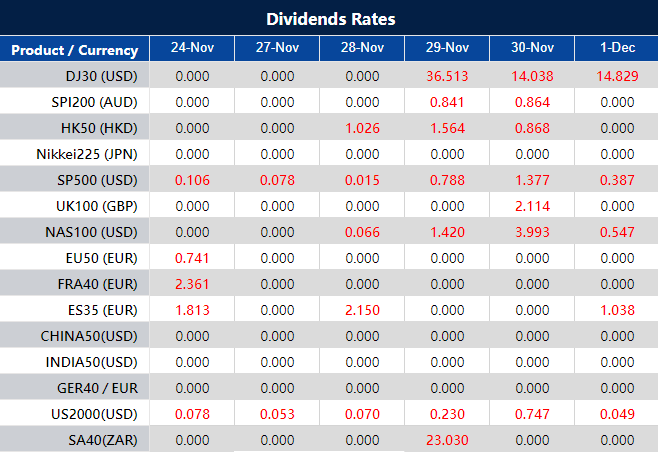

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on November 24, 2023 at 7:17 am, by anakin

European stocks showed a cautious upward trend as the US markets remained closed, with the Stoxx 600 index edging up by 0.3%. Despite oil price falls from the postponed OPEC meeting, oil and gas stocks surged while travel stocks faced a decline. Eurozone’s PMI data revealed worrying employment drops, yet signs of a slowing decline in business activity emerged. Meanwhile, attention shifted to the Dutch election’s potential impact. In the US, the Thanksgiving holiday bolstered positive sentiment despite a modest dollar decline. Wall Street futures mirrored gains in European markets, while attention shifted to S&P Global PMI projections amid a lack of major US releases. Currencies like the Euro and Pound remained steady against the dollar, driven by encouraging PMI data, while others, including the Aussie and Kiwi Dollars, saw mixed movements influenced by domestic indicators and market sentiments.

Stock Market Updates

With the US markets closed, European stocks closed slightly higher on Thursday. The pan-European Stoxx 600 index edged up by 0.3%, showcasing a cautious upward trend amidst investor uncertainty. Despite the ongoing fall in oil prices stemming from OPEC’s postponed meeting, oil and gas stocks surged by 1.4%, countering the downward pressure. However, travel stocks faced a contrasting fate, experiencing a 1% decline. The preliminary purchasing managers’ index data for November in the eurozone painted a worrisome picture, revealing a significant drop in employment for the first time in nearly three years. Even as business activity continued to contract, there were glimmers of hope as the rate of decline in both output and new business showed signs of slowing down. Meanwhile, attention turned to the Dutch election results, particularly an exit poll suggesting the potential for a substantial victory by right-wing populist Geert Wilders and his Freedom Party, the PVV.

In the U.S., stocks saw an increase on Wednesday, buoyed by the benchmark 10-year Treasury yield’s temporary dip to a two-month low. The broadening of the November market rally extended into the Thanksgiving holiday, fostering positive momentum in the market.

