As we step into the week commencing March 4th, anticipation fills the financial sphere for a flurry of significant economic disclosures. Investors and policymakers alike brace themselves for a cascade of reports set to influence the Federal Reserve’s trajectory leading up to the forthcoming FOMC meeting on March 19-20. All eyes are fixed on Federal Reserve Chair Jerome Powell’s semiannual monetary policy testimony before the House Financial Services and Senate Banking Committees, a session historically known as the Humphrey-Hawkins testimony, promising to command considerable attention.

This testimony is eagerly awaited for any signals indicating shifts in the Federal Reserve’s monetary policy stance. In an environment where the Federal Reserve maintains a firm grip on the federal funds target rate range of 5.25-5.50 percent to rein in inflation and ensure price stability, Powell’s remarks will be scrutinized for any hints of policy adjustments. Despite strides made in controlling inflation, the Fed’s dual mandate urges caution in loosening monetary policy, particularly with the tight labor market’s potential to spur wage inflation.

Against expectations of tempered economic growth, the imminent Beige Book release holds the promise of offering invaluable anecdotal evidence on economic conditions across the 12 Districts. While recent data suggest a resilient US economy buoyed by robust consumer spending and a strong labor market, striking a balance between nurturing growth and preventing inflation remains a nuanced challenge.

This week also heralds the arrival of the monthly employment report for February, with analysts projecting a slight moderation in nonfarm payroll growth, yet underscoring the enduring strength of the labor market fundamentals. As businesses grapple with recruitment hurdles, the interplay between job vacancies, wage pressures, and inflation dynamics assumes critical significance for market strategies.

For forex traders and market analysts at VT Markets, these unfolding events carry paramount importance. The impending economic indicators and Powell’s testimony not only provide insights into the US economic outlook but also wield significant implications for currency markets and trading strategies. As we embark on this pivotal week, remaining informed and adaptable will be imperative for navigating the evolving market landscape.

Key Takeaways:

Fed Chair Jerome Powell’s testimony could offer new insights into the Federal Reserve’s monetary policy direction.

The Beige Book and the monthly employment report will provide further clarity on the US economic health and labor market dynamics.

Market participants should remain vigilant, adapting their strategies in response to the unfolding economic indicators and central bank policies.

Stay connected with VT Markets for real-time analysis and insights on how these developments impact the forex market and trading opportunities.

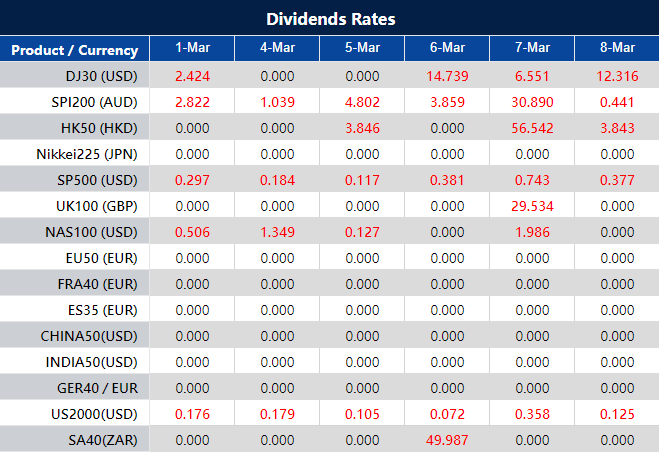

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Thursday, the Nasdaq Composite achieved a record close at 16,091.92, its highest since November 2021, driven by a surge in tech stocks, particularly those involved in artificial intelligence. This uplift in the stock market saw the S&P 500 also reaching new heights, alongside modest gains for the Dow Jones, marking a continuation of Wall Street’s positive trend into its fourth consecutive month. The enthusiasm around AI and major tech companies has played a pivotal role in this rally, overshadowing concerns about inflation and economic slowdown. Meanwhile, in the currency market, the US Dollar Index saw an upward movement, influencing major currency pairs and setting the stage for watchful anticipation of upcoming economic data and central bank communications. This complex financial landscape, highlighted by tech stock surges and currency fluctuations, encapsulates the dynamic interplay between equity markets and global economic indicators.

