The AI trade has spent two years rewarding the loudest names: chip designers, cloud platforms, and data centre builders. Yet one of the more interesting moves in 2026 came from a company better known for bathrooms than semiconductors.

On 22 January, shares in Japan’s TOTO jumped nearly 10% and rose as much as 11% intraday after analysts pointed investors toward its electrostatic chucks, ceramic components used in chipmaking equipment and seen as beneficiaries of tighter memory supply tied to AI infrastructure demand.

What matters here is not that TOTO suddenly became an AI company. It is that part of its business that sits further upstream, in the manufacturing layer, that helps keep semiconductor production running. That is where the market has started to widen its focus—beyond computation and models and into the materials, tools, and specialised components that support the whole buildout.

TOTO’s Key Results: Why Investors Took Notice

TOTO drew market attention not because its bathroom business changed overnight, but because its advanced ceramics segment showed how AI demand can lift smaller upstream suppliers in semiconductor manufacturing.

- In TOTO’s third-quarter FY ending March 2026 materials, advanced ceramics posted ¥47.0 billion in sales, up 37% year on year.

- Operating profit from advanced ceramics rose to ¥20.2 billion, up ¥6.0 billion.

- In its first-half FY ending March 2026 materials, TOTO’s business overview shows New Business Domains at 7% of the sales-mix snapshot, while the company’s reported first-half figures imply a contribution closer to 8.5% of total sales.

- TOTO also said advanced ceramics benefited from stronger electrostatic chuck demand as data-centre-driven semiconductor demand improved.

TOTO’s Inclusion in the AI Conversation

TOTO is now being discussed in AI-related market commentary because part of its business supports chipmaking equipment, placing it inside the upstream semiconductor supply chain.

While they earn most of their money from housing and sanitary products, their advanced ceramics business indicates sales in electrostatic chucks and related components used inside semiconductor manufacturing equipment. It is being re-rated because part of its business sits upstream, where manufacturing bottlenecks can become just as valuable as algorithmic breakthroughs.

In its first-half FY ending March 2026 materials, TOTO said advanced ceramics benefited from stronger electrostatic chuck demand as the semiconductor market improved on data-centre demand, while higher operating levels at manufacturers also supported replacement demand.

How the Market Is Repricing Upstream AI Exposure

This move is less about toilets than it is about how the semiconductor supply chain is tightening under AI demand.

- Memory is being treated as a longer-cycle constraint. Bloomberg reported that Goldman Sachs linked TOTO’s electrostatic chucks to NAND chipmaking and said they should benefit from AI infrastructure buildout, which is tightening both high-end and commodity memory supply.

- Higher fab utilisation supports both new orders and replacement demand. In TOTO’s first-half FY ending March 2026 materials, the company said advanced ceramics benefited from both fresh equipment investment by device makers and high operating levels at manufacturers, which lifted replacement demand as well.

- Memory suppliers are planning for a cycle that lasts longer than a short spike. Reuters reported on 18 March that Samsung wants to move toward three- to five-year contracts with major customers as AI data-centre demand fuels what it called an “unprecedented supercycle.”

- Pricing pressure in memory is spreading beyond chipmakers alone. Gartner said in February that combined DRAM and SSD prices could rise as much as 130% by the end of 2026, showing that memory tightness is becoming a wider market issue rather than a niche supplier story.

