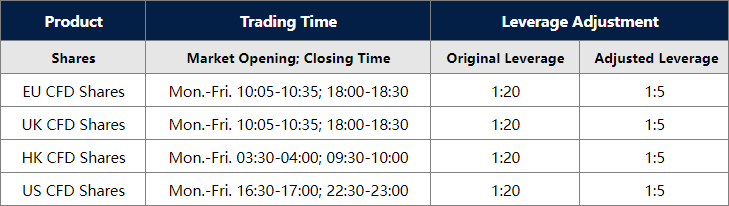

To provide a favorable trading environment to our clients, VT Markets will modify the trading setting of All Shares on MT5 on Nov 13, 2023:

1. Adjustment: New positions opened within 30 minutes before market closing and after market opening will start with leverage of 1:5. After the mentioned period, the leverage will be resumed to original leverage and will not be adjusted back to 1:5.

2. Product: EU, UK, HK and US CFD Shares

3. Platform: MT5

The above data is for reference only, please refer to the MT5 software for specific data.

Friendly reminders:

1. All specifications for CFD Shares stay the same except leverage during the mentioned period.

2. The margin requirement of the trade may be affected by this adjustment. Please make sure the funds in your account are sufficient to hold the position before this adjustment.

If you’d like more information, please don’t hesitate to contact [email protected].

On Monday, the stock market continued its positive momentum, with the Nasdaq Composite achieving its longest winning streak since January. The S&P 500 and Dow Jones also edged up, with the market pausing to digest the previous week’s robust rally. Investors are eagerly awaiting the Federal Reserve’s announcements and corporate earnings reports for potential bullish catalysts. Additionally, the currency market saw some notable movements, with the EUR/USD, USD/JPY, and other currencies responding to Treasury yields and economic data. As November traditionally performs well for the stock market, investors are keeping a close watch on market developments and central bank policies.

Stock Market Updates

On Monday, the stock market continued its positive momentum, building on last week’s strong rally. The Nasdaq Composite recorded its longest winning streak since January, rising by 0.3% to close at 13,518.78, while the S&P 500 edged up by 0.18% to finish at 4,365.98. The Dow Jones Industrial Average also inched up 0.1% to settle at 34,095.86. According to Adam Sarhan, CEO of 50 Park Investments, the market appeared to be taking a pause to digest the previous week’s robust rally and was waiting for the next bullish catalyst, which could come from the Federal Reserve’s announcements or corporate earnings reports. Notably, Nvidia saw a 1.7% increase in its stock price due to optimism from Bank of America ahead of its earnings report, while Bumble’s shares dropped 4.4% following the announcement that its CEO would step down in January. Meanwhile, SolarEdge Technologies saw a 5.1% decline after a downgrade from Wells Fargo. Bond yields reversed their trend from the previous week, with the 10-year Treasury yield rising by 9 basis points to approximately 4.653%.

The stock market’s recent performance marked the best week of 2023, with the Dow recording its largest weekly gain since October 2022, and the S&P and Nasdaq achieving their best weekly results since November 2022. A softer monthly jobs report had driven bond yields lower, providing support to equities. As the week progressed, there was a lighter schedule for economic data and company earnings, but seasonal tailwinds were expected to bolster the stock market’s recovery. November traditionally performs well for the S&P, and it marks the beginning of the best six-month return period for the market since 1950. The average return for the S&P has been 7% from November through April during this period. Earnings season was also winding down, with over 400 S&P companies having already reported their quarterly financial results. Investors were looking forward to updates from companies such as Walt Disney, Wynn, MGM Resorts, and Occidental Petroleum. Additionally, market participants were closely watching Federal Reserve Chair Jerome Powell’s scheduled speeches, hoping for insights into the potential direction of the central bank’s monetary policy, given the recent trend of lower bond yields.