Stock Market Updates

On Thursday, the Nasdaq Composite surged to a record close, marking its first since November 2021, by advancing 0.90% to finish at an all-time high of 16,091.92. This rise was significantly buoyed by a rally in tech stocks and chips. The S&P 500 also reached a new record, increasing by 0.52% to end at 5,096.27, while the Dow Jones Industrial Average saw a modest gain of 0.12%, closing at 38,996.39. This upward movement in the stock market concluded February trading on a high note, extending Wall Street’s positive momentum into a fourth consecutive month, despite concerns over the durability of the AI-fueled rally. The Nasdaq led with a 6.12% gain for the month, followed by the S&P 500 with a 5.17% increase, and the Dow with a 2.22% rise, marking its first four-month winning streak since May 2021.

The resurgence of the Nasdaq has been particularly fueled by a wave of enthusiasm for artificial intelligence, significantly lifting major tech stocks, referred to as the “Magnificent 7” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla), and subsequently, the broader markets throughout 2023 and into this year. This rally comes after a challenging 2022 characterized by worries over rising interest rates and recession fears. In the specifics of the day’s trading, notable performers included Advanced Micro Devices, which saw a jump of more than 9%, and the VanEck Semiconductor ETF, which closed 2.2% higher. Despite the Federal Reserve’s preferred inflation measure remaining above target in January, it did not exceed Wall Street forecasts, suggesting that consumer spending remains strong. Additionally, while there were setbacks, such as Snowflake’s share drop following the announcement of its CEO’s retirement and disappointing revenue guidance, Okta experienced a significant rise of nearly 23% after reporting strong results.

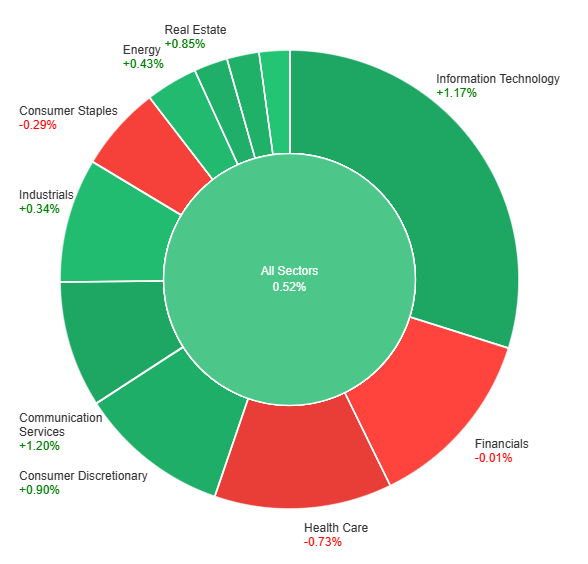

On Thursday, the stock market witnessed a positive overall performance with all sectors combined showing a gain of +0.52%. Leading the gains were Communication Services and Information Technology, up by +1.20% and +1.17% respectively, demonstrating strong investor confidence in these sectors. Other sectors such as Consumer Discretionary, Real Estate, and Materials also posted notable increases, ranging from +0.79% to +0.90%. However, not all sectors fared as well; Utilities showed minimal growth at +0.04%, while Financials slightly declined by -0.01%. The Consumer Staples and healthcare sectors faced downturns, decreasing by -0.29% and -0.73% respectively, indicating areas of investor concern or profit-taking.

Currency Market Updates

The currency market experienced notable movements, with the USD Index (DXY) advancing above the 104.00 barrier, marking its third consecutive session of gains. This strength in the US Dollar influenced various currency pairs, notably pushing the EUR/USD pair to challenge the key support level at 1.0800. The anticipation of economic data releases, including the final S&P Global Manufacturing PMI, Construction Spending, and the ISM Manufacturing PMI, alongside speeches from several Federal Reserve officials, seems to underpin the dollar’s momentum. Furthermore, the currency market is keenly awaiting inflation figures from the euro area, alongside unemployment and manufacturing data, which could influence the EUR/USD trajectory in the coming sessions.

