The Federal Reserve kept its policy rate unchanged at 3.5–3.75%. The decision matched market expectations.

Updated projections point to slow easing ahead. The median forecast shows one 25 bp rate cut in 2026 and one 25 bp cut in 2027, unchanged from December.

Inflation Progress And Policy Conditions

The Fed said any cuts would depend on clear progress towards its inflation target. Geopolitical tensions in the Middle East were cited as a source of uncertainty for inflation and economic activity.

The note also set out a base case that rates stay on hold for the next two years. It added that near-term cuts are not expected.

The article was produced using an AI tool and reviewed by an editor.

Given the Federal Reserve’s decision to hold its policy rate in the 3.5-3.75% range, we see a clear signal of a higher-for-longer environment. The projection for only one small rate cut this year means traders should not position for imminent easing. This steady policy stance is likely to keep short-term interest rates anchored for the foreseeable future.

Trading Implications And Risk Hedges

This cautious approach is supported by recent data, which makes the Fed’s stance more credible. The latest Consumer Price Index report for February showed core inflation holding at 3.3%, still well above the 2% target. Combined with a resilient labor market that added 210,000 jobs last month, there is little pressure on the Fed to act quickly.

For the coming weeks, this suggests a strategy of selling volatility. With the Fed’s path clearly communicated, implied volatility on major indices should decrease, making strategies like selling VIX calls or establishing iron condors on the SPX attractive. Looking back at 2025, we saw how uncertainty around Fed pivots caused volatility spikes, a condition that now seems less likely.

Traders should also look at interest rate futures, where the market may have been pricing in more aggressive cuts. As these expectations are unwound, there is an opportunity in selling SOFR futures contracts for the second half of 2026. This is reinforced by the 2-year Treasury yield, which has remained firm above 3.6% following the announcement, reflecting the market’s adjustment.

However, we must remain aware of the geopolitical risks mentioned. The situation in the Middle East could cause a sudden oil price shock, which would complicate the inflation picture. A prudent hedge would be to own some cheap, out-of-the-money call options on WTI crude oil or the VIX to protect against a sudden market disruption.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

The Wall Street Journal reported on Friday, citing officials, that the Pentagon is sending about 2,200 to 2,500 Marines from the California-based USS Boxer amphibious ready group and the 11th Marine Expeditionary Unit to the Middle East. The deployment also includes three warships.

After the report, markets stayed risk-averse. At the time of publication, the Nasdaq Composite was down 1.2% and the S&P 500 was down about 0.8%.

Market Reaction And Dollar Trend

The US Dollar Index held small daily gains above 99.60. It remained on track to end the week in negative territory.

We remember when news of roughly 2,500 Marines being sent to the Middle East hit the wires back in early 2025, causing an immediate risk-averse reaction in the markets. That event set a precedent for lingering geopolitical tension that continues to influence our trading strategies today. The initial 1.2% dip in the Nasdaq Composite at the time was a clear signal of how sensitive tech and growth stocks are to global instability.

This underlying uncertainty has kept the CBOE Volatility Index, or VIX, elevated compared to historical averages. While it is not at crisis levels, it is currently hovering around 18, reflecting persistent market anxiety over potential escalations. For traders, this means option premiums are more expensive than they were during calmer periods, making hedging a more costly but necessary consideration.

Given this environment, buying put options on broad market indices like the SPX and QQQ is a primary defensive strategy to protect portfolios against a sudden downturn. We are seeing increased open interest in puts expiring in the next 45 to 60 days as institutions brace for potential shocks. With the S&P 500 trading near 5,500, the cost of this insurance is a small price to pay for downside protection.

Volatility And Energy Focus

Traders should also look directly at volatility products. VIX futures for April and May 2026 are trading in contango, priced higher than the spot index, which suggests the market is pricing in even greater turbulence in the coming months. Using call options on the VIX or VIX-related ETFs can provide a direct and leveraged hedge against a market sell-off.

The location of these tensions continues to make energy derivatives a critical focus. Following the troop movements in 2025, we saw WTI crude oil prices jump over 7% in a matter of weeks. Today, with WTI holding firm around $92 a barrel, using call options on crude futures or energy stocks is a viable way to speculate on price spikes should the situation deteriorate further.

