Hopes for a Russia-Ukraine truce lead Brent oil prices to a six-month low

Renewed hope for a ceasefire between Russia and Ukraine has affected the oil market. ICE Brent crude fell over 0.9% to $60.56 per barrel, reaching its lowest closing price since May. US President Trump mentioned positive developments in discussions held in Berlin, but disagreements over territory are still a major obstacle to a solution.

Even though Russian oil exports remain steady, finding buyers has become challenging due to sanctions. India’s imports of Russian crude are predicted to drop to around 800,000 barrels per day this month, down from 1.9 million barrels per day in November. This decreased demand has led to a rising surplus of Russian oil available at sea.

December’s Eurozone HCOB Composite PMI at 51.9 falls short of the expected 53

The Eurozone HCOB Composite PMI for December is 51.9, which is lower than the expected 53. This indicates a slowdown in economic activity in both the services and manufacturing sectors within the Eurozone.

This PMI number may change how people view the economy in the region, potentially influencing monetary policy and market sentiment. Focus may shift to upcoming events and data releases that could further affect market trends.

ECB’s Expected Response

Due to the slowdown indicated by the latest PMI data, we can expect the European Central Bank (ECB) to take a more cautious approach. With the PMI at 51.9 compared to the 53 forecast, and following November’s inflation rate of 2.7%, we see signs of a decreasing price environment. The combination of slowing growth and easing inflation makes it very unlikely for the ECB to raise interest rates in early 2026. For currency traders, this situation supports the idea of a weaker Euro against the US Dollar in the coming weeks. The Federal Reserve has been more firm in combating inflation, creating a policy gap that benefits the dollar. Consider starting or increasing short positions in EUR/USD futures, aiming for the 1.05 level, which we last saw in October 2025. In the stock market, this data suggests potential challenges for corporate earnings, particularly in cyclical sectors. It might be wise to purchase protective puts on the EURO STOXX 50 index to protect against a possible downturn as we approach the first quarter of 2026. This strategy is similar to how the market reacted in late 2023, when similar weakening data resulted in underperformance for European stocks.Bonds and Volatility

This situation is likely favorable for government bonds, as the market anticipates earlier rate cuts. We see long positions on German 10-year Bund futures as a smart move, with yields potentially dropping from their current level of 2.5%. The last time we saw a consistent weakening in PMIs like this in 2023, Bund yields fell by over 50 basis points in just one quarter. Overall market volatility may rise as investors react to this unexpected weakness. We will keep a close eye on the VSTOXX index, currently near a historical low of 14. If it breaks above 18, it would signal growing uncertainty and could present an opportunity for those trading volatility options. Create your live VT Markets account and start trading now.The Japanese yen may rise further due to a weak US dollar and expectations of a BoJ decision.

The Japanese Yen (JPY) is showing strength early in the European session on Tuesday, causing the USD/JPY pair to drop below the 155.00 level. This movement is influenced by the expected interest rate hike from the Bank of Japan (BoJ) and a general weakness in stock markets, which have helped the JPY perform well recently.

Despite bullish feelings, Japan’s financial difficulties, linked to Prime Minister Sanae Takaichi’s spending initiatives, are limiting JPY gains. At the same time, the US Dollar (USD) is hovering around its lowest point in months due to predictions of future rate cuts by the Federal Reserve, which is boosting the JPY further.

Expectations for BoJ Rate Hike

Investors are anticipating a BoJ rate hike following Governor Kazuo Ueda’s comments about an improved economic and price outlook. Japanese business sentiment has hit a four-year high, supporting the idea of tighter BoJ policies, even as Japan’s manufacturing activity shows slower contraction. Mixed private surveys reflect varied economic activity in Japan, but the JPY continues to thrive as a safe-haven asset amid worries over stock valuations. Traders are considering the possibility of two more Fed rate cuts by 2026, keeping the USD in a weak position, especially with the USD Index close to its lows. Expectations regarding the Fed’s leadership and upcoming economic data are impacting USD/JPY trading strategies. Traders are waiting for US payroll and inflation figures for more insights into the economic landscape. If the USD/JPY drops below the 154.00 level, it may further decline, while resistance is seen near 155.40. A recovery would depend on surpassing crucial levels.Divergent Monetary Policies