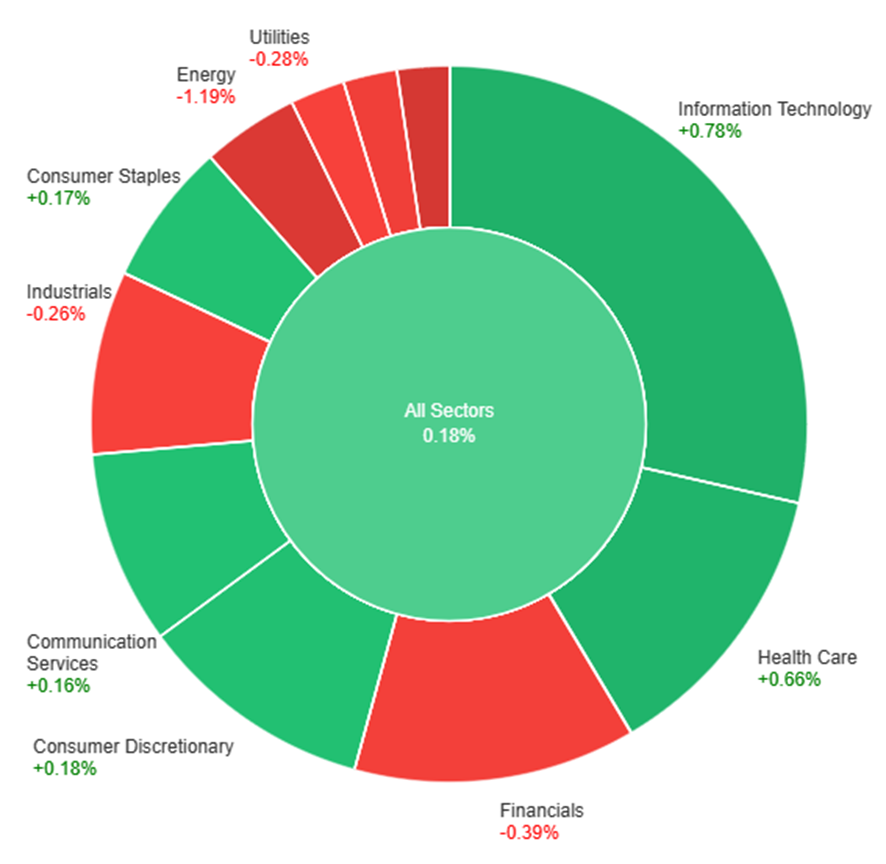

On Monday, the overall market showed a slight gain of 0.18%. Among the sectors, Information Technology and Health Care performed the best, with gains of 0.78% and 0.66%, respectively. The Consumer Discretionary and Consumer Staples sectors also saw modest increases of 0.18% and 0.17%. On the other hand, the Energy and Real Estate sectors faced significant declines, dropping by 1.19% and 1.41%, respectively. The Industrials and Utilities sectors experienced losses of 0.26% and 0.28%, while Financials and Materials both declined by 0.39% and 0.51%.

Currency Market Updates

In the aftermath of Friday’s disappointing U.S. jobs data release, the U.S. dollar index remained relatively stable on Monday. Modest gains in the Euro to U.S. dollar (EUR/USD) and the British pound, however, were countered by gains in the U.S. dollar to Japanese yen (USD/JPY) pairs, largely driven by the rebound in Treasury yields. Much of the previous week’s decline in Treasury yields and the U.S. dollar was attributed to speculative short positions in the Treasury market being squeezed. This squeeze followed relief over the Treasury refunding announcement, diminishing concerns of imminent Federal Reserve interest rate hikes, and was compounded by the soft employment and ISM non-manufacturing reports released on Friday. As Treasury yields and the U.S. dollar appear to be less vulnerable to further losses, market focus turns to the upcoming $112 billion Treasury refund scheduled for Tuesday to Thursday, as well as speeches by Federal Reserve officials later in the week, which are expected to caution against overpricing substantial rate cuts in 2024. The U.S. economic calendar for the week is relatively light, with the next significant data point being the November 14th Consumer Price Index (CPI) report. The CPI is anticipated to show modest growth at 0.1% and 0.3% in both overall and core month-on-month figures, which could reinforce the current market expectations for a rate cut by June.

