WTI oil rises to $61.24, while Brent remains steady at $64.58 at the start of the European session

West Texas Intermediate (WTI) Oil prices rose in early European trading, reaching $61.24 per barrel, up from Friday’s close of $60.70. In contrast, Brent crude remained steady at about $64.58.

WTI Oil is a high-quality type of crude oil known for its low gravity and sulfur content, making it easy to refine. It is produced in the United States and distributed through the Cushing hub, a key benchmark in the oil market that is often cited in news reports.

In October, Turkey’s year-on-year consumer price index was unexpectedly low at 32.87%

Turkey’s Consumer Price Index (CPI) for October increased by 32.87% compared to last year. This is slightly lower than the expected 33.2%, showing a small but important shift in inflation trends.

In economic news, trade tensions may be affecting China’s growth, according to Standard Chartered. Meanwhile, the US Dollar Index (DXY) remains just under the 100.00 mark, which many see as an important psychological level.

Currency Market Movements

The EUR/USD exchange rate is close to a three-month low, as the US Dollar stays strong. Gold prices are having difficulty rising, despite a brief increase during the day, largely due to the Federal Reserve’s strict policies that support a strong USD. In currency trading, the AUD/USD pair has climbed to about 0.6550 ahead of announcements from the Reserve Bank of Australia (RBA). In the stock markets, Dow Jones Futures show some stability amid ongoing US-China tech access tensions. FXStreet reminds us that financial markets can be unpredictable and that investments come with risks. It’s important for readers to do their own research since the information shared may not be entirely accurate. Investments can lead to risks, including potential losses. Market tension is quite high, with Gold surpassing $4,000 and the US Dollar Index staying firm below 100. This movement to safer assets is driven by renewed fears over US-China trade. Derivative traders should prepare for increased volatility, as the CBOE Volatility Index (VIX) has jumped over 15% this past month, trading above 22.Strategic Financial Moves

The US Dollar Index is testing the key 100 level. If it breaks above, it could lead to further selling in pairs like EUR/USD, which is already close to three-month lows. Given the Federal Reserve’s strict policies, it may be wise to buy call options on the dollar or put options on the Euro in the coming weeks. We saw the dollar gain strength in late 2022, when the Fed was raising rates aggressively. The renewed fear of limiting China’s access to NVIDIA technology puts pressure on the entire semiconductor sector. It might be a good idea to buy protective put options on tech-focused indices like the Nasdaq 100 or on individual stocks like NVIDIA. This strategy provides some protection against unexpected geopolitical news. Turkey’s inflation of 32.87%, though slightly lower than expected, still presents a significant challenge for the Lira. The Central Bank of the Republic of Turkey (CBRT) kept its policy rate at 50% in October, underlining its ongoing battle with inflation. This environment is primed for volatility, making long straddles on the USD/TRY pair a potential way to profit from sharp price movements. As Gold futures exceed the $4,000 per ounce threshold, the demand for safe assets is clear. Open interest in gold call options has increased by 25% over the past quarter, showing strong bullish sentiment from traders. We should consider using pullbacks to enter long positions through futures contracts or by selling out-of-the-money put options to earn premiums while remaining bullish. Create your live VT Markets account and start trading now.EUR/JPY stays strong above 177.50 as JPY weakens amid Japan’s holiday trading lull

Data Dependent Approach

Francois Villeroy, a policymaker at the European Central Bank, emphasized the need for a flexible approach to manage various financial risks by relying on data and forecasts. ECB Governor Martins Kazaks warned against overreacting to inflation and growth risks in the Eurozone. Today, the Euro gained value against major currencies, especially the British Pound. The heat map below shows the percentage changes between these currencies, with the base currency listed in the left column and the quote currency in the top row. For instance, the Euro has strengthened by 0.08% against the Japanese Yen. This information is for informational purposes only and should not be considered financial advice, as market investments involve risks. The EUR/JPY pair remains stable near 177.70, highlighting a clear difference in policies between central banks. The European Central Bank takes a data-driven approach, while the Bank of Japan is cautious about making significant policy changes. This fundamental difference will likely influence the market in the upcoming weeks. Despite Japan’s core inflation staying above the 2% target for over a year, last noted at 2.7% in October 2025, the Bank of Japan has kept its policy rate around 0.1%. Speculation about the new Prime Minister pushing for more fiscal stimulus further complicates the likelihood of major rate hikes. This suggests continued pressure on the Yen, as monetary policy is unlikely to provide support.Strategic Opportunities in the Market

