Daylight savings will take place in the US on 9 March 2025, with clocks moving forward by one hour. This change affects the opening and closing times of US markets, which will occur an hour earlier.

Discussions around the persistence of daylight savings have been noted, with comments indicating that it is unlikely to be abolished. Adjustments for daylight savings have not yet been implemented in Europe and Australia.

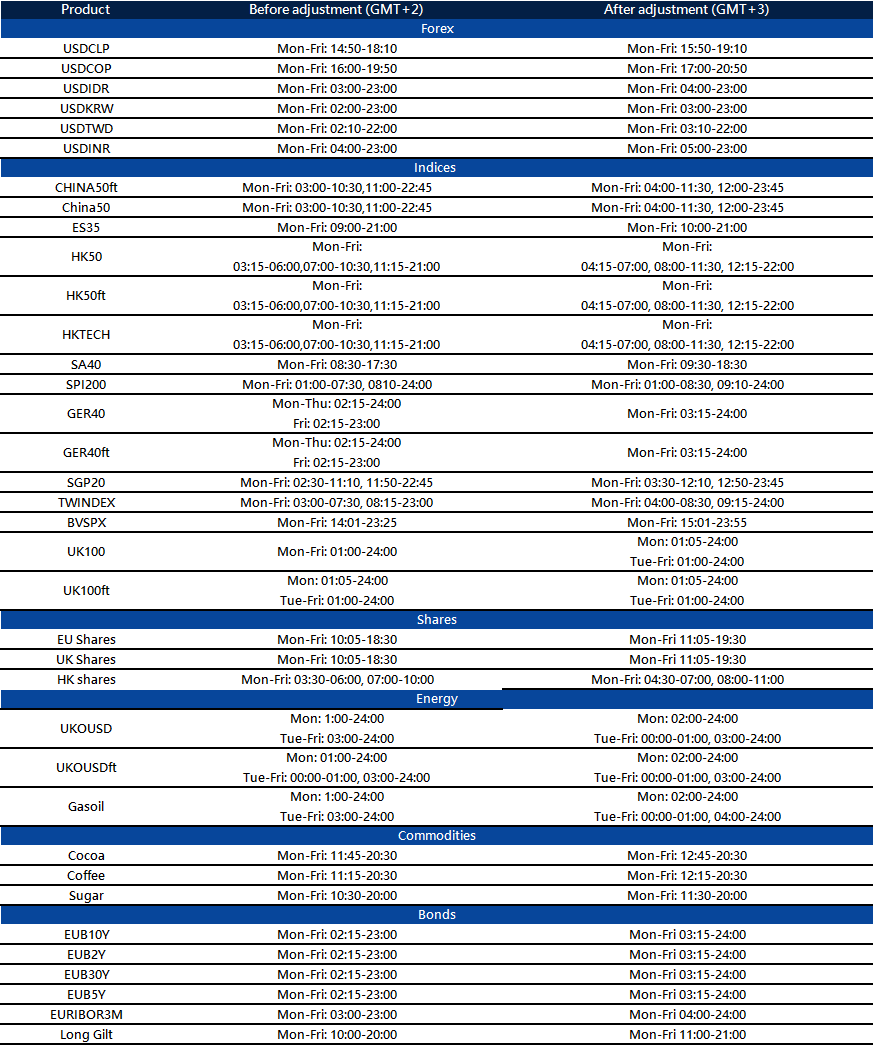

Trading Hour Adjustments

That means trading hours for key exchanges in the United States will shift forward by sixty minutes. Any trading strategies that depend on specific times must reflect this adjustment.

We have seen ongoing debates about whether to remove daylight savings altogether, but so far, no decisive action has been taken. Lawmakers have brought it up, yet nothing concrete has come of it. This means the time adjustment is here to stay for the foreseeable future.

Meanwhile, markets in Europe and Australia will maintain their existing hours until they apply their own time changes. This temporary imbalance affects those with holdings across multiple regions, particularly strategies that rely on overlapping trade windows. For a few weeks, those who engage with European or Australian markets will see altered gaps between session openings and closings. Liquidity levels during these hours may shift, and traders need to be aware of how this could impact pricing.

Market participants relying on automated systems must confirm whether their platforms account for this shift. Any discrepancies in execution times could lead to unexpected fills or delays. Human oversight remains necessary, even for those who operate primarily through algorithmic models.

Market Volatility Considerations

Beyond timing changes, historical data suggests price behaviours sometimes show short-term shifts around daylight savings adjustments. Volatility patterns in the first few sessions after the switch may not align with previous weeks. We have observed volume fluctuations as global participants adapt. Some traders may step back briefly, while others take advantage of the altered flow.

Europe’s own clock adjustment is scheduled for 30 March 2025, restoring prior market alignments. Until then, those trading across both regions must accommodate the temporary disconnect. Australia’s change happens separately, adding another layer for those engaged in those markets.

Every year, certain participants underestimate the implications of this shift. Some orders are placed based on outdated time assumptions, leading to missed trades or unforeseen exposure. Those who ensure their schedules are aligned with the new trading hours will avoid these mistakes. It is not just about knowing when opening bells ring but also about understanding how liquidity and momentum respond in the following sessions.

{kind=link}