The currency market experienced some notable movements on Monday, with the EUR/USD reaching a high of 1.0756 but facing resistance from Fibonacci levels and the limited continuation of last week’s yield spread between German bunds and U.S. Treasuries. The convergence of the 100-day and 200-day moving averages at 1.0805-6 and the daily cloud top at 1.0799 on Tuesday represent key technical levels to watch. While Friday’s surge above the 55-day moving average was seen as bullish, the U.S. dollar to Japanese yen (USD/JPY) pair rose by 0.33%, fueled by the rebound in Treasury yields, leaving Japanese government bond (JGB) yields relatively unchanged. The trajectory of Treasury yields this week, influenced by supply dynamics and Federal Reserve comments, is a pivotal factor for the USD/JPY pair. Meanwhile, the Bank of Japan’s potential shift away from yield curve control and negative interest rates may receive some guidance from Japan’s wage data scheduled for Tuesday. Higher long-term JGB yields could make holding foreign exchange-hedged Treasury positions less attractive, thereby supporting the Japanese yen. Notably, the USD/JPY’s recent decline from its 2023 peak to last year’s 32-year high at 151.74/94 raises concerns about a significant double-top reversal in the making. Sterling experienced a slight decline on Monday after relinquishing early gains, with its movement capped by the 200-day moving average. On the other hand, higher-beta currencies like the Australian dollar and the Chinese yuan gained 0.3% and 0.42%, respectively.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Faces Headwinds as USD Index Rebounds Amid Uncertainty Over Fed’s Rate-Hike Path

The EUR/USD pair encounters resistance as the USD Index (DXY) rebounds from an eight-week low, fueled by mixed signals from Federal Reserve officials regarding future rate hikes. This shift led to an uptick in US Treasury bond yields and USD short covering. The uncertainty surrounding the Fed’s next policy move has caused investors to speculate that the rate-hiking cycle may be approaching its end, with market pricing indicating a higher chance of a rate cut in June 2024. All eyes are now on Fed Chair Jerome Powell’s upcoming appearances for further guidance.

According to technical analysis, the EUR/USD moved slightly lower on Monday, easing from the upper band of the Bollinger Bands. Currently, the EUR/USD is trading between the upper and middle band, indicating the potential for a slight lower movement to reach the middle band. The Relative Strength Index (RSI) is at 60, signaling that the EUR/USD is back in neutral bias.

Resistance: 1.0765, 1.0835

Support: 1.0693, 1.0615

XAU/USD (4 Hours)

XAU/USD Softens as Positive Market Sentiment Eases Safety Demand

At the beginning of the week, a more optimistic market sentiment diminished the appeal of safe-haven assets, causing Gold (XAU/USD) to trade at around $1,983 per troy ounce with a softer tone. This decline was tempered by the relative absence of the US Dollar in investors’ focus. Despite limited activity in stock markets due to a lack of significant news, Wall Street’s major indexes extended their gains from Friday. This was supported by government bonds and equities, as the United States Nonfarm Payrolls Report and the Federal Reserve’s announcement signaled the end of the monetary tightening cycle. Central banks worldwide also expressed concerns about the impact of tightening on economic growth rather than current inflation levels, contributing to the overall market stability. While this week lacks significant economic events, the upcoming one is expected to bring updates on inflation from major economies, including the United States.

According to technical analysis, XAU/USD moves lower on Monday and is able to reach the lower band of the Bollinger Bands. Presently, the price of gold is moving near the lower band, creating a possibility to push lower. The Relative Strength Index (RSI) is currently at 38, indicating a slight bearish bias for the XAU/USD pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Significant economic events are expected to impact the forex market this week. Traders should closely monitor the Reserve Bank of Australia’s rate statement and the UK’s Gross Domestic Product (GDP) release. These indicators could substantially sway market conditions, underscoring the importance of staying abreast of recent developments to ensure a successful trading week.