In contrast, the Eurozone’s key interest rate stands at 3.75%, creating a favorable interest rate gap for traders. With Eurozone inflation currently at 2.5%, above the target, the ECB is unlikely to consider rate cuts anytime soon. This situation strengthens the Euro against the Yen and boosts the attractiveness of the carry trade. Given this context, it is smart to consider strategies that could benefit from a future rise in EUR/JPY. Buying call options on the pair is a way to capture potential gains while managing risk, especially with uncertainty surrounding the BoJ’s December meeting. Implied volatility may increase as this date approaches, making it a good time to examine option pricing. Looking back, this upward trend is not new; the pair has climbed from the 170 level in late 2024 and below 150 in 2023. This long-term upward trend supports the idea that any dips are likely to be seen as buying opportunities. The path of least resistance seems to be upward for the near future. Create your live VT Markets account and start trading now.USD/CHF remains steady near 0.8050 ahead of Swiss inflation data, supported by USD gains

**Federal Reserve Impact**

Right now, the US Dollar Index is at about 99.85. Over the past week, the US Dollar has gained 0.24% against the Australian Dollar, but it’s lost value against several other currencies: 0.02% against the Canadian Dollar, 0.76% against the Japanese Yen, 1.36% against the British Pound, and 1.01% against the Swiss Franc.

Discussions at the Federal Reserve about inflation have changed expectations regarding future interest rates after a 25 basis point cut last Wednesday. Fed Chair Jerome Powell said it is unlikely that there will be another rate cut in December. The chance of a December rate cut has decreased from 91.7% to 69.3%.

Focus will be on the US ISM Manufacturing PMI for October, which is expected to rise to 49.2 from 49.1. The Swiss Franc is stable ahead of the Swiss CPI data for October. Swiss monthly inflation is projected to drop to 0.1%, but annual inflation is expected to rise to 0.3%. The next Swiss CPI report will be released on November 3, 2025.

**US Dollar Strength**

The US Dollar is getting stronger because the Federal Reserve indicated that another interest rate cut in December is unlikely. The probability of a cut has quickly fallen from over 90% to below 70%. This change is pushing the USD/CHF currency pair higher.

Recent Swiss inflation data came in lower than expected at -0.2% for the month. This marks three months of decline, keeping the annual rate slightly positive at 0.3%, which is well below the Swiss National Bank’s target. Without rising inflation, the SNB has no reason to strengthen the Franc, making it vulnerable against a robust Dollar.

Economic data from the US suggests it is holding strong, supporting the Fed’s cautious approach. Last week’s final Q3 GDP figures showed the economy grew at an annualized rate of 2.3%, surpassing early estimates. This indicates that the slowdown prompting the October rate cut might be less severe than anticipated. This is in stark contrast to Switzerland’s sluggish growth and disinflationary pressures.

We’ve seen this divergence before, especially in 2022 when the Fed’s aggressive rate hikes pushed the USD/CHF above parity. While the circumstances are different now, the principle of differing policies influencing the currency pair remains.

For traders, this signals an opportunity to bet on further strength in USD/CHF in the coming weeks. Implied volatility has risen, with one-month options showing greater potential price swings. This makes strategies like buying call options appealing to take advantage of upward momentum. A move toward the 0.8200 psychological level appears possible if US economic data continues to stay strong.

Create your live VT Markets account and start trading now.

GBP/USD faces downward pressure as the Pound loses ground against the US Dollar below 1.3150.

The Pound Sterling (GBP) has been falling against the US Dollar (USD), with the GBP/USD briefly dropping below 1.3150. This shift is mainly due to expectations surrounding a US-China trade agreement and the anticipated dovish announcements from the US Federal Reserve.