On the other side of the spectrum, the GBP/USD pair faced downward pressure, hinting at a potential move towards the 1.2600 region, influenced by a stronger dollar and upcoming economic releases from the UK. Meanwhile, the USD/JPY pair saw a decline to the 149.20 area, reacting to market speculations about a potential policy shift by the Bank of Japan. The AUD/USD pair also succumbed to the dollar’s strength, breaking below the 0.6500 support level amid concerns over China and forthcoming economic data from Australia. Additionally, the market focus is shifting toward China with the upcoming Manufacturing PMIs, which could have significant implications for the global currency markets, highlighted by a slight drop in the USD/CNH pair to the 7.2100 zone. Amidst these currency shifts, commodities such as WTI oil and precious metals like gold and silver displayed varied performances, adding another layer of complexity to the global financial landscape.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Dips Amidst USD Rebound and Rate Cut Speculations

The EUR/USD pair has seen a downturn for the third consecutive session, touching the 1.0800 level as the US Dollar gains strength, driven by renewed interest from investors. This movement is in sync with the rising US Dollar Index (DXY), surpassing the 104.00 mark, despite a drop in US yields. The Dollar’s resurgence, after a brief dip following US PCE data indicating disinflation, was bolstered by Atlanta Fed President Raphael Bostic’s remarks on the stubborn path to the 2% inflation target and the potential for a policy rate reduction in the summer. Concurrently, both US and German bond yields experienced a decline amid anticipations of a Federal Reserve rate cut, possibly in June, with a 52% probability as forecasted by the CME Group’s FedWatch Tool. This is paralleled by the ECB’s openness to initiating its easing cycle, hinted at for a June start by board member Peter Kazimir, amidst signs of waning inflation in Germany and ahead of crucial CPI data for the eurozone that could influence ECB rate cut timings.

On Thursday, the EUR/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price is moving below the middle band, suggesting a potential upward movement to reach above the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 47, signaling a neutral outlook for this currency pair.

Resistance: 1.0832, 1.0858

Support: 1.0812, 1.0783

XAU/USD (4 Hours)

XAU/USD Surge Amid Disinflation Confirmation and Rate Cut Speculation

Following the release of the Core Personal Consumption Expenditure (PCE) Price Index, which met expectations and indicated ongoing disinflation, gold prices experienced a significant increase of over 0.50% during Thursday’s North American trading session. This data release led to a decrease in US Treasury bond yields, inversely benefiting the price of gold, propelling XAU/USD to $2,046. The anticipation of the Core PCE report, showing a year-on-year deceleration in inflation for January, alongside a sharp decline in headline inflation, fueled expectations of potential rate cuts by the Federal Reserve. Market predictions, influenced by the CME FedWatch Tool, now foresee a higher likelihood of a rate cut by June, contributing to the bullish momentum in gold prices amidst a broader analysis of economic indicators such as Initial Jobless Claims and Pending Home Sales.

On Thursday, XAU/USD moved higher to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential higher movement to reach above the upper band and reach the resistance level. The Relative Strength Index (RSI) stands at 63, signaling a bullish outlook for this pair.

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

Saturday, 2nd March 2024, 02:00 (GMT+2) – Sunday, 3rd March 2024, 24:00 (GMT+2)

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed. If you don’t want to hold any open positions during the maintenance, it is suggested to close the position in advance.

3. Following the maintenance, it is important to note that the minimum supported version of MT5 will be 4047. Please ensure that your MT5 version is above 4047 to maintain smooth operation. The latest version of MT5 can be downloaded from our official website by navigating to “Trading” → “MetaTrader 5”.