Here are some notable highlights for the week:

Reserve Bank of Australia Rate Statement (7 November 2023)

The Reserve Bank of Australia (RBA) considered raising its cash rate in October 2023 but chose to maintain it at 4.1% for the fourth consecutive month.

Analysts anticipate the central bank will increase its cash rate to 4.35% at its next meeting on 7 November.

New Zealand Inflation Expectations (8 November 2023)

Inflation expectations in New Zealand rose to 2.83% in Q3 2023, up from 2.79% in Q2 2023.

The data for Q4 2023 is scheduled to be released on 8 November, with analysts forecasting a decline to 2.6%.

UK Gross Domestic Product (10 November 2023)

The British economy expanded by 0.2% month-over-month in August 2023, following a contraction of 0.6% in July.

The figures for September are due to be released on 10 November, with analysts predicting a 0.1% growth in the country’s GDP.

University of Michigan Consumer Sentiment Index (10 November 2023)

The University of Michigan’s consumer sentiment index for the US was revised upward to 63.8 in October 2023 from the preliminary estimate of 63.

Analysts anticipate the next report will reflect a sentiment index of 65.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

Phase 1 : 4th of November 2023 (Saturday) 02:00 – 03:00 (GMT+3)

Phase 2 : 5th of November 2023 (Sunday) 07:00 – 14:00 (GMT+3)

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed.

3. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

4. Please note after the Phase 2 maintenance finished, the system time will change from (GMT+3) to (GMT+2)

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]

In a remarkable Thursday rally, stocks saw a surge as Treasury yields dropped, sparking investor speculation that the Federal Reserve may pause its rate hikes for the remainder of 2023. The Dow Jones Industrial Average posted its strongest performance since June, the S&P 500 marked its best day since April, and the Nasdaq Composite had its best session since July. All 11 S&P 500 sectors ended in positive territory, with energy and real estate leading the way. Meanwhile, the US dollar faced mixed performance in the currency market, retreating initially but recovering as Treasury yields rebounded, amid a backdrop of changing central bank signals. Despite the risk-on sentiment, market caution remained as key economic reports were on the horizon.

Stock Market Updates

Stocks surged on Thursday as Treasury yields dropped, as investors speculated that the Federal Reserve might halt rate hikes for the rest of 2023. The Dow Jones Industrial Average recorded its strongest performance since June, rising 564.5 points or 1.7% to close at 33,839.08. Similarly, the S&P 500 had its best day since April, gaining 1.89% and settling at 4,317.78, marking its first back-to-back days of over 1% gains since February. The Nasdaq Composite also posted its best session since July, climbing 1.78% to close at 13,294.19. On a weekly basis, the S&P 500 was up approximately 4.9%, and the Dow had gained 4.4%, while the Nasdaq was on track for a more than 5% increase. The rally was widespread, with all 11 S&P 500 sectors ending in positive territory, led by energy and real estate, which both rose 3.1%.

The decline in bond yields was notable, with the 10-year Treasury yield falling by approximately 12 basis points to 4.668%, following its recent surge above 5%. This drop in yields was influenced by data showing easing inflation and a slowing labor market. Labor costs unexpectedly decreased in the third quarter, and weekly jobless claims ticked higher to 217,000. These developments added to investor confidence that the Federal Reserve might have finished its rate hikes. The Fed’s decision to keep interest rates unchanged for the second consecutive time on Wednesday had already triggered a substantial rally in the Dow, with the S&P 500 and Nasdaq Composite also ending up more than 1%.

