This week’s macro landscape is defined by a tension between easing headline inflation and persistent core price pressures.

US CPI for January slowed to 2.4% year on year, coming in below the 2.5% forecast and down from 2.7% in December. Softer energy costs, particularly lower petrol prices, contributed to the decline in the headline figure.

Beneath the surface, however, inflation remains less reassuring. The Federal Reserve’s preferred measure, December’s PCE index, stands at 2.9% year on year, with core PCE at 3.0%. Services inflation and other essential costs continue to run firm, keeping policymakers cautious about easing policy prematurely.

Labour market data paints a similarly mixed picture. January Non-Farm Payrolls rose by 130,000, comfortably above expectations of around 70,000 and significantly higher than December’s revised 48,000 reading.

At the same time, earlier benchmark revisions showed that employment figures throughout 2025 had been overstated, aligning with VT Markets’ research highlighting a gradual softening in the jobs market.

Minutes from the Fed and recent official commentary underscore a guarded approach. Policymakers describe progress towards the 2% inflation target as uneven and emphasise that any rate reductions will remain data-dependent, while some still point to the possibility of further tightening should inflation stall.

Fed funds futures and FedWatch indicators now imply a strong likelihood of rates remaining unchanged through the March meeting, with markets increasingly anticipating the first cut around mid-2026 rather than earlier in the year.

The Tariff Twist

A significant development followed the US Supreme Court’s ruling that the authority to impose broad-based tariffs lies with Congress rather than the President.

The judgment removes a key executive policy instrument and could result in approximately $160 billion in refunds to importers.

For financial markets, this development carries two primary implications:

1. USDX impact: The unwinding of tariff-related inflows may weigh on the dollar if importers reverse earlier currency hedges.

2. S&P 500 effect: Reduced effective import costs could help stabilise corporate margins and support forward earnings expectations.

Nonetheless, the White House is reportedly considering a 150-day Emergency Surcharge as an interim measure. Market participants will be monitoring whether such a proposal withstands legal scrutiny.

Escalating US–Iran Tensions And The Geneva Deadline

Washington has issued a 48-hour ultimatum to Iran, demanding agreement to a revised framework ahead of Thursday’s meeting in Geneva.

The US has deployed carrier groups to the region. Although Iran has stated it will not capitulate, diplomatic discussions have not formally collapsed.

This development carries direct implications for XAUUSD and crude markets:

1. Heightened geopolitical risk tends to bolster safe-haven demand, supporting XAUUSD above the 5,000 level.

2. A breakdown in negotiations could prompt traders to price in a spike in oil and generate short-term strength in USDX.

Market Movements Of The Week

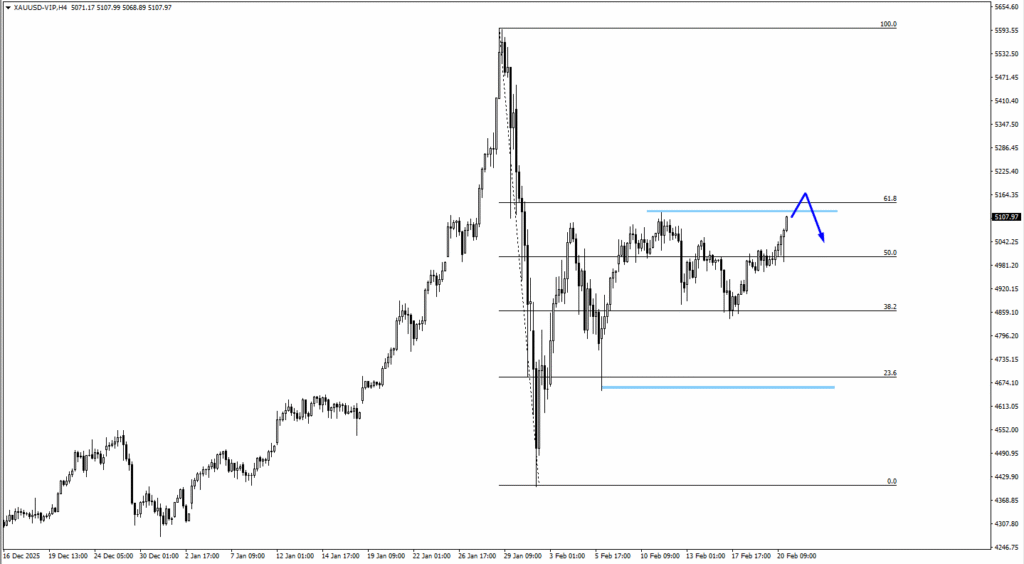

Gold (XAUUSD)

– XAUUSD climbed to around $5,170 in early Asian trading on Monday, approaching 61.8% Fibonacci resistance at 5164.35.