Finally, we should not ignore the flight-to-safety trade in currencies. Last year, the US Dollar Index saw short-term bids on the news, and this dynamic remains in play. The dollar index has since trended higher, now sitting around 104, as global investors seek refuge; using options on currency ETFs like UUP can be an effective way to hedge against international risk.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Scotiabank’s global FX strategy team reports broad US Dollar strength, with G10 currency moves returning to a pattern seen in the early stages of the US/Iran conflict. They describe risk sentiment as fragile as markets weigh the chance of a longer conflict, shifting central bank paths, and sharp repricing in bond yields.

The report cites attacks on major Iranian gas fields and key Qatari LNG export facilities, raising concerns about a lengthened conflict and an extended repair timeline. Yields have risen in recent days, with large moves in the UK, following Fed caution, a hawkish ECB stance, and an aggressive U-turn from the Bank of England.

Dollar Strength And Policy Shift

For the Federal Reserve, expectations for easing have faded, with fed funds futures pricing very little policy change in either direction through September 2027. In commodities, oil prices have diverged, with WTI stabilising in the mid-$90 per barrel range while Brent has rallied towards $100 per barrel amid renewed tensions.

We are seeing the US Dollar strengthen broadly, driven by both the escalating conflict and a clear shift in central bank policy. The Dollar Index (DXY) has pushed above 107.50, a level we have not seen sustained since the market uncertainty of late 2025. This environment favors strategies like buying call options on the dollar or futures contracts that bet on its continued rise against other G10 currencies.

With risk sentiment so fragile, we see an opportunity in volatility itself. The VIX index, a measure of market fear, has surged past 22 this week, a sharp increase from its average of 15 during the final quarter of 2025. As Fed funds futures now price in very little chance of rate changes, traders can use options like straddles on major stock indices to profit from large market swings in either direction.

The divergence in oil prices presents a clear spread trading opportunity for the coming weeks. The premium of Brent crude over WTI has widened to over $5 per barrel, reflecting the direct geopolitical risk to global supplies from recent attacks. We believe traders should consider strategies that go long Brent futures while shorting WTI contracts to capitalize on this spread potentially widening further if tensions remain high.

Equity Risk And Hedging

This environment of a strong dollar and repriced yields is historically challenging for equity markets, reminding us of the pullback during the rate hike cycle in 2025. Consequently, purchasing put options on major indices like the S&P 500 offers a direct way to hedge portfolios. These positions can protect against potential downside in the near term as the market digests these overlapping risks.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

The Canadian dollar was slightly stronger against the US dollar and ahead of other G10 currencies. This followed earlier outperformance seen during the early phase of the US/Iran conflict.

Narrowing yield spreads were cited as a main factor. A Bank of Canada meeting that caused limited market reaction was also linked to the move.

Markets were pricing about 60 bps of Bank of Canada tightening by year-end. Very little was priced for the next two meetings, which left the currency open to repricing if policy expectations changed.

A fair value estimate was put in the low 1.34s at 1.3413, tied to the latest move in yield spreads. USDCAD was described as failing to break above the local range set in late January, with resistance in the mid-1.37s.

The article stated it was produced using an artificial intelligence tool and reviewed by an editor. It also described FXStreet Insights as a journalist team that selects market observations and adds analysis from internal and external contributors.

The Canadian dollar is showing notable strength against the US dollar, which we see as a signal to position for further USDCAD downside. This strength is backed by narrowing interest rate differentials between Canada and the United States. The market is now anticipating the Bank of Canada will hike rates by about 0.60% before the end of the year.

To support this view, we’ve seen Canada’s latest CPI print for February 2026 come in at 2.9%, slightly above the 2.7% consensus and reinforcing the case for a more hawkish Bank of Canada. Furthermore, WTI crude oil prices have remained firm above $85 per barrel, providing a supportive backdrop for the commodity-linked loonie. These factors reinforce our belief that the fair value for USDCAD is currently closer to the 1.34 level.

