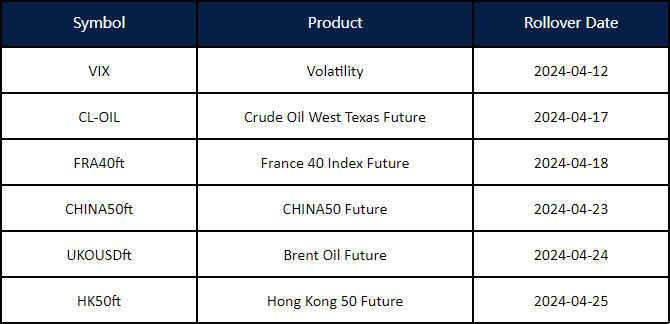

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

On a day marked by cautious trading, stock markets ended with marginal changes as investors weighed the impact of rising Treasury yields against the backdrop of impending U.S. inflation data, with Tesla’s stock standing out after an upbeat announcement from CEO Elon Musk. In currency markets, the U.S. Dollar resumed its downward trajectory, influenced by anticipation ahead of key economic reports, while the EUR/USD and GBP/USD pairs gained ground. Commodities saw mixed fortunes, as crude oil prices dipped due to easing geopolitical concerns, whereas gold and silver prices soared, reaching new highs amidst the dollar’s weakness and investors’ hunt for safe-haven assets. This confluence of events reflects a global financial landscape bracing for significant economic indicators and central bank actions that could reshape market dynamics in the near term.

Stock market updates

Stocks closed with minimal changes on Monday as an increase in Treasury yields held investors back from making significant moves, awaiting crucial U.S. inflation data. The Dow Jones Industrial Average slightly fell by 11.24 points or 0.03% to settle at 38,892.80, while the S&P 500 dipped by 0.04%, ending the day at 5,202.39. On the other hand, the Nasdaq Composite saw a slight increase of 0.03%, closing at 16,253.96. Tesla’s shares surged 4.9% following CEO Elon Musk’s announcement of a robotaxi reveal in early August, highlighting a noteworthy move in the market amidst a general state of anticipation.

The increase in Treasury yields acted as a barrier to significant market gains, with the benchmark 10-year Treasury note yield climbing about 4 basis points to 4.42%. Investors are keenly awaiting the March consumer and producer price indexes due later this week to gauge the effectiveness of the Federal Reserve’s efforts to combat inflation. The anticipated CPI figure, expected to rise by 0.3% last month, is particularly under scrutiny for indications on when the Fed might start reducing interest rates, stirring speculations and strategies among market participants.

Despite the subdued market movements, optimism remains tied to the broader economic outlook, especially after a stronger-than-expected jobs report last Friday. The report spurred hopes for sustained corporate earnings growth amidst a robust economy, despite the potential for enduring higher interest rates. This hope comes after both the Dow and S&P 500 experienced notable weekly losses, marking a period of cautious investor sentiment as they navigate through the implications of economic data and Federal Reserve policies on the market’s future direction.

Currency market updates

The U.S. Dollar resumed its downtrend at the start of the week amid rising anticipation for several key U.S. economic reports due later in the week, including the NFIB Business Optimism Index and the RCM/TIPP Economic Optimism Index, among others. The EUR/USD pair showed strength, rebounding from Friday’s dip to touch the 1.0860 area again. Similarly, the GBP/USD pair advanced to two-day highs near 1.2660, buoyed by risk sentiment and ahead of the BRC Retail Sales Monitor report. Meanwhile, the USD/JPY pair saw a modest increase but struggled to breach the significant 152.00 level, with market participants also eyeing upcoming consumer confidence and machine tool orders data from Japan.

The Australian Dollar made gains against the weakening U.S. Dollar, pushing past the 0.6600 mark and reaching two-day highs as traders anticipated domestic consumer confidence indexes. This movement in currency pairs comes amid a backdrop of cautious trading ahead of substantial economic indicators and central bank communications, including a scheduled speech by Minneapolis Fed President N. Kashkari, all of which could significantly influence market sentiment and currency valuations.

In commodities, crude oil prices faced another day of declines amid diminished geopolitical tensions, affecting market dynamics. Conversely, gold prices maintained their upward trajectory, reaching new all-time highs past $2,350, while silver prices also surged, surpassing the $28.00 per ounce mark for the first time since mid-June 2021. These movements in precious metals and energy commodities reflect the broader market’s response to fluctuating economic indicators, geopolitical developments, and the overarching trend of dollar weakness, all contributing to the complex interplay of forces shaping the currency markets.