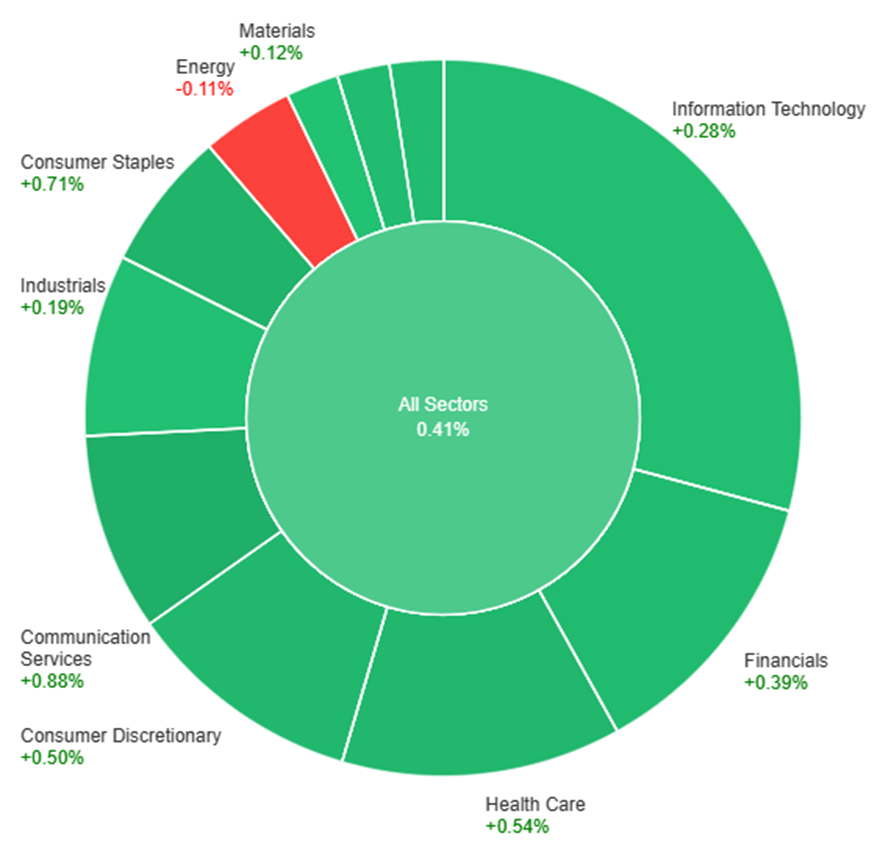

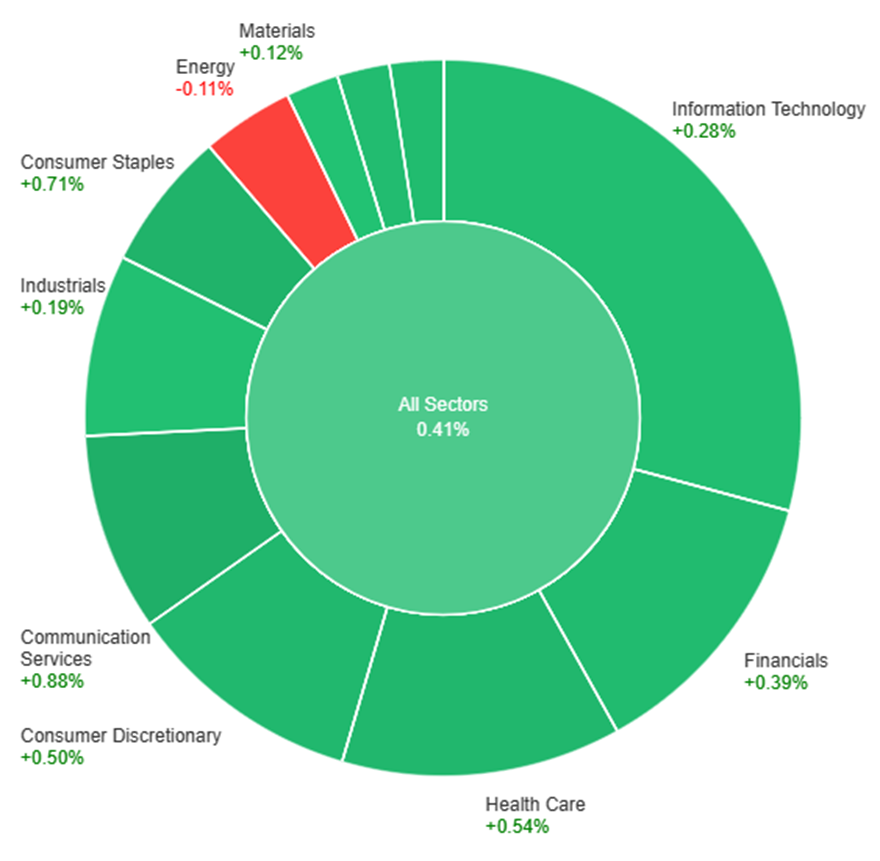

Stock markets were closed on Thursday, here it is the latest updates from Wednesday, across various sectors, the market generally saw positive gains, with the Communication Services sector leading the way with a rise of 0.88%. Following closely were Consumer Staples at 0.71% and Health Care at 0.54%. Sectors such as Financials, Real Estate, and Consumer Discretionary also experienced moderate gains, ranging from 0.37% to 0.50%. However, some sectors did not fare as well, with Energy being the only sector to experience a decrease, falling by 0.11%. Sectors like Information Technology, Industrials, and Materials saw gains ranging from 0.12% to 0.28%, contributing to the overall positive trend in the market for the day.

Currency Market Updates

In a truncated trading session due to the Thanksgiving holiday, the US Dollar experienced a modest decline, settling around 103.75 in the US Dollar Index (DXY), lingering below the 104.00 mark. Despite the closure of US markets, positive sentiment prevailed in Wall Street futures following gains in European markets. With no major US data scheduled for release on Friday and a shortened Wall Street session, attention turned to the S&P Global PMI projection, indicating a slight anticipated downturn in both the Services and Manufacturing sectors.

Meanwhile, the performance of other currencies against the dollar varied. The Euro maintained a relatively stable position around 1.0900 against the dollar, buoyed by encouraging Eurozone PMI figures and an uneventful account of the European Central Bank’s latest meeting. The Pound exhibited strength, reaching a two-month high against the dollar at 1.2530, driven by positive UK PMI data. Other currencies like the Japanese Yen, New Zealand Dollar, Canadian Dollar, and Australian Dollar displayed mixed movements against the US Dollar, influenced by domestic economic indicators and market sentiment. Despite subdued price action, the Australian Dollar managed to rise against the dollar, hovering around 0.6550, while the New Zealand Dollar awaited Q3 Retail Sales data and the Canadian Dollar looked toward the release of September Retail Sales figures.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Inches Up Amidst Low Volume Consolidation: Eurozone Data Insights and ECB Outlook