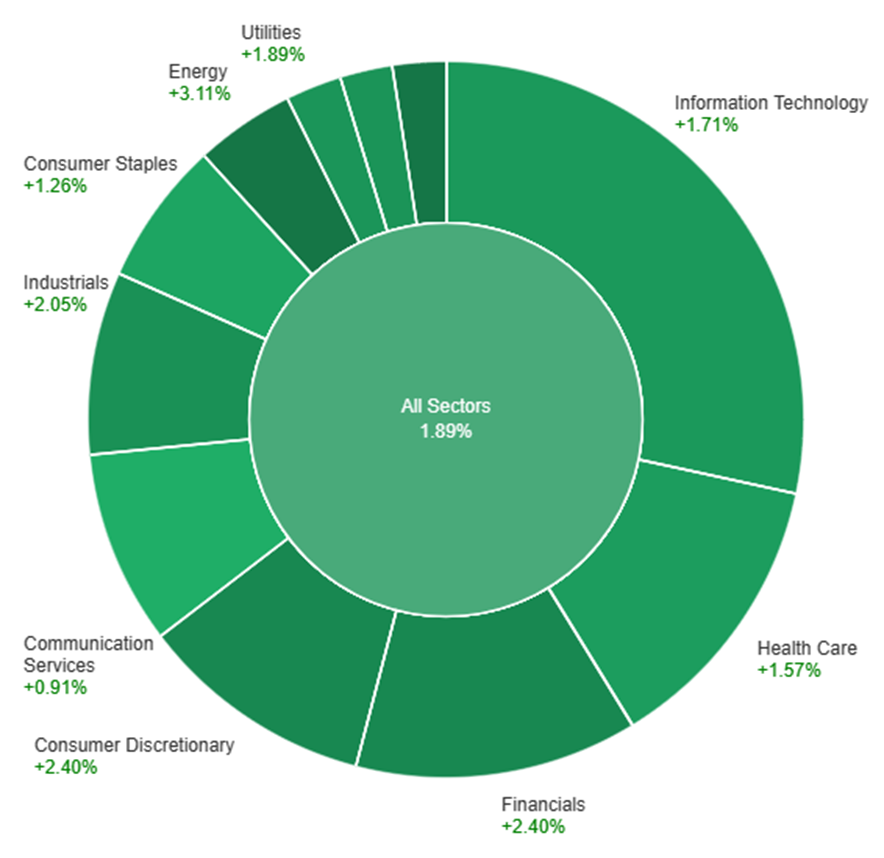

On Thursday, across various sectors, the stock market experienced a 1.89% increase. The energy and Real Estate sectors showed the strongest performance with gains of 3.11% and 3.09% respectively. Following closely, the Financials and Consumer Discretionary sectors both saw increases of 2.40%. Industrials and Materials sectors rose by 2.05% and 1.92%, while Utilities and Information Technology posted gains of 1.89% and 1.71%. Health Care and Consumer Staples sectors also advanced, albeit at a slower rate, recording increases of 1.57% and 1.26%. Lastly, the Communication Services sector showed the smallest increase at 0.91%.

Currency Market Updates

In the currency market update, the US dollar faced mixed performance as it retreated on Thursday due to an unexpected drop in the US unit and a slight increase in jobless claims. However, the dollar managed to recover from its lows as EUR/USD encountered resistance, and Treasury yields rebounded, leading to a yield curve inversion. Despite a 0.5% increase in EUR/USD during afternoon trading, the currency pair was unable to surpass the 55-day moving average, which had previously capped October’s highs. To confirm that the rebound high at 1.0695 in October was not just part of an ABC correction, a close above the moving average and the daily cloud base at 1.0659/64 was necessary.

The broader market sentiment remained risk-on, with yields increasing and the safe-haven appeal of the US dollar waning as the Bank of England (BoE) and the Federal Reserve signaled that their rate hikes were likely completed. Additionally, the European Central Bank (ECB) expressed confidence in the current state of interest rates, contributing to the dollar’s decline. Despite a recessionary reading in the eurozone, the ECB’s chief economist saw a good case for a soft landing. Sterling gained 0.4% against the weakening US dollar, while USD/JPY fell by 0.34%. The Australian and Canadian dollars rose by 0.54% and 0.76%, respectively, driven by risk-on sentiment. However, with key jobs and ISM reports scheduled for Friday, risks were seen rising in the market, and investors remained cautious about the dollar’s future performance.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Faces Headwinds as Economic Data Paints Gloomy Picture

On Thursday, the US saw an increase in weekly Initial Jobless Claims, reaching the highest level in seven weeks, while the Unit Labor Cost dropped significantly. In the Eurozone, the Manufacturing PMI decreased, signaling a contraction in activity, with several key nations facing economic challenges. These factors could limit the Euro’s strength and pose challenges for the EUR/USD pair. Upcoming data releases, including the Eurozone Unemployment rate and US employment figures, will be closely watched, providing clarity for the direction of the currency pair.