The difference between the Bank of Japan’s and the Federal Reserve’s policies is crucial at this time. There’s strong belief that the BoJ will raise interest rates on Friday, December 19th, while the Fed is likely to keep cutting rates in 2026. This policy shift is a major reason to expect a stronger yen soon. Recent data shows Japan’s core consumer price index has stayed above 2.5% for the fifth month in a row, giving the BoJ ample reason to tighten monetary policy. This marks a significant shift from the ultra-loose approach we’ve seen for years, which began to change in 2024. The rising business sentiment, now at a four-year peak, also supports a potential rate hike. Meanwhile, the US dollar appears weak. The most recent Nonfarm Payrolls report revealed a slowing US economy, with just 95,000 jobs added in October, strengthening expectations that the Fed will need to cut rates again next year. This has pushed the US Dollar Index (DXY) down to lows not seen since October 2025. For traders, the current environment favors strategies that benefit from a falling USD/JPY exchange rate. This could mean buying JPY call options or shorting USD/JPY futures, anticipating the pair will decline further. The key event to watch is the BoJ meeting on Friday, paired with the US inflation data on Thursday, which could bring volatility. From a technical standpoint, the failure of the pair to stay above the 155.00 mark is a bearish sign. If it breaks below the recent low of around 154.35, it could test the 154.00 support level, which we see as crucial. If this level is broken, it could trigger further declines. However, there are risks of a sudden bounce back if the BoJ is more cautious than expected or if US inflation reports higher than anticipated. A rise above the 156.00 area would challenge the bearish outlook, potentially leading to a quick unwinding of short positions and pushing the pair higher. Create your live VT Markets account and start trading now.Germany’s HCOB Composite PMI falls to 51.5, missing expectations of 52.5

The Germany HCOB Composite PMI for December was 51.5, below the expected 52.5. This indicates a slight contraction in both the service and manufacturing sectors of the German economy.

The PMI is an important gauge of economic health. Values above 50 indicate growth, while values below 50 signal contraction. The recent drop points to a potential slowdown in economic activity, which may affect future growth expectations.

Impact On Monetary Policy

This data could impact the European Central Bank’s (ECB) policy decisions. People in the Eurozone and broader financial markets will closely watch the implications of this information. This trend matches other economic indicators, which also show signs of weakening. If the anticipated economic recovery does not happen, Germany may need to revise its economic forecasts in the coming months. The latest German composite PMI reading for December 2025 was 51.5, falling short of the 52.5 forecast. This confirms a slowdown in economic expansion. Although still above the 50-point mark indicating growth, this figure shows a clear sign of weakening momentum and reinforces our cautious outlook for the Eurozone’s largest economy.Economic Impact Analysis

This disappointing figure is part of a larger trend; the German IFO Business Climate index dropped to 86.1 in November 2025, the lowest level in over a year. Pessimism about the next six months played a big role in this outlook, which is also reflected in the PMI data. This trend suggests that the economic challenges from the interest rate hikes of 2023 and 2024 are affecting the economy more than expected. For those trading currency derivatives, this data strengthens the case for a weaker Euro as we head into the new year. Traders may look to buy put options on the EUR/USD, possibly targeting the 1.04 level for contracts expiring in late January 2026. This strategy plays directly on the growing divide between a slowing Eurozone and a stronger US economy. On the equity front, we may see weakness in the German DAX index, which includes many export-focused manufacturing companies. Demand for protective puts on DAX futures or related ETFs may increase as institutional investors hedge against a potential downturn. We previously witnessed a similar trend in late 2022 when energy concerns led to hedging activity before a market dip. This news also impacts interest rate traders by delaying expectations for any further ECB rate hikes in early 2026. As a result, we might consider long positions in German Bund futures. A flight to safety combined with a more dovish ECB could lead to higher bond prices and lower yields. The increased uncertainty might also make call options on the VSTOXX, the Eurozone’s volatility index, a worthwhile strategic play in the coming weeks. Create your live VT Markets account and start trading now.Germany’s HCOB Services PMI for December was 52.6, falling short of expectations.

The HCOB Services PMI for Germany in December was 52.6, which is lower than the expected 52.8. This indicates slower growth in the services sector, potentially affecting the Eurozone’s economic outlook.

This news comes during a time of uncertainty about economic recovery, which could influence how markets react in both currency and stock exchanges. Investors may pay more attention to upcoming economic reports and decisions from key financial bodies like the European Central Bank and the Federal Reserve.