The EUR/USD saw a modest rise amidst low trading volume, hovering around 1.0900 while the US Dollar Index weakened slightly, fostering support for the pair amid subdued market activity. Eurozone PMI figures showed improvements in both the Manufacturing and Services sectors, yet remaining below the growth threshold. The data initially boosted the Euro but lacked sustained momentum due to minimal trading. The upcoming German GDP report and ZEW survey are anticipated to impact market sentiment. ECB’s recent meeting minutes revealed a consensus on maintaining policy rates and addressing heightened economic uncertainty. Despite ECB President Lagarde and council members slated to speak, clear insights into monetary policy adjustments aren’t expected, especially amid the US market’s closure for Thanksgiving, likely leading to thin trading conditions.

On Thursday, the EUR/USD moved flat as the US market holiday. Currently, the price is moving just below the middle band of the Bollinger Bands with a potential of moving in consolidation as the US market will also close earlier today. The Relative Strength Index (RSI) stays at 54 which reflects a neutral position for the currency pair.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Struggles to Hold $2,000 Amidst Quiet Trading Session

Gold Spot experienced a fluctuating journey, initially surging towards $2,000 in the Asian session, propelled by a weaker US Dollar, only to retract gains and settle around $1,990 during American hours amid limited trading activity with US markets closed. Despite benefiting from increased risk appetite and a weakening dollar, bolstered by favorable Eurozone PMIs, the precious metal fell short of reclaiming the $2,000 mark. With expectations of continued thin trading and a shortened US market session on Friday, Gold faces a landscape favoring consolidation, although the bullish bias persists for XAU/USD.

On Thursday, the XAU/USD moved flat as the US market holiday. Currently, the price is moving just below the middle band of the Bollinger Bands with a potential of moving in consolidation as the US market will also close earlier today. The Relative Strength Index (RSI) stays at 55 which reflects a neutral position for the pair.

Resistance: $1,996, $2,008

Support: $1,988, $1,973

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Flash Manufacturing PMI

22:45

49.9

USD

Flash Services PMI

22:45

50.4

Written on November 24, 2023 at 1:06 am, by anakin

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

25th of November 2023 (Saturday) 00:00-23:59 (GMT+2)

26th of November 2023 (Sunday) 00:00-23:59 (GMT+2)

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed. If you don’t want to hold any open positions during the maintenance, it is suggested to close the position in advance.

3. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]

Written on November 23, 2023 at 8:23 am, by anakin

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on November 23, 2023 at 7:45 am, by anakin

The stock market witnessed a surge in major indices, with the Dow Jones, S&P 500, and Nasdaq all marking notable gains, signaling a widening positive trend across the market. However, the energy sector faced a slight decline due to OPEC’s postponed meeting on production cuts. Treasury yields experienced a significant drop, reaching a low not seen since September, influenced by the Federal Reserve’s persistent stance on monetary policy. Despite slight fluctuations and concerns over export restrictions on China impacting Nvidia’s shares, the market remains on track for monthly gains. Meanwhile, in currency markets, the US dollar strengthened against various currencies like the euro, yen, and pound, driven by positive US economic data and global market dynamics. The focus now shifts to upcoming flash PMI releases, which are anticipated to shape currency trajectories and impact key support levels.

Stock Market Updates

The stock market saw a rise in indices as the Dow Jones Industrial Average gained 184.74 points to reach 35,273.03, marking a 0.53% increase. Similarly, the S&P 500 climbed 0.41% to 4,556.62, and the Nasdaq Composite advanced by 0.46% to 14,265.86. This broadening market rally was reflected in over half of the stocks on the NYSE showing gains, suggesting a widening scope for the positive trend. Notably, smaller cap stocks outperformed with a 0.7% and 0.6% rise for small and mid-cap stocks, respectively. However, the energy sector faced a 0.1% decline due to OPEC’s postponed meeting on production cuts, impacting companies like Marathon Oil, EOG Resources, and Devon Energy.

The Treasury yield for the 10-year briefly dropped to 4.369%, hitting its lowest since September, a significant decrease from October’s milestone of crossing the 5% mark for the first time in 16 years. The Federal Reserve’s notes from its recent meeting suggested a persistent stance on restrictive monetary policy, with no hint of imminent interest rate cuts. Despite this, investor optimism prevailed regarding the December meeting. Nvidia’s quarterly report revealed better-than-expected earnings and revenue but cautioned about the impact of export restrictions on China, leading to a 2.5% drop in its shares. Despite Tuesday’s slight decline, the major indices remain on track for monthly gains, with the Nasdaq rallying 11% in November, the Dow up nearly 7%, and the S&P 500 rising over 8%. The market sentiment leans towards the possibility of continued rally, especially with inflation trends and the likelihood of a “soft landing” from the Fed, as noted by Charlie Ripley, a senior investment strategist at Allianz Investment Management. The New York Stock Exchange closed for Thanksgiving and will have an early closure on Friday.