Recent progress in the US-China trade talks, particularly regarding export controls and shipping levies, has also impacted the market. On October 24, the US Bureau of Labor Statistics reported that the Consumer Price Index rose by 0.3% in September, bringing the annual inflation rate from 2.9% to 3%. This figure was lower than the expected 3.1%.

Bearish Trend Continues

The GBP/USD pair remains weak, close to its lowest level since April 14, indicating a continued bearish trend. Federal Reserve Chair Jerome Powell’s recent comments about not expecting an interest rate cut in December have further bolstered the USD, despite concerns about economic risks linked to a potential US government shutdown. It’s notable that the pound was trading above 1.3100 not long ago, as market dynamics have shifted dramatically since then. Currently, GBP/USD is struggling to maintain the 1.2450 level, signaling a clear long-term downtrend. The previous focus on a US-China trade deal has now shifted to persistent inflation issues on both sides of the Atlantic. The current main factor affecting the market is the differing inflation rates. The latest data from the US Bureau of Labor Statistics shows that annual inflation has eased to 2.8%, approaching the Federal Reserve’s target. In contrast, data from the UK’s Office for National Statistics shows inflation stubbornly high at 3.5%, leading the Bank of England to adopt a stricter policy.Policy Gap and Market Strategy

This gap in policy is crucial for our strategy in the upcoming weeks. The Bank of England is likely to keep its base rate at 5.0% well into the new year to tackle price pressures. Meanwhile, the market is considering that the US Federal Reserve may start cutting rates by the second quarter of 2026, a significant shift from its previous hawkish stance. With this in mind, we should rethink our bearish positions on the pound. The UK’s interest rate advantage over the US could create a support level for GBP/USD, limiting further declines. Derivative traders might consider buying call options to prepare for a possible rebound, as the pound could strengthen if the Fed makes more explicit signals about rate cuts. Implied volatility for GBP/USD options has been decreasing, making them relatively inexpensive to buy. This situation offers an opportunity to create low-cost trades that could benefit from a recovery or stabilization above the 1.2400 level. We are looking at longer-dated call spreads to take advantage of a potential gradual increase through the first quarter of next year. Create your live VT Markets account and start trading now.Amid uncertainties about the BoJ, GBP/JPY stabilizes around the mid-202.00s with limited gains.

The GBP/JPY exchange rate has stabilized in the mid-202.00s after a brief dip during the Asian session. This change happened as uncertainty surrounding the Bank of Japan (BoJ) helped support the Japanese Yen (JPY). However, potential gains for the British Pound (GBP) are limited due to ongoing fiscal concerns in the UK and speculation about possible rate cuts from the Bank of England (BoE).

The exchange rate is currently trading in a narrow range due to Japan’s holiday, along with minimal movement in spot prices. The JPY remains under pressure from doubts about BoJ’s potential rate hikes, and there may be intervention if the Yen weakens further. In the UK, concerns over fiscal health and the likelihood of BoE rate cuts discourage strong bullish positions on the GBP.

Cautious Anticipation Ahead

As we look ahead, there is cautious anticipation for the BoE’s policy announcement. There’s about a one-third chance of a 25 basis points cut. This expectation arises from declining inflation and rising unemployment, which suggest a need for a rate cut. Even though economic conditions are creating pressure to sell GBP/JPY on any upticks, the actual outcome will depend on the upcoming signals from the BoE this week. Recent trends show the JPY has strengthened against the British Pound this past week, reflecting the complex dynamics of currency markets and global fiscal policies. With GBP/JPY hovering in the mid-202.00s, we find ourselves in a classic standoff ahead of a critical central bank decision. Traders should focus on the BoE’s policy update this Thursday, November 6th. The uncertainty about a potential rate cut adds significant short-term risk. There is an increasing case for a BoE rate cut, which could put pressure on the Pound. Recent UK inflation data from October shows the headline rate dropped to 2.1%, only slightly above the central bank’s target and far from the highs witnessed in 2023. Coupled with slowing wage growth, this provides the BoE a reason to ease policies and help the struggling economy.Yen’s Weakness Driven By BoJ Reluctance