4. The MT4 server remains unaffected by this maintenance and will continue to facilitate transactions without interruption. Please refer to MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on February 29, 2024 at 10:35 am, by anakin

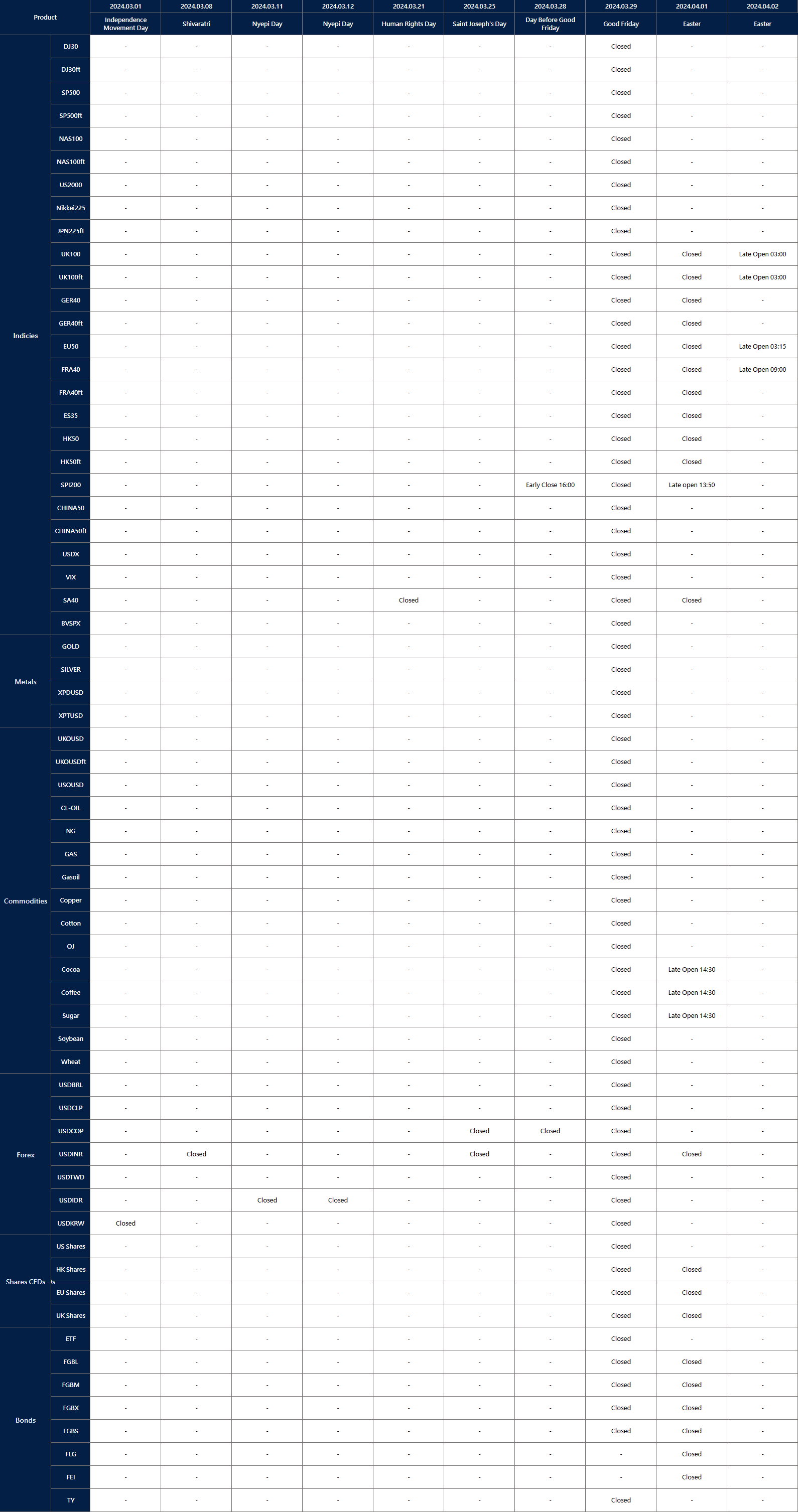

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the remaining affected products:

Note: The dash sign (-) indicates normal trading hours.