Overview Of Economic Impact

In summary, the lower-than-expected Services PMI may impact market trends, possibly changing trading strategies within the Eurozone. The German services PMI at 52.6, while still indicating growth, adds to concerns about the slowing momentum of Europe’s largest economy. Eurozone inflation remained high at 2.9% last month, complicating the European Central Bank’s future plans. This increases the importance of upcoming inflation and employment data before the new year. For those trading DAX derivatives, this could limit the recent rally, which has seen the index rise 6% year-to-date. The VDAX-NEW volatility index has seen a slight increase to around 18, making strategies like protective puts or selling out-of-the-money call spreads appealing. This decline in services follows a weak manufacturing report from last week, confirming a consistent trend.Market And Strategy Implications

The data places slight pressure on the euro, which is trading around 1.07 against the U.S. dollar. It may be wise to consider EUR/USD put options to guard against signs of a European slowdown, especially given the stronger data from the U.S. last quarter. The gap between expectations for the ECB and the Federal Reserve may widen with news like this. We also observed a drop in German 10-year bund yields to about 2.45% following the report. This supports the idea that holding long positions in Bund futures could be a good safeguard against potential economic downturns in the coming weeks. In 2023’s slowdown, we similarly saw bond prices rise as economic data weakened. Overall, this minor miss suggests we should brace for increased market fluctuations rather than clear trends. Our focus should be on strategies that can benefit from sideways movement or provide protection against downturns. All eyes will now be on the flash Eurozone PMI data later this week for further insights into this trend. Create your live VT Markets account and start trading now.Calm trading is seen in USD/CHF near 0.7960 as the US NFP report approaches.

The USD/CHF pair is holding steady around 0.7960 as we await the US Nonfarm Payrolls (NFP) report for October and November. Predictions suggest that 40,000 new jobs will be added in November, a drop from 119,000 in September. The US Dollar Index is near an eight-week low at around 98.15.

The Unemployment Rate is expected to stay the same at 4.4%. This employment data is key for the Federal Reserve’s monetary policy since officials are more focused on the job market rather than inflation. San Francisco Fed President Mary Daly supports cutting interest rates, citing high inflation and a weakening job market.

Swiss Economic Outlook

In Switzerland, inflation is expected to average 0.2% this year and into 2026, which will affect the Swiss National Bank’s policy decisions. GDP growth is projected to slow to 1.1% in 2026, down from 1.4% in 2025. Meanwhile, the USD/CHF remains steady as investors watch for upcoming US economic data, including Retail Sales and S&P Global PMI reports. The market is eagerly waiting for today’s jobs report, keeping USD/CHF stable near 0.7960. We’re anticipating a low number of 40,000 new jobs, a sharp decrease from the monthly average of over 180,000 in much of 2024. This number is crucial as the Federal Reserve has expressed concerns about a softening labor market. If the jobs number meets or falls below expectations, the US Dollar may weaken further as traders bet on Fed rate cuts in early 2026. Futures markets already show an over 85% chance of a rate cut by the end of the first quarter. This suggests that traders might look to buy put options on USD/CHF to prepare for a decline. On the flip side, if the jobs report exceeds expectations, we could see a significant rally in the US Dollar as the market adjusts its dovish bets. We witnessed a similar quick turnaround in the third quarter of 2024 when a strong inflation reading surprised traders. In such a case, call options on USD/CHF could yield substantial gains.Volatility and Market Strategy

Due to high anticipation, volatility is heightened, making options pricier than they were weeks ago. If the jobs report hits the mark, the pair may not move much, resulting in a drop in this priced-in volatility. Selling straddles or strangles could be a good strategy to profit from this expected decrease after the announcement. However, the Swiss Franc’s potential is limited by consistently low inflation forecasts of just 0.2% for the next year. With Swiss economic growth also expected to drop to 1.1% in 2026, the Swiss National Bank is unlikely to tighten its policy. Thus, the Fed’s actions will be the main influence on the currency pair in the upcoming weeks. Create your live VT Markets account and start trading now.Profit-taking causes gold prices to drop as US employment data comes into focus

Gold prices dropped early on Tuesday in Europe, influenced by profit-taking and advancements in peace talks regarding Ukraine. As a safe-haven asset, gold faced pressure due to the Federal Reserve’s indication of only one rate cut expected next year amid ongoing uncertainty.

Although gold retreated from its seven-week highs, upcoming US retail sales, PMI data, and the nonfarm payrolls report may shed light on interest rate changes and affect gold prices. The recent Federal Reserve rate cut hints at more reductions in 2026, lowering the opportunity cost for holding gold.