For derivative traders, the repeated failure of USDCAD to break above the mid-1.37s presents a clear opportunity. We believe selling USDCAD call options with strike prices around 1.3750 or 1.3800 for April and May 2026 expiries is a compelling strategy. This allows traders to collect premium by betting that this strong resistance ceiling will hold in the near term.

We remember a similar setup in the third quarter of 2025 when narrowing yield spreads also capped USDCAD gains significantly. During that period, the pair pulled back from similar levels over several weeks. This historical precedent suggests that the current environment is favorable for strategies that profit from a decline or stagnation in the USDCAD exchange rate.

The main risk to this outlook is a sudden dovish shift from the Bank of Canada, which seems unlikely given recent data. To manage this possibility, traders could consider using bear put spreads on USDCAD instead of more aggressive short futures positions. This would define the risk while still allowing for profit if the pair moves towards our 1.34 target.

Start trading now – Click here to create your real VT Markets account

EUR/GBP rose on Friday after falling the day before following the European Central Bank (ECB) and Bank of England (BoE) policy decisions. It traded near 0.8647 and stayed within the tight range seen for more than a week.

Both central banks kept rates unchanged on Thursday, with the ECB at 2% and the BoE at 3.75%. Inflation risks were linked to higher oil and energy prices during the US-Israel war with Iran.

Policy Stance And Growth Outlook

The ECB said it is not committing to a set rate path and will base decisions on inflation risks and the outlook. Its projections show 2026 growth at 0.9% in the baseline, 0.6% in an adverse case, and 0.4% in a severe case.

For 2026, the ECB sees inflation at 2.6% in the baseline, 3.5% in an adverse case, and 4.4% in a severe case. The BoE lifted its inflation view, with CPI averaging about 3% in Q2 2026, up from 2.1% in February.

Markets fully price an ECB hike by July and another by year-end, with some pricing a move as early as April. For the BoE, markets price more than two hikes this year, with about a 50% chance of an April hike.

Looking Back To 2025

Looking back to 2025, we can see the market was fixated on the race between the ECB and BoE to raise rates amid a major energy shock. The EUR/GBP cross was trapped in a narrow range around 0.8650 as traders weighed which central bank would be forced to act more aggressively. This uncertainty created significant tension in the currency pair.

The paths taken since then have become much clearer. The ECB did execute several rate hikes through 2025, bringing its main rate to 3.25%, and Eurostat’s flash estimate for February 2026 inflation has now fallen to 2.4%, much closer to the target. This has vindicated the ECB’s front-loaded approach from last year.

In contrast, the UK struggled more profoundly with the stagflationary shock. The BoE raised its bank rate to 4.75%, but the latest CPI data from the Office for National Statistics still shows inflation stubbornly high at 3.1%, while Q4 2025 GDP growth was confirmed at -0.2%. The UK economy is now paying a higher price in terms of weaker growth.

This divergence has pushed EUR/GBP up towards 0.8870, well above the tight range from last year. With the ECB now perceived as having more policy flexibility than the BoE, the upward trend in the cross looks set to continue. We believe the BoE is stuck, unable to cut rates due to inflation but hesitant to hike further due to the weak economy.

Given this outlook, we should consider buying EUR/GBP call options with strike prices above 0.8900 to capitalize on further upside. The implied volatility in the pair has decreased from its 2025 highs, making options relatively cheaper now. This strategy allows us to profit from continued euro strength while defining our risk.

We can also look at volatility-based trades. While overall volatility is lower, any negative surprise from UK economic data could cause sharp spikes in the pound’s movement. Therefore, we should be cautious about selling GBP volatility and instead consider structures that benefit from a steady grind higher in EUR/GBP.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Christopher Waller said he was prepared to dissent based only on the jobs report, but inflation has since become a bigger concern. He said he now expects labour force growth to be near zero.

He said near-zero labour force growth changes the breakeven level of job growth. He added that zero job growth may be what keeps the unemployment rate stable, even if it does not seem “normal”.

Oil Prices And Core Inflation

Waller said if oil stays high for months, it can feed into core inflation. He said a high and persistent oil shock would not be transitory, and it cannot be ignored, so caution is warranted.