– 5164.35 remains a key rejection zone, with 4981.20 acting as 50% support.

– Catalyst: Fed rate cut expectations and upcoming US inflation data.

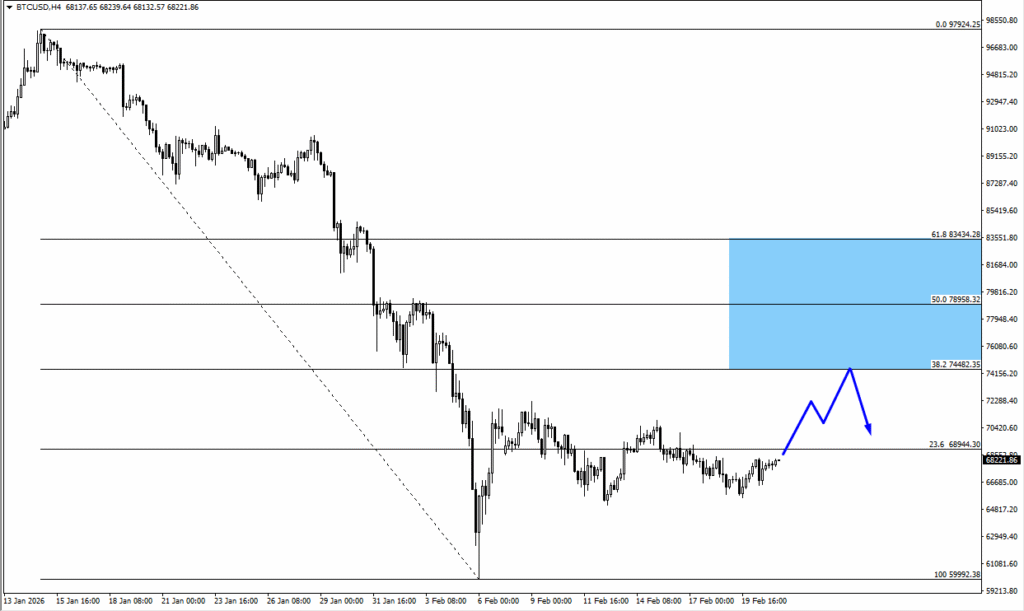

Bitcoin (BTCUSD)

– BTCUSD rejected $65,000 and stabilised near $62,000.

– $59,500 support is critical for the structure.

– Catalyst: US inflation and SP500 reaction.

