costs for corporations and make stocks less appealing. In this environment, buying protective put options on the S&P 500 for the first quarter of 2026 makes sense. Create your live VT Markets account and start trading now.In South Korea, year-on-year producer price index growth increased to 1.9%, up from 1.5%

The Producer Price Index (PPI) in South Korea increased to 1.9% year-on-year in November, up from 1.5% the month before. This rise may indicate rising inflation and could influence future consumer prices, monetary policy, and the economy as a whole.

Other market topics include changes in currencies like the Japanese yen and the Australian dollar, as well as expectations for the USD/CAD. Investors are also looking at commodities like gold in light of economic policies and are waiting for decisions from central banks like the Bank of England and the People’s Bank of China.

Expert Analysis

Expert insights and broker recommendations for 2025 are available, focusing on effective trading strategies in Forex and commodities. This information highlights potential risks and uncertainties in the market, stressing the importance of conducting personal research. In November, South Korea’s producer prices rose by 1.9%, an increase from the previous 1.5%. This increase often indicates that consumer prices will soon rise too, posing challenges for the Bank of Korea. Investors may need to rethink expectations for interest rate cuts. We see this development alongside consumer inflation still at 2.8% in November 2025, surpassing the central bank’s target of 2%. Although economic growth has been slow, with modest numbers from the third quarter, this ongoing inflation makes it hard for the Bank of Korea to relax its policies. The central bank has maintained its key interest rate at 3.50% for over a year, and this data strengthens their cautious approach. For currency traders, these conditions favor a stronger Korean Won, especially since the US Federal Reserve may start cutting rates in the first half of 2026. This difference in policies could attract capital to South Korea, making options on the KRW or selling USD/KRW futures appealing. We might see the USD/KRW pair test the 1,320 support level soon.Interest Rate Market Impact

Regarding the interest rate markets, this new PPI data likely dispels thoughts of a Bank of Korea rate cut early in 2026. Current derivative pricing for a rate cut in the first quarter seems out of sync with the ongoing inflation trend. This presents an opportunity to position for Korean short-term rates to remain higher for longer than what the market expects. This situation could pose challenges for Korean equities. Higher borrowing costs combined with a stronger Won could be tough on the export-heavy KOSPI 200 index. Major exporters have benefited from a weaker currency for most of 2025, but that advantage is now waning. Thus, we might want to consider buying put options on the KOSPI 200 to protect against a potential market decline as we head into the new year. Create your live VT Markets account and start trading now.In November, South Korea’s Producer Price Index rose from 0.2% to 0.3% month-on-month.

In November, South Korea’s Producer Price Index (PPI) rose by 0.3%, up from last month’s 0.2% increase. This index shows how prices for goods and services change, which affects the economy.

In the currency market, the GBP/JPY pair climbed above the mid-208.00s after the Bank of Japan raised rates by 25 basis points. Despite a stronger national Consumer Price Index, the Japanese Yen weakened as traders awaited more policy news.

Australian Dollar Stability

The Australian Dollar stayed stable, thanks to a hawkish outlook from the Reserve Bank of Australia. The USD/CAD traded below 1.3800 amid talks of possible rate cuts from the Federal Reserve. Gold prices dipped below $4,350 due to profit-taking and low long liquidation. Meanwhile, cryptocurrencies like Pump.fun, Pudgy Penguins, and Hyperliquid saw double-digit declines in a bearish market. The Bank of England cut rates to 3.75%, a decision that sparked some internal disagreement. Ripple’s value remained at $1.82, influenced by low retail interest in the larger cryptocurrency market.Federal Reserve Rate Cuts Expectation

On December 19, 2025, the main focus in the markets is the expectation of Federal Reserve rate cuts. November’s US Consumer Price Index showed a rate of 2.7%, reinforcing this expectation. The derivatives market now indicates more than an 85% chance of a 25 basis-point cut by the Fed in early 2026, putting pressure on the US dollar. This contrasts with other central banks, which have a more aggressive stance. The European Central Bank has raised its inflation forecasts, and the Reserve Bank of Australia remains firm in its policy, suggesting strength for the Euro and Australian Dollar. Recently, the yield gap between US and German 2-year bonds narrowed by 30 basis points, benefiting long EUR/USD positions. The Japanese Yen has weakened, despite the Bank of Japan’s recent rate hike, indicating that traders viewed the move as too small. Historical policy shifts from the BoJ suggest that the market does not expect a significant tightening cycle, making carry trades like long GBP/JPY appealing, even at high levels. Commodity markets are influenced by specific conditions. Expectations of a Russia-Ukraine peace deal are keeping WTI crude oil under $56, and implied volatility in oil options spiked over 15% in the past two weeks, hinting at anticipated price changes. Gold’s drop below $4,350 amid Fed easing expectations is notable, suggesting traders are either booking profits or believe a soft economic landing will lessen demand for safe-haven assets. Create your live VT Markets account and start trading now.Banxico lowers rates to 7% after a 4-1 vote, with dissent from Heat

The Bank of Mexico, known as Banxico, lowered interest rates from 7.25% to 7% after a 4-1 vote. Deputy Governor Jonathan Heat disagreed and wanted to keep rates the same.