On Wednesday, across various sectors, the market generally saw positive gains, with the Communication Services sector leading the way with a rise of 0.88%. Following closely were Consumer Staples at 0.71% and Health Care at 0.54%. Sectors such as Financials, Real Estate, and Consumer Discretionary also experienced moderate gains, ranging from 0.37% to 0.50%. However, some sectors did not fare as well, with Energy being the only sector to experience a decrease, falling by 0.11%. Sectors like Information Technology, Industrials, and Materials saw gains ranging from 0.12% to 0.28%, contributing to the overall positive trend in the market for the day.

Currency Market Updates

The recent updates in the currency markets have seen the US dollar gaining strength, primarily driven by positive data on U.S. jobless claims and Michigan sentiment, reinforcing the Federal Reserve’s stance against premature rate cuts. Treasury yields experienced an upsurge following a notable drop in initial claims during the job report survey week and a concurrent decrease in continued claims, supporting the dollar’s ascent. Despite below-forecast October durable goods orders, the upward revision in Michigan sentiment and a rise in 1-year inflation expectations propelled Treasury yields further, benefiting the dollar. Notably, EUR/USD faced a 0.3% decline, largely influenced by the widening gap between 2-year Treasury yields and bund yields.

Meanwhile, USD/JPY exhibited a rebound, erasing a significant portion of its previous dive, driven partly by Japan’s economic view being reduced for the first time in 10 months, following an unexpected drop in Q3 GDP. Sterling experienced a 0.4% decline amid the dollar’s broader resurgence and the announcement of fiscal stimulus plans by British Finance Minister Jeremy Hunt. The pound found support at the 1.2450 200-DMA, with the retreat in risk-sensitive cable partially offset by the rise in U.S. equities. Other currencies like the Aussie faced a 0.24% fall, encountering resistance at the 200-DMA amidst a backdrop of weakened Chinese markets and commodities.

The upcoming focus in the market lies on the November flash PMI releases, which are expected to serve as crucial indicators for major economies, potentially impacting the trajectory of currencies like EUR/USD and influencing key support levels, such as the 100-day moving average around 1.08. Additionally, USD/JPY’s movement is closely tied to the convergence of various DMAs in a specific range, indicative of potential future trends. These developments reflect a dynamic landscape in the currency market, shaped by economic data releases and geopolitical events impacting different currencies differently.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Corrects Amidst US Dollar Strength: Market Anticipation on Eurozone Rates and US Data

The EUR/USD retreated to 1.0850 as the US Dollar surged post-release of robust US economic data, marking a correction from recent highs. Bundesbank President Joachim Nagel’s remarks on Eurozone interest rates nearing their peak spurred speculation, hinting at limited rate hikes without an inflation rebound. Thursday’s focus lies on preliminary November PMI data, expected to show slight improvements below the pivotal 50 mark, potentially amplifying pressure on EUR/USD if outcomes disappoint. Concurrently, the US Dollar strengthened on mixed data, including a larger-than-expected drop in Jobless Claims and a sizable contraction in Durable Goods Orders. With US markets closed Thursday, attention shifts to the ECB’s monetary policy meeting minutes, while Treasury yields bolster the Dollar’s corrective momentum amid anticipations for market consolidation.

On Wednesday, the EUR/USD demonstrated a robust downward trend, hitting the lower band of the Bollinger Bands. Presently, it trades marginally above this point, suggesting a potential upward shift aiming for the middle band. With the Relative Strength Index (RSI) resting at 50, it reflects a neutral position for the currency pair.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Retreats Amid US Dollar Rebound and Economic Data Surge

In response to a surge earlier in the week, Spot Gold (XAU/USD) experienced a pullback as it approached the critical resistance level of $2,010. The decline continued through the American session, signaling potential further downside, albeit at a gradual pace. Despite this retreat, the yellow metal retains an underlying bullish outlook. Concurrently, the US Dollar Index (DXY) rebounded from monthly lows, spurred by robust US economic data, reaching 104.20 before retracing slightly below 104.00. The climb was supported by an uptick in US Yields following a bounce from 4.37% to 4.40%. Notably, recent US data showcased a drop in Initial and Continuing Claims alongside a larger-than-expected contraction in October Durable Goods Orders. With the US market set to be closed on Thursday, a decline in trading volume is anticipated in the upcoming sessions.

On Wednesday, XAU/USD experienced a downward movement, reaching the middle band of the Bollinger Bands. Presently, the gold price hovers slightly above this level, indicating a potential minor uptick aiming for the upper band. The Relative Strength Index (RSI) sits at 55, indicating a period of consolidation for the XAU/USD pair.