Picks of the day analysis

EUR/USD (4 Hours)

EUR/USDrises amidst diverging central bank strategies and economic outlooks

The EUR/USD pair experienced a notable increase, touching the 1.0860 mark, driven by a downturn in the US Dollar alongside positive movements in both US and German yields, all against a backdrop of unchanged monetary policies. As both the Federal Reserve (Fed) and the European Central Bank (ECB) gear up for expected easing cycles starting in June, differences in the pace of interest rate cuts may lead to divergent central bank strategies. Despite a potential initial alignment in easing measures, the medium-term outlook suggests a stronger Dollar, influenced by more robust fundamentals in the US compared to the eurozone. This scenario positions the EUR/USD for a possible downward adjustment, initially aiming for its year-to-date low around 1.0700, with further potential declines beneath the 1.0500 level.

On Monday, the EUR/USD moved higher trying to reach the upper band of the Bollinger Bands. Currently, the price is moving in the middle between the middle and upper band, suggesting a potential slight downward movement to reach the middle band before going back higher. Notably, the Relative Strength Index (RSI) maintains its position at 57, signaling a neutral but bullish outlook for this currency pair.

Sydney, Australia, 9 April, 2024 – Global multi-asset broker VT Markets is hosting its most significant event to date—an exclusive three-day gathering in Monaco, the home ground of their key partner, Formula E team, Maserati MSG Racing.

Taking place from 25th to 27th April, select VIP guests, partners and media are invited for exclusive experiences including a media event, exquisite private yachting along the Monegasque coast, and thrilling views of the Formula E race.

The media event will feature keynote addresses from representatives of both VT Markets and Maserati MSG Racing. Attendees will have the unique opportunity to gain invaluable insights into the future of trading, the partnership story and significance of both companies’ shared dedication to seizing opportunities and driving progress.

“We look forward to a challenging yet fruitful 2024, as we increase our global footprint, bringing with us opportunity and excellence that we strive to provide,” remarked Ludovic Moncla, Head of Affiliates, VT Markets, who will be speaking at the event. “”In addition to our recent approval as a member of the Financial Commission, this initiative underscores our ongoing commitment to enhancing the client experience, with further enhancements on the horizon.” “We firmly believe that our partnership with VT Markets will unlock exciting opportunities for both brands,” said a spokesperson for Maserati MSG Racing. “By aligning our shared values of innovation and performance, we are confident in our ability to reach new audiences and achieve greater success together.”

Attendees can expect engaging discussions, networking opportunities, and exclusive insights into the future of trading. To learn more about this event please visit the VT Markets Events website (https://www.vtmarketsmy.com/company/about-us/events/). Members of the press or media who would like access or further information to cover the event may contact [email protected].

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

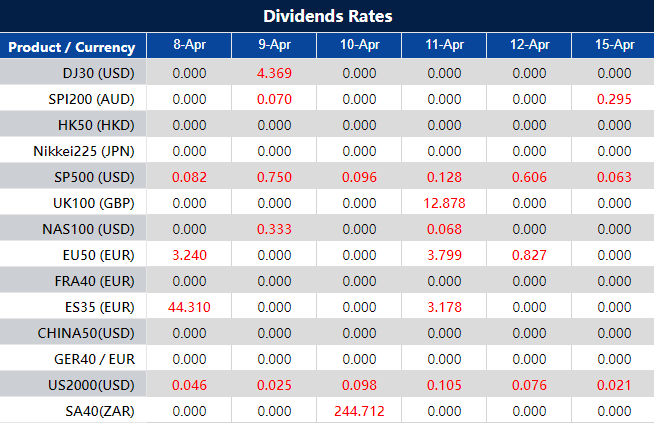

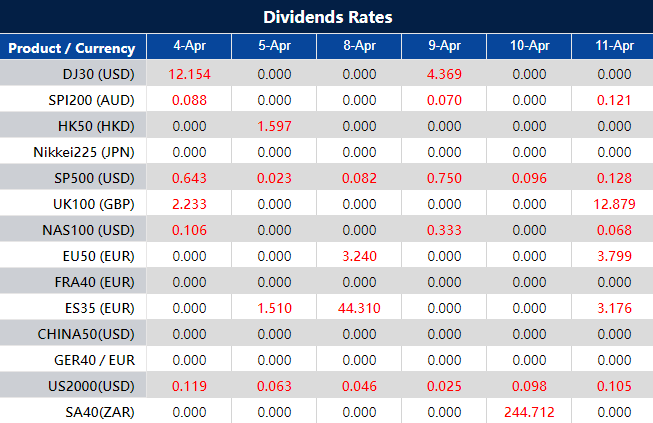

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

As we approach the second week of April 2024, financial markets and policymakers around the globe are bracing for a series of critical economic reports and central bank decisions. These events are expected to offer valuable insights into the ongoing economic recovery efforts, inflationary pressures, and future monetary policy directions. Here’s a day-by-day breakdown of what to anticipate:

Reserve Bank of New Zealand holds firm

On 10 April 2024, the Reserve Bank of New Zealand (RBNZ) made headlines by maintaining its official cash rate (OCR) at 5.5% during its first policy meeting of the year. This decision marked the fifth consecutive meeting without a change in the rate, signalling a cautious stance by the RBNZ amidst economic uncertainties. Analysts are already looking ahead, predicting the OCR to remain at 5.5% following the upcoming meeting, reflecting a steady approach to monetary policy.

U.S. inflation trends upward

In a surprising turn, the annual inflation rate in the United States nudged up to 3.2% in February 2024 from 3.1% in January. This incremental rise, though slight, has caught the attention of market watchers who now forecast a further increase to 3.4% for March. The data, expected to be released on 10 April 2024, will be pivotal for future Federal Reserve decisions.

Bank of Canada’s rate decision

The Bank of Canada, on its part, held its overnight rate target steady at 5% during its March meeting. The bank’s commitment to normalising its balance sheet, despite inflationary concerns, suggests a cautious optimism. Analysts anticipate this trend to continue, with expectations set for the interest rate to remain at 5% in the Bank of Canada’s next meeting.

Federal Reserve and ECB stance

Minutes from the Federal Reserve’s meeting, expected on 11 April 2024, will be closely scrutinised. With the fed funds rate holding steady at a 23-year peak of 5.25%-5.5%, the Federal Reserve’s projections for future rate cuts will be of significant interest. Similarly, the European Central Bank (ECB), which has kept interest rates at historically high levels, faces its own set of challenges balancing recession risks with inflation. Analysts foresee the ECB maintaining its current interest rate levels at 4.5% in its forthcoming meeting.

Upcoming economic data

Additionally, the release of the U.S. Producer Price Index (PPI) on 11 April will offer insights into wholesale price movements, having risen by 0.6% in February. Expectations for March are set at a more modest 0.3% increase. The UK’s GDP data, expected on 12 April, will also be pivotal. After a modest expansion of 0.2% in January, forecasts for February suggest a slight increase of 0.1%, indicating a cautious yet positive economic trajectory.

In summary, the coming week promises a wealth of information for economists, investors, and policymakers alike. With each announcement, the global economic picture for 2024 will become clearer, highlighting the delicate balance central banks are striking between fostering economic growth and managing inflationary pressures.

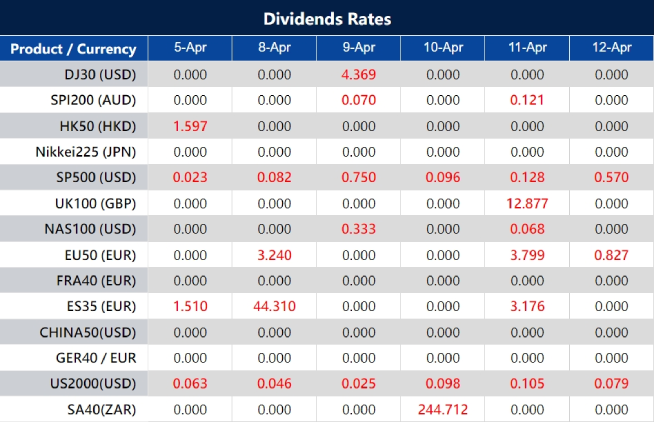

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Stocks plummeted amid rising oil prices and concerns over the Federal Reserve’s interest rate policies, with major indices like the Dow Jones, S&P 500, and Nasdaq experiencing significant drops. The spike in oil prices to over $86 a barrel fueled inflation fears, while remarks from Fed officials suggested a cautious approach to rate cuts, contributing to market volatility. Meanwhile, in currency markets, the USD Index fell, the euro and pound gained, and gold prices briefly touched all-time highs, reflecting a complex interplay of economic indicators and central bank signals affecting investor sentiment.