Banxico’s board will review future rate changes while monitoring the inflation target, expected by the third quarter of 2026. The exchange rate of the US Dollar to Mexican Peso (USD/MXN) hardly changed, remaining around 18.00.

Bank Meetings and Influence

Banxico meets eight times a year and pays close attention to the US Federal Reserve’s decisions, usually holding its meetings a week later. The bank uses interest rates to control inflation, aiming to keep it between 2% and 4%. Higher interest rates can attract more investment, strengthening the Mexican Peso, while lower rates might cause it to weaken. Banxico acted quickly to stabilize the peso after the Covid-19 pandemic, sometimes even before the US Fed made changes. Banxico’s job is to maintain the value of the Mexican Peso and ensure inflation stays within target levels. Its decisions can significantly impact Mexico’s economy and how confident investors feel.Market Reactions and Strategies

The recent rate cut to 7.00% by the Bank of Mexico was expected, which is why the market’s response in the USD/MXN pair was muted. This marks the start of a gradual easing cycle rather than a series of aggressive cuts. The latest inflation data for November 2025 is at 4.1%, supporting the central bank’s cautious approach. A key consideration is the rate difference with the United States, which stands at 250 basis points. The US Federal Reserve has kept its benchmark rate at 4.50% for the last two meetings, citing ongoing core inflation of 3.8%. This large gap makes holding the Mexican Peso appealing for carry trades. Since this decision was widely anticipated, implied volatility in USD/MXN options has likely decreased, making strategies like selling out-of-the-money calls an attractive way to earn income. This will work well if the pair stays below crucial resistance, such as the 18.07 level. For those expecting a change in direction, lower volatility also makes buying long-dated calls a less expensive option to bet on a weaker Peso next year. We are closely monitoring the forward markets as they will show how quickly traders believe the rate gap will close. The Peso’s strong performance is a trend continuing from 2023 and 2024 when the rate difference often exceeded 600 basis points. As long as Banxico signals a slower pace of rate cuts than the market expects, holding short positions on USD/MXN futures remains a solid strategy. Create your live VT Markets account and start trading now.Westpac Consumer Survey in New Zealand rises to 96.5 from 90.9

The Westpac New Zealand Consumer Survey for the fourth quarter rose from 90.9 to 96.5. This increase indicates that consumer confidence in New Zealand’s economy is growing, which could impact economic growth and monetary policy decisions.

Factors Influencing Consumer Sentiment

Several factors are driving this increase in consumer sentiment, including expectations for inflation and job availability. It’s important to monitor this trend, as it may influence the Reserve Bank of New Zealand’s future interest rate choices. Higher consumer confidence can lead to increased spending, which may boost economic activity and impact the New Zealand Dollar in the foreign exchange market. The rise in the Westpac Consumer Survey reflects a more positive view among consumers, which could aid New Zealand’s economic recovery. The jump in consumer confidence to 96.5 is significant as we approach the holiday season. Currently, New Zealand’s annual inflation rate remains high at 3.8% from last quarter. This optimistic consumer sentiment likely reduces the chance of an early interest rate cut from the Reserve Bank of New Zealand in 2026, challenging the market expectations that had been building over the last few months. We should think about buying call options on the NZD/USD with expiration dates in February and March 2026. If this renewed confidence leads to strong retail sales, the New Zealand dollar might break out of the narrow range it has been in for much of this year. We also expect an increase in implied volatility, which suggests it’s wise to establish these positions sooner rather than later.Interest Rates and Currency Implications

This change is notable compared to late 2023 and early 2024 when consumer confidence was low and the economy was shrinking. The Official Cash Rate has remained high at 5.50% since mid-2023, and this new data implies that households are beginning to adapt to this situation, giving the central bank more flexibility to hold its current stance. This positive outlook also makes interest rate swaps more appealing. The market had been anticipating a series of rate cuts to start in mid-2026, but this favorable data could delay those expectations. We could position ourselves to benefit from the Official Cash Rate remaining high through the first half of next year. From a cross-currency perspective, this strengthens the case for buying NZD against AUD. The Australian economy is slowing, which increases the chances that the Reserve Bank of Australia may need to cut rates before the Reserve Bank of New Zealand does. This difference in monetary policy could benefit the New Zealand dollar in the coming weeks. Create your live VT Markets account and start trading now.Gold pulls back from highs after weak US inflation report, currently trading at $4,335