Conversely, the weakness of the Japanese Yen stems from the BoJ’s hesitance to commit to further rate hikes. Even though core inflation in Japan has remained above 2% for over a year, officials are worried about harming a fragile recovery. However, we can’t ignore the possibility of currency intervention from the Ministry of Finance, especially since the exchange rate is at levels last seen in 2008. In light of these dynamics, traders might consider using options to manage the expected volatility from the BoE meeting. Implied volatility on short-term GBP/JPY options has likely risen, making strategies like selling call spreads appealing for those who think the pair’s potential upside is limited. This approach allows traders to profit if the exchange rate stays below a certain level, minimizing risk while generating premium income. Looking further into November, the UK’s fiscal situation will be the next major factor to watch. Finance Minister Rachel Reeves is set to present the Autumn budget on November 26. With the UK’s debt-to-GDP ratio exceeding 100%, any indication of unfunded spending could lead to a negative market reaction for the Pound. The bond market turmoil following the 2022 mini-budget remains fresh in traders’ minds, so they will be very alert to any similar signs. Create your live VT Markets account and start trading now.Week Ahead: Trade Truce Sets The Tone

Financial markets are heading into the new week with more hesitation than conviction.

The Federal Reserve’s late-October update shifted the landscape. A December rate cut is no longer seen as a done deal.

Chair Jerome Powell reiterated that policy decisions will remain data-dependent, yet with a federal government shutdown halting much of the data flow, the Fed is effectively ‘driving through fog’. Traders, in turn, are rethinking how quickly monetary easing might resume.

The outcome so far? A mixed dollar, cautious equity markets, and investors taking refuge in safe-haven assets until clearer signals emerge.

The Fog Before The Cut

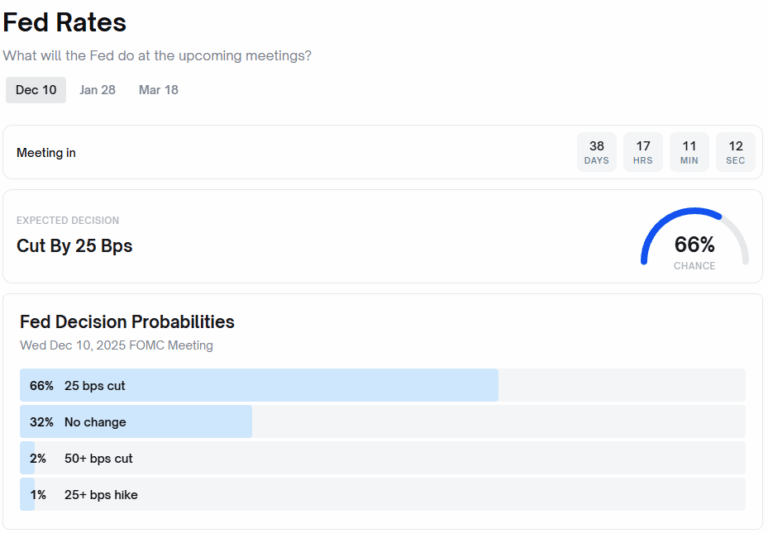

Before the Fed’s October meeting, futures markets were nearly unanimous in predicting a rate cut in December.

But Powell’s cautious tone has flipped the sentiment. According to the CME FedWatch Tool, the odds of a cut have tumbled from roughly 90% to around 63%, while Polymarket data suggests a 66% probability of a 25-basis-point reduction and a 32% chance of no change.

In short, the market still sees easing ahead. It just no longer trusts it will come smoothly.

The shift reflects Powell’s warning about divisions within the Fed and the impact of the data blackout due to the government shutdown.

Without updated figures, policymakers are essentially flying blind, and traders are hedging both sides of the trade to manage risk.

Options markets point to growing volatility pricing, suggesting investors expect a slower, bumpier approach to policy easing rather than a straightforward rate-cut trajectory.

A Case For Patience

If inflation continues its downward path, the Fed will have the justification to cut rates, but not necessarily the urgency.

September’s CPI rose 3.0% year-on-year, slightly up from 2.9%, largely due to higher energy costs. Yet beneath the surface, inflation pressures are easing:

– Core CPI stayed at 0.3% month-on-month, in line with a gradual cooling trend.

– The shelter component, the biggest driver of inflation, dropped to 0.16% m/m, its lowest level in more than a year.