He said he wants to wait and see how conditions develop before deciding on rate cuts later this year. He also said he does not think there is a need to consider rate hikes.

Waller said structural inflation may be close to 2% now, but tariffs keep it higher. He said if tariff effects do not roll off by the second half of the year, it will be tricky, though market pricing has not shown de-anchoring of expectations.

He said higher petrol prices could damage the consumer outlook, and some shocks could lead firms to cut labour. He also said there is no reason to make bank reserves scarce just to reduce the balance sheet, and proposals on reserve demand and balance sheet shrinkage warrant study and discussion.

Implications For Markets And Traders

It seems the path forward is a holding pattern, as inflation has become the primary concern again. While we don’t think rate hikes are on the table, the prospect of rate cuts later this year is fading. We need to wait and see how the data evolves before making any major policy decisions.

The latest February 2026 CPI report, coming in at 3.4%, confirms this cautious stance and makes it difficult to justify easing policy. With WTI crude stubbornly holding around $95 a barrel due to ongoing geopolitical tensions, there’s a real risk this high energy cost will start pushing up core inflation. This kind of persistent oil shock is something we cannot simply ignore.

Our view on the labor market is also shifting, as we now expect labor force growth to be near zero. This changes the math, meaning even a flat jobs report might be enough to keep the unemployment rate stable at its current 3.8%. This makes the monthly jobs number a much more sensitive indicator for potential wage inflation.

We are making some progress on underlying inflation, but looking back at the situation in 2025, it’s clear the tariffs from the Trade Modernization Act are holding prices artificially high. If these tariffs don’t roll off by the second half of this year as expected, it will create a tricky situation. Market expectations for inflation to drop are heavily tied to this assumption.

For derivative traders, this environment suggests playing for range-bound markets in the short term, but with an eye on volatility. Selling short-dated options on indexes like the S&P 500 could be viable, as the Fed seems locked in place for now. However, buying longer-dated volatility, perhaps through VIX calls or long-dated straddles, makes sense to hedge against a potential shock.

The main risks are a sudden shock that forces companies to start cutting labor, or consumer confidence finally breaking under the weight of high gas prices. We saw consumer sentiment waver during the brief recession scare of late 2025, and it could happen again. Any sharp downturn in retail sales or consumer credit data would be a major red flag.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

E-Mini Dow Jones futures fell for several days ahead of triple witching. A possible short-term support area is 45,780, a pivot low from December 2025.

Pivot lows are points where price previously turned higher after testing support. When revisited, they can act as support again and may lead to a bounce.

Key Support Level At 45780

If 45,780 does not hold, the next support area is around 45,286. This level matches prior pivot highs that later acted as support, and it sits along a trendline marked by earlier pivot lows.

This sets up a resistance-turned-support pattern, where an old ceiling becomes a floor. The 45,286 area combines multiple technical reference points, which can attract buyers or prompt short covering.

Triple witching can increase volatility because options, futures, and index contracts expire at the same time. This can push prices more sharply in either direction around levels such as 45,780 and 45,286.

With the triple witching expiration now past, we see the market testing a critical support zone around 45,780. This level is important as it marks the pivot low from back in December 2025, a point where buyers previously stepped in with force. The recent pressure comes after February’s CPI report showed inflation at 3.4%, slightly above expectations and keeping the Federal Reserve on alert.

Strategy Considerations After Expiration

For derivative traders, this 45,780 level presents an opportunity to sell weekly put options with strikes around 45,500, collecting premium on the expectation of a short-term floor. This strategy benefits from both a price bounce and the elevated volatility, which we’ve seen tick up with the VIX climbing to 18.5 this past week. Alternatively, buying short-dated call options could be a lower-risk way to play for a quick rebound.

If sellers push the market through that first level, we are looking at 45,286 as a more significant area to add long exposure. This zone represents a classic case of prior resistance from late 2025 now acting as a support floor, reinforced by a rising trendline. The recent weak Philly Fed Manufacturing Index adds to the narrative that if the market drops this far, dip-buyers may see it as a better value proposition.