Friendly Reminder:

1. The above data is for reference only, please refer to the MT4/MT5 software for specific data.

2. VT Markets’ MT4/MT5 server time is scheduled to be adjusted from GMT+2 to GMT+3 on 10th March, in alignment with the upcoming daylight saving time. We kindly advise all clients to be aware of the forthcoming announcements for further details regarding specific adjustments.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on February 29, 2024 at 9:28 am, by anakin

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on February 29, 2024 at 9:02 am, by anakin

On Wednesday, stocks saw a decline as investors awaited an important inflation report due later in the week, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all experiencing losses. Notable decliners included UnitedHealth, Intel, Alphabet, and Urban Outfitters, the latter due to disappointing quarterly results. The market’s attention is now on January’s forthcoming personal consumption expenditure (PCE) data, a crucial inflation indicator for the Federal Reserve. This anticipation comes amid mixed movements in the currency market, where the dollar index made slight gains while investors closely monitor upcoming inflation reports from the U.S. and the eurozone. These reports are pivotal for future monetary policy and interest rate expectations, especially with predictions leaning towards rate cuts by the Federal Reserve and the European Central Bank (ECB) within the year, amidst contrasting inflationary trends in the U.S. and eurozone.

Stock Market Updates

Stocks experienced a decline on Wednesday as the market anticipated an important inflation report set to be released later in the week. The S&P 500 dropped slightly by 0.17%, closing at 5,069.76, while the Nasdaq Composite experienced a more significant fall of 0.55%, ending at 15,947.74. The Dow Jones Industrial Average also saw a minor decrease, losing 23.39 points, or 0.06%, to close at 38,949.02, marking its third consecutive day of losses. Among the notable decliners were UnitedHealth, which fell nearly 3%, and tech giants Intel and Alphabet, which dropped 1.7% and 1.8%, respectively. Additionally, Urban Outfitters saw a significant decrease of 12.8% following its announcement of weaker-than-expected fourth-quarter results.

The market’s focus is now on the upcoming personal consumption expenditure reading for January, a critical inflation measure closely watched by the Federal Reserve. This report is highly anticipated as investors and analysts gauge the potential for continued economic growth and the impact of inflation on monetary policy. The market’s recent performance has been less robust, with the major indexes on track for their second negative week in the last three, despite having reached record highs recently. The downturn, especially in the tech sector, has sparked debates about the durability of the market rally, which has been partly driven by enthusiasm over advancements in artificial intelligence.

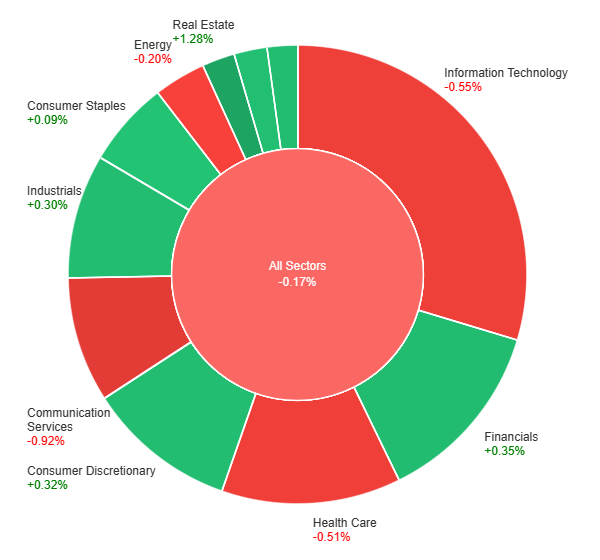

On Wednesday, the overall market experienced a slight downturn, with all sectors combined seeing a decrease of 0.17%. Despite this general downtrend, several sectors managed to post gains, led by Real Estate, which saw a notable increase of 1.28%. Other sectors that experienced growth included Financials, Consumer Discretionary, Utilities, Industrials, Materials, and Consumer Staples, with increases ranging from 0.09% to 0.35%. On the flip side, some sectors faced declines, with Energy, Health Care, Information Technology, and Communication Services witnessing drops between -0.20% and -0.92%, indicating a mixed performance across different areas of the market.