– Over 51% of CPI categories are now in outright decline from their peaks, well above the long-term average of 32%.

Such broad-based disinflation indicates that the inflation battle is mostly won.

While Fed staff still forecast core PCE to end the year near 3%, the broader trend in price pressures looks decisively softer.

The key takeaway? Inflation is falling sharply. Yet the Fed remains cautious about cutting rates too soon and risking a policy reversal if prices reaccelerate.

From Euphoria To Hesitation

The market’s behaviour after Powell’s press conference told its own story.

– US equities retreated from recent highs as traders priced in fewer cuts and slower growth prospects.

– The US Dollar Index (USDX) climbed back toward the 99.00–100.00 zone, signalling a defensive shift.

– Gold stalled around $2,070, caught between softer inflation data and a firmer dollar.

– Bond yields drifted lower, though not enough to reignite a sustained equity rally.

Prediction platforms such as Polymarket reflect this sentiment, showing a notable drop in confidence. It’s still leaning dovish, but with heavy hedging across asset classes.

Over $9 million has now been wagered on the Fed’s December decision, underscoring how pivotal it is to global positioning and risk sentiment.

Cautious Easing On The Horizon

The next move may depend less on a single economic print and more on how long the uncertainty lingers.

If the government shutdown stretches into mid-November, as betting markets imply, the Fed could enter December with limited data visibility.

That scenario favours a 25-basis-point cut as the most likely outcome, but with low conviction.

In essence, the market faces a split narrative:

– Macroeconomic indicators justify a cut.

– Policy caution urges delay.

– And risk assets remain directionless in the meantime.

Market Movements Of The Week

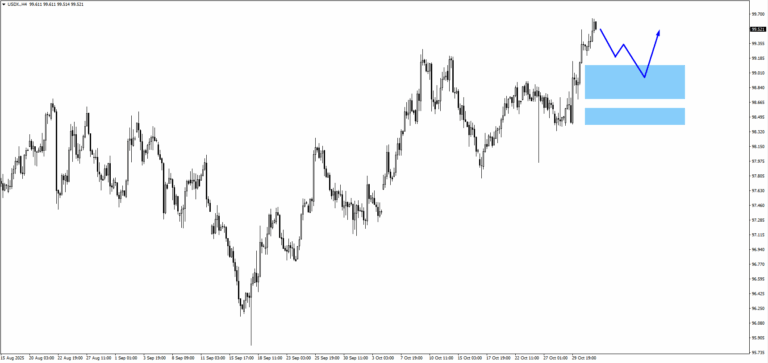

USDX (Dollar Index)

– Still supported by reduced rate-cut certainty, consolidation near 99.00.

– Watch 98.50 as short-term support, resistance at 100.20.

– Break above 100 could extend toward 100.75, reversal signals near 98.50.

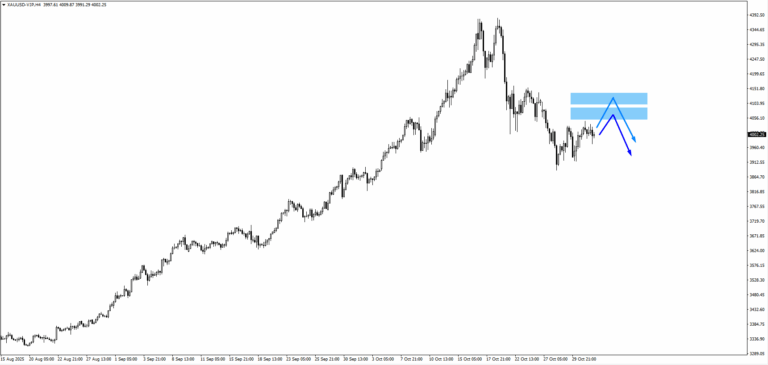

Gold (XAUUSD)

– Stalled around $4,070 as traders balance cooling inflation with firmer yields.

– Resistance at $4,120, support near $3,930.

– Range-bound until a clearer Fed direction.