Resistance: $1,996, $2,008

Support: $1,988, $1,973

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

JPY

Bank Holiday

USD

Bank Holiday

EUR

French Flash Manufacturing PMI

16:15

43.2

EUR

French Flash Services PMI

16:15

45.6

EUR

German Flash Manufacturing PMI

16:30

41.1

EUR

German Flash Services PMI

16:30

48.4

GBP

Flash Manufacturing PMI

17:30

45.0

GBP

Flash Services PMI

17:30

49.5

Written on November 23, 2023 at 2:11 am, by anakin

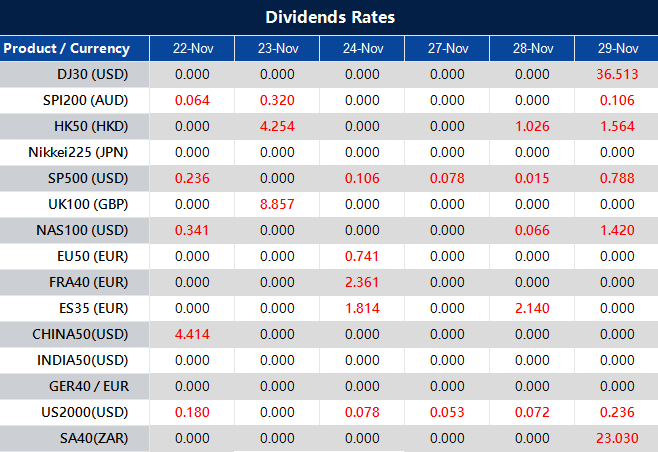

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on November 22, 2023 at 6:48 am, by anakin

The Federal Reserve’s indication of maintaining high-interest rates led to a stock market dip, impacting indices like the Dow Jones, S&P 500, and Nasdaq Composite. This stance affected sectors including housing, reflected in the lowest existing home sales since 2010, impacting companies like Lowe’s and American Eagle. Amidst this, Amazon’s stock fell due to Jeff Bezos’ shares sale, while Nvidia faced a slight decline ahead of its earnings announcement. The dollar saw a rebound after a significant drop, influenced by FOMC minutes and market volatility from weak economic data. Currency pairs like EUR/USD faced downward trends, diverging from USD/JPY’s speculative long positions. Expectations on rate cuts varied between the ECB and Fed, impacting movements in pairs like USD/CAD and USD/CNY. Future market sentiments hinge on upcoming economic releases like U.S. durable goods and jobless claims, likely affecting currency valuations and sentiments.

Stock Market Updates

The stock market saw a decline following the release of the Federal Reserve meeting minutes, which indicated no plans for interest rate cuts. This led to the Dow Jones slipping by 0.18%, closing at 35,088.29, while the S&P 500 dipped 0.20% and the Nasdaq Composite fell by 0.59%. The Fed emphasized the need for a “restrictive” policy to combat potentially stubborn or rising inflation, maintaining the benchmark rate at 5.25% to 5.5%. Market expectations suggest the Fed will maintain this stance through its December meeting, with potential rate cuts anticipated from May onwards.

This environment of sustained higher rates impacted various sectors. Housing data revealed a tough month for homebuyers, with existing home sales dropping to 3.79 million units, the slowest pace since August 2010. Companies like Lowe’s and American Eagle faced stock declines due to reduced sales outlooks and weaker operating income guidance, respectively. Additionally, Amazon’s shares dropped 1.5% following news of former CEO Jeff Bezos selling 1.67 million shares. Amidst this, Nvidia, despite hitting an all-time high on Monday, experienced a slight dip in shares by 0.9% on Tuesday ahead of its earnings announcement.