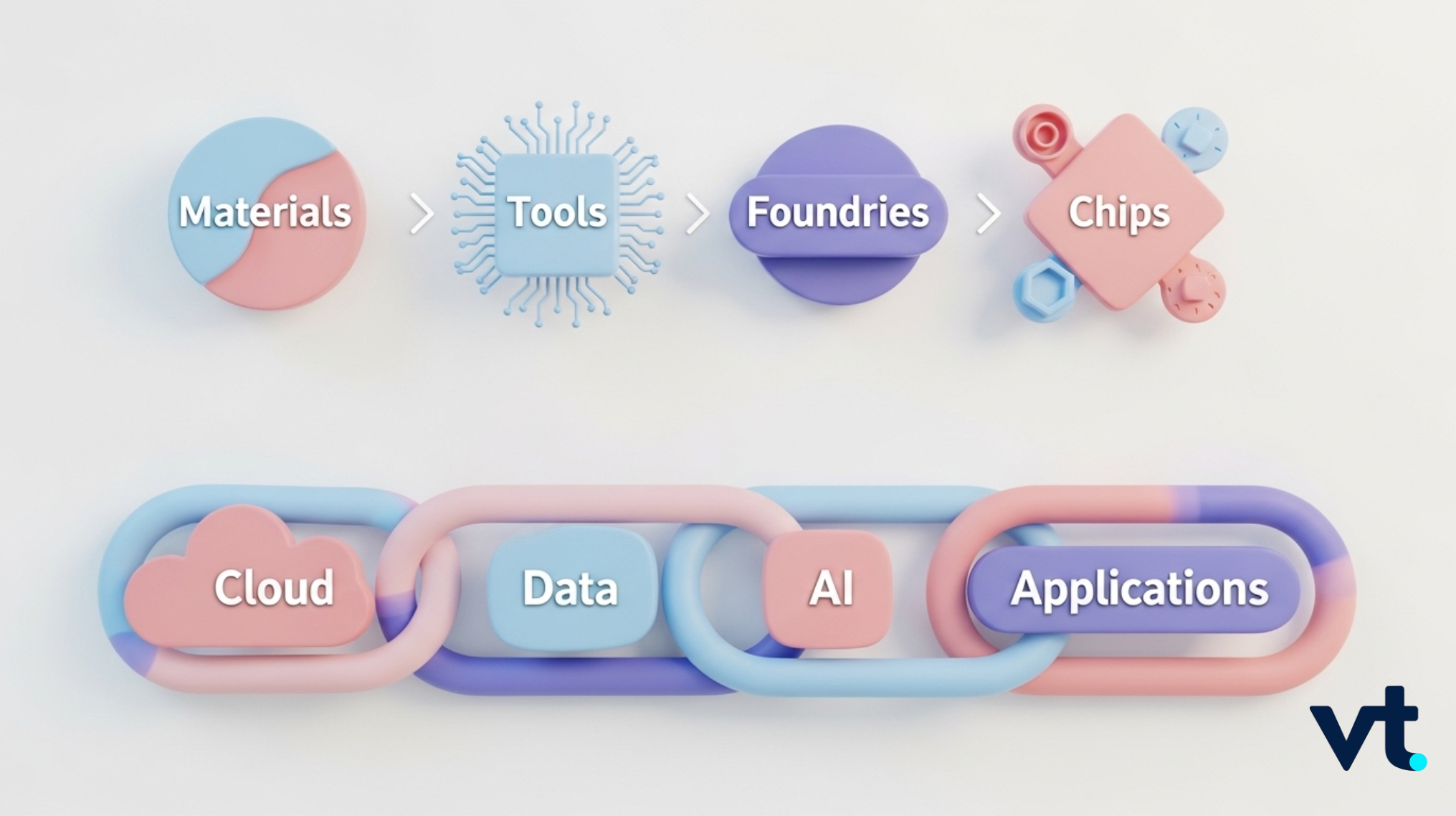

Understanding the Multi-Layered AI Supply Chain

The latest move in TOTO reflects a broader market shift. Investors are looking beyond cloud giants and chip designers to the materials, tools and production systems that support AI hardware demand.

In technical terms, more AI infrastructure means more chips, more chip output means fabs stay busy for longer, and busy fabs need more tools, more replacement cycles and more specialised components inside those tools. TOTO benefits from that last part of the chain.

The AI buildout is creating value across more layers of the market than the first wave of winners suggested.

| Early Layers in the chain | What it does | Names to watch |

| Upstream fab tools / process-enabling equipment | Makes deposition, etch, lithography, inspection, process-control and wafer-handling systems or critical components inside them | AMAT, KLAC, LRCX, ASML, ASM, TOTO |

| Foundry / manufacturing | Manufactures the chips after tool and materials layers are in place | TSM, GFS, UMC |

| Materials / industrial inputs / connectivity | Supplies gases, specialty materials, glass, fibre and packaging-related inputs that keep AI hardware production and data transfer running | APD, Air Liquide, GLW, DD |

Equipment intensity remains elevated because AI capacity still needs to be built. TSMC said in January that it expects 2026 capital spending of $52 billion to $56 billion, reflecting continued investment in advanced semiconductor capacity. At the industry level, SEMI said foundry and logic wafer-fab-equipment sales are expected to keep growing in 2026 as chipmakers add capacity for AI accelerators and high-performance computing.

TOTO sits in the upstream manufacturing layer, though in a more specialised form than the established equipment giants. Its connection to AI comes from the infrastructure used to make semiconductors, not from AI software, cloud applications, or chip design itself.

That places it closer to Applied Materials, KLA, Lam Research, ASML and ASM than to Nvidia-style front-end winners. Its role is smaller and more niche, but niche positions can become highly valuable when demand is strong, capacity is tight, and replacement is not easy.

Trade these available names as CFD Shares at VT Markets.

Under-the-Radar Firms in the AI Supply Chain

TOTO is not alone. A growing number of lesser-known firms are gaining attention because they serve the manufacturing, materials and connectivity layers beneath the better-known AI winners.