Currency Market Updates

The currency market is currently experiencing nuanced movements as investors anxiously await inflation reports from the U.S. and eurozone, which could significantly influence the trajectory of risk-sensitive currencies. The dollar index saw a slight increase of 0.1%, though it retreated from its early Wednesday highs, indicating a cautious stance among traders. The EUR/USD pair dipped marginally by 0.05%, recovering after testing key support levels amid a broad-based rise in the dollar earlier in the day. The focus now shifts to Thursday’s release of the U.S. core PCE and eurozone CPI reports, which are expected to play a critical role in determining whether the recent reduction in anticipated Fed rate cuts for 2024—and the consequent support this has lent to the dollar—will continue or come to a halt.

Market expectations are leaning towards the Federal Reserve beginning to cut rates by June, with a total of 81 basis points of easing anticipated by the end of the year. Similarly, a June rate cut by the ECB is fully priced in, with expectations of 90 basis points of cuts throughout the year. These developments come as core PCE in the U.S. is forecasted to rise, contrasting with December’s figures, and with the euro zone’s overall and core CPI also set for release, offering further insights into inflationary trends. Amidst this backdrop, the USD/JPY pair has seen a slight increase, attempting to continue its upward trend as markets digest varying signals from Fed speakers and global economic indicators, highlighting the interconnectedness of global financial markets and the significant impact of central bank policies and economic data on currency valuations.

The EUR/USD pair experienced a decline early Friday, pressured by disappointing sentiment indicators from Europe and a significant disparity in US GDP figures that maintained the currency pair’s position within a familiar range midweek. With a packed schedule, Thursday’s focus shifts to German Retail Sales and CPI data, alongside the US Personal Consumption Expenditure (PCE) Price Index inflation figures. The week will conclude with Friday’s release of the pan-European Harmonized Index of Consumer Prices (HICP) inflation data and the US ISM Manufacturing PMI for February, providing critical insights into economic health and potential currency movement directions.

On Wednesday, the EUR/USD moved slightly lower and was able to reach the lower band of the Bollinger Bands. Currently, the price is moving just below the middle band, suggesting a potential upward movement to reach above the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 51, signaling a neutral outlook for this currency pair.

Resistance: 1.0858, 1.0896

Support: 1.0823, 1.0783

XAU/USD (4 Hours)

XAU/USD Steady Amid Economic Expansion and Fed Remarks

Gold prices remained stable near $2,030 on Wednesday, achieving a modest increase of 0.17% as the US economy showed signs of expansion according to the latest BEA report. Despite the US GDP for the last quarter of 2023 slightly missing expectations and mixed retail and wholesale inventory data, a fall in US Treasury bond yields has supported gold prices, keeping them near monthly and weekly highs, just below the 50-day SMA. Meanwhile, comments from Federal Reserve Regional Presidents, Susan Collins and John Williams, about potentially easing policy later in the year while still not meeting the core inflation goal of 2%, have influenced market sentiment, alongside a cautious Wall Street trading mostly in the red.

On Wednesday, XAU/USD moved slightly higher to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential higher movement to reach above the upper band and reach the resistance level. The Relative Strength Index (RSI) stands at 57, signaling a neutral but bullish outlook for this pair.

Resistance: $2,042, $2,056

Support: $2,030, $2,017

Economic Data

Currency

Data

Time (GMT+8)

Forecast

EUR

German Prelim CPI m/m

All day

0.5%

CAD

GDP m/m

09:30

0.2%

USD

Core PCE Price Index m/m

09:30

0.4%

USD

Unemployment Claims

09:30

209K

Written on February 29, 2024 at 4:12 am, by anakin

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on February 28, 2024 at 8:01 am, by anakin

On Tuesday, the stock market displayed mixed outcomes with the S&P 500 and Nasdaq Composite experiencing slight gains, while the Dow Jones Industrial Average faced a minor decline amidst anticipation for upcoming inflation data. Corporate earnings, particularly from Macy’s and Lowe’s, alongside economic indicators, played significant roles in market dynamics. Meanwhile, the currency market witnessed subtle shifts, with the Japanese yen strengthening against the dollar following Japan’s higher-than-expected core CPI report. Investor focus remains on key economic releases, including the personal consumption expenditure price index, with global monetary policy expectations influencing market sentiment.