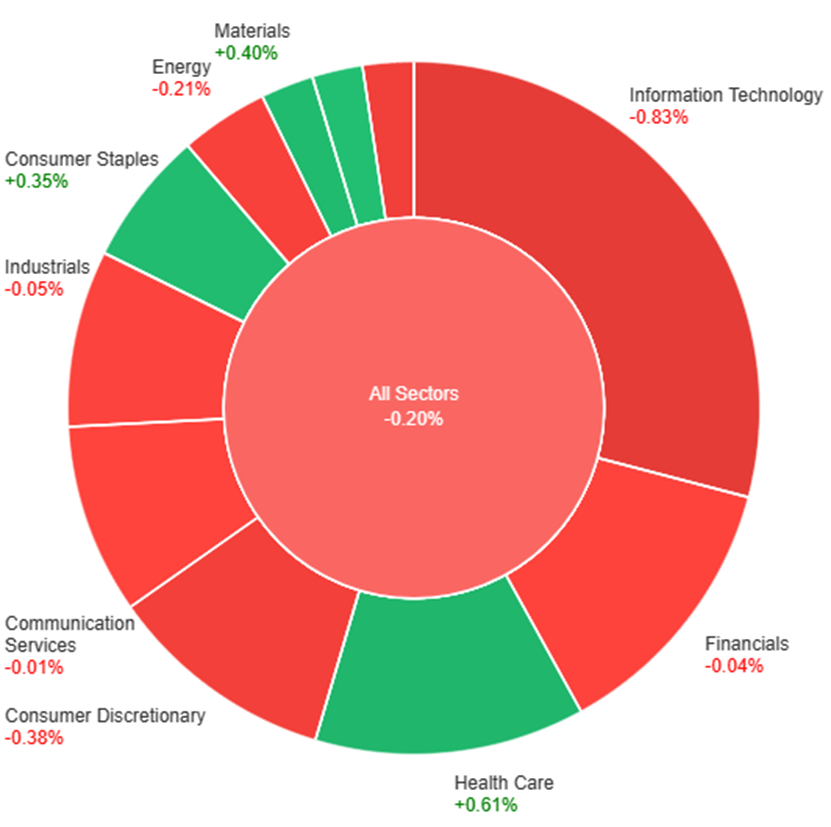

On Tuesday, across all sectors, there was a slight downturn of 0.20%. However, some sectors experienced positive growth, with Health Care leading the way at +0.61%, followed by Materials (+0.40%), Consumer Staples (+0.35%), and Utilities (+0.22%). Conversely, Information Technology witnessed the most significant decline at -0.83%, while Consumer Discretionary (-0.38%) and Real Estate (-0.47%) also faced notable decreases. Communication Services showed marginal negative movement at -0.01%, and Energy (-0.21%), Financials (-0.04%), and Industrials (-0.05%) followed suit with minor decreases.

Currency Market Updates

In recent market updates, the US dollar index showed a slight rebound after a 4% decline following the November 1st Federal Reserve meeting. This recovery was driven by short positions taking profits ahead of the release of the Federal Open Market Committee (FOMC) minutes. However, the dollar’s decline had been influenced by soft data on jobs, CPI, and retail sales, contributing to market volatility. Despite falling Treasury yields, profit-taking affected the Nasdaq index, reflecting the broader susceptibility of markets to traders’ profit-booking strategies. The dollar’s trajectory remains tied to economic forces, exemplified by existing home sales falling below forecasts and hitting their lowest since 2010, indicating the substantial impact of the Fed’s 5.25% rate hike, which could continue to exert pressure on the dollar’s value.

Meanwhile, in currency pairs, the EUR/USD saw a 0.33% decrease, retracting from earlier gains and hovering around the 61.8% Fibonacci level. The market sentiment differs between pairs, with USD/JPY showing increased speculative long positions compared to EUR/USD, potentially influencing a downward trend. Expectations regarding rate cuts diverge between the European Central Bank (ECB) and the Federal Reserve, with markets leaning towards rate adjustments in April for the ECB and May for the Fed. Additionally, the Sterling rose to a 10-week high against the dollar, backed by relatively hawkish comments from Bank of England speakers, despite market pricing predicting a potential rate cut by June. Other currency pairs, such as USD/CAD and USD/CNY, exhibited varied movements influenced by economic indicators and reports, underscoring the complex interplay of factors affecting currency markets. Looking ahead, upcoming releases like U.S. durable goods and jobless claims are anticipated to impact market sentiments and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Corrects from Three-Month High Amid Dollar Strength

The EUR/USD pair retreated on Tuesday following a recent peak, marking a corrective move amidst a weaker US Dollar. Factors including steady yields and a dip in equities favored the Greenback, causing the Euro to lag. US data revealed a larger-than-expected drop in Existing Home Sales, impacting market sentiment. Meanwhile, upcoming reports like Jobless Claims, Durable Goods Orders, and the University of Michigan Consumer Sentiment will likely influence further market movements. The FOMC minutes reiterated concerns about inflation, signaling potential future tightening measures. The Euro’s performance was also affected by a decline against the GBP, with anticipation building for the Eurozone’s preliminary November PMIs as the next key report.

In technical analysis, the EUR/USD is showing a strong upward trend on early Tuesday just to end the day weaker able to reach the middle band of the Bollinger Bands. It’s currently trading just around this level, indicating the possibility of another upward movement. The Relative Strength Index (RSI) at 57 shows a neutral but slightly bullish stance.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Surges Towards Key Resistance Amidst Dollar Stability

Spot Gold demonstrated a robust surge on Tuesday, rallying from sub-$1,980 levels to approach a significant resistance mark at $2,010. This bullish movement occurred despite a dip in stock prices and a stabilized US Dollar. The climb coincided with steady US yields, showcasing resilience after briefly touching $2,007 before retracing toward $2,000. The prevailing upward bias hinges on the anticipation that the Federal Reserve has halted interest rate hikes, bolstering Gold’s appeal. However, while market attention focuses on the upcoming FOMC minutes and critical US data releases like Jobless Claims and Durable Goods Orders, a more aggressive Gold rally may hinge on a clear downturn in Treasury yields signaling a peak, as of now, keeping the metal’s surge subdued.

In technical terms, the analysis shows that XAU/USD moved higher on Tuesday, able to reach the upper band of the Bollinger Bands. The gold price is currently moving back below this band, suggesting a possible minor increase to reach back to the upper band. With the Relative Strength Index (RSI) at 63, it signals a continuing slight bullish trend for the XAU/USD pair.