Technical Analysis Of Gold

Gold maintains its long-term upward trend, staying above the 100-day Exponential Moving Average. Initial resistance is seen at $4,350, while immediate support sits at $4,285. Further declines could test levels at $4,257 or $4,210. Gold is valued for its stability and status as a safe-haven asset, particularly during financial instability. It generally moves inversely to the US Dollar and Treasury rates. In 2022, central banks, especially from emerging markets, accumulated over 1,136 tonnes of gold, worth around $70 billion, which helped them diversify their reserves amid economic uncertainties. Gold prices reflect factors like geopolitical stability, interest rates, and currency strength. Given gold’s recent pullback, we are looking for chances created by short-term profit-taking and positive developments in Ukraine peace talks. The US Nonfarm Payrolls report released earlier today showed a weaker than expected increase of only 155,000 jobs, indicating a cooling labor market. This supports the notion that the Federal Reserve may continue its rate-cutting cycle through 2026. Traders face a key conflict between the Fed’s projection of one rate cut in 2026 and the market’s expectation of at least two cuts. With last week’s core CPI data from November 2025 showing inflation at 2.8%, its lowest in over two years, there is reason to predict a more dovish stance from the Fed. This discrepancy suggests that any signs of economic weakness could significantly shift derivatives pricing toward more aggressive rate cuts, which would be favorable for gold.Opportunities And Risks In Gold Trading

Despite a supportive fundamental landscape, progress in Ukraine peace talks poses a significant challenge, as a resolution could reduce gold’s appeal as a safe-haven asset. A summit scheduled for early January 2026 in Geneva could also limit any short-term rallies. Traders should remain alert for any breakthroughs that might lead to a swift drop in gold prices. Despite geopolitical uncertainties, strong support from central bank purchases offers a price floor. The World Gold Council’s Q3 2025 report highlighted ongoing major purchases by central banks, especially in emerging markets, a trend likely to persist. This consistent demand indicates that price dips, particularly towards the $4,257 level, could be seen as buying opportunities. Looking at history, we recall the Fed’s pivot in 2019, when a shift to rate cuts prompted a prolonged rally in gold, a scenario that might repeat. Currently, options strategies could be beneficial; call spreads could exploit a breakthrough above the $4,350 resistance, while buying puts could serve as a wise hedge against a fall below the $4,285 support, especially if peace talks progress. Create your live VT Markets account and start trading now.US nonfarm payrolls data expected to increase volatility in the Forex market today

The US Dollar stabilized early Tuesday after small losses against major currencies on Monday. Important US economic data is coming out soon, including the October and November Nonfarm Payrolls (NFP), wage inflation, November’s Unemployment Rate, October Retail Sales, and the preliminary December S&P Global PMI. On Monday, the US Dollar dropped by 0.15% but stayed above 98.00 on Tuesday. Predictions suggest the Unemployment Rate will remain at 4.4% in November, with NFP expected to rise by 40,000.

EUR/USD held steady around 1.1750, waiting for German and Eurozone HCOB PMI data. GBP/USD dipped slightly but stayed above 1.3350, as we await the October employment figures from the UK’s Office for National Statistics. In Canada, the annual inflation rate remained steady at 2.2% in November. USD/CAD remained close to 1.3800, while USD/JPY fell about 0.4% due to expected changes in Bank of Japan policies.

Australia And Gold Market Trends

Private sector growth in Australia slowed, causing AUD/USD to trade below 0.6650. Gold prices hovered around $4,280, experiencing a decline amidst optimism over a possible Russia-Ukraine peace deal. Nonfarm Payrolls provide key insights into US employment, influencing decisions by the Federal Reserve and often positively impacting the US Dollar. A strong NFP typically indicates economic growth, affecting both currency and commodities like Gold. However, the market can react in complex ways, with various report details shaping the outcome. Today’s main event is the release of Nonfarm Payrolls data, expected to create considerable market volatility. Anticipating a minimal gain of only 40,000 jobs, we should be ready for sharp price movements in major currency pairs and indices. Derivatives traders can use options to position for this anticipated volatility spike, regardless of the market’s direction.Impact Of The US Labor Market

The weak outlook suggests a slowing US labor market, increasing pressure on the Federal Reserve to consider interest rate cuts. The Fed has held rates steady for an extended period, so any signs of economic weakness could speed up expectations for rate reductions in early 2026. This trend supports a bearish outlook for the US Dollar, as lower interest rates usually weaken a currency. So far this month, the US Dollar has lost ground against most major currencies, especially the Canadian Dollar. The reported unemployment rate of 4.4% is significantly higher than the under-4% levels typical of late 2023 to early 2024, indicating a clear shift in the labor market. If payroll numbers hit or drop below the 40k forecast, we might see another major drop in the USD Index. Additionally, the Bank of Japan is signaling a more aggressive policy stance, creating a clear divergence with the Fed. This makes shorting the USD/JPY pair an attractive strategy, as a dovish Fed paired with a hawkish BoJ supports this move. Traders could consider buying put options on USD/JPY to potentially profit from downward movement while managing risk. Gold is currently retreating, but we should see this in light of its rise above $4,300, which reflects ongoing inflation and geopolitical risks over the past two years. A weak jobs report would be bullish for gold, as it would likely weaken the dollar and lower real interest rates. Any price dips ahead of the data could be a good opportunity to position for a rise. The most important factor will be the deviation from the 40k expectation, as this will shape the market’s immediate response. A surprise figure that significantly exceeds this number could trigger a swift short squeeze on the dollar, catching many traders off guard. Thus, using defined-risk options strategies is wise to guard against unexpected outcomes. Create your live VT Markets account and start trading now.GBP/USD falls ahead of UK employment data, with unemployment rate expected to rise to 5.1%