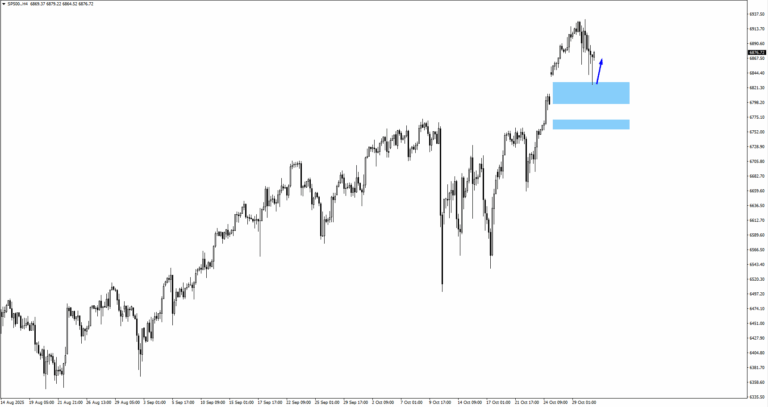

SP500

– Pulled back after testing 6,950 as caution dominates.

– 6,750 support remains critical. 7,000 psychological barrier caps upside.

– Sensitive to shifts in rate-cut probabilities and shutdown headlines.

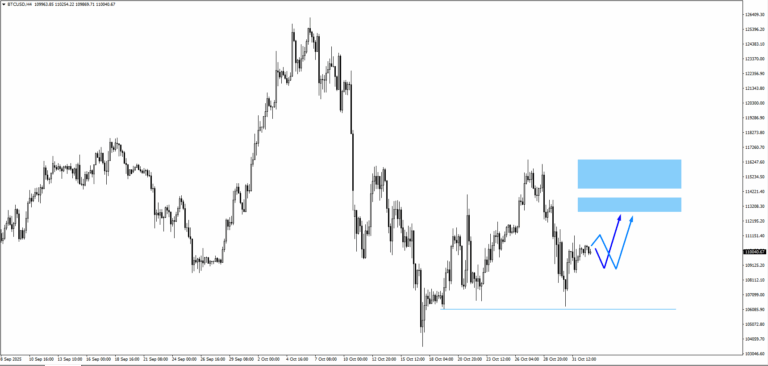

BTCUSD

– Consolidating above 106,000. Upside targets 112,800–114,650 if risk stabilises.

– Break below 106,000 exposes 103,500.

– Volatility may pick up as liquidity thins into mid-month.

Market Snapshot

Markets have shifted from confidence to caution following Powell’s recent remarks, which underscored the Federal Reserve’s data-dependent stance.

Although inflation continues to ease across key sectors, the path forward for policy remains uncertain. Traders are now positioning for a possible rate cut in December, but with no clear signal from the Fed, the U.S. dollar has held steady and broader risk sentiment remains subdued.

Here are the FX option expiries for the New York cut on November 3 at 10:00 AM Eastern Time.

On November 3rd, foreign exchange option expiries at the New York cut, which occurs at 10:00 AM Eastern Time, have been recorded.

For EUR/USD, the options are set at:

– **1.1400** with **686 million euros**

– **1.1450** with **772 million euros**

USD/JPY Option Expiries

In the USD/JPY market, the options include: – **1.1 billion USD** at **150.00** – **385 million USD** at **151.50** – **401 million USD** at **152.50** In the GBP/USD market, options are positioned at: – **1.3100** for **468 million GBP** – **1.3350** for **372 million GBP** For AUD/USD, an option is noted at: – **0.6600** with **338 million AUD** EUR/GBP options have a set point at: – **0.8775** with a value of **300 million euros** We’re seeing large option expiries in EUR/USD at 1.1400 and 1.1450, which will likely influence price movements today. The euro’s strength reflects a growing policy gap, as recent US job data shows hiring slowed to **150,000 in October**. This suggests the Federal Reserve might cut rates sooner than the European Central Bank. The latest Eurozone inflation report indicates a steady **2.5%** annual figure, which supports the view that the ECB will proceed cautiously for a longer time. The significant **$1.1 billion** expiry at **150.00** in USD/JPY signals that this zone is still crucial, akin to its role during intervention periods in **2022 and 2023**. Despite the Bank of Japan ending its negative interest rate policy earlier this year, the ongoing rate gap with the US fuels carry trades. Traders should prepare for volatility but be careful of official remarks, as this level often triggers actions from the Ministry of Finance.GBP/USD Market Trends