Stock Market Updates

On Tuesday, the stock market saw mixed results as investors awaited crucial inflation data expected later in the week. The S&P 500 edged up by 0.17% to 5,078.18, while the Nasdaq Composite saw a modest increase of 0.37%, closing at 16,035.30. Contrarily, the Dow Jones Industrial Average experienced a slight downturn, dropping by 96.82 points, or 0.25%, to end at 38,972.41. Notable movements included Macy’s, which surged 3.4% after announcing plans to close approximately 150 underperforming stores due to a previous revenue shortfall. Additionally, Lowe’s shares increased by 1.7% following an earnings beat, with Zoom Video and Hims & Hers Health also making significant gains after surpassing Wall Street’s earnings expectations.

A mix of corporate earnings reports and economic indicators influenced the market’s dynamics. The utilities sector led the market with a 1.9% increase, while the communications services and technology sectors also saw gains. This activity followed a decline from record highs the previous week, spurred by Nvidia’s impressive earnings. Moreover, investor sentiment was affected by a drop in consumer confidence amid concerns over a potential labor market slowdown and a divisive political climate, as reported by the Conference Board. Additionally, a decrease in orders for long-lasting goods in January, particularly in transportation, underscored these economic uncertainties. As investors look ahead, the forthcoming release of the personal consumption expenditure price index and personal income data will be closely scrutinized for insights into economic health and monetary policy direction.

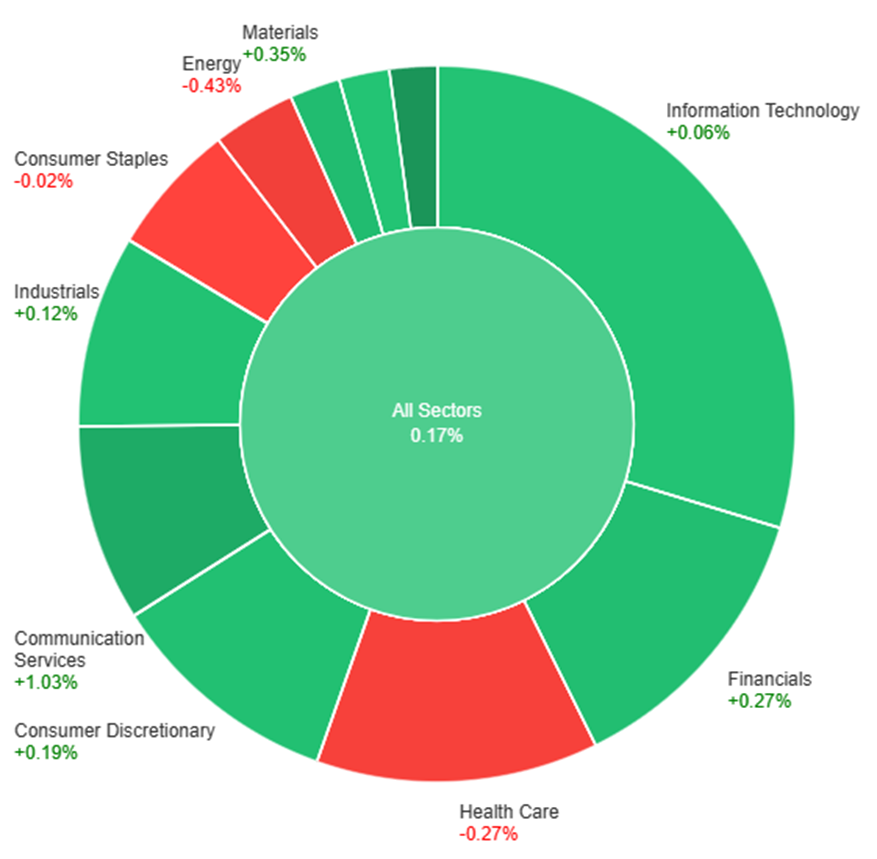

On Tuesdayday, the overall market saw modest gains, with all sectors collectively up by 0.17%. Utilities led the performance with a significant increase of 1.89%, followed by Communication Services and Materials, which rose by 1.03% and 0.35%, respectively. Financials, Consumer Discretionary, and Industrials also experienced gains, though more modest, ranging from 0.12% to 0.27%. Information Technology and Real Estate sectors saw minimal increases, whereas Consumer Staples, Health Care, and Energy sectors faced declines, with Energy recording the largest drop at -0.43%.