Corning (GLW) is adding to the data connectivity spectrum. Having reported in January to have signed a deal in worth up to $6 billion with Meta for fibre-optic cables used in AI data centres, and forecasted stronger sales on optical-fibre demand tied to data-centre and AI infrastructure needs.

Air Liquide is another example supporting industrial inputs. Capitalising on AI-related semicaonductor gas demand, including its purchase of DIG Airgas and a $250 million investment in Idaho to support Micron’s advanced memory lines.

Applied Materials shows what happens when the market already understands the same layer more clearly. Forecasting second-quarter revenue and profit above estimates, with AI chip demand and memory capacity expansions driving sales.

A useful way to think about these names is not ‘surprise AI stock’ versus ‘obvious AI stock’. It is whether the company sits at a point in the stack where demand compounds, lead times matter, and replacement is difficult.

How Your AI Portfolio Stacks Up

As always, caution is advised. Now, with more potential selection and selectivity.

Not every hidden supplier deserves the same AI adoption re-rating. Some companies are directly linked to wafer fabrication; others are loosely adjacent. TOTO’s ceramics arm sits closer to the production bottleneck than a generic industrial name, but that still does not make it a pure semiconductor stock..

When supply chains start pricing in a long expansion, valuations can move ahead of what end demand eventually absorbs. Concerns about overheating in AI investment even as memory demand remains strong.

AI Supply Chain Stocks to Watch

The more useful distinction is not whether a stock looks like a traditional AI winner. It is whether the company sits at a part of the chain where demand compounds, capacity stays tight and substitution is difficult.

Interested in the growing AI supply chain?

Monitor real-time CFD price action of these shares on VT Markets APP.

How are Upstream Chip Manufacturing Important?

AI demand still depends on semiconductor production, and that means fab tools, process systems, specialty materials and replacement cycles remain important parts of the trade. The case for these quieter names is gaining support because the AI buildout is still creating pressure in the physical layers of the supply chain, not only in software or cloud spending.

- AI investment is still translating into production bottlenecks. Demand is continuing to flow through into semiconductor manufacturing, where capacity, process control and equipment availability still matter. Deloitte expects the global semiconductor industry to reach US$975 billion in annual sales in 2026, driven by the AI infrastructure boom.

- Tighter memory and fab capacity are raising the value of upstream suppliers. As chipmakers add capacity for AI accelerators and high-performance computing, the importance of tooling, replacement cycles and specialised components used in wafer production rises with it.

- Smaller specialists are starting to reflect that shift in their numbers. TOTO’s advanced ceramics unit is growing much faster than the group’s housing businesses and is highly profitable relative to its small revenue share.

- Industrial policy is reinforcing the manufacturing backdrop. Japan, which wants domestically made chip sales to rise to ¥40 trillion by 2040 from roughly ¥8 trillion as reported in March.

Taken together, that points to a broader shift in market attention: away from AI demand only at the top of the stack, and toward the supply constraints and specialised manufacturing layers underneath it.

Market Sentiment on the AI Trade

TOTO’s rally suggests the market is beginning to reward scarcity and specialised industrial roles inside the AI chain, not only the loudest names at the top. It is starting to look further upstream, where capacity constraints, specialist tooling and hard-to-replace components can matter just as much.

That shift matters because the next phase of AI trade may depend less on obvious AI exposure and more on where scarcity sits inside the chain. For TOTO, the focus now is whether advanced ceramics can continue outgrowing the rest of the business and whether that niche role in semiconductor manufacturing keeps translating into visible earnings strength.

TOTO may be a narrow expression of the theme, but narrow can still be powerful when demand is strong and substitution is difficult. That is what makes this more than a one-day surprise rally.

Key Definitions in the Upstream AI Supply Chain

What is the upstream AI supply chain?

The upstream AI supply chain refers to the materials, tools, components and fabrication systems needed to produce semiconductors before they reach cloud platforms, AI models or end-user applications.

What are electrostatic chucks?

Electrostatic chucks are specialised components used in semiconductor manufacturing equipment to hold wafers securely during processing. They are part of the infrastructure used inside chip fabrication plants.

What is fab utilisation?

Fab utilisation refers to how fully a semiconductor fabrication plant is being used. Higher fab utilisation usually means stronger production activity, which can increase demand for replacement parts, maintenance and tool-related components.

What is equipment intensity in chip manufacturing?

Equipment intensity refers to how much specialised manufacturing equipment is needed to produce semiconductors at a certain scale or level of complexity. Higher equipment intensity often supports demand for tool makers and their supply chains.

What is a bottleneck supplier?

A bottleneck supplier is a company that provides a hard-to-replace material, component or tool in a production chain. These suppliers can become more valuable when demand rises and alternatives are limited.

Start trading now – Click here to create your real VT Markets account