Gold prices dropped after reaching nearly two-month highs as traders took advantage of weaker US inflation reports. The US Consumer Price Index (CPI) is at its lowest in years, but concerns about a possible government shutdown make the data less reliable. While short-term easing from the Federal Reserve is expected to be limited, a weaker US Dollar and geopolitical tensions continue to support gold prices.

Gold hit a high of $4,374 following the US’s disappointing inflation figures, closing at $4,335. The US core CPI for November is its lowest since 2021, raising concerns over potential data inaccuracies due to the government shutdown.

Federal Reserve and Interest Rate Expectations

The chance of a rate cut at the Federal Reserve’s January meeting is currently 24%, with a 60 basis point decrease factored in for the year. This puts pressure on the US Dollar, benefitting gold prices. However, easing geopolitical tensions may limit gold’s rise as US-Russia discussions are set to resume. In November, US CPI rose by 2.7% year-on-year, down from 3.0% in September, with core CPI at 2.6%. Physical gold exports from Switzerland to India dropped 15% in November due to high prices, while shipments to China increased. US Treasury yields fell, with the 10-year rate at 4.12%, and the US Dollar Index slightly up at 98.43. Gold’s upward trend paused below $4,350, and its momentum appears to be weakening. With gold’s recent pullback, there’s a short-term chance to prepare for consolidation or a slight dip. The failure to surpass the all-time high of $4,381 indicates possible buyer fatigue. Derivative traders might consider selling call options with a strike price above $4,400. This strategy collects premium while expecting recent highs to act as strong resistance in the upcoming weeks.Market Backdrop and Currency Impact

Gold prices have more than doubled from around $2,100 in 2023. This significant increase makes current prices sensitive to profit-taking on any news. Now that prices are below $4,350, buying short-dated put options could shield against a sharp decline toward the $4,300 support level. However, we shouldn’t be overly negative, as the fundamental outlook for gold remains encouraging. The market expects 60 basis points of interest rate cuts for next year, a big change from the aggressive rate hikes of 2022 and 2023. Lower interest rates reduce the cost of holding non-yielding gold, which should support prices. The weakness in the US Dollar is another important factor. The US Dollar Index is around 98.43, down from the 104-106 range throughout much of 2023, making gold more affordable for foreign buyers. This trend is supported by ongoing demand from central banks, which continue to make significant purchases after acquiring 1,136 tonnes in record numbers back in 2022. We must approach the recent soft inflation report with caution, as the data may have been affected by the 43-day government shutdown. The true inflation situation remains unclear, and the upcoming Personal Consumption Expenditures (PCE) report will be crucial. Any indication that inflation is more persistent than the CPI shows could quickly revive expectations of a cautious Fed, leading to a surge in gold prices. Create your live VT Markets account and start trading now.Argentina’s unemployment rate fell to 6.6% in the third quarter, down from 7.6%

Argentina’s unemployment rate has dropped to 6.6% in the third quarter, down from 7.6% previously. This is a good sign for the labor market, but challenges remain.

The economic landscape is constantly shifting, influenced by various factors affecting currencies and commodities. Market reactions may vary as analysts evaluate this data alongside global economic trends.

Unemployment Rate Drop

The decline in Argentina’s unemployment rate to 6.6% is encouraging. It suggests that the economic reforms started in late 2023 might be stabilizing the labor market. This marks the second consecutive quarterly drop, indicating a slow yet genuine recovery after the severe recession in 2024. Traders should see this not as a sign of rapid growth but as reduced risk for Argentine investments. For those trading the Argentine Peso, this news could support a strategy of selling USD/ARS volatility. Following the significant devaluation in 2024, when the unofficial exchange rate exceeded 2,000 pesos to the dollar, the currency has been somewhat stable around 1,500 pesos in the latter part of 2025. Given this positive news, it may be wise to consider selling out-of-the-money call options on the USD/ARS pair, as the likelihood of a major currency collapse seems lower in the short term. In equity derivatives, focus on the Merval index, which has increased by nearly 50% in 2025 as foreign investment cautiously returns. This employment report benefits consumer and banking stocks, which make up a large part of the index. Buying call options on Merval-linked ETFs for the first quarter of 2026 could be an easy way to position for continued positive sentiment.Risk Management Strategies