Currency Market Updates

The currency market saw nuanced movements with the dollar index slightly declining by 0.09%, influenced by a mix of supportive corporate month-end flows and weaker-than-expected U.S. economic data concerning durable goods and consumer confidence. The Japanese yen emerged as a notable performer, appreciating following a report that showed Japan’s core CPI rising above forecasts. This development came amidst static policy pricing from major central banks such as the Federal Reserve, European Central Bank, and the Bank of Japan, with the market participants keenly awaiting further key data releases scheduled for later in the week and the next.

The FX landscape was further characterized by the lingering weakness of the USD against the JPY, spurred by Japan’s inflation data, while the EUR/USD, GBP/USD, and other major currency pairs saw marginal gains. Despite some reasons to overlook the disappointing U.S. durable goods data, attributed partly to Boeing’s challenges, the misses in economic reports have heightened the anticipation for upcoming releases on core PCE, income, spending, and employment data. Market speculation regarding the Federal Reserve’s interest rate path remains a focal point, especially after Kansas City Fed President Jeffrey Schmid’s hawkish remarks, contrasting with the market’s reduced expectations for Fed rate cuts. The evolving monetary policy expectations for the ECB, BoE, and BoJ also play a critical role in shaping the currency market dynamics, with all eyes on the upcoming eurozone CPI and U.S. core PCE data to gauge potential shifts in monetary policy and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Stabilizes Amid Anticipation of Key Economic Data

The EUR/USD pair has been hovering around the 1.0850 mark, showing little movement as traders await impactful economic releases. Following a more significant than expected decline in US Durable Goods Orders for January, market focus now shifts to upcoming US GDP figures, German Retail Sales, CPI data, and the US PCE inflation report. These forthcoming data points are crucial for gauging the economic health of both regions and could potentially influence the currency pair’s direction.

On Tuesday, the EUR/USD moved slightly lower and was able to reach the middle band of the Bollinger Bands. Currently, the price is moving around the middle band, suggesting a potential downward movement to reach below the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 53, signaling a neutral outlook for this currency pair.

Resistance: 1.0858, 1.0896

Support: 1.0823, 1.0783

XAU/USD (4 Hours)

XAU/USD See Modest Gains Amid Weakening Dollar and Anticipation for Key Economic Reports

Gold (XAU/USD) experienced a slight increase in its price during Tuesday’s mid-North American session, trading at $2,034.88, a 0.18% gain, amid a backdrop of falling US Treasury bond yields and a weakening US Dollar, as indicated by a 0.05% drop in the US Dollar Index (DXY). This modest uptick occurs as the precious metal hovers around the 50-day Simple Moving Average, with investors keenly awaiting the Personal Consumption Expenditures (PCE) report and latest Gross Domestic Product (GDP) data, which are anticipated to be significant factors that could drive Gold out of its current $2,020-$2,050 trading range. The outlook is further clouded by the recent report on Durable Goods Orders for January, which fell more sharply than expected, and mixed Home Prices data, suggesting a potentially volatile period ahead for Gold prices.

On Tuesday, XAU/USD moved lower to reach the middle band of the Bollinger Bands. Currently, the price is moving just above the middle band, suggesting a potential consolidation movement. The Relative Strength Index (RSI) stands at 53, signaling a neutral outlook for this pair.

Resistance: $2,042, $2,056

Support: $2,030, $2,017

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

AUD

CPI y/y

08:30

3.4% (Actual)

NZD

Official Cash Rate

09:00

5.50% (Actual)

NZD

RBNZ Monetary Policy Statement

09:00

NZD

RBNZ Rate Statement

09:00

USD

Prelim GDP q/q

21:30

3.3%

Written on February 28, 2024 at 2:48 am, by anakin

{kind=link}