In the GBP/USD market, the significant options at **1.3100** and **1.3350** indicate a belief in ongoing dollar weakness and relative strength in the pound. The Bank of England is still dealing with stubborn inflation in the service sector, an issue that has lingered since inflation peaked at **11.1%** in late **2022**. This ongoing price pressure keeps the BoE more hawkish than the Fed, supporting a bullish outlook for the pound in the coming weeks. Traders should focus on these large expiry levels as key pivot points for the next few weeks, as they highlight areas of significant interest. With different themes from central banks, buying volatility through strategies like straddles or strangles may be beneficial before upcoming inflation reports. These option barriers indicate where many positions could be either defended or unwound, leading to localized price fluctuations. The AUD/USD expiry at **0.6600** suggests a more stable sentiment, with the pair stuck between a weaker US dollar and ongoing uncertainties in China’s economy. Recent manufacturing PMI data from China remains just above the **50-point** mark, failing to indicate a strong recovery and limiting the Aussie’s upside. Meanwhile, the EUR/GBP option at **0.8775** suggests a phase of consolidation, as both the UK and Eurozone tackle similar, though slowly easing, inflation challenges. Create your live VT Markets account and start trading now.US Dollar Index rises above 99.50 during Asian trading amid Fed’s hawkish stance

The US Dollar Index (DXY), which tracks the USD against six other currencies, is trading around 99.75 in early Monday Asian hours. This increase is due to a tough stance from the US Federal Reserve, as traders await the upcoming October ISM Manufacturing PMI report.

The Federal Reserve has recently cut interest rates by 25 basis points, but they hinted that this might be the last cut of the year. This choice comes from a desire to better understand the economy before making further rate adjustments.

Impact of Federal Reserve Officials’ Comments

Comments from Federal Reserve officials, such as Dallas Fed President Lorie Logan and Cleveland Fed President Beth Hammack, who were against the rate cut, have helped strengthen the USD. The market’s expectation for a December rate cut has dropped to 68%, down from 93% the previous week. The ongoing US government shutdown is now in its sixth week and may push the DXY lower. The US Dollar is the official currency of the United States and is widely used around the world. It makes up 88% of global foreign exchange transactions, averaging $6.6 trillion daily as of 2022. Its value is influenced by economic indicators and Federal Reserve policies. A year or two ago, the US Dollar Index rose above 99.50 when the Federal Reserve suggested they might pause rate cuts. On November 3, 2025, the situation is different, with the DXY steady around 106.30. This reflects a period of strong dollar performance, supported by high interest rates in 2024. Back then, officials’ tough stance on inflation was clear. The latest Core PCE for September 2025 is at 2.8%, still above the Fed’s target. With unemployment rising to 4.2% in the latest report, the Fed faces pressure to keep rates steady for now.How Treasury Yields Affect the Dollar

This creates uncertainty regarding the Fed’s next steps, unlike late 2023 when the market focused on rate cut timing. For traders in derivatives, this environment suggests strategies that take advantage of volatility. Major data releases could lead to sharp changes in the dollar. Options strategies like straddles or strangles on major currency pairs such as EUR/USD could be effective in this uncertain climate. The yield on the 10-year US Treasury note is around 4.5%, significantly higher than German or Japanese government bonds. This yield difference supports the dollar, making it risky to oppose it for a long time. Traders should closely watch these spreads, as any narrowing might indicate a change in market direction. We must also consider risks, like the government shutdown concerns when the dollar was under 100. Although that issue has been resolved, renewed debates about the US debt ceiling are expected in early 2026. Any signs of political deadlock could weaken dollar strength, creating quick selling opportunities. Create your live VT Markets account and start trading now.Core inflation in Indonesia increased to 2.36% year-on-year, up from 2.19% previously.

In October, Indonesia’s core inflation rose to 2.36% year-on-year, up from 2.19% the previous month.

This increase signals a shift in the country’s economy, suggesting that market factors are influencing consumer prices.