A test of 45,286 would justify a more aggressive stance, such as scaling into E-Mini Dow futures contracts or selling puts with further out expirations, like those for late April 2026. Historically, these confluent support zones have produced multi-week rallies, as we saw after similar sell-offs in the third quarter of 2025. This makes it a high-probability zone for a more sustained market bottom rather than just a temporary bounce.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

GBP/USD fell on Friday and traded near 1.3380 at the time of writing, down 0.39% on the day. The drop followed a strong rally on Thursday after the Bank of England decision.

The move lower came as the US Dollar regained some strength, despite wider markets being shaped by tighter pricing of global monetary policy. This led to a corrective pullback in the pair.

Bank Of England Holds Rate

The Bank of England left its policy rate unchanged at 3.75%, in line with expectations. However, the vote was unanimous at 9-0 to hold, compared with forecasts of a 7-2 split.

The latest decision contrasted with the previous close 5-4 outcome. The Bank said it could act if inflation stays persistent.

We remember that hawkish surprise from the Bank of England back in 2025, when the unanimous 9-0 vote to hold rates signaled a deep commitment to fighting inflation. That move caught many off guard and set a precedent for the bank’s cautious stance. This history reminds us that the BoE is willing to delay policy shifts until it is absolutely certain inflation is contained.

Fast forward to today, March 20, 2026, and we see GBP/USD trading near 1.2850 with a similar dynamic at play. UK inflation, while down from its peaks, remains sticky at 2.8% according to the latest ONS figures, which is still well above the BoE’s 2% target. This persistent inflation explains why the BoE is holding its main rate at 4.5% and is reluctant to signal the start of an easing cycle.

Trading Implications For Sterling

Given the discrepancy between market hopes for rate cuts and the BoE’s stubborn caution, volatility in the pound is likely to increase. Derivative traders should consider buying GBP/USD straddles or strangles with expirations in the next two to three months to profit from sharp price moves around upcoming inflation reports and BoE meetings. Futures markets are currently pricing in at least two rate cuts by the end of the year, a view that seems overly optimistic given the central bank’s commentary.

This contrasts with the situation in the United States, where core inflation has fallen more convincingly to 2.5%, giving the Federal Reserve a clearer path to begin easing policy. This policy divergence should provide a floor for the pound against the dollar, making limited-risk bullish strategies attractive. Therefore, positioning through GBP/USD bull call spreads could be a prudent way to capitalize on potential sterling strength if the BoE continues to hold rates longer than the Fed.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

USD/JPY traded near 158.70 on Friday, up 0.61% on the day, rebounding after a sharp fall on Thursday. The move followed a firmer US Dollar after recent volatility and a reassessment of US policy expectations.

The US Dollar was supported by pricing for a longer Federal Reserve pause. The Fed kept rates in the 3.50%–3.75% range, cited elevated uncertainty tied to geopolitical tensions, and fewer officials now expect rate cuts this year.

Federal Reserve Policy Outlook

CME FedWatch readings show markets largely expect rates to stay unchanged through year-end. The US Dollar Index (DXY) also rebounded towards 99.50.

Energy-market stress and Middle East tensions were linked to higher demand for liquidity, which supported the Dollar. Rising oil prices were also associated with further US Dollar support.

In Japan, the Bank of Japan maintained a hawkish stance, which limited pressure on the Yen. Governor Kazuo Ueda said a rate rise remains possible if any slowdown linked to Middle East tensions is temporary.

The BoJ also pointed to uncertainty around growth due to rising energy costs. Geopolitical tensions involving the US, Israel and Iran continued to drive risk aversion, which can support the Yen, though US policy expectations dominated in the near term.

Rate Differentials And Market Positioning

We are seeing the interest rate difference between the US and Japan dictating the direction of USD/JPY, pushing it toward the 159.00 level. The Federal Reserve’s commitment to holding rates firm is the main driver behind the dollar’s strength. This situation suggests that selling any dips in the pair remains a viable strategy for now.

The case for a strong dollar is supported by solid economic data, which we’ve seen consistently over the last year. For instance, the latest non-farm payrolls report for February 2026 showed a robust addition of 250,000 jobs, while core inflation is proving sticky at 3.1%, well above the Fed’s target. This economic resilience gives the Fed no reason to consider cutting rates, which should keep upward pressure on the pair.