Stock market updates

Stock markets experienced a significant downturn on Thursday, fueled by a combination of rising oil prices, mounting fears that the Federal Reserve may delay interest rate cuts, and apprehension about the upcoming March jobs report. This cocktail of concerns led to a sharp sell-off, marking the Dow Jones Industrial Average’s worst performance since March 2023, as it plunged by 530.16 points or 1.35%, settling at 38,596.98. The S&P 500 and Nasdaq Composite weren’t spared either, recording declines of 1.23% and 1.40% to close at 5,147.21 and 16,049.08, respectively, highlighting a broader market apprehension.

Amidst the trading day, a sudden spike in crude oil prices exacerbated the market’s woes, with West Texas Intermediate (WTI) crude breaching the $86 per barrel mark, a peak not seen since October. This surge sparked additional inflationary fears among investors, contributing to the market’s downturn. Complicating matters, Minneapolis Fed President Neel Kashkari’s comments added to the uncertainty, hinting at a potential reconsideration of rate cuts if inflation persists. These factors, combined with a rise in the 10-year Treasury yield to 4.305%, underscored the growing caution among investors, reflected in the day’s volatile trading patterns.

Analysts and investors alike are adopting a cautious stance, closely monitoring the 10-year Treasury yield as a key indicator of future Federal Reserve actions. The overarching sentiment is one of caution, with a focus on how the Fed’s interest rate policies and inflationary pressures will shape market dynamics moving forward.

Currency market updates

The currency markets saw varied movements as the USD Index (DXY) experienced a further decline, dipping into the sub-104.00 region. Anticipation is building for April 5, with market participants keenly awaiting the Non-farm Payrolls, Unemployment Rate, and speeches from several FOMC members. The euro maintained a positive trajectory, reaching new multi-day highs near 1.0880, while the British pound edged close to the significant 1.2700 mark, marking its third consecutive session of gains. Meanwhile, the USD/JPY pair fluctuated within a narrow range, signaling a period of consolidation.

In the commodity currency space, the Australian dollar showcased notable strength, surpassing the 0.6600 threshold, amid expectations for the upcoming Balance of Trade results. This movement reflects broader currency market dynamics, where specific data releases and economic indicators are keenly anticipated for their potential impact on currency valuations. Additionally, the trading session for WTI crude remained relatively flat, yet close to its yearly highs, indicating a sustained interest in energy markets.

Precious metals witnessed a mixed session; gold prices paused after reaching an all-time high above $2,300 per troy ounce, while silver prices ended the session with minimal changes, despite hitting new highs earlier. These movements underscore the volatility and diverse influences at play within the currency and commodity markets, as investors navigate through economic data releases, central bank communications, and broader geopolitical factors impacting market sentiment and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USDrises amid divergent central bank policies and economic outlooks

Despite a significant drop in the US Dollar, leading to a robust increase in EUR/USD to the 1.0870-1.0880 range, the currency pair’s movement reflects broader economic trends, including fluctuating US yields and a steady rise in German bund yields. Central bank policies are in the spotlight, with both the Fed and ECB expected to begin easing cycles possibly by June, although their approaches may diverge. The Fed faces challenges in curbing housing sector inflation, while the ECB grows confident about reaching its inflation target, hinting at upcoming rate cuts. However, the long-term outlook suggests a potential strengthening of the Dollar against the Euro, especially if the ECB and Fed initiate simultaneous easing, potentially driving EUR/USD down to new lows.

On Thursday, the EUR/USD moved lower after reaching the upper band of the Bollinger Bands. Currently, the price is moving in the middle between the middle and upper band, suggesting a potential slight downward movement to reach the lower band before going back higher. Notably, the Relative Strength Index (RSI) maintains its position at 59, signaling a neutral but bullish outlook for this currency pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, the Dow Jones experienced a slight decline, continuing its downward trend for the third consecutive day, while the S&P 500 and Nasdaq saw modest gains. Market fluctuations were influenced by individual stock performances, such as Intel’s significant drop, and broader economic indicators pointing towards a resilient economy, which in turn affected investor sentiments regarding the Federal Reserve’s interest rate policies. In currency markets, the US dollar faced pressure, with notable movements against the Euro, British pound, and Australian dollar amidst geopolitical tensions and commodity price rallies. Investors remain cautiously optimistic, balancing between the best first quarter since 2019 and the potential for a volatile period ahead as markets adjust to recent gains and anticipate the Federal Reserve’s next moves.