According to technical analysis, the EUR/USD moves higher on Wednesday, approaching the upper band of the Bollinger Bands then goes back lower. Currently, the EUR/USD is trading just above the middle band, indicating the potential for a slightly lower movement to reach the middle band. The Relative Strength Index (RSI) is at 55, signaling that the EUR/USD is in neutral bias.

Resistance: 1.0645, 1.0705

Support: 1.0592, 1.0526

XAU/USD (4 Hours)

XAU/USD Faces Pressure from China’s Economic Woes as Traders Eye US Jobs Data for Direction

Gold (XAU/USD) is grappling with the potential impact of downbeat Chinese economic data, considering China’s status as the world’s leading gold producer and consumer. Concerns arise as the Caixin Manufacturing PMI for October fell below expectations, raising doubts about the nation’s economic recovery. On Friday, all eyes will be on the US Nonfarm Payrolls data, Unemployment rate, and Average Hourly Earnings for October, which will guide traders in their search for trading opportunities within the gold market.

According to technical analysis, XAU/USD is moving in consolidation on Thursday and is able to reach the middle band of the Bollinger Bands. Presently, the price of gold is consolidating near the middle band, creating a possibility to push back lower. The Relative Strength Index (RSI) is currently at 47, indicating a neutral bias for the XAU/USD pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, US stocks rebounded, led by technology stocks, as the Federal Reserve chose to maintain interest rates, easing concerns of an imminent rate hike. The Dow Jones, S&P 500, and Nasdaq Composite all posted gains, with technology stocks like AMD, Micron Technology, and Nvidia leading the charge. The Federal Reserve’s decision also led to a drop in Treasury yields and boosted equity markets. The US dollar strengthened despite lower yields, supported by Fed Chair Jerome Powell’s stance against rate cuts and mixed economic data. The currency market saw the USD/JPY pair decline, the euro (EUR/USD) struggle, the British pound (GBP) face challenges, and the Australian dollar (Aussie) rise. Looking ahead, economic data and central bank meetings will continue to shape market dynamics.

Stock Market Updates

Stocks rebounded on Wednesday, following a challenging three-month period, after the Federal Reserve decided to keep interest rates unchanged for the second consecutive time, leading investors to believe the central bank would maintain its current stance for the remainder of the year. The Dow Jones Industrial Average rose by 221.71 points (0.67%) to 33,274.58, the S&P 500 increased by 1.05% to 4,237.86, briefly crossing its 200-day moving average, and the Nasdaq Composite gained 1.64% to reach 13,061.47. Information technology stocks were the standout performers, with gains of approximately 2%. Notable semiconductor companies like Advanced Micro Devices and Micron Technology saw significant increases of 9.7% and 3.8%, respectively. Nvidia shares also rose by more than 3%.

The Federal Reserve decided to maintain rates in the range of 5.25% to 5.5%, in line with expectations. The central bank reported that economic activity had expanded strongly in the third quarter, suggesting robust growth. While the recent rise in yields has reduced the likelihood of a rate hike in December, Fed Chair Jerome Powell did not completely rule out the possibility, indicating that it may not be difficult to raise rates after pausing for two meetings. Bond yields fell following the rate decision and the Treasury’s bond sale plans, which provided a boost to equities. The 10-year Treasury yield dropped below 4.8% after reaching above 5% in October, which had caused concerns in the markets.