On the other side, we must watch the Bank of Japan, which has been signaling a potential hike, a major shift since it ended negative interest rates back in early 2024. Japan’s own core inflation has been holding around 2.2%, giving the central bank justification to finally tighten its policy. This threat of intervention is what is likely preventing a more explosive move above 160.00, a level that triggered intervention in the past.

Given these opposing forces, options traders should consider strategies that benefit from rising volatility. The geopolitical uncertainty in the Middle East, combined with WTI crude oil prices holding firm around $92 a barrel, is creating an unpredictable environment. Buying straddles or strangles could be an effective way to play potential sharp moves in either direction over the next several weeks.

For those with a more patient outlook, the carry trade remains a primary strategy. Holding a long USD/JPY position allows traders to collect the positive swap, or rollover credit, from the wide interest rate gap between the Fed and the BoJ. This provides a steady income stream while waiting for the uptrend to resume.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

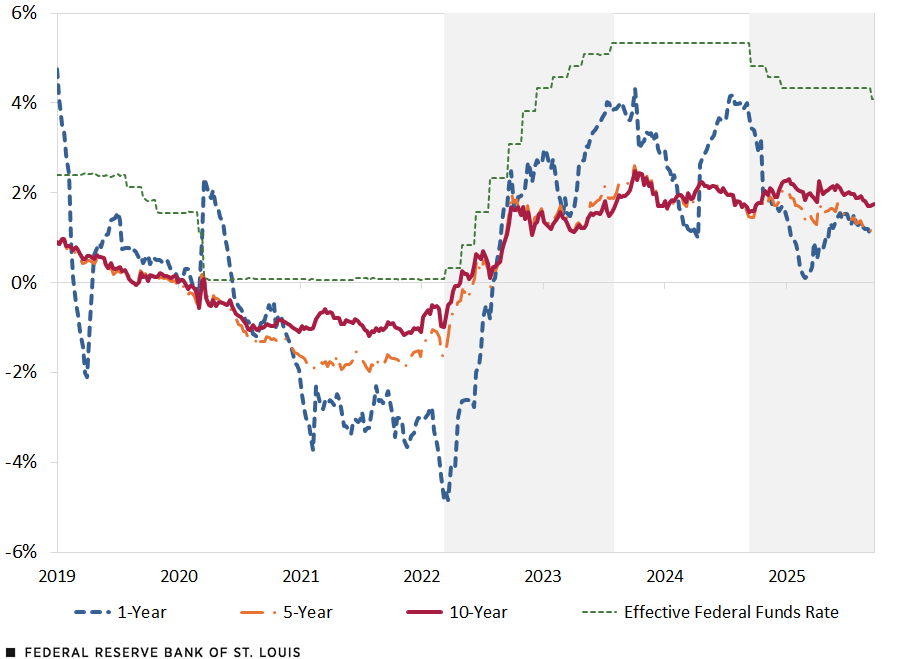

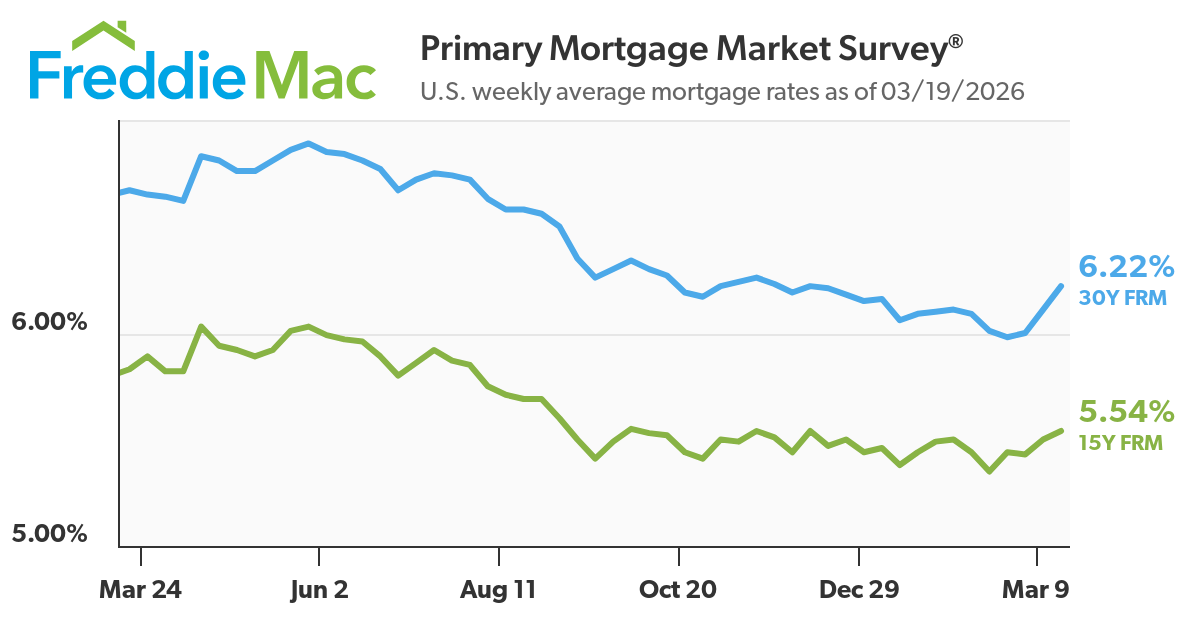

Mortgage rates are primarily driven by US Treasury yields, with the 10-year acting as the key benchmark rather than the Fed’s policy rate.

The Fed’s cautious stance on rate cuts in 2026, amid persistent inflation and energy-driven risks, is keeping long-term yields—and mortgage rates—elevated.

Mortgage rates serve as a leading indicator for financial conditions, influencing housing demand, consumer spending, and broader market sentiment.

The Fed does not set Mortgage Rates

Mortgage rates are often misunderstood as being directly controlled by the Federal Reserve. In practice, the relationship is indirect and mediated through financial markets.

As of early 2026, the average US 30-year fixed mortgage rate has been hovering just above the 6% mark—rising to around 6.1% in mid-March after briefly dipping below 6% in February. This movement did not come from a change in the Fed’s policy rate, which remained on hold, but from shifts in bond yields and market expectations.