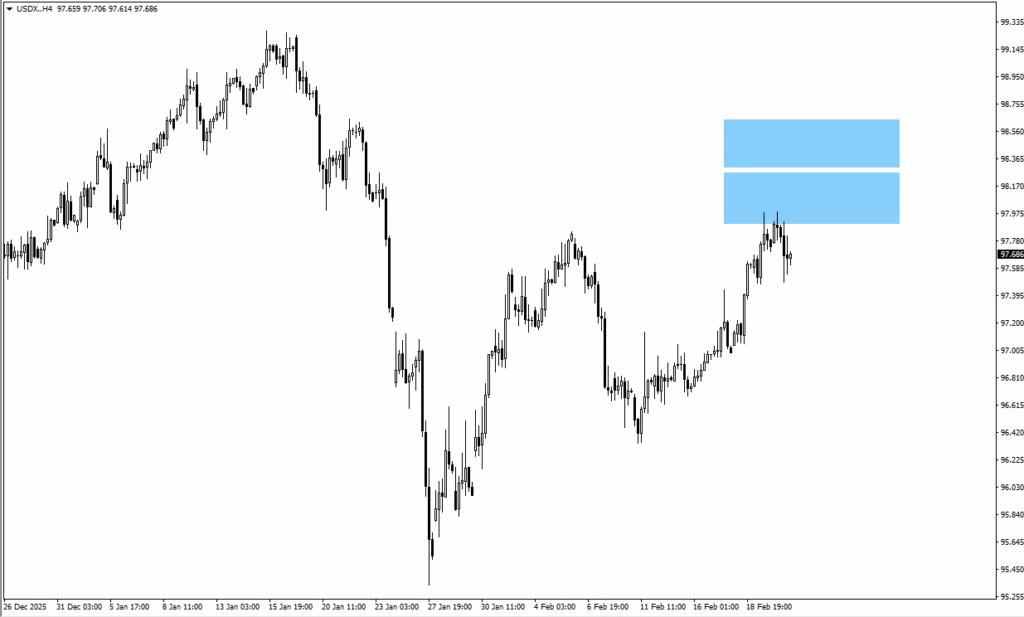

US Dollar Index (USDX)

– USDX testing 98.10 resistance zone.

– 98.65 breakout shifts momentum bullish.

– Catalyst: Fed rate cut expectations and PPI.

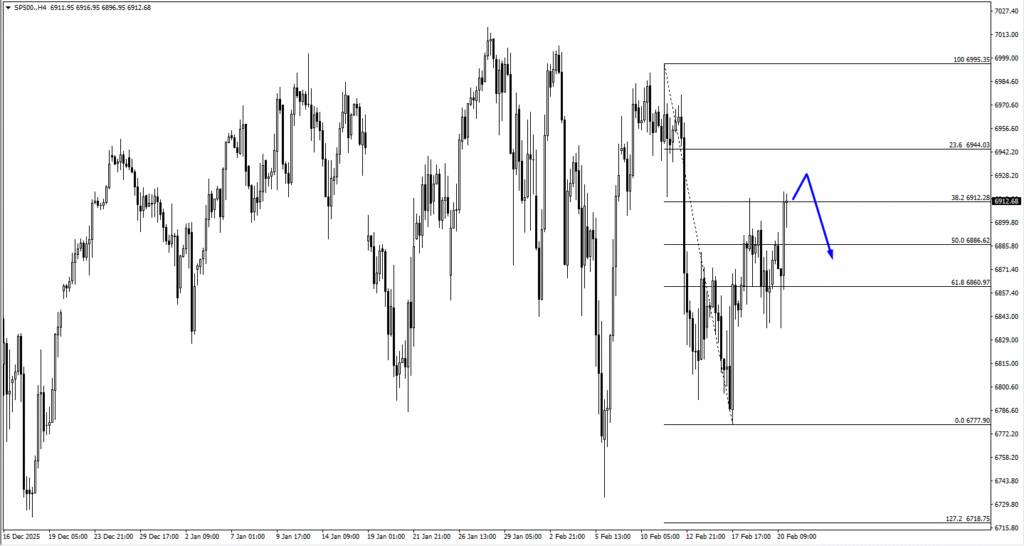

SP500

– SP500 is trading around 6,912, which aligns exactly with the 38.2% retracement.

– Immediate resistance sits at 6,944 at the 23.6% retracement, where sellers may react.

– Deeper support sits at 6,860, which is the 61.8% retracement zone.

Key Events This Week

26 February 2026

1. US – Iran Talks Geneva

Expect gold and oil volatility.

27 February 2026

1. US PPI m/m, Forecast: 0.30%, Previous: 0.50%

Direct input for Fed rate cut expectations.

Bottom Line

Gold begins the week pressing against the 61.8% Fibonacci resistance level at 5164.35, with XAUUSD trading just below this critical threshold. The next directional move is likely to hinge on evolving expectations around Fed rate cuts and incoming US inflation data.

With US PPI figures and additional labour data due, markets are reassessing the timing of the initial Fed rate reduction. Should inflation continue to moderate, XAUUSD may extend its rebound.

Conversely, if price pressures re-emerge, the dollar could strengthen and restrain further gains in gold. The coming week will centre on whether conviction builds around rate cut expectations or whether the narrative undergoes another adjustment.