The UK Office for National Statistics will release its labour market report at 07:00 GMT. The UK ILO Unemployment Rate is expected to rise slightly to 5.1% in October, up from 5.0% the month before. In September, there was a drop of 22,000 in Employment Change. November’s Claimant Count Change is anticipated to increase by 22,300 from October’s figure of 29,000, while the Claimant Count Rate is likely to remain at 4.4%.

GBP/USD is trading lower ahead of the UK’s labour market data. Traders are cautious because of upcoming US economic reports, including Nonfarm Payrolls, Retail Sales, and the Purchasing Managers Index, scheduled for release on Tuesday. If the US data is better than expected, it could lift the Pound Sterling, pushing it towards the 1.3400 psychological level. Initial resistance is at 1.3438, followed by 1.3471.

Stabilized Trading Range

The GBP/USD pair is stable, trading within the 1.3370-1.3365 range as traders await important economic releases. Key UK inflation data on Wednesday and the Bank of England’s policy decision on Thursday will be vital for the Pound. Additionally, US consumer inflation figures on Thursday will significantly impact GBP/USD’s short-term trajectory. Risk aversion has limited GBP/USD’s gains, with expectations of a BoE rate cut on Thursday. The market has almost fully priced in a 25-basis point rate cut, with another cut expected by mid-2026. This morning, the Pound is trading cautiously as the latest labour market data surfaces from the Office for National Statistics. The UK unemployment rate for November has just been reported at 4.5%, a slight rise from October’s 4.3%. This reinforces a cautious market mood. A weaker jobs report increases the likelihood that the central bank might need to take action soon. The current sideways movement of GBP/USD around the 1.3370 mark indicates that traders are waiting for a clear signal before making significant moves. Similar quiet periods in late 2023 were often interrupted by sharp movements as major economic data were released. This could make buying options, which benefit from increased volatility, an appealing strategy ahead of Thursday’s Bank of England decision.Monetary Policy Divergence

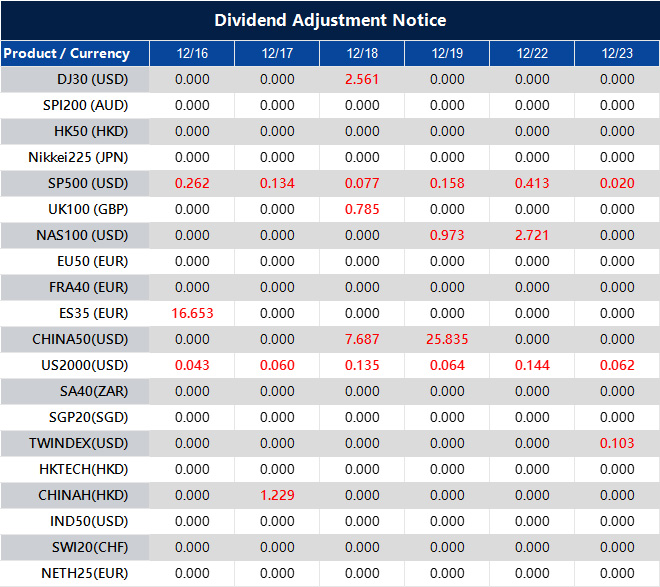

A major factor affecting the Pound is the growing gap between central bank policies. The market is now pricing in over an 85% chance of a 25-basis point rate cut by the Bank of England this week. This move is primarily a response to recent UK inflation data, which has cooled to 2.4%, closer to the bank’s target than the higher 3.1% inflation rate in the United States. This divergence is likely to limit the Pound’s strength against the dollar. Considering the potential for a rate cut, we are monitoring the 1.3400 level as a significant resistance point that may hold firm. Derivative traders with long positions might think about hedging by purchasing put options with a strike price below 1.3350 to guard against a negative response to the Bank of England’s announcement. A drop below the mid-1.3300s support could lead to a slide toward 1.3200. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Dec 16 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].