Mortgage rates rose for a third week, reaching a three-month high as wartime inflation fears drove up yields for the government bonds that guide home loans https://t.co/p7pXZwdBsL

For traders, this distinction matters. Mortgage rates are not a policy tool, they are a market-derived price of long-term capital, reflecting inflation expectations, growth outlook, and risk premia.

Term premium Investors demand compensation for holding long-duration bonds in uncertain environments.

Market volatility In unstable conditions, lenders widen spreads, increasing mortgage rates beyond what yields alone would suggest.

For traders, this makes the bond market the primary signal to watch. Read about how liquidity affects the movement of bond markets and geopolitical structure here.

Why the Fed Still Matters

The Federal Reserve might not set mortgage rates, but they definitely shape them.

The Fed anchors expectations around inflation, growth, and future policy. Those expectations feed directly into bond markets, particularly the US 10-year Treasury yield, which is the primary benchmark for mortgage pricing.

In 2026, the Fed’s stance has shifted markets away from aggressive easing and toward a more cautious outlook. That shift alone has been enough to keep borrowing costs elevated.

What the Fed is Signalling in 2026

Data-dependent rate cuts The Fed has made it clear that easing will depend on sustained progress in inflation, not forecasts alone.

Persistent inflation concerns Core inflation—especially in services—remains sticky, limiting the scope for rapid rate cuts.

Sensitivity to energy prices Rising oil prices and geopolitical risks are feeding into inflation expectations, keeping pressure on yields.

How This Feeds Into Mortgage Rates

Delayed rate-cut expectations Markets have repriced from multiple cuts to a slower path. This has kept the 10-year yield elevated around ~4.1%–4.3%.

Higher-for-longer narrative Even without hikes, the absence of cuts keeps financial conditions tight and borrowing costs elevated.

Quantitative tightening (QT) The Fed continues to shrink its balance sheet, reducing demand for Treasuries and mortgage-backed securities—pushing yields higher.