Stock market update

The Dow Jones Industrial Average experienced a slight decline on Wednesday, continuing its struggle to break free from the slump that has characterized the second quarter. The Dow fell by 43.10 points, a 0.11% drop, closing at 39,127.14, marking its third consecutive day of losses. In contrast, the S&P 500 managed a slight increase of 0.11%, closing at 5,211.49, its first gain of the week, while the Nasdaq Composite saw a 0.23% rise, ending the day at 16,277.46. The downturn for the Dow was primarily due to a significant over 8% drop in Intel shares following the announcement of operating losses in its semiconductor manufacturing sector. Despite a positive trend for most of the day, artificial intelligence leader Nvidia ended in the red, hampering the overall market gains. However, substantial increases in major technology stocks like Netflix, up by 2.6%, and Meta Platforms, with a 1.9% gain, provided some support to the market.

Interest rates have continued to place pressure on the stock market. The release of ADP data on Wednesday indicated a higher-than-expected increase in private payrolls for March, signaling a resilient economy but also heightening investor anxiety over the Federal Reserve’s interest rate policies. Comments from Federal Reserve officials dampened hopes for early rate cuts, with Atlanta Fed President Raphael Bostic suggesting a potential rate decrease not occurring until the fourth quarter. Fed Chair Jerome Powell emphasized the need for more evidence of inflation easing before any reduction in borrowing costs. Market predictions now lean heavily towards unchanged rates at the Fed’s May policy meeting, with a diminishing likelihood of a cut by June, as reflected in the shifting odds according to the CME FedWatch Tool and Fed funds futures data.

Despite the challenging start to the quarter, some market analysts remain optimistic, viewing the recent downturn as a period of consolidation after a strong first quarter, the best since 2019 for the S&P 500.

Currency market update

The US dollar experienced additional downward pressure, challenging the 104.00 level as measured by the USD Index (DXY). Upcoming economic data includes February’s Balance of Trade results and weekly Initial Jobless Claims on April 4, alongside speeches from Fed members Barkin, Goolsbee, and Mester. The Euro gained momentum against the dollar, pushing towards the significant 200-day SMA at the 1.0830 region, with market participants looking forward to the final HCOB Services PMIs from Germany and the euro area, as well as the release of the ECB Accounts on the same day. Meanwhile, the British pound surged to new multi-day highs beyond the 1.2600 mark, aligning with the 100-day SMA, ahead of the final S&P Global Services PMI announcement for the UK.

The Japanese yen maintained a steady position against the dollar, staying below the 152.00 mark, with investors eyeing the upcoming release of weekly Foreign Bond Investment figures in Japan. The Australian dollar saw increased buying interest, surpassing the crucial 200-day SMA around 0.6545, with the final Judo Bank Services PMI report due on April 4. In the commodities market, ongoing geopolitical tensions drove West Texas Intermediate (WTI) oil prices to new 2024 highs, exceeding the $86.00 per barrel mark. Safe-haven demand, coupled with anticipations of Federal Reserve rate cuts in June, propelled gold prices to a record peak near the $2,300 per troy ounce, while silver prices continued their rally, reaching new highs just above the $27.00 level per ounce for the first time since June 2021.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD surges amid diverging central bank policies and mixed economic signals

The EUR/USD pair experienced a significant upswing, breaking past the 1.0800 mark and nearing the 200-day SMA, driven by a noticeable decline in the US Dollar amidst contrasting movements in US and German bond yields. Despite the Federal Reserve and the European Central Bank both indicating the onset of easing cycles potentially beginning in June, divergences in their approach could lead to varied strategies. This period saw mixed messages from Fed officials on interest rate adjustments, amidst indicators suggesting a softer economic landscape in the eurozone but expectations of a resilient US economy. These dynamics, coupled with inflation data below expectations in the euro area, hint at a complex interplay of economic factors influencing the EUR/USD trajectory, with a potential shift towards a stronger Dollar in the medium term as both central banks embark on easing measures, potentially driving the pair to revisit its recent lows.

On Wednesday, the EUR/USD moved higher, able to reach the upper band of the Bollinger Bands. Currently, the price is moving slightly below widen the upper band, suggesting a potential another upward movement to reach the resistance level. Notably, the Relative Strength Index (RSI) maintains its position at 67, signaling a bullish outlook for this currency pair.