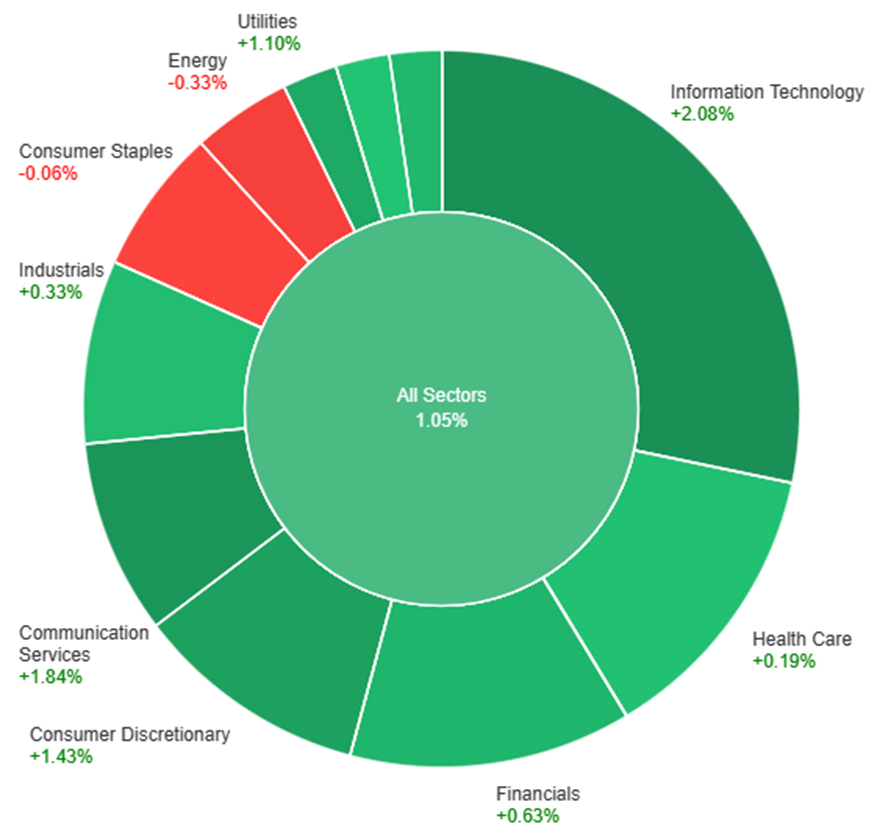

On Tuesday, the overall market saw a positive trend, with all sectors collectively rising by 1.05%. Among the top-performing sectors, Information Technology led the way with a substantial increase of 2.08%, followed by Communication Services at 1.84% and Consumer Discretionary at 1.43%. Meanwhile, Consumer Staples and Energy were the only sectors that experienced declines, with decreases of -0.06% and -0.33%, respectively. The rest of the sectors showed modest gains, contributing to the overall positive market performance.

Currency Market Updates

In the latest currency market updates, the US dollar experienced a 0.39% increase, despite a notable drop in Treasury yields. This surge came after the Federal Reserve’s decision to maintain its policy of keeping interest rates high for an extended period. Fed Chair Jerome Powell also clarified that there had been no discussions about rate cuts at this point. Prior to the Fed’s statement, the US dollar had seen a slightly stronger performance. However, it encountered resistance due to the pullback in USD/JPY and dovish reactions to disappointing US economic data, as well as the Treasury refunding announcement, which had pushed Treasury yields lower. Notably, ADP reported only 113k job additions, falling short of the forecasted 150k, and the combined readings for September and October were the weakest since January 2021. The ISM manufacturing data also unexpectedly slipped further into contraction, possibly influenced by the earlier UAW strike, which has since been resolved. On a positive note, the JOLTS report revealed an unexpected tightening of the labor market, with an increase in job openings and a decrease in layoffs to a 9-month low. These developments, combined with Tuesday’s data from the NY Fed’s MCTI, indicating persistent inflation, raised questions about whether the drop in Treasury yields was an overreaction, especially considering the Treasury’s refunding announcement showed a slower pace of issuance increases.