What the Data Shows

The US 10-year Treasury yield has remained above 4% in recent weeks

The 30-year fixed mortgage rate has rebounded to around ~6.1% in March, after dipping below 6% in February

The spread between yields and mortgage rates remains elevated, reflecting risk and market volatility

Why This Matters for Markets

Fed tone moves yields—even without action A hawkish shift in communication can push yields higher immediately.

Mortgage rates follow expectations, not decisions Markets price future policy, not current rates.

Housing becomes a transmission channel Higher mortgage rates tighten financial conditions, impacting consumption and growth.

Mortgage Rates as a Macro Signal

Mortgage rates act as a real-time indicator of financial conditions.

When rates rise:

Housing affordability deteriorates Monthly repayments increase significantly. A 1% rise in mortgage rates can increase monthly payments by hundreds of dollars on a standard loan.

Transaction volumes slow Existing home sales and mortgage applications tend to decline.

The “rate lock-in effect” intensifies Homeowners with sub-3% mortgages from prior years are reluctant to sell, tightening supply further.

When rates fall:

Refinancing activity picks up

Homebuyer demand improves

Housing-related sectors stabilise

For instance, earlier in 2026, when rates briefly dipped below 6%, pending home sales saw a modest rebound, highlighting how sensitive housing demand is to even small rate moves.

Sales of newly built homes in January dropped 17.6% month over month to a seasonally adjusted, annualized pace of 587,000 units, according to the U.S. Census Bureau. That is the slowest pace since 2022.

For traders, this links mortgage rates directly to:

consumer confidence

retail spending

cyclical equity sectors

What is Driving Mortgage Rates in 2026

Several macro forces are currently shaping mortgage rate dynamics:

Sticky core inflation Services inflation remains persistent, limiting the Fed’s ability to ease policy aggressively.

Energy market volatility Geopolitical tensions, particularly in the Middle East, have supported oil prices, feeding into inflation expectations and bond yields.

Repricing of Fed expectations Markets have shifted from expecting multiple cuts to a more gradual easing cycle, supporting higher yields.

Structural housing demand Despite higher borrowing costs, demographic demand and limited housing supply are preventing a sharp collapse in the market.

Elevated term premium Investors are demanding higher compensation for holding long-term debt amid fiscal uncertainty and large government issuance.

Together, these forces explain why mortgage rates have remained relatively elevated despite no new rate hikes.

What Traders Should Watch

To anticipate mortgage rate movements, traders should monitor a combination of macro and market indicators:

US 10-year Treasury yield (primary driver) Sustained moves above key levels (e.g., 4.2%–4.5%) typically lead to higher mortgage rates.

Inflation data (CPI, PCE) Upside surprises tend to push yields higher and delay rate cuts.

Federal Reserve communication Shifts in tone, particularly around inflation or labour markets, can quickly reprice expectations.

Housing data releases Mortgage applications, building permits, and home sales provide real-time demand signals.

Oil and energy prices Rising energy costs can feed into inflation expectations, indirectly lifting yields.

Bottom Line

Mortgage rates are best understood as a reflection of the bond market rather than a direct outcome of Federal Reserve policy.

In 2026, the combination of persistent inflation, cautious central bank messaging, and elevated term premiums keeps borrowing costs relatively high. For traders, mortgage rates offer a valuable lens into financial conditions: bridging policy expectations, consumer behaviour, and market sentiment.

Understanding this relationship is key to navigating both housing trends and broader macro-driven market moves.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Trader’s Takeaway

Do mortgage rates follow the Federal Reserve rate?

Not directly. Mortgage rates are more closely tied to long-term Treasury yields, though Fed policy influences those yields through expectations.

Why did mortgage rates rise even when the Fed paused?

Because bond yields increased due to inflation concerns and shifting expectations around future rate cuts.

What spread exists between Treasury yields and mortgage rates?

Typically between 150 and 300 basis points, depending on market conditions and risk factors.

Will mortgage rates fall if the Fed cuts rates?

Not necessarily. Mortgage rates will only decline meaningfully if long-term yields fall, which depends on inflation and growth expectations.

Start trading now – Click here to create your real VT Markets account