Resistance: $2,008, $2,040

Support: $1,993, $1,973

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Unemployment Claims

21:30

226K

USD

Revised UoM Consumer Sentiment

23:00

61.1

Written on November 22, 2023 at 5:23 am, by anakin

In order to provide you with a better user experience, VT Markets will update our MT5 software on November 25, 2023 (Saturday), requiring a minimum version of 3980 and Windows 10. During this upgrade period, the MT5 trading software will be temporarily unavailable for login and use. However, this will not impact your existing trading orders, and there will be no changes to your trading account or login password for the software.

If your current software version has not been updated, we sincerely recommend that you upgrade it after November 25, 2023.

Check your MT5 software version with the following steps:

※ PC: Open the MT5 software>Help>About;

※ Android: Open the MT5 app>About;

※ iOS: Open the MT5 app>Settings>Settings.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Written on November 21, 2023 at 7:07 am, by anakin

The stock market rallied as tech giants Microsoft and Nvidia drove significant gains, marking record highs amidst former OpenAI chief Sam Altman’s move to lead a new AI research team at Microsoft and Nvidia’s imminent earnings report. With the Dow Jones, S&P 500, and Nasdaq Composite all climbing, investors remained optimistic despite holiday closures. Lower-than-expected U.S. inflation data lessened concerns about rate hikes, reinforcing asset values but keeping a watchful eye on fiscal spending. Meanwhile, currency markets saw the U.S. dollar decline as risk-on sentiment grew, fueled by market anticipation of a potential Fed rate cut based on softer CPI data. Major currencies like the Euro and Sterling gained against the dollar, signaling changing market perceptions over traditional indicators like yield spreads. Ahead, crucial economic events and jobless claims data hold sway over market sentiments and currency movements.

Stock Market Updates

The stock market surged at the start of the week, with tech giants like Microsoft and Nvidia leading the charge. Microsoft saw a 2% rise, hitting a new high, following the announcement of former OpenAI chief Sam Altman joining to spearhead a new AI research team. Simultaneously, chipmaker Nvidia climbed 2.3%, reaching an all-time high just before its earnings report. This drove the Dow Jones Industrial Average up by 203.76 points, marking a 0.58% increase to close at 35,151.04. The S&P 500 also saw gains of 0.74%, finishing at 4,547.38, and the Nasdaq Composite surged 1.13% to close at 14,284.53, both marking their fifth straight day of growth.

The tech and communication services sectors notably drove these gains, witnessing increases of 1.5% and 1%, respectively. With Thanksgiving approaching, markets prepared for closure on Thursday and a shortened trading day on Friday. Despite historical choppiness around this holiday, November has consistently proven to be the S&P 500’s most successful month. Additionally, investors were buoyed by recent lower-than-anticipated U.S. inflation data, easing concerns about persistently high prices and suggesting the possibility of the Federal Reserve halting interest rate hikes. This trend further supported asset values, particularly with the concurrent drop in Treasury yields. However, market watchers remain vigilant about potential fiscal spending and deficit concerns, which could trigger upward pressure on yields. Wall Street is eagerly awaiting the release of the latest Fed minutes scheduled for Tuesday.