In the context of global currency dynamics, the USD/JPY pair experienced a 0.47% decline following a post-BoJ meeting surge that fell short of the 32-year peak reached in 2022 due to Japanese intervention warnings. The euro (EUR/USD) saw a 0.3% decrease, with the lower 10-day Bolli and last week’s low putting pressure on it, regardless of the fall in Treasury yields. This decline was triggered by downbeat Chinese manufacturing data, which raised concerns for the eurozone, particularly Germany, given its reliance on Chinese business. The British pound (GBP) also fell by 0.16%, remaining close to October’s lows as policymakers faced a dilemma ahead of the Bank of England (BoE) meeting. The BoE is grappling with the challenge of managing the UK’s high inflation rate of 6.7% alongside indications of economic stress. On a positive note, the Australian dollar (Aussie) saw a 0.7% rise, benefiting from higher equities. Looking ahead, Thursday is expected to bring additional economic data, including Challenger layoffs, jobless claims, unit labor costs, and durable orders, with Friday’s jobs data and ISM non-manufacturing figures on the horizon. These factors collectively shaped the currency market’s landscape, with the US dollar’s resilience against various headwinds being a notable highlight.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Faces Uncertain Outlook as ECB Maintains Rates and Eurozone Economic Indicators Signal Recession Risks

The European Central Bank (ECB) opted to keep interest rates steady last week, but expectations of rate cuts in Q2 next year persist due to disinflationary pressures resulting from sluggish GDP growth and concerning PMI data. In addition, recent economic indicators in the Eurozone, such as the preliminary HICP and GDP figures, painted a challenging picture with lower-than-expected readings, raising concerns about the possibility of a recession. Traders are keeping an eye on upcoming data releases and ECB communications, while the US Nonfarm Payrolls report on Friday is poised to influence the direction of the EUR/USD pair, with an estimated 180K job additions in October.

According to technical analysis, the EUR/USD moves higher on Wednesday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading above the middle band, indicating the potential for a slightly higher movement to reach the upper band. The Relative Strength Index (RSI) is at 54, signaling that the EUR/USD is in neutral bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Faces Mixed Signals Amid Weaker Chinese Data and Upcoming US Employment Figures

In the gold market, the weaker Chinese economic data poses a potential challenge, as the world’s largest gold producer and consumer experiences a drop in manufacturing PMI. However, the focus is now shifting to the upcoming US employment data, with initial jobless claims expected to rise and the Nonfarm Payrolls report on Friday projected to add jobs in October. These events hold the key to determining the direction of gold prices in the near term.

According to technical analysis, XAU/USD is moving in consolidation on Wednesday and was able to reach the narrow lower band of the Bollinger Bands. Presently, the price of gold is consolidating near the middle band, creating a possibility to push back lower. The Relative Strength Index (RSI) is currently at 50, indicating a neutral bias for the XAU/USD pair.

Sydney, Australia, 1 November 2023 – Online brokerage VT Markets has announced the return of its flagship trading competition, the King of the Hill trading contest. Scheduled to take place from 1 November 2023 to 31 January 2024, this latest edition of the contest promises a bigger, better experience across the board.

For the first time ever, VT Markets will be offering an amplified prize pool of USD 200,000 and increasing the number of potential winners from 25 to 60. Additionally, all participants will also receive complimentary points for VT Markets’ ClubBleu loyalty programme—the latest mark of VT Markets’ ongoing commitment towards its community.

Aside from these enhanced rewards, VT Markets is also expanding other aspects of the contest in unprecedented fashion. Setting the stage for a truly global spectacle, the upcoming King of the Hill trading contest will be open to multiple new regions, including India, Indonesia, and countries from the Middle East.

Commenting on these changes, a VT Markets spokesperson stated: “The evolution of our King of the Hill trading contest has been breathtaking to behold, and that has been due in no small part to our fantastic community. Given the overwhelmingly positive responses we’ve seen in every previous iteration of the contest, we’re now elevating the stakes and inviting a wider array of traders to showcase their trading prowess. With a significantly larger prize pool and up to 500:1 leverage at every trader’s disposal, this contest will no doubt be the most exciting one yet.”

More information will be made available closer to the launch of the contest. For all the latest news and updates, visit the relevant King of the Hill page below:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.