Nevertheless, we must be careful since central bank reserves are still very low, and inflation, while down from its peak, was reported at 8.5% month-over-month in November 2025. Therefore, any long positions should be protected. Pairing long equity calls with a small purchase of far out-of-the-money USD/ARS calls could help safeguard against any sudden political or economic changes. Create your live VT Markets account and start trading now.Holiday Trading Adjustment Notice – Dec 19 ,2025

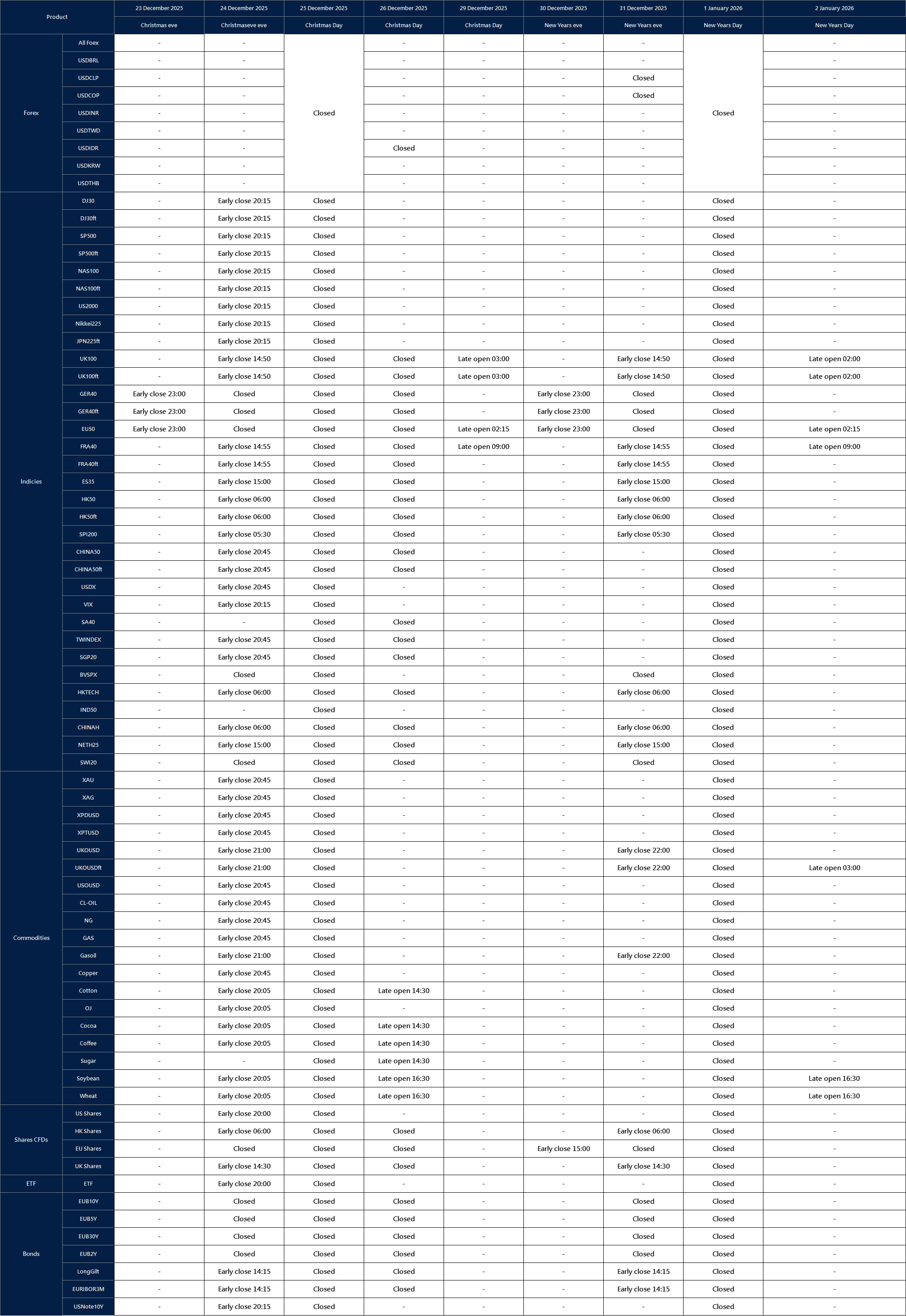

Dear Client,

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the affected products:

Holiday Trading Adjustment Notice

Note: The dash sign (-) indicates normal trading hours.

Friendly Reminder:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]

{kind=link}