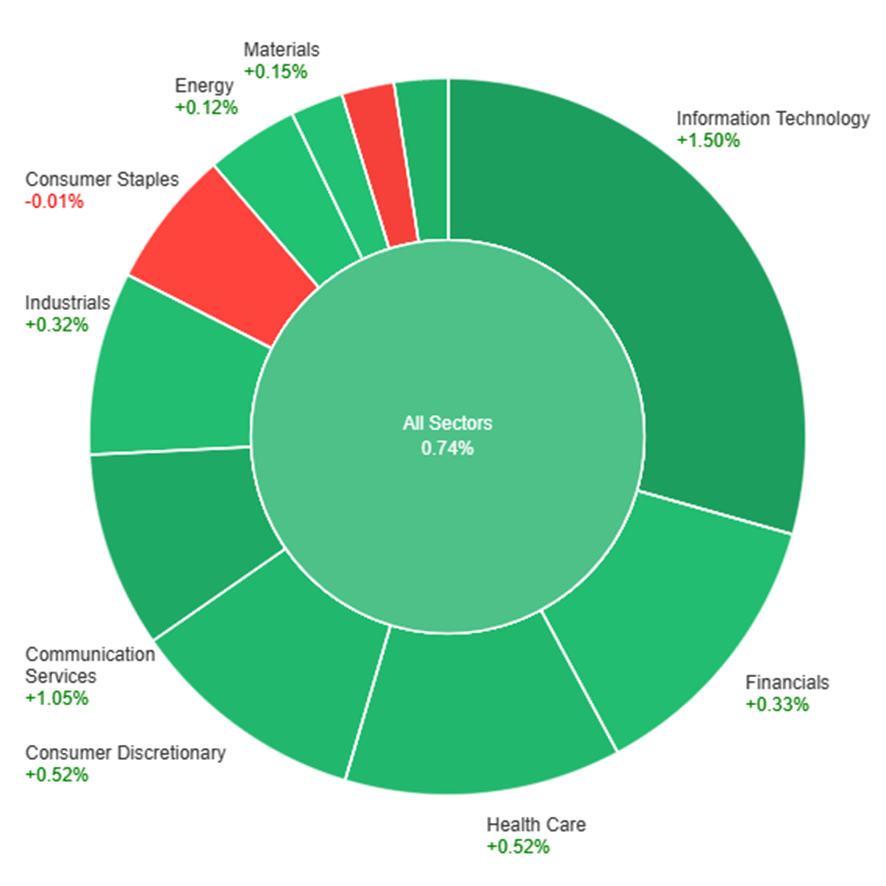

On Monday, the market saw a positive trend across most sectors, with a general increase of 0.74%. The standout performers were Information Technology and Communication Services, surging by 1.50% and 1.05%, respectively. Real Estate also demonstrated strength with a 0.79% rise, followed closely by Health Care and Consumer Discretionary, both gaining 0.52%. However, sectors like Utilities and Consumer Staples experienced slight declines of -0.31% and -0.01% respectively, while Energy and Materials showed marginal increases of 0.12% and 0.15%. Overall, the market exhibited broad positivity, particularly in the tech and communication sectors, driving the day’s gains.

Currency Market Updates

The recent fluctuations in the currency market, particularly concerning the US dollar, have been influenced by various economic indicators and shifting market sentiments. The dollar index experienced a notable decline, dropping by 0.49% and breaching key levels, primarily due to increased risk appetite following heightened expectations of a Federal Reserve rate cut. This shift was triggered by softer-than-expected US CPI data, causing the dollar’s safe-haven status to wane as risk-on flows took precedence in determining its value.

Despite certain supportive comments regarding disinflation from Richmond Fed President Thomas Barkin and the adjustment in yield spreads favoring the dollar, the currency continued its downward trajectory post-soft CPI release. The market’s anticipation of more disinflationary US data adds weight to the likelihood of an earlier Fed rate cut, potentially moving from June-July expectations to a more imminent cut in May. This shift aims to mitigate the risk of a severe economic downturn and further diminishes the dollar’s safe-haven appeal, influenced significantly by market perceptions rather than traditional indicators like yield spreads.

Looking ahead, market attention is directed toward crucial economic events such as Tuesday’s US existing home sales and the release of Fed meeting minutes. However, the pivotal moment arrives with Wednesday’s jobless claims data, as an above-forecast figure could intensify the substantial sell-off of USD/JPY, possibly pushing it below crucial support levels. This recent market sentiment has seen other major currencies like the Euro and Sterling make gains against the dollar, influenced not just by traditional yield spreads but more prominently by the selling pressure on the dollar as equities rallied.

The EUR/USD soared to a three-month high around 1.0950 as the US Dollar continued its downward trajectory, driven by market expectations of the Fed’s halted interest rate hikes and Wall Street’s buoyant stock prices. The US Dollar Index (DXY) hit a low of 103.45, seeking stability amidst its decline. Anticipation builds for the Fed’s meeting minutes while key US data on the Chicago Fed National Index and Existing Home Sales are on the horizon. Meanwhile, Europe gears up for the release of crucial preliminary November PMIs. Despite the risk-on sentiment favoring the EUR/USD, the US economy’s stronger performance against the Eurozone remains a fundamental support for the Dollar’s outlook.

In technical analysis, the EUR/USD is showing a strong upward trend on Monday, nearing the upper band of the Bollinger Bands. It’s currently trading just below this level, indicating the possibility of further upward movement. The Relative Strength Index (RSI) at 77 confirms a consistent bullish trend in the market.

Resistance: 1.1004, 1.1042

Support: 1.0937, 1.0885

XAU/USD (4 Hours)

XAU/USDRecovers from Dip Amid Dollar Vulnerability and Fed Expectations

Spot Gold faced a dip to $1,965 before bouncing back during the Asian session, indicating ongoing upside potential against a weakened US Dollar and decreasing Treasury yields. Despite the Greenback’s monthly lows and a subdued bond market, both Gold and Silver are not responding to the buoyant market sentiment. With anticipation building around the Federal Reserve’s meeting minutes release, the prevailing belief that the Fed might have concluded its rate hikes is impacting the Dollar’s short-term prospects, sustaining the upside potential for Gold.

In technical terms, the analysis shows that XAU/USD is on an upward trajectory this Monday, targeting the upper band of the Bollinger Bands. The gold price is presently just under this band, suggesting a possible minor increase to reach the upper band. With the Relative Strength Index (RSI) at 62, it signals a continuing slight bullish trend for the XAU/USD pair.

Resistance: $1,992, $2,008

Support: $1,973, $1,955

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

CAD

Consumer Price Index

21:30

0.1%

Written on November 21, 2023 at 